however lags well behind the hype, amongst practitioners, policy makers and industry commentators alike. ‘Blockchain’ technology seems to promise major change for capital markets and other financial services – some say it may ultimately prove to be as important an innovation as the internet itself – but few can say exactly how or why. Michael Mainelli, Alistair Milne (2016) The Impact and Potential of Blockchain on the Securities Transaction Lifecycle http://ssrn.com/abstract=2777404 Ferdinando Ametrano 2017 3/55

1. Cryptography 2. Distributed systems (networking and data transmission) 3. Game theory 4. Economic and monetary theory Mainly not a technology, a cultural paradigm shift instead Ferdinando Ametrano 2017 4/55

or organization • Instantaneous peer-to-peer transactions • No need for trusted third party • Cryptographic security • Synergic economic incentives • Efficient low-cost banking for everybody everywhere https://bitcoin.org/en/faq http://www.coindesk.com/information/ Ferdinando Ametrano 2017 5/55

cost • Why pay a fee to move bytes representing wealth? • Why only 9-5, Monday-Friday, two days settlement? • Who (and when) will gift humanity with a global instantaneous free p2p payment network? BANK Ferdinando Ametrano 2017 6/55

no regulator • Censorship resistant: no frozen funds • Open-access: no discrimination, no amount limits, 24/7, 365 days • Free: negligible transaction costs • Borderless: no geographic limits • Transnational: no specific jurisdiction applies • Secure: non falsifiable, non repudiable transactions • Resilient: nothing has been able to stop it or break it Ferdinando Ametrano 2017 7/55

means has been possible for decades • In digital cash schemes, a single digital token, being just a file that can be duplicated, can be spent twice • A centralized trusted party has always been required to prevent double spending Ferdinando Ametrano 2017 10/55

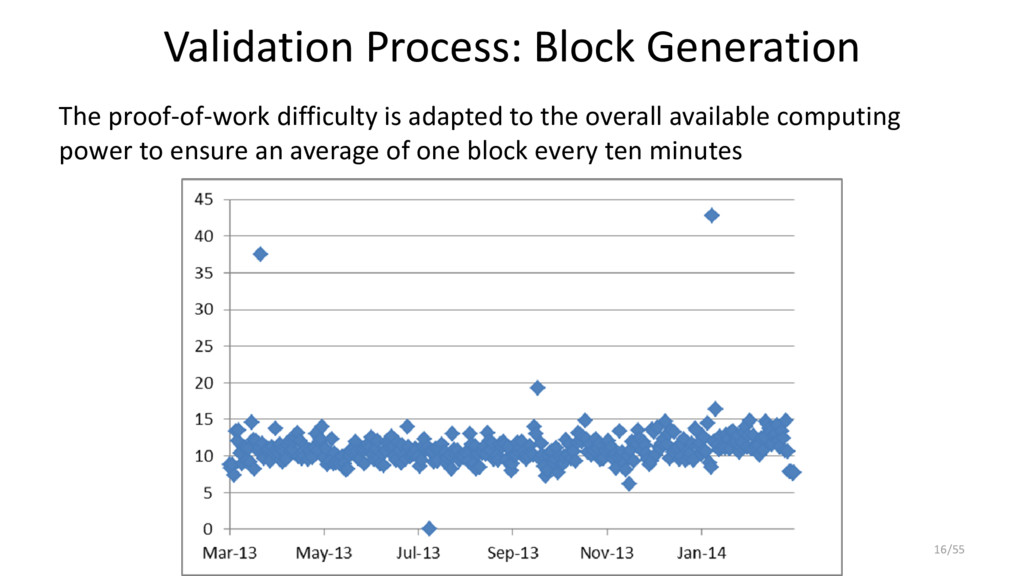

• Transactions are cleared in blocks, thus a blockchain: the nodes providing computational power for clearing are called miners • Miners compete to validate a new block of transactions: the winner providing proof-of-work is rewarded with the issue of new bitcoins in a special coinbase transaction included in the block • Miners solve the double spending problem: – conflicting transactions spending the same coins would invalidate the block – an invalid block would be rejected from the network – the bitcoin reward would be removed from transaction history – miner would have wasted his work Ferdinando Ametrano 2017 11/55

transaction history? • Consensus in an asynchronous network with faulty (or malicious) nodes is proved to be impossible • A problem known as Byzantine General Problem Ferdinando Ametrano 2017 12/55

using (game theory) economic incentive for the mining nodes to be honest. Bitcoin – solves double spending without a central trusted party – can resist attacks of malicious agents, as long as they do not control network majority • Miners are compensated for their proof-of-work using seigniorage revenues, i.e. with issuance of new bitcoins • Seigniorage revenues subsidize the network, making transaction almost free Ferdinando Ametrano 2017 13/55

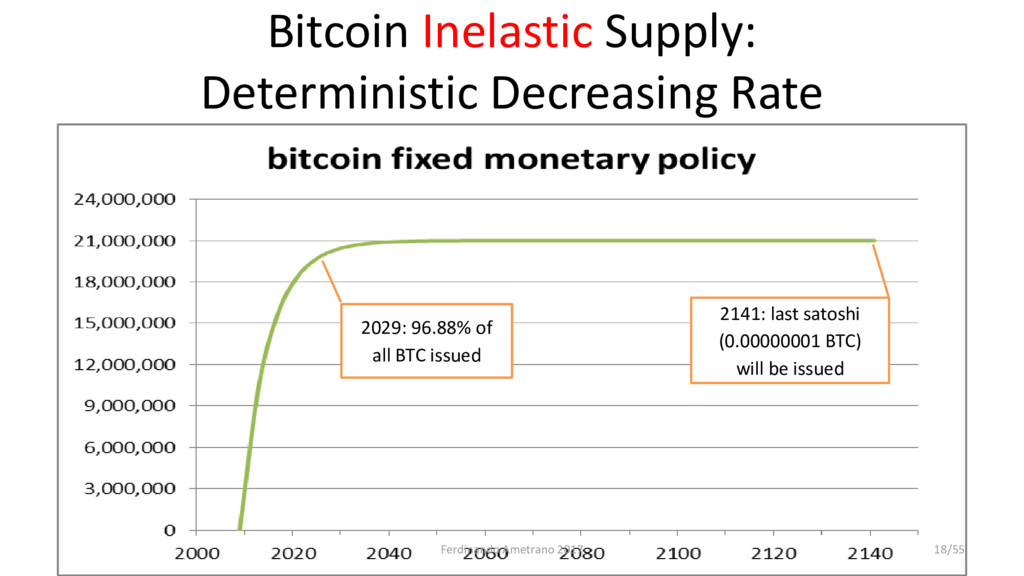

minutes –halving every 4Y • This is the only way new bitcoins are released • It is called mining because of its similarity with the progressive scarcity of gold extraction • Supply free of discretionary intervention Ferdinando Ametrano 2017 17/55

Gradually switch over to a fee-based system: as block space is limited, market is already requiring a growing satoshi/byte fee to be included into a block • Switch to a different paradigm? We have about 120 years to come up with a solution Ferdinando Ametrano 2017 19/55

exists as validated transaction • Asset, not liability • Bearer instrument • It can be transferred but not duplicated (i.e. it can be spent, but not double-spent) • Scarce in digital realm, as nothing else before • Mimicking gold monetary policy • More a crypto-commodity then a cryptocurrency Bitcoin is digital gold this is the brilliant groundbreaking achievement by Satoshi Nakamoto Ferdinando Ametrano 2017 20/55

the commodity money standard – scarce – pleasant color, i.e. resistant to corrosion and oxidation – high malleability – relative easiness of its purity assessment • Gold purity certification • Representative money • Fractional receipt money • Fiat money and legal tender Ferdinando Ametrano 2017 21/55

born into a gift economy 2. Enlarged relationship circle requires exchange economy 3. Barter economy: coincidence of wants 4. Trade economy: money as medium of exchange 5. Global information economy: supranational digital money Ferdinando Ametrano 2017 22/55

coinage is an almost uninterrupted story of debasements; history is largely a history of inflation engineered by governments for their gain • why government monopoly of the provision of money is regarded as indispensable? It deprived public of the opportunity to discover and use a better reliable money Blessed will be the day when it will no longer be from the benevolence of the government that we expect good money but from the regard of the banks for their own interest A Free-Market Monetary System, Gold and Monetary Conference, New Orleans, Nov. 1977, https://mises.org/daily/3204 Hayek, F. A., Denationalisation of Money, The Institute of Economic Affairs, http://www.mises.org/books/denationalisation.pdf Ferdinando Ametrano 2017 23/55

no barrier to enter, no editorial control –Email has not been designed by a consortium of postal agencies –Internet has not been developed by a consortium of telcos • Will a decentralized transactional economy be shaped by a consortium of banks? Ferdinando Ametrano 2017 24/55

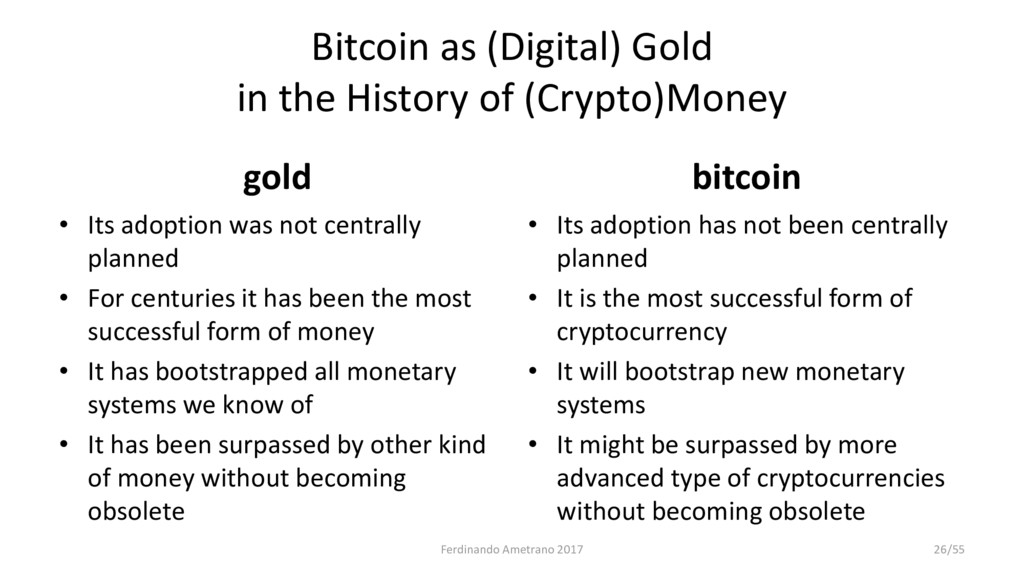

• Its adoption was not centrally planned • For centuries it has been the most successful form of money • It has bootstrapped all monetary systems we know of • It has been surpassed by other kind of money without becoming obsolete bitcoin • Its adoption has not been centrally planned • It is the most successful form of cryptocurrency • It will bootstrap new monetary systems • It might be surpassed by more advanced type of cryptocurrencies without becoming obsolete Ferdinando Ametrano 2017 26/55

unit of account against which the value of every other good is measured • The price system measures the value of goods relative to the value of money Good money should provide stable prices to best perform its role as unit of account Ferdinando Ametrano 2017 28/55

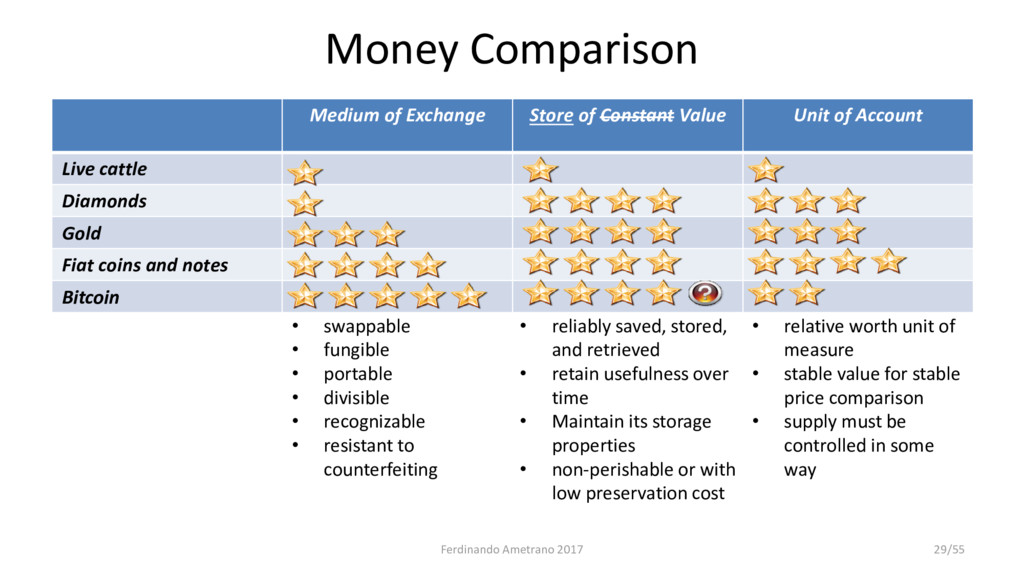

of Account Live cattle Diamonds Gold Fiat coins and notes Bitcoin • swappable • fungible • portable • divisible • recognizable • resistant to counterfeiting • reliably saved, stored, and retrieved • retain usefulness over time • Maintain its storage properties • non-perishable or with low preservation cost • relative worth unit of measure • stable value for stable price comparison • supply must be controlled in some way Ferdinando Ametrano 2017 29/55

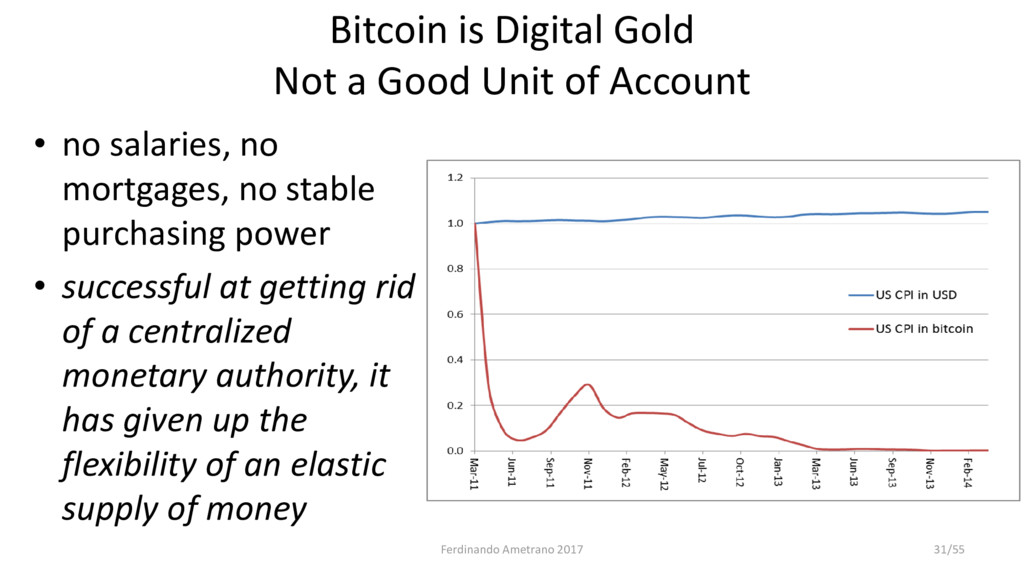

• no salaries, no mortgages, no stable purchasing power • successful at getting rid of a centralized monetary authority, it has given up the flexibility of an elastic supply of money Ferdinando Ametrano 2017 31/55

supply • Price stability paradigm with respect to a given reference basket • Concurrent cryptocurrencies will compete in monetary policy definition and reference basket choices Ferdinando Ametrano 2017 32/55

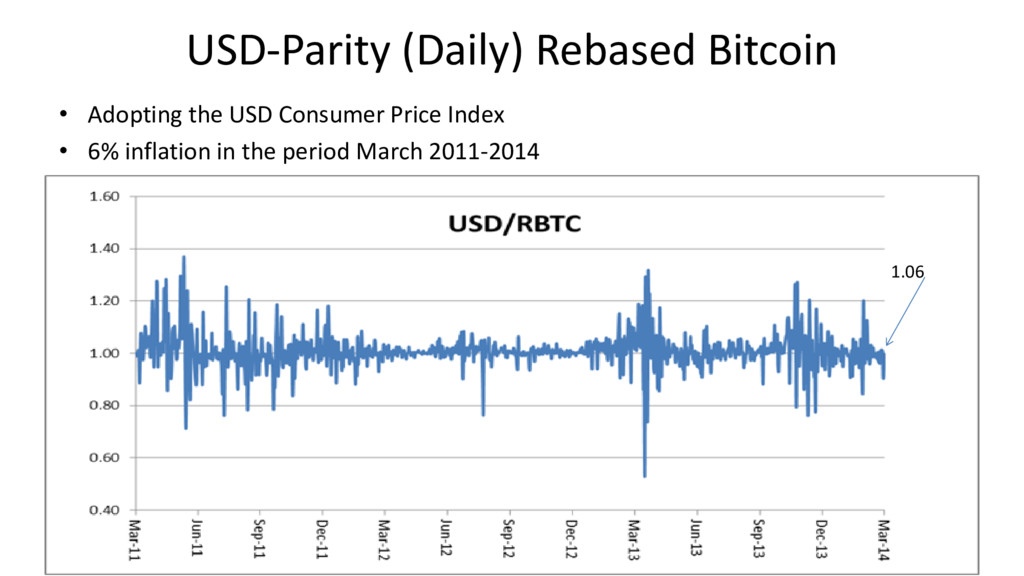

• x500 increase for BTC demand relative to USD • 29-March-14: 12.5M bitcoins in circulation • Inflate their number 500 times to 6250M • On 29-Mar-14 it would have been equivalent –to own BTC1 worth $500 –or (rebased) RBTC500 each worth $1 Ferdinando Ametrano 2017 33/55

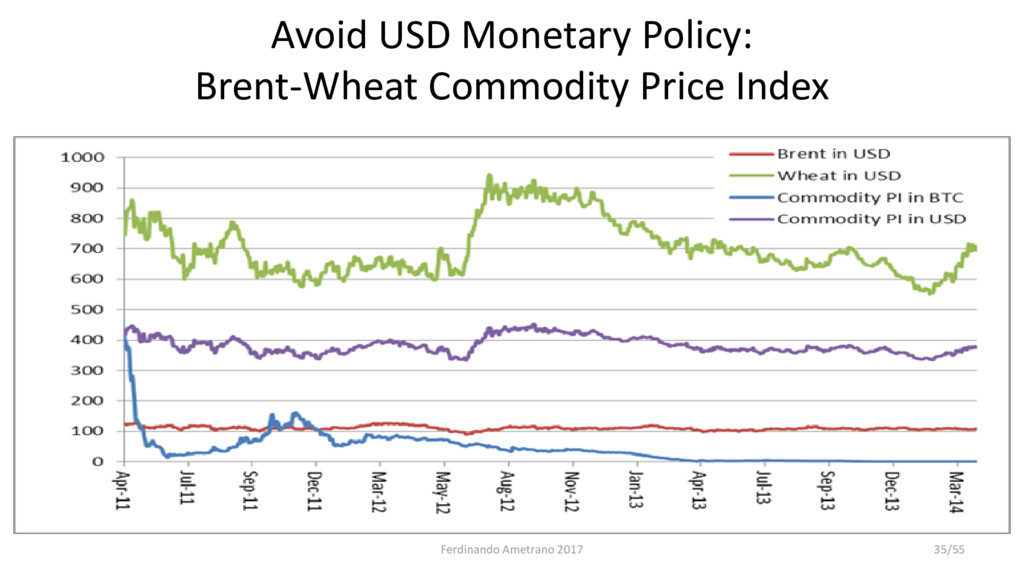

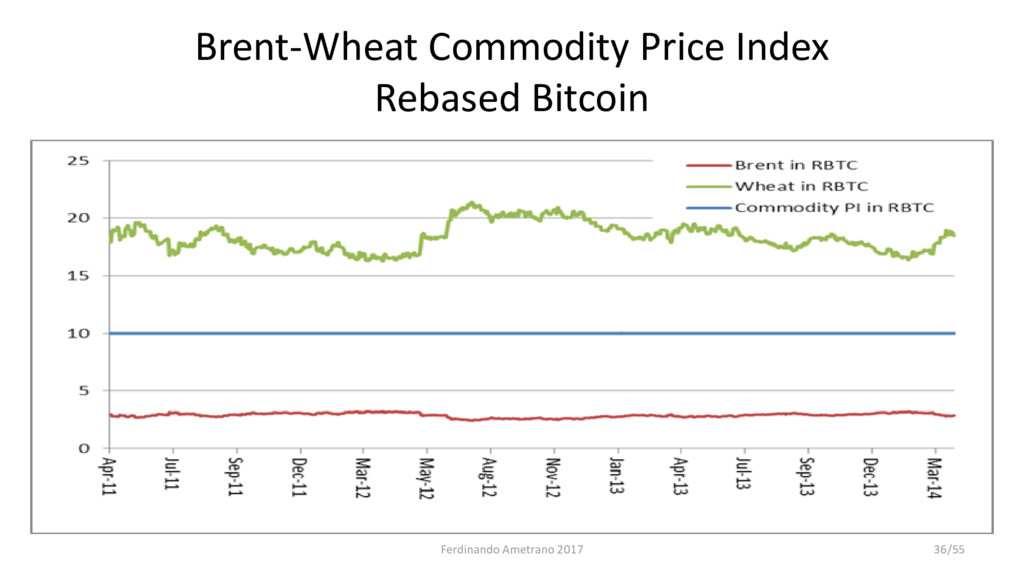

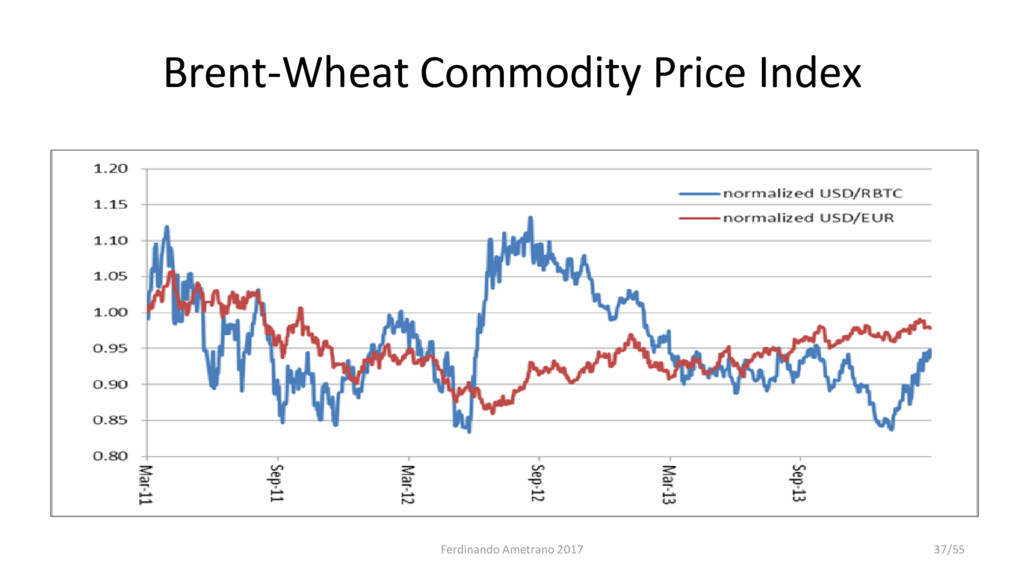

for the sake of discussion, basically to leverage its historic price time series • Bitcoin is good as it is: more of a cryptocommodity than a cryptocurrency, bitcoin is digital gold Ferdinando Ametrano 2017 38/55

stability – Salaries, mortgages, forward payments are now possible • Problems: – Number of coins in a wallet changes without direct in/out flows – Purchasing power of a given wallet is not stable – Coins still have speculative investment appeal and so enjoy limited transaction usage Ferdinando Ametrano 2017 39/55

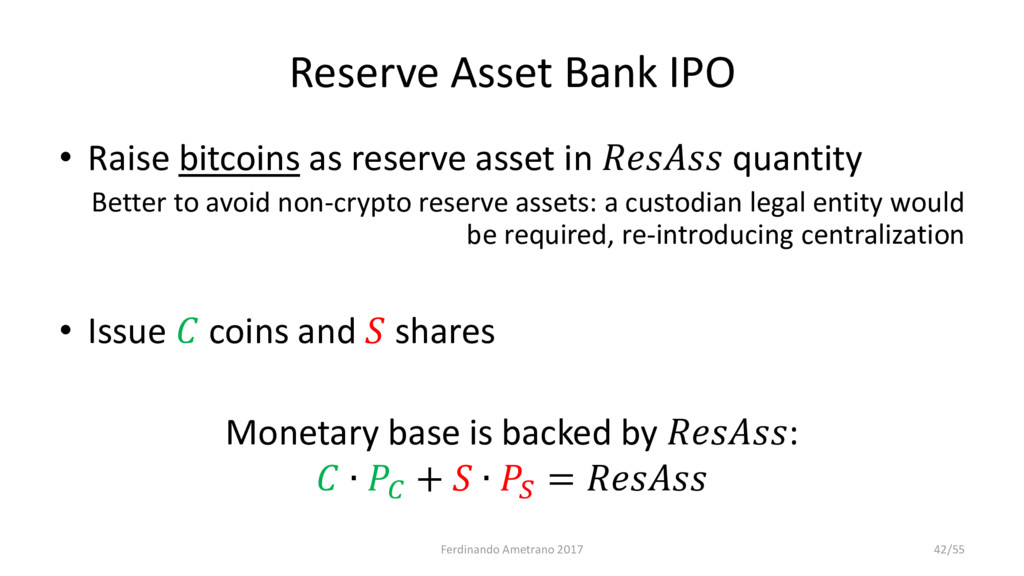

in quantity Better to avoid non-crypto reserve assets: a custodian legal entity would be required, re-introducing centralization • Issue coins and shares Monetary base is backed by : ∙ + ∙ = Ferdinando Ametrano 2017 42/55

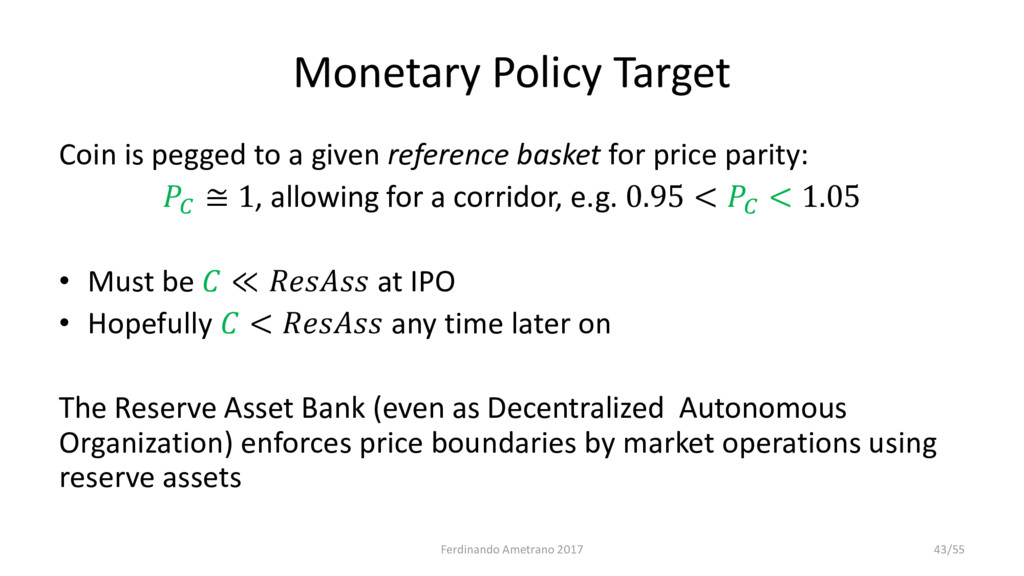

basket for price parity: ≅ 1, allowing for a corridor, e.g. 0.95 < < 1.05 • Must be ≪ at IPO • Hopefully < any time later on The Reserve Asset Bank (even as Decentralized Autonomous Organization) enforces price boundaries by market operations using reserve assets Ferdinando Ametrano 2017 43/55

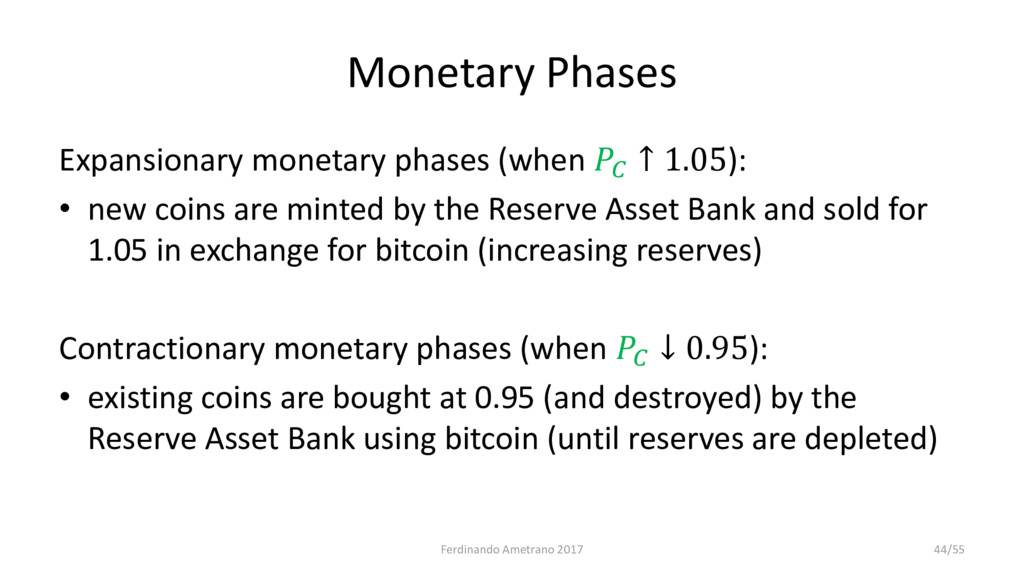

coins are minted by the Reserve Asset Bank and sold for 1.05 in exchange for bitcoin (increasing reserves) Contractionary monetary phases (when ↓ 0.95): • existing coins are bought at 0.95 (and destroyed) by the Reserve Asset Bank using bitcoin (until reserves are depleted) Ferdinando Ametrano 2017 44/55

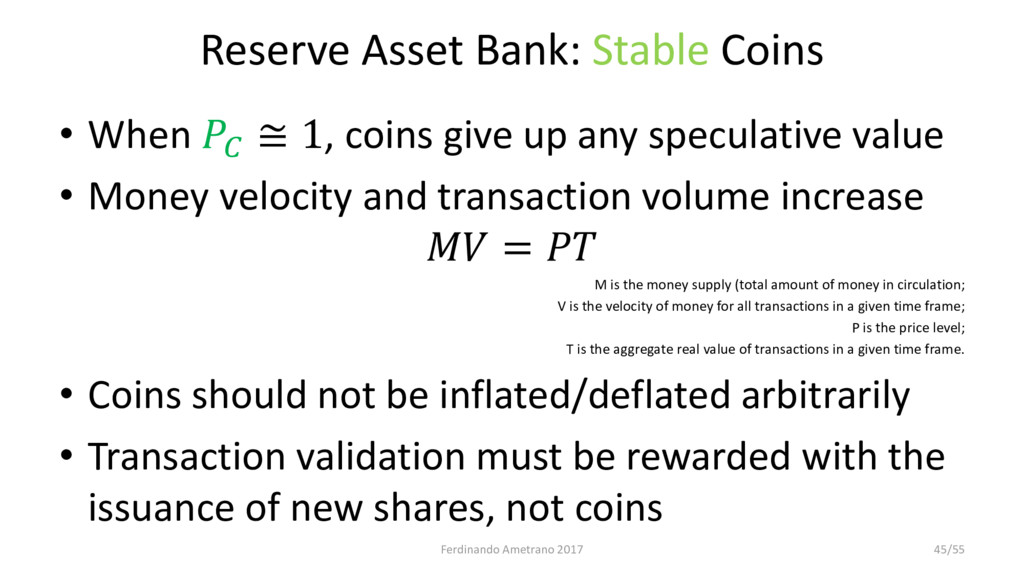

give up any speculative value • Money velocity and transaction volume increase = M is the money supply (total amount of money in circulation; V is the velocity of money for all transactions in a given time frame; P is the price level; T is the aggregate real value of transactions in a given time frame. • Coins should not be inflated/deflated arbitrarily • Transaction validation must be rewarded with the issuance of new shares, not coins Ferdinando Ametrano 2017 45/55

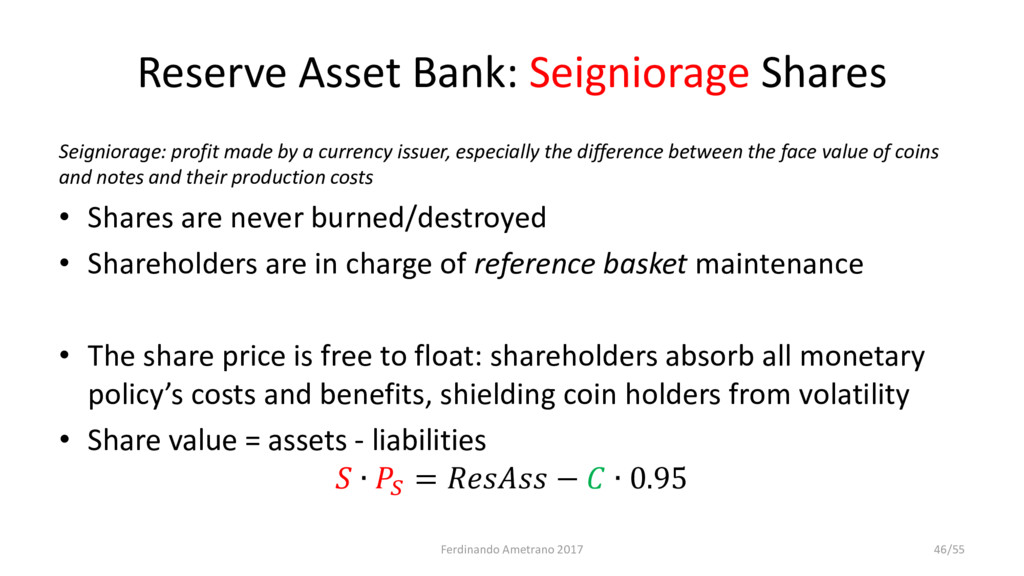

currency issuer, especially the difference between the face value of coins and notes and their production costs • Shares are never burned/destroyed • Shareholders are in charge of reference basket maintenance • The share price is free to float: shareholders absorb all monetary policy’s costs and benefits, shielding coin holders from volatility • Share value = assets - liabilities ∙ = − ∙ 0.95 Ferdinando Ametrano 2017 46/55

• If ↓ 0.95 and < ∙ 0.95: coin is dead, Reserve Bank defaulted, = 0 • If ↓ 0.95 and > ∙ 0.95: coin is dead, Reserve Bank has not defaulted, > 0 (no interest for stable coins, shares are the equivalent of bitcoins) Ferdinando Ametrano 2017 47/55

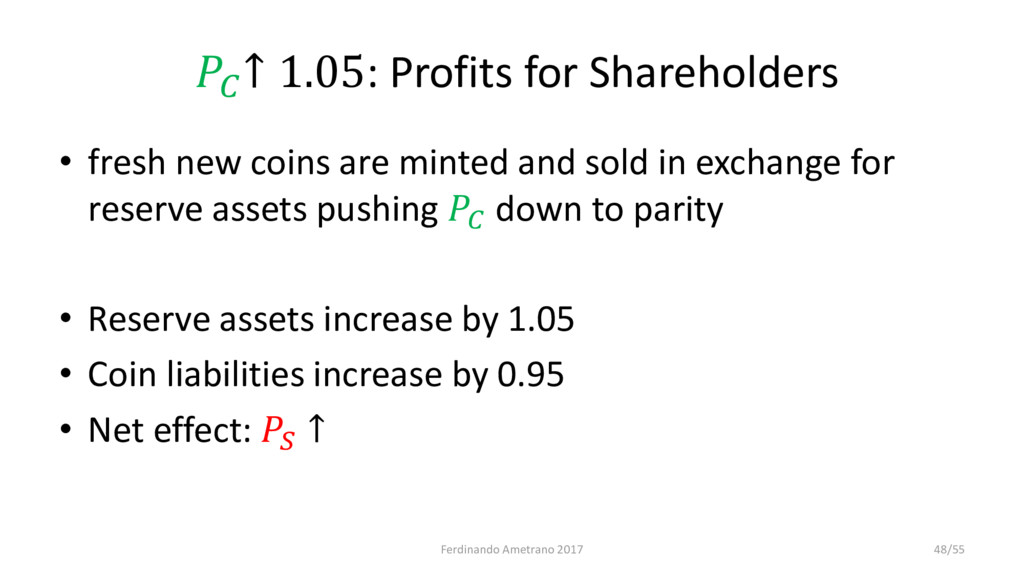

minted and sold in exchange for reserve assets pushing down to parity • Reserve assets increase by 1.05 • Coin liabilities increase by 0.95 • Net effect: ↑ Ferdinando Ametrano 2017 48/55

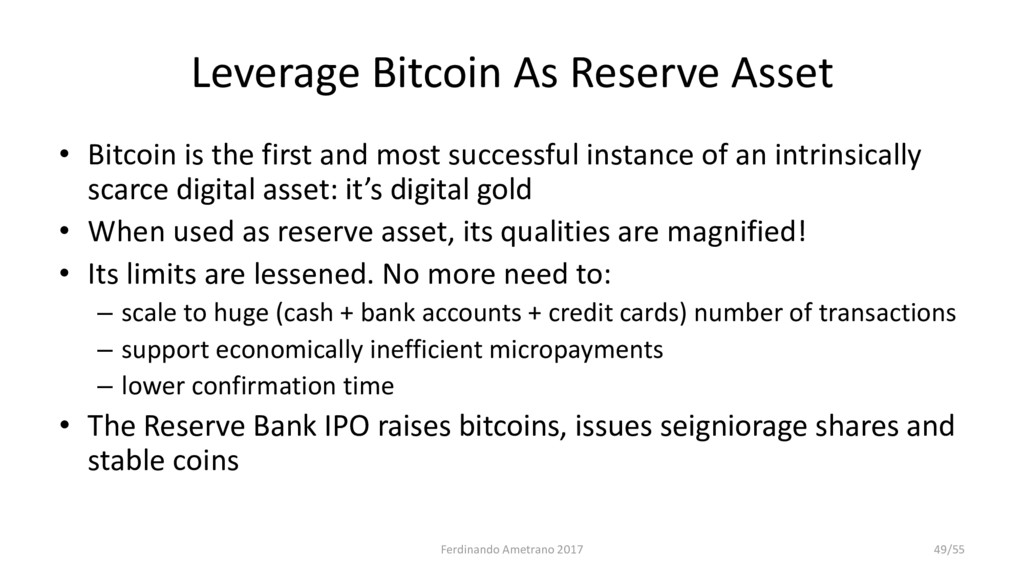

and most successful instance of an intrinsically scarce digital asset: it’s digital gold • When used as reserve asset, its qualities are magnified! • Its limits are lessened. No more need to: – scale to huge (cash + bank accounts + credit cards) number of transactions – support economically inefficient micropayments – lower confirmation time • The Reserve Bank IPO raises bitcoins, issues seigniorage shares and stable coins Ferdinando Ametrano 2017 49/55

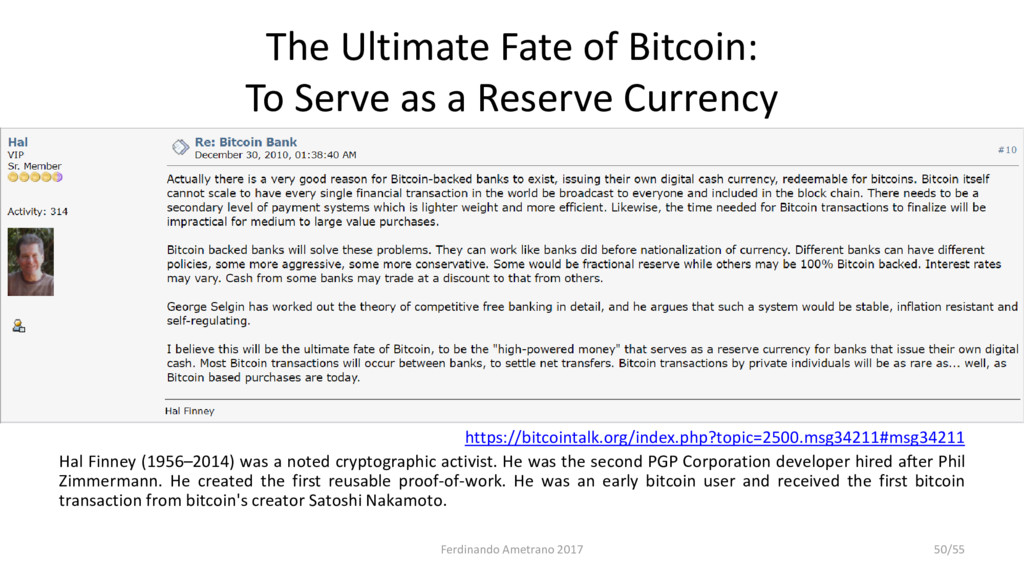

Currency https://bitcointalk.org/index.php?topic=2500.msg34211#msg34211 Hal Finney (1956–2014) was a noted cryptographic activist. He was the second PGP Corporation developer hired after Phil Zimmermann. He created the first reusable proof-of-work. He was an early bitcoin user and received the first bitcoin transaction from bitcoin's creator Satoshi Nakamoto. Ferdinando Ametrano 2017 50/55

power expenses of proof-of- work, bitcoins are irrevocably paid to the Reserve Asset Bank by validating nodes (proof-of-payment) • Chances of being appointed for the next block generation are proportional to the overall submitted payments, i.e. to the accumulated proof-of-payment • When a node is picked up for block generation its proof-of- payment resets to zero • Even if a node is not picked up, its payments are never reimbursed Ferdinando Ametrano 2017 51/55

issuance of a new share • Since = − ∙ 0.95 , that should be the price a rational agent is willing to commit as payment • Share price estimation in bitcoin is obtained as by-product • Existing shareholders are not really diluted: for the issuance of each new share, increases accordingly Ferdinando Ametrano 2017 52/55

Solution, http://ssrn.com/abstract=2425270 • Morini M., Inv/Sav Wallets and the Role of Financial Intermediaries in a Digital Currency, http://ssrn.com/abstract=2458890 • Sams R., A Note on Cryptocurrency Stabilisation: Seigniorage Shares, https://github.com/rmsams/stablecoins/blob/master/00-main.pdf • Buterin V., The Search for a Stable Cryptocurrency, https://blog.ethereum.org/2014/11/11/search-stable-cryptocurrency/ • Ametrano F., Cryptocurrency Price Stability With Seigniorage Shares And Reserve Bank, http://ssrn.com/abstract=2508296 Ferdinando Ametrano 2017 53/55

seigniorage revenues 2. Bitcoin is a scarce digital asset, i.e. the digital equivalent of gold 3. Hayek Money is the price stability paradigm of elastic non- discretionary money supply 4. Coin/share dual asset ledger can decouple transactional and speculative money demand 5. Bitcoin can be used as reserve asset by a decentralized Reserve Asset Bank (DAO) to stabilize the coin 6. Proof-of-Payment leverages bitcoin as off-chain resource to be consumed in order to receive seigniorage revenues Ferdinando Ametrano 2017 55/55

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}