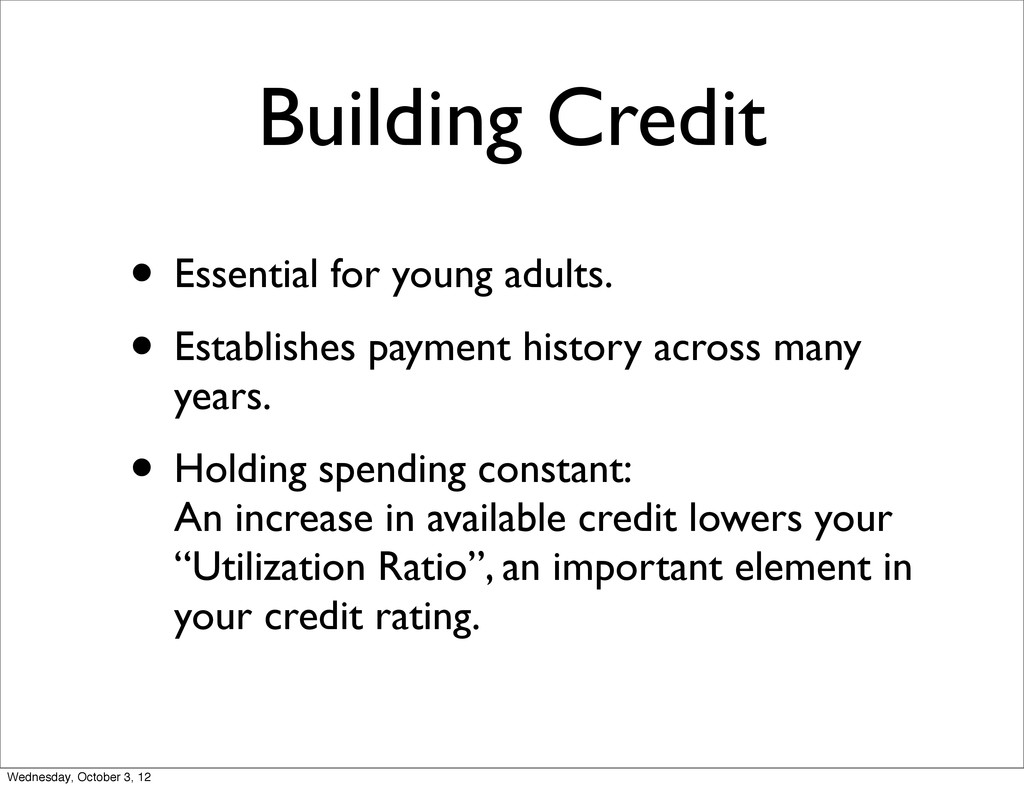

history across many years. • Holding spending constant: An increase in available credit lowers your “Utilization Ratio”, an important element in your credit rating. Wednesday, October 3, 12

Often convertible to cash (cash back) • Slightly lower redemption values (price of flexibility) • Airline/Hotel • Specific points/miles redeemable often with a single company. • Slightly higher redemption values. Wednesday, October 3, 12

signing up for a card (sometimes with spending requirements). • Credit card companies willing to take a short-term lost in hopes of long-term gain (yearly fee, interest charges). • Sometimes targeted offers are sent offering even higher initial point bonuses (Chase Sapphire with 75,000 reported). Wednesday, October 3, 12

sometimes varying by spending category. • Economic incidence: cash/check payers subsidize card payers. Paying cash has an opportunity cost. • Points/Miles not considered income by IRS, so they are essentially tax free! Wednesday, October 3, 12

• Hotel/Airline points: • Look up price of alternatives you would normally have chosen and calculate effective cash value to you • Valuation varies from person to person • Sometime exhibit diminishing marginal utility (who would use 100 nights at a Marriott?) Wednesday, October 3, 12

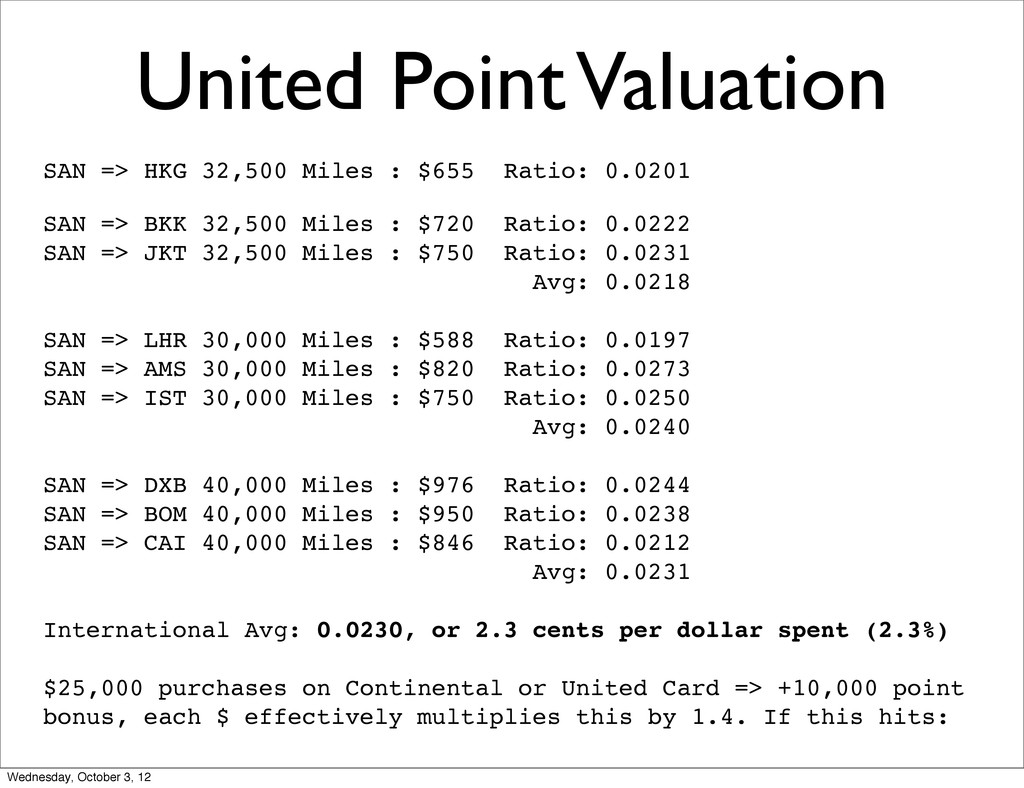

Ratio: 0.0201 SAN => BKK 32,500 Miles : $720 Ratio: 0.0222 SAN => JKT 32,500 Miles : $750 Ratio: 0.0231 Avg: 0.0218 SAN => LHR 30,000 Miles : $588 Ratio: 0.0197 SAN => AMS 30,000 Miles : $820 Ratio: 0.0273 SAN => IST 30,000 Miles : $750 Ratio: 0.0250 Avg: 0.0240 SAN => DXB 40,000 Miles : $976 Ratio: 0.0244 SAN => BOM 40,000 Miles : $950 Ratio: 0.0238 SAN => CAI 40,000 Miles : $846 Ratio: 0.0212 Avg: 0.0231 International Avg: 0.0230, or 2.3 cents per dollar spent (2.3%) $25,000 purchases on Continental or United Card => +10,000 point bonus, each $ effectively multiplies this by 1.4. If this hits: Wednesday, October 3, 12

• Chase Freedom: 5% return on up to $1500 on categories that vary. Use Chase Freedom for those categories. • Airline/Hotel cards give greater return on purchases with their company. • Keep in mind diminishing marginal utility of points/miles. Wednesday, October 3, 12

Point valuation can be higher than that. • Great way to contribute to spending plateaus - optimize accordingly! • Be careful with utilization ratio - could hurt your credit if this dips too low. • California charges 2.3% - more difficult but still could be worthwhile. Wednesday, October 3, 12

credit (> 720) • If cards have spending requirements, plan acquisition before spending. • Applying will ding your credit slightly (“hard” credit inquiry). • If getting more than one card, apply at the same time (grouped hard credit inquiries less damaging). • Carefully manage acquisitions from same bank (Chase is conservative). Wednesday, October 3, 12

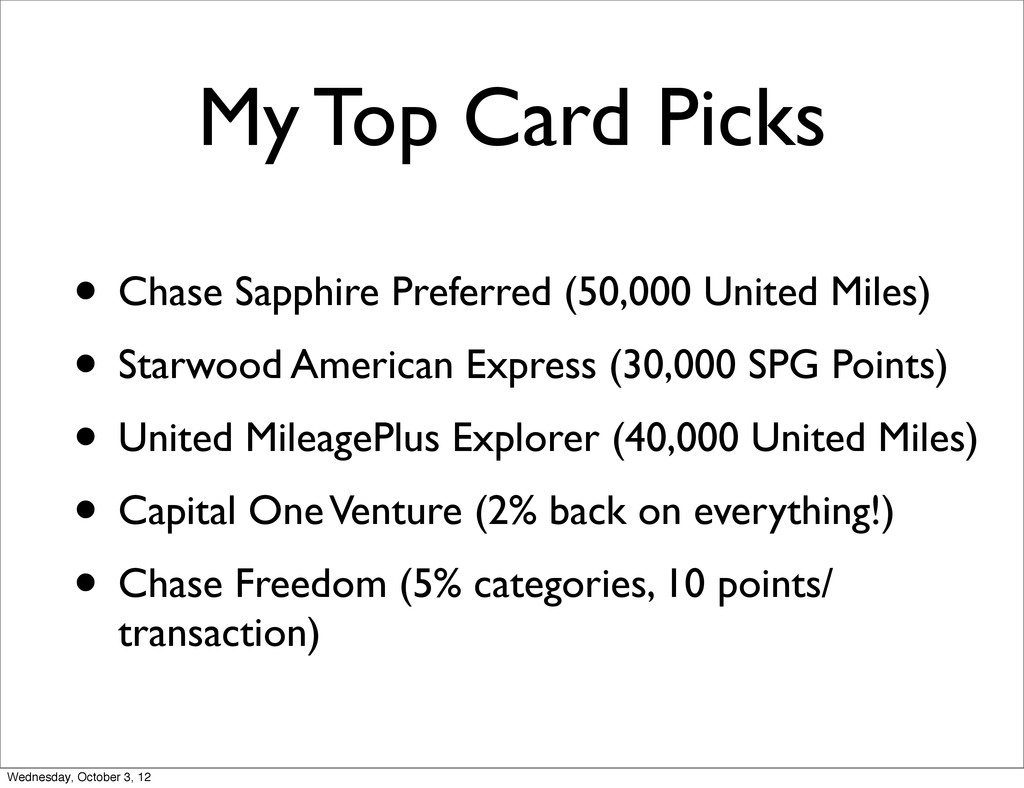

Miles) • Starwood American Express (30,000 SPG Points) • United MileagePlus Explorer (40,000 United Miles) • Capital One Venture (2% back on everything!) • Chase Freedom (5% categories, 10 points/ transaction) Wednesday, October 3, 12

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}