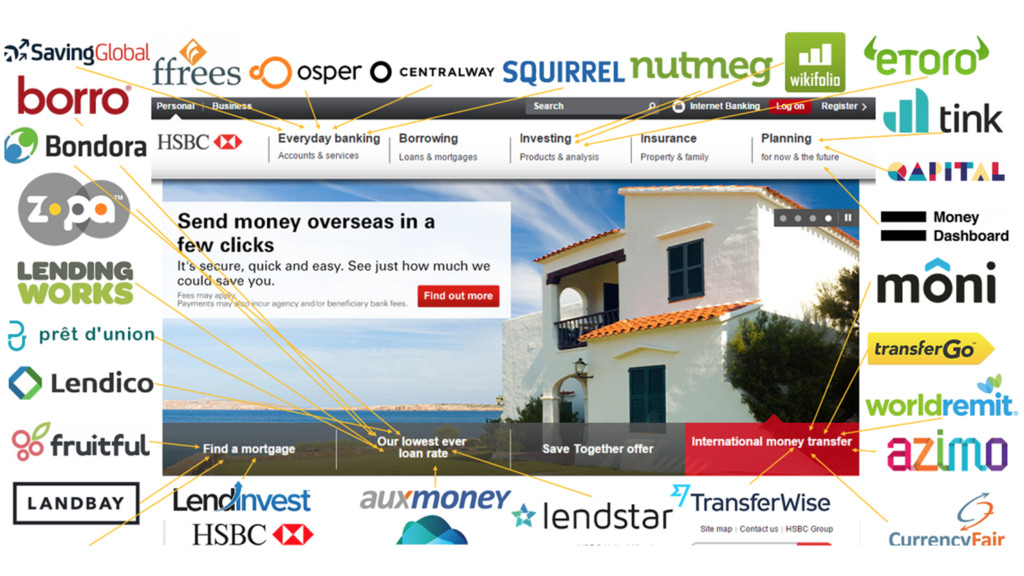

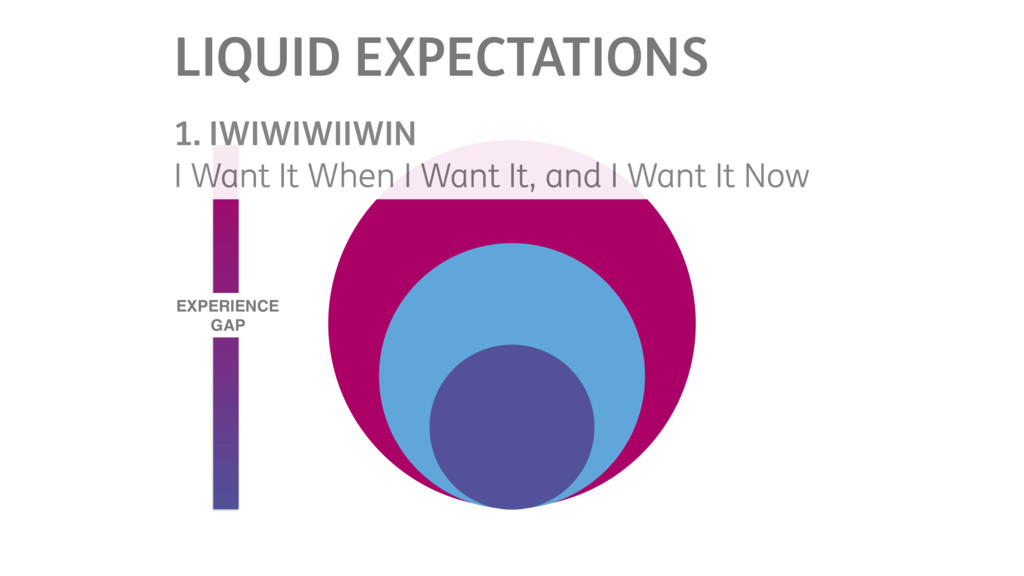

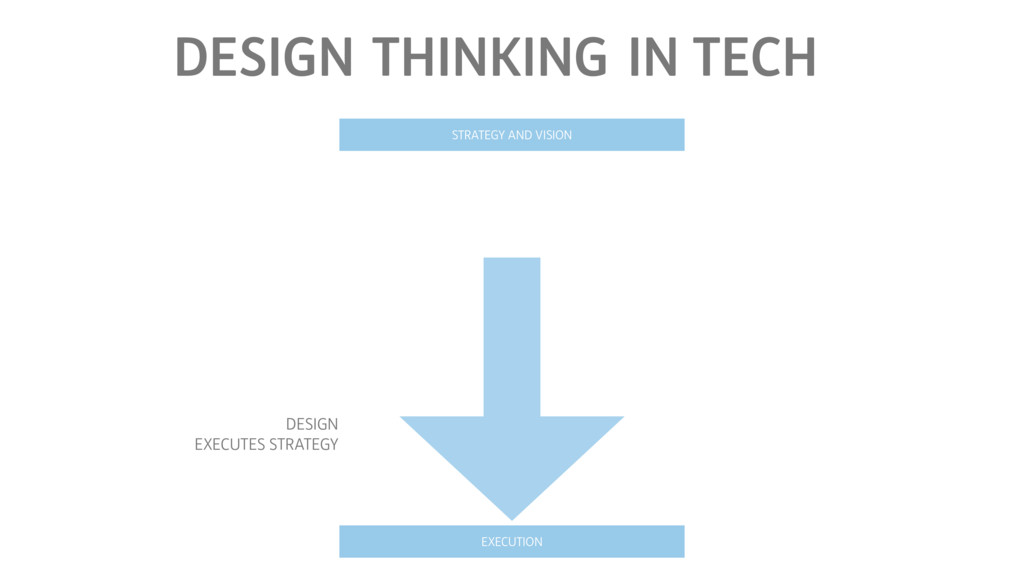

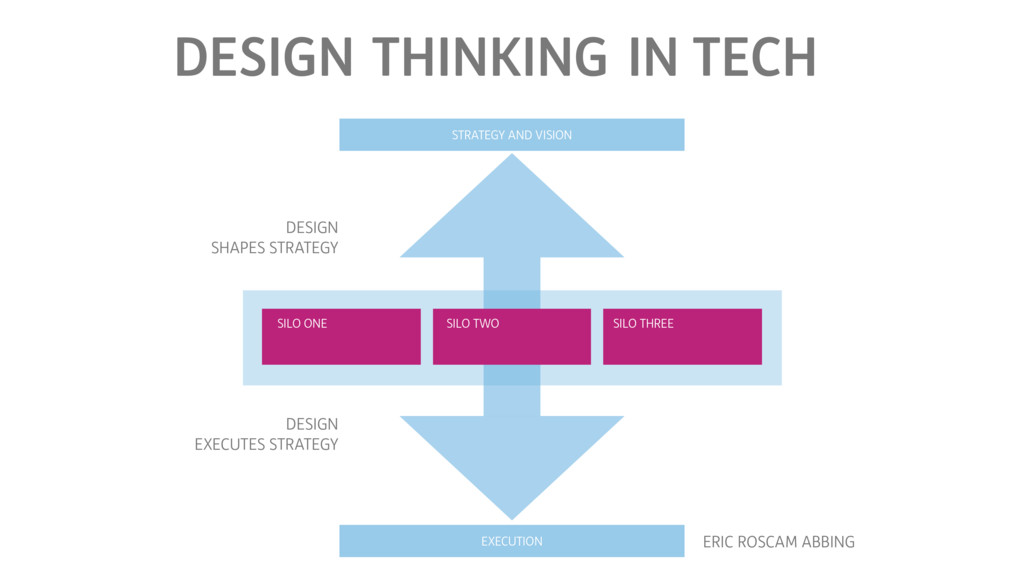

The race for the best technology' is shifting toward 'the race for the best experience'. Or in other words: what software left when it ate the world...

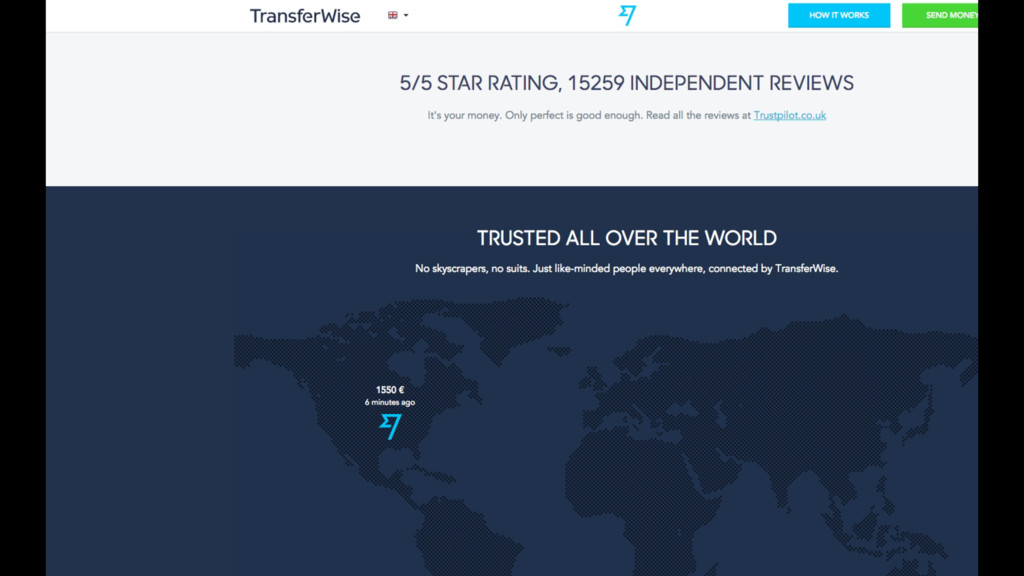

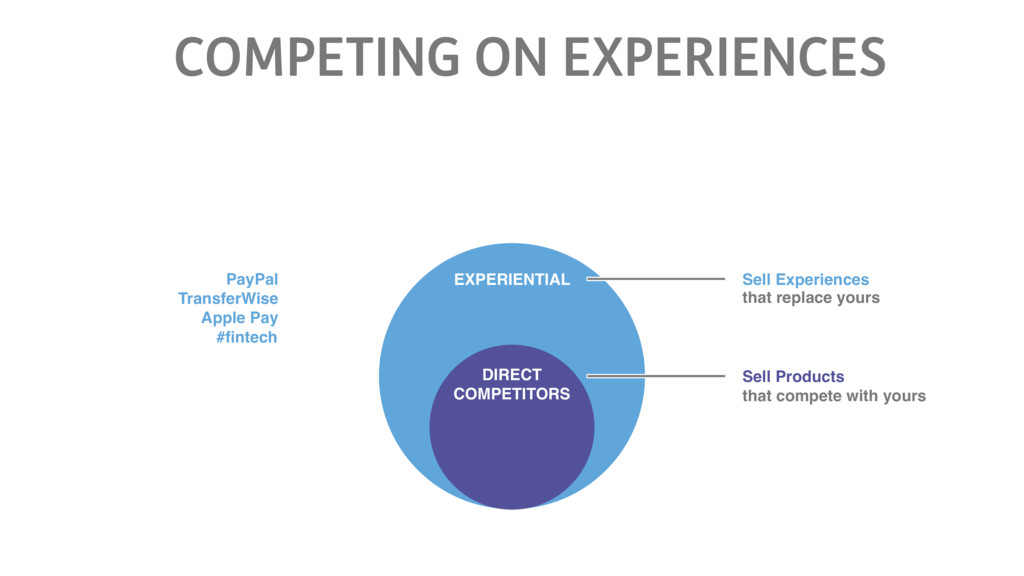

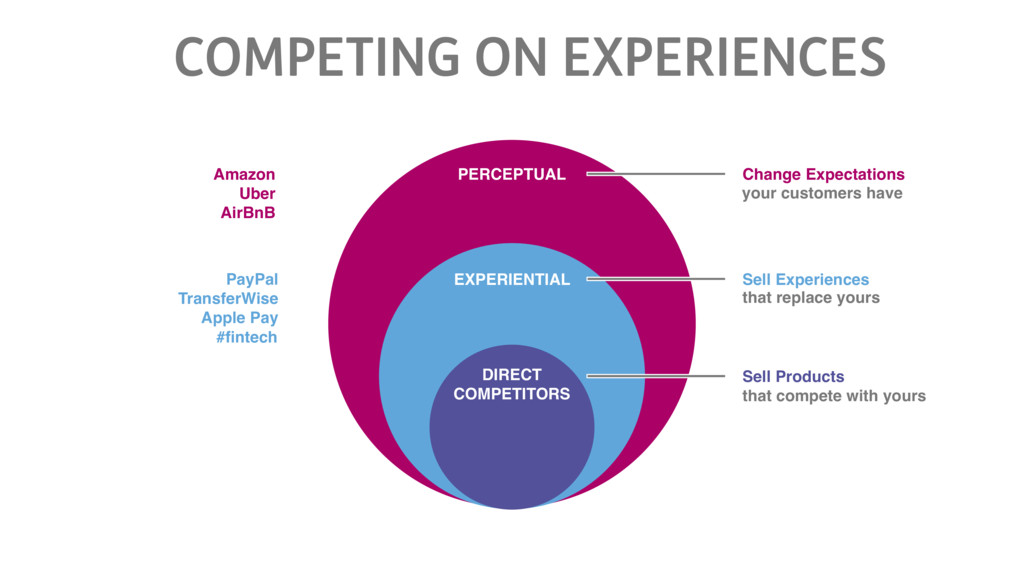

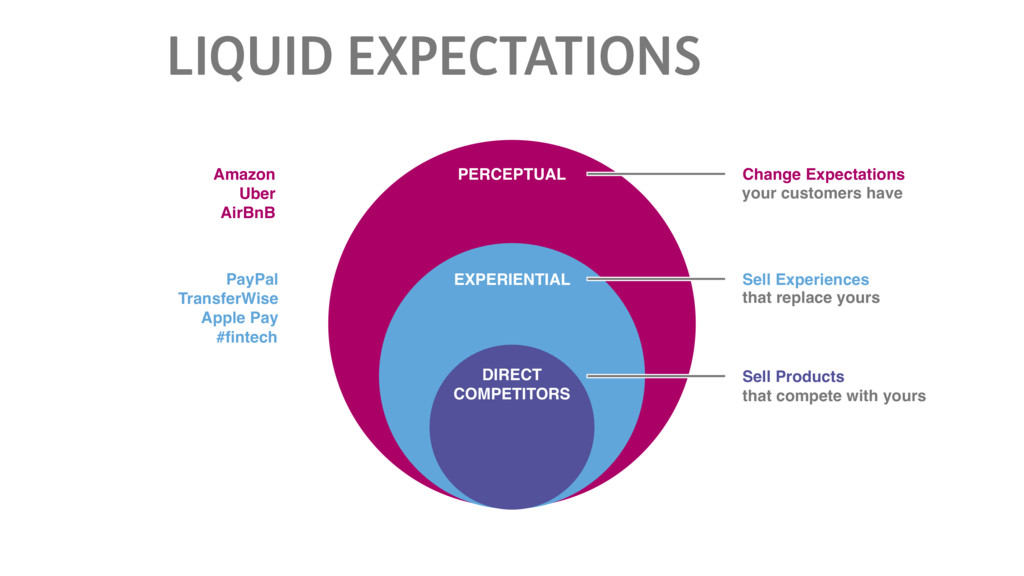

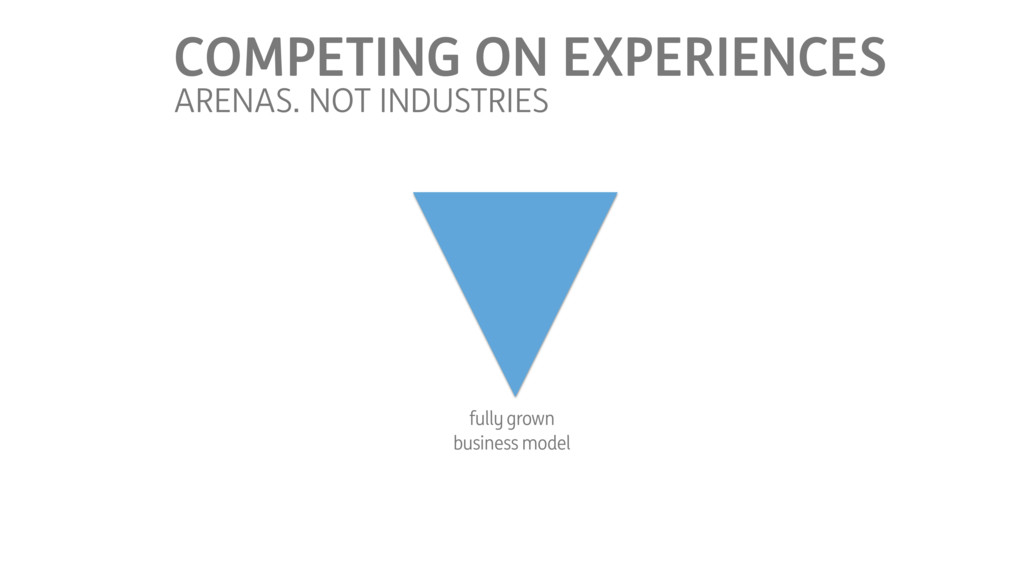

compete with yours Sell Experiences that replace yours Change Expectations your customers have PayPal TransferWise Apple Pay Amazon Uber AirBnB #fintech

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[email protected] @absynthmind](https://files.speakerdeck.com/presentations/d304d55072574901abd5bf47343b8baf/slide_40.jpg){kind=link}