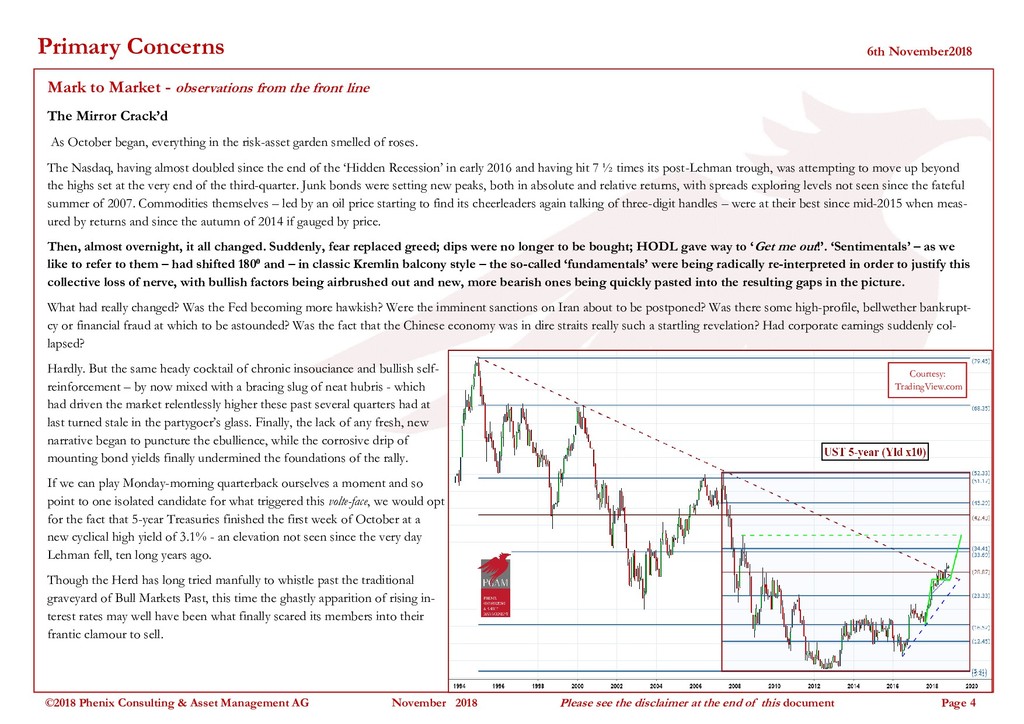

October is often the cruellest month in markets and so it proved again this year. The pain was widespread across all major asset classes and geographies. Though still ahead of most of their rivals for the year-to-date, commodites were no exception, with the ongoing collapse of the record longs in crude driving the tape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}