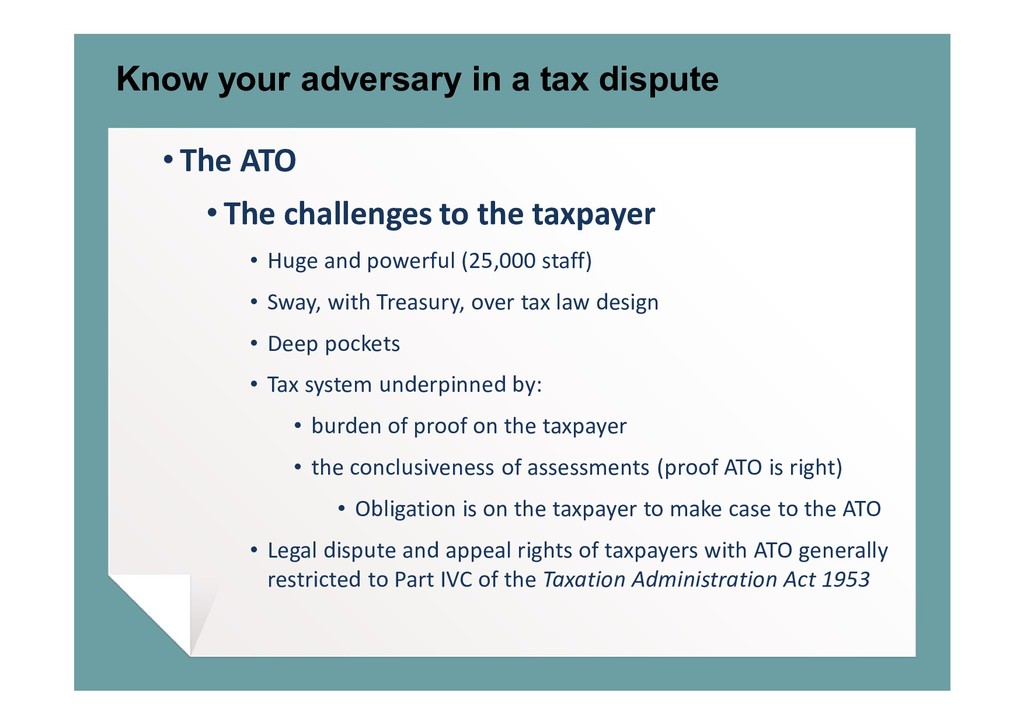

The Australian Taxation Office has now sanctioned distinct ways of resolving tax disputes and there has been an expansion of resources available to taxpayers to assist with dispute resolution with the Tax Office. Objection rights still underpin taxpayer rights to challenge assessments but a number of different approaches to resolve tax disputes can now be considered and, in various circumstances, there is support with costs of the challenge. Implications of particular approaches and what may be effective in terms of both time and money are considered.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}