2020 (FI2020), a global multi-stakeholder movement to achieve full financial inclusion and initiated by the Center for Financial Inclusion at Accion. During Financial Inclusion Week stakeholders across the globe are participating in conversations exploring the most important steps to achieving full financial inclusion, while keeping clients first in a digital world.

it important? Financial Inclusion Facilitates day-to-day living Helps with planning & risk management (for goals and/or emergencies) Enables investment, e.g. in health and education Improvement in overall quality of life Financial products & services for individuals and businesses which are: • Accessible • Affordable • Available • Sustainable • Responsible • Competitive @dianacbiggs 2016

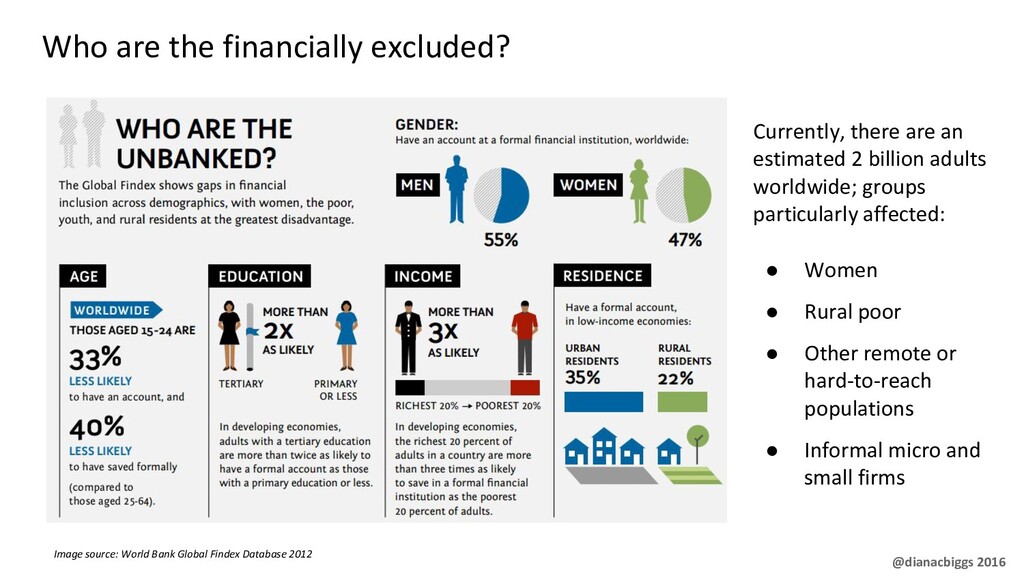

2 billion adults worldwide; groups particularly affected: • Women • Rural poor • Other remote or hard-to-reach populations • Informal micro and small firms Image source: World Bank Global Findex Database 2012 @dianacbiggs 2016

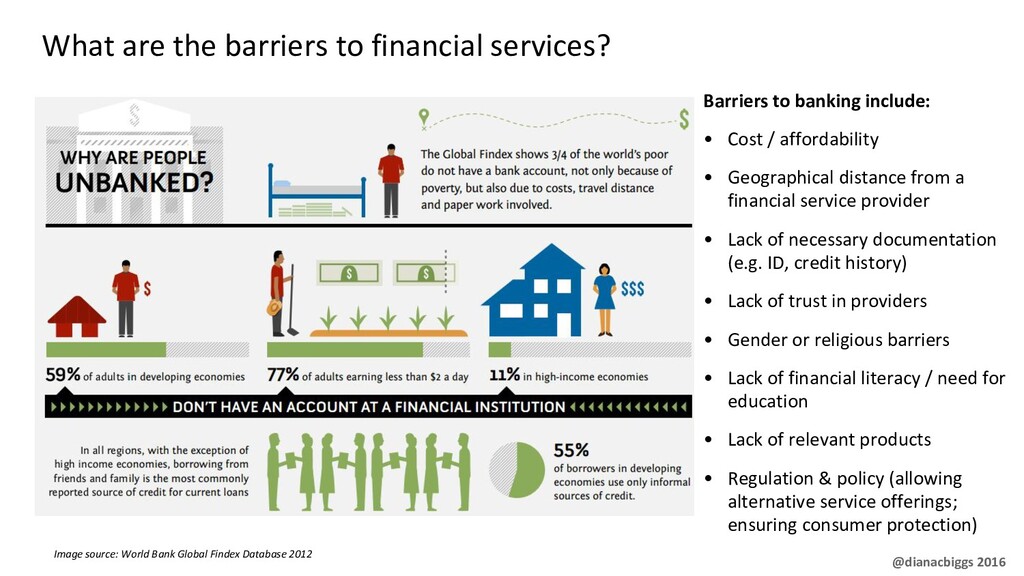

include: • Cost / affordability • Geographical distance from a financial service provider • Lack of necessary documentation (e.g. ID, credit history) • Lack of trust in providers • Gender or religious barriers • Lack of financial literacy / need for education • Lack of relevant products • Regulation & policy (allowing alternative service offerings; ensuring consumer protection) Image source: World Bank Global Findex Database 2012 @dianacbiggs 2016

inclusion 2016 1970s Early studies in Microfinance Launch of Aadhaar ID, India (2009) Launch of Kiva MPESA Pilot in Kenya Enablers: • Global ubiquity of mobile phones • Growing access to internet / data • Introduction of digital FS offerings / digital cash • Government commitment / enabling policy • Digital ID offerings • The problem is understood (increasing data) Financial Inclusion: enabler for 7 of 17 UN SDGs (2015) G20 Financial Inclusion Action Plan (2010) 2005 World Bank Universal Financial Access (UFA) goal 2020 2010 Yunus / Grameen win Nobel Peace Prize (2006) MPESA launch (2007) Launch of M-SHWARI (2012) UN Year of Microcredit Yunus launched Grameen bank (1983) UK banks looking at financial edu @dianacbiggs 2016

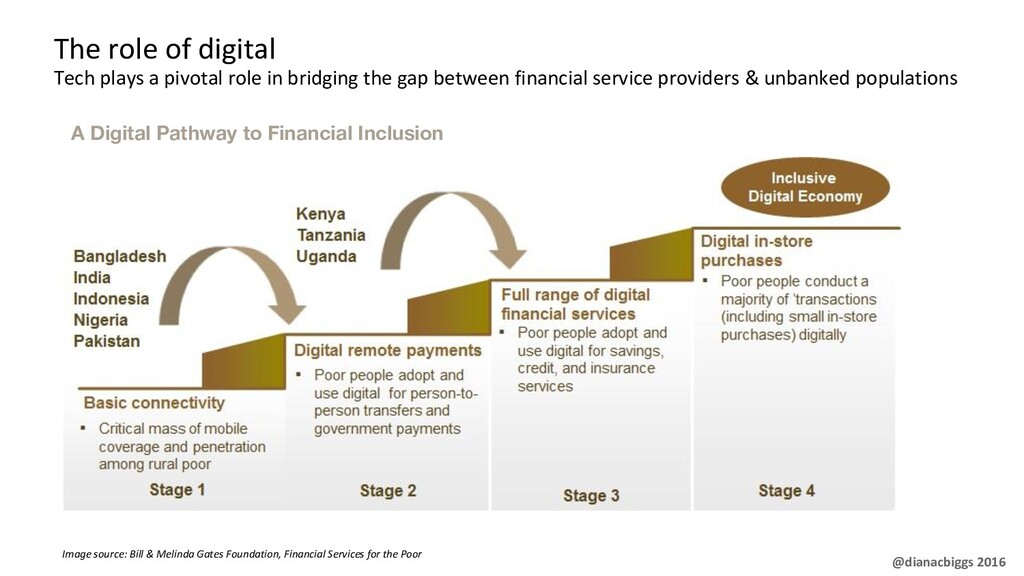

bridging the gap between financial service providers & unbanked populations A Digital Pathway to Financial Inclusion Image source: Bill & Melinda Gates Foundation, Financial Services for the Poor @dianacbiggs 2016

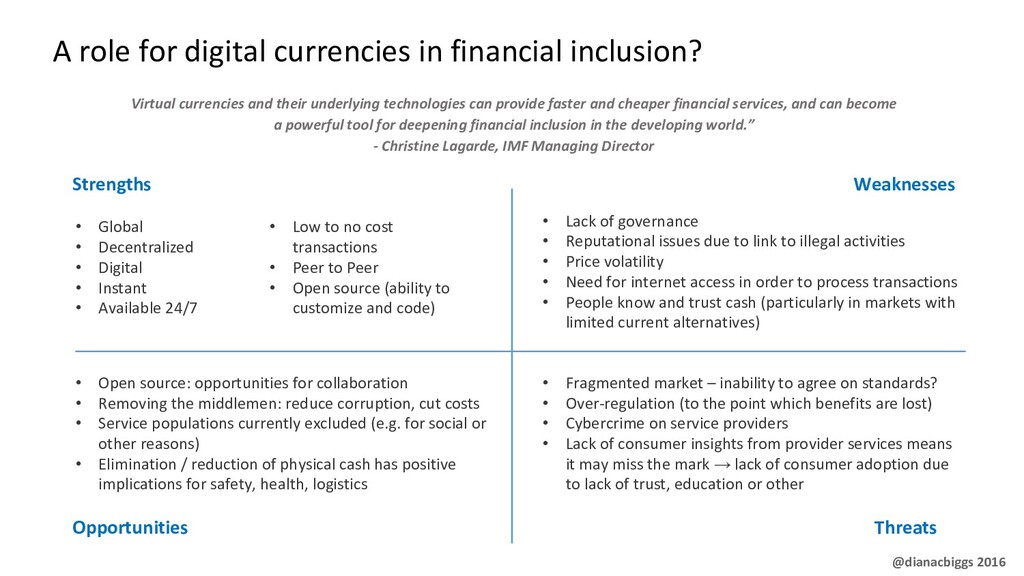

and their underlying technologies can provide faster and cheaper financial services, and can become a powerful tool for deepening financial inclusion in the developing world.” - Christine Lagarde, IMF Managing Director • Global • Decentralized • Digital • Instant • Available 24/7 Weaknesses Strengths Opportunities Threats • Lack of governance • Reputational issues due to link to illegal activities • Price volatility • Need for internet access in order to process transactions • People know and trust cash (particularly in markets with limited current alternatives) • Open source: opportunities for collaboration • Removing the middlemen: reduce corruption, cut costs • Service populations currently excluded (e.g. for social or other reasons) • Elimination / reduction of physical cash has positive implications for safety, health, logistics • Fragmented market – inability to agree on standards? • Over-regulation (to the point which benefits are lost) • Cybercrime on service providers • Lack of consumer insights from provider services means it may miss the mark → lack of consumer adoption due to lack of trust, education or other • Low to no cost transactions • Peer to Peer • Open source (ability to customize and code) @dianacbiggs 2016

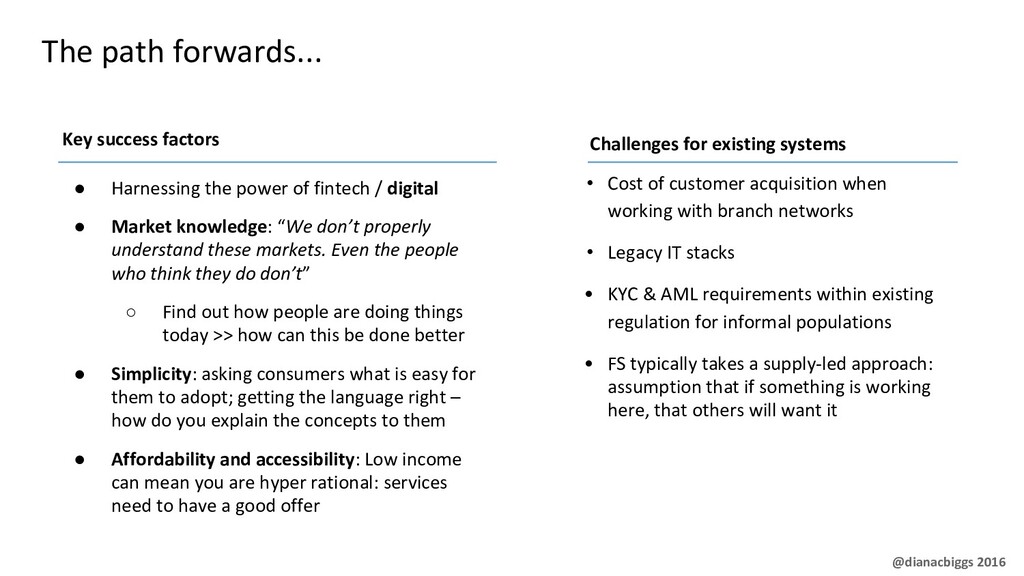

with branch networks • Legacy IT stacks • KYC & AML requirements within existing regulation for informal populations • FS typically takes a supply-led approach: assumption that if something is working here, that others will want it • Harnessing the power of fintech / digital • Market knowledge: “We don’t properly understand these markets. Even the people who think they do don’t” ◦ Find out how people are doing things today >> how can this be done better • Simplicity: asking consumers what is easy for them to adopt; getting the language right – how do you explain the concepts to them • Affordability and accessibility: Low income can mean you are hyper rational: services need to have a good offer Key success factors Challenges for existing systems @dianacbiggs 2016

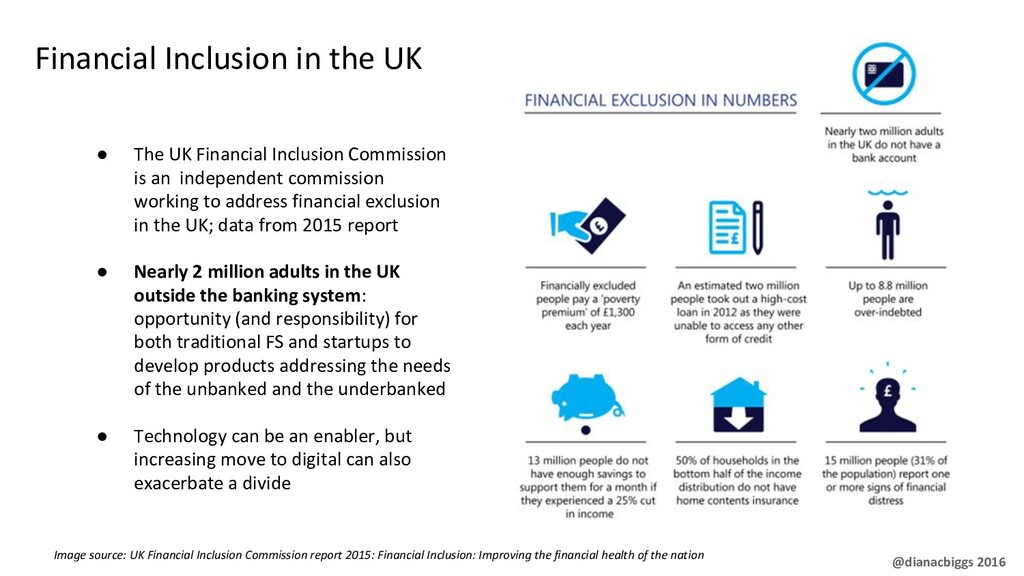

working to address financial exclusion in the UK; data from 2015 report • Nearly 2 million adults in the UK outside the banking system: opportunity (and responsibility) for both traditional FS and startups to develop products addressing the needs of the unbanked and the underbanked • Technology can be an enabler, but increasing move to digital can also exacerbate a divide Financial Inclusion in the UK @dianacbiggs 2016 Image source: UK Financial Inclusion Commission report 2015: Financial Inclusion: Improving the financial health of the nation

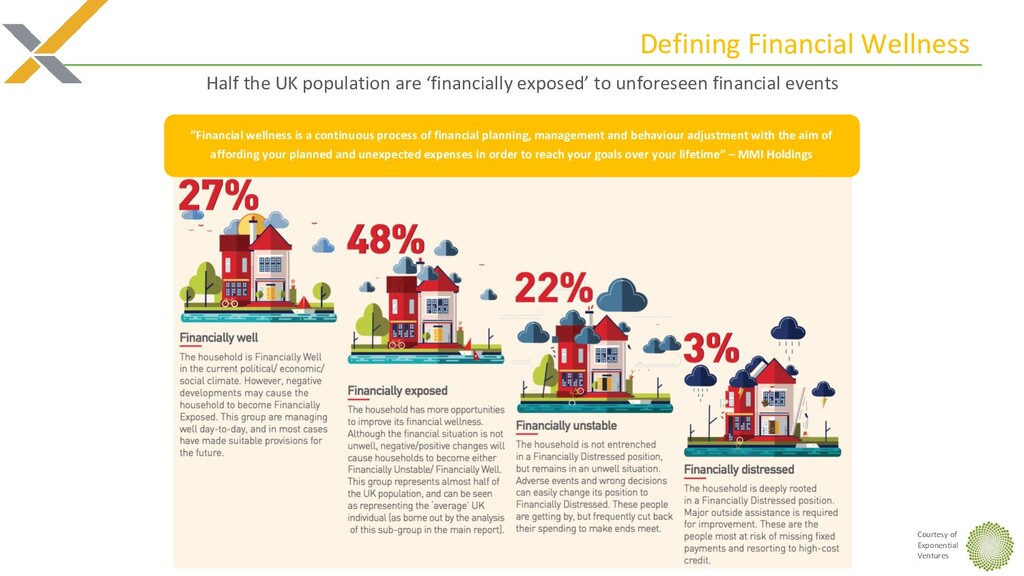

to unforeseen financial events ”Financial wellness is a continuous process of financial planning, management and behaviour adjustment with the aim of affording your planned and unexpected expenses in order to reach your goals over your lifetime” – MMI Holdings Courtesy of Exponential Ventures

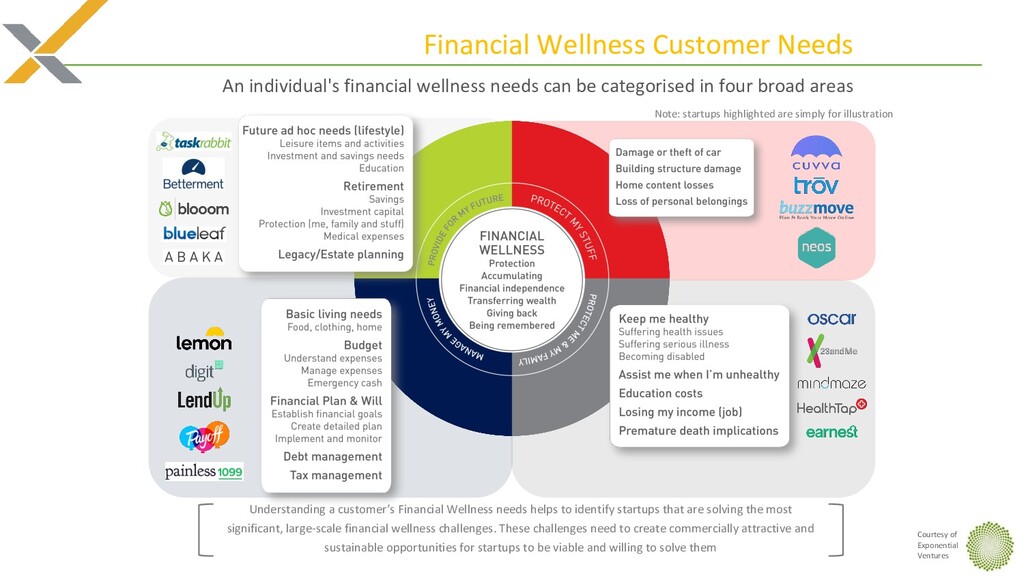

be categorised in four broad areas Understanding a customer’s Financial Wellness needs helps to identify startups that are solving the most significant, large-scale financial wellness challenges. These challenges need to create commercially attractive and sustainable opportunities for startups to be viable and willing to solve them Note: startups highlighted are simply for illustration Courtesy of Exponential Ventures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}