of many parts working together, how bad with their product be if they just randomly assembled car’s? Creating a system to review a file is the KEY to quality and production Creating a system of daily work habits is KEY to customer service Remember underwriting a loan is not about just “the door” or “the engine” it’s about the entire car running well!

effect of loan guidelines and loan program requirements FNMA or FHLMC – also referred to as “agency” or GSE’s Investor (Cole Taylor is both Investor (wholesale) and company (retail)) Company Channel Specific Loan Type ( IE DURP guidelines are different then standard)

it translates to “risk” which translates to guidelines Primary = Highest LTV Second Home = Standard LTV’s Investment = Lowest LTV’s Understanding the level of risk will help identify the “depth” of rules

score and history of paying back other obligations Capacity The borrowers financial ability to pay back the mortgage. This includes focus on income, employment history, current debts. Capital The borrowers money in checking, savings, investments, and other properties. Collateral The value of the property the borrower is pledging as security against the loan

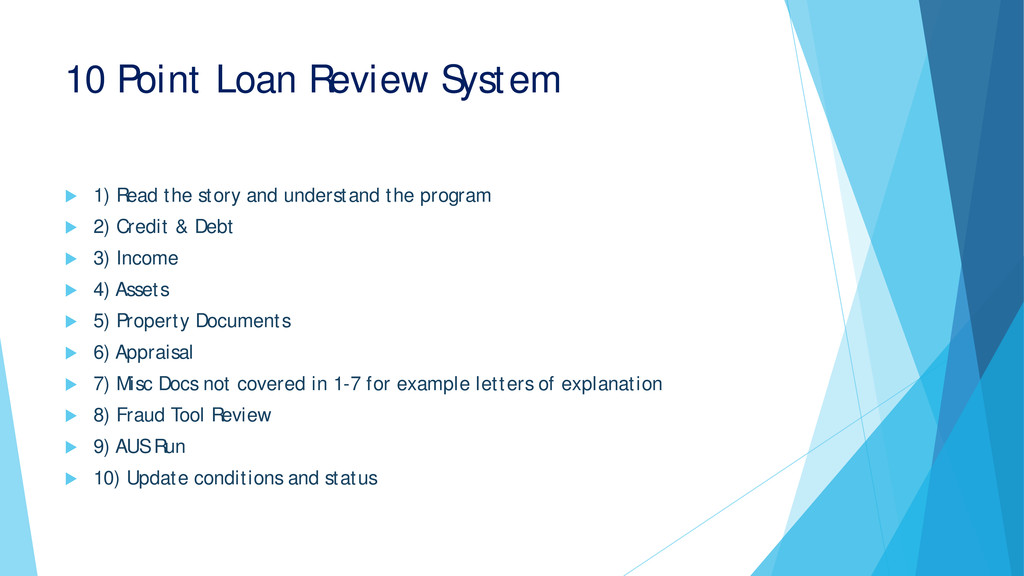

and understand the program 2) Credit & Debt 3) Income 4) Assets 5) Property Documents 6) Appraisal 7) Misc Docs not covered in 1-7 for example letters of explanation 8) Fraud Tool Review 9) AUS Run 10) Update conditions and status

your “to do list” working www.simpleology.com Underwrite a new file Check your messages and return calls Clear 2-3 condition files Wash, rinse, repeat

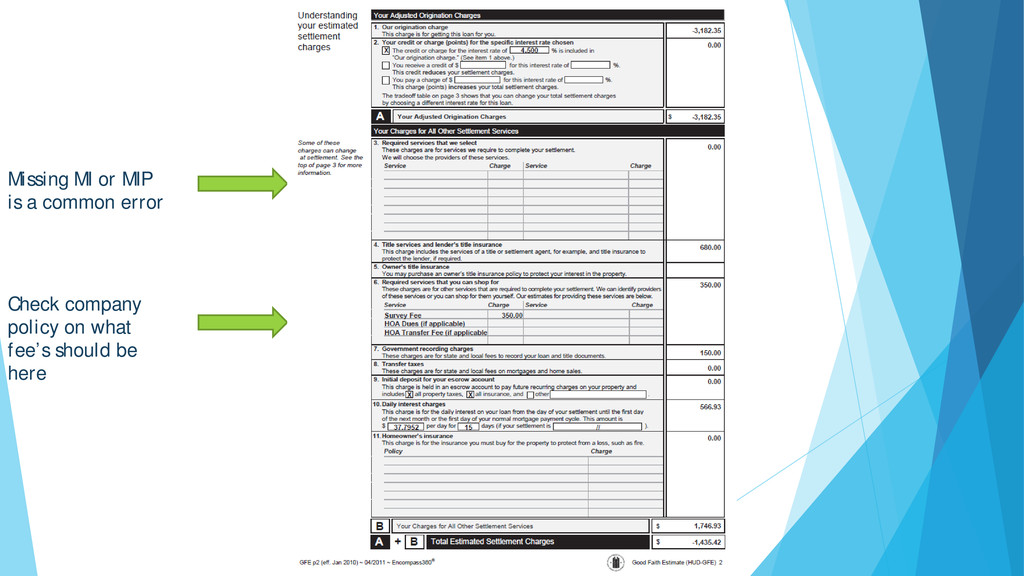

start with the number 1 problem seen in underwriting auditing in regards to the Good Faith Estimate IT’s MISSING! Regulations require that a GFE is issued to the borrower within three business days of taking the loan application.

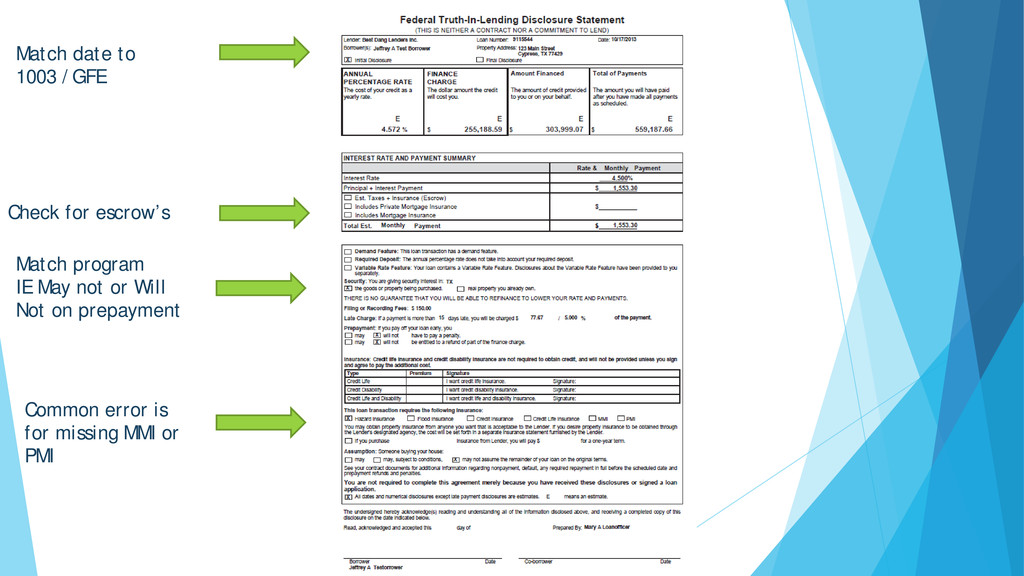

TIL Lets start with the number 1 problem seen in underwriting auditing in regards to the Truth In Lending IT’s MISSING!! (common theme huh?) A TIL is issued along with the GFE

120 days of closing Asset documents within 120 days of closing Appraisal within 120 days of closing Title Documents 90 days of closing POP QUIZ!!! 1) How many days prior to application can the borrowers paystub be dated? 2) How many days prior to application can the borrowers bank statement be dated?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}