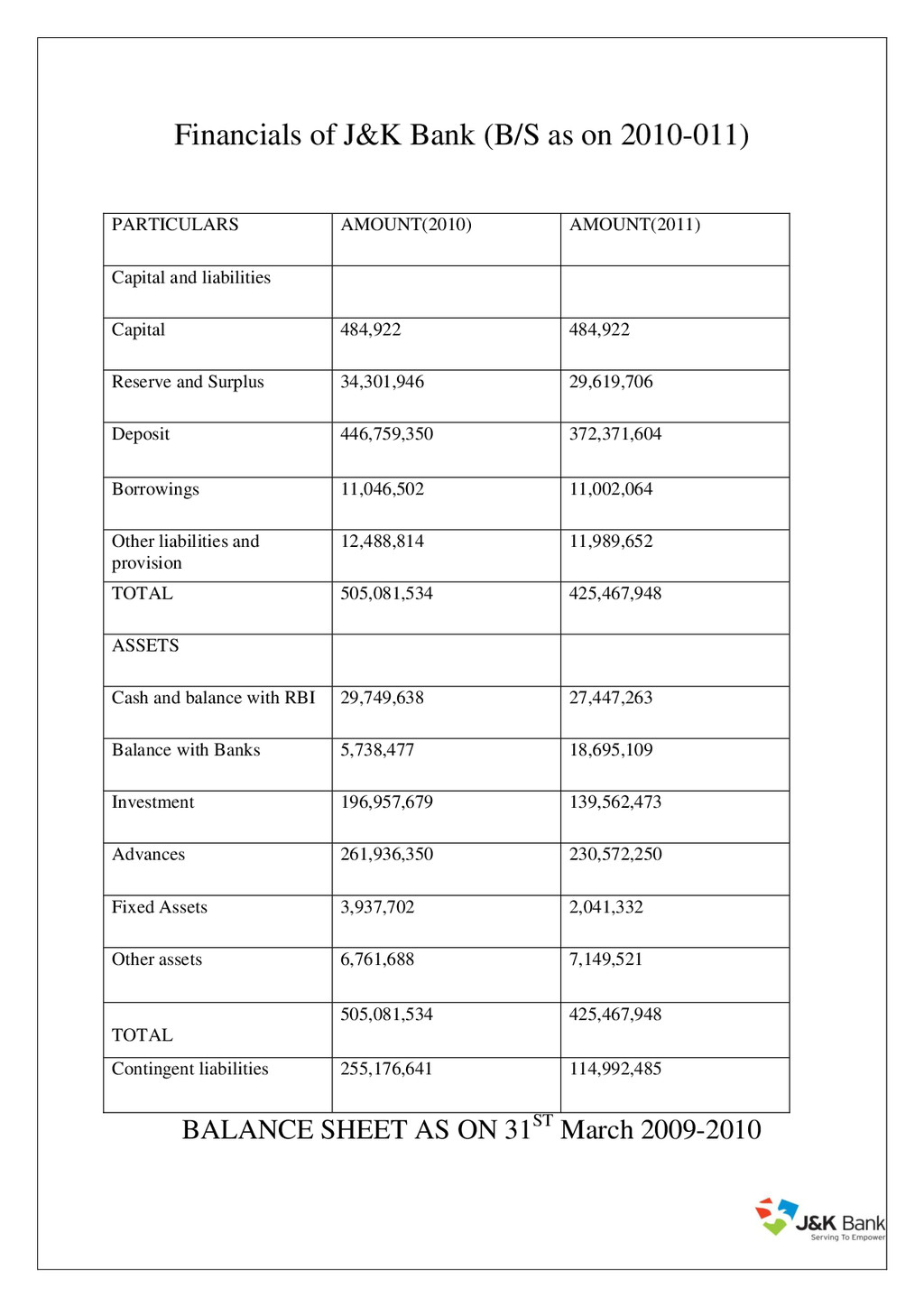

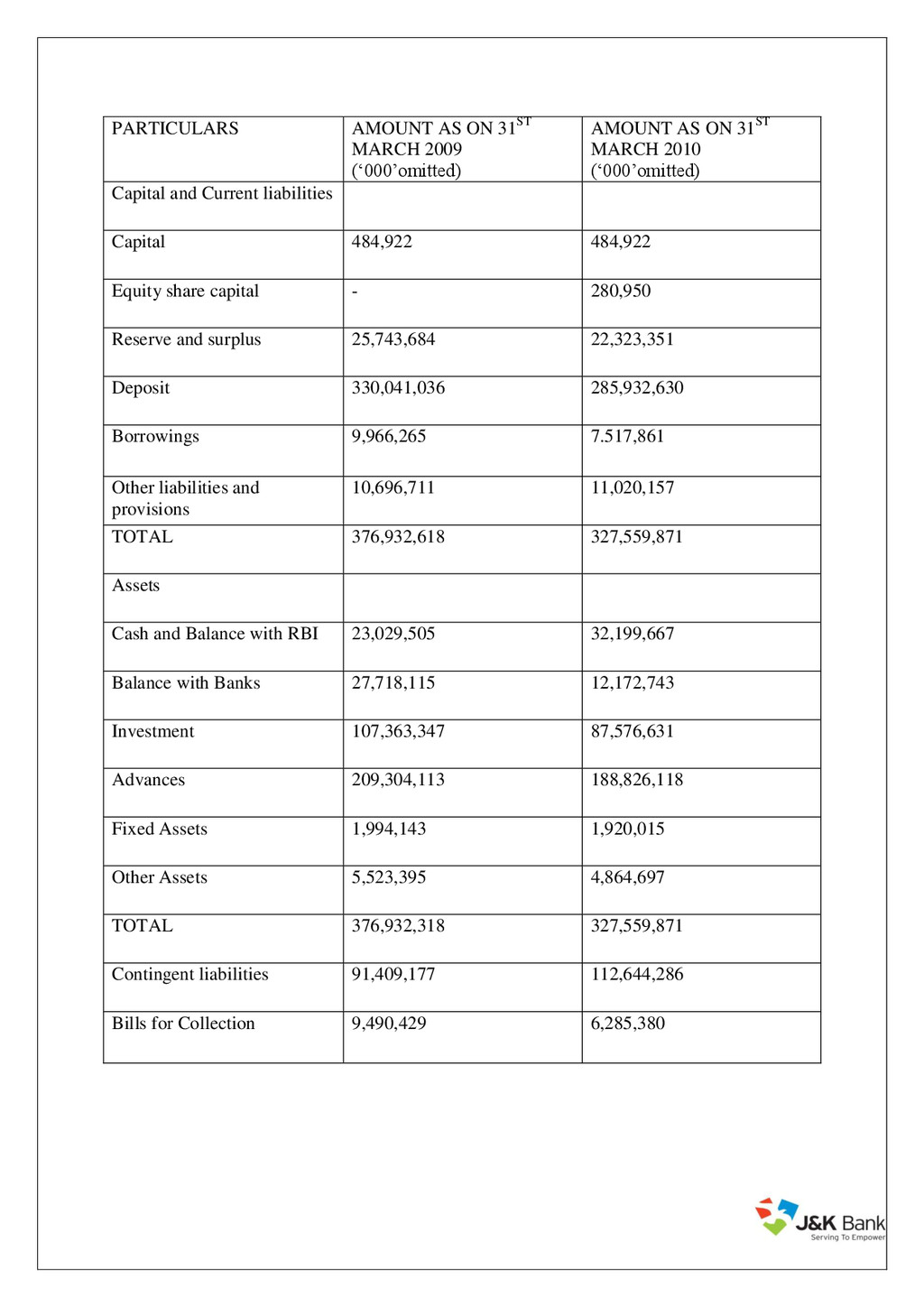

ON 31ST MARCH 2010 („000‟omitted) Capital and Current liabilities Capital 484,922 484,922 Equity share capital - 280,950 Reserve and surplus 25,743,684 22,323,351 Deposit 330,041,036 285,932,630 Borrowings 9,966,265 7.517,861 Other liabilities and provisions 10,696,711 11,020,157 TOTAL 376,932,618 327,559,871 Assets Cash and Balance with RBI 23,029,505 32,199,667 Balance with Banks 27,718,115 12,172,743 Investment 107,363,347 87,576,631 Advances 209,304,113 188,826,118 Fixed Assets 1,994,143 1,920,015 Other Assets 5,523,395 4,864,697 TOTAL 376,932,318 327,559,871 Contingent liabilities 91,409,177 112,644,286 Bills for Collection 9,490,429 6,285,380

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}