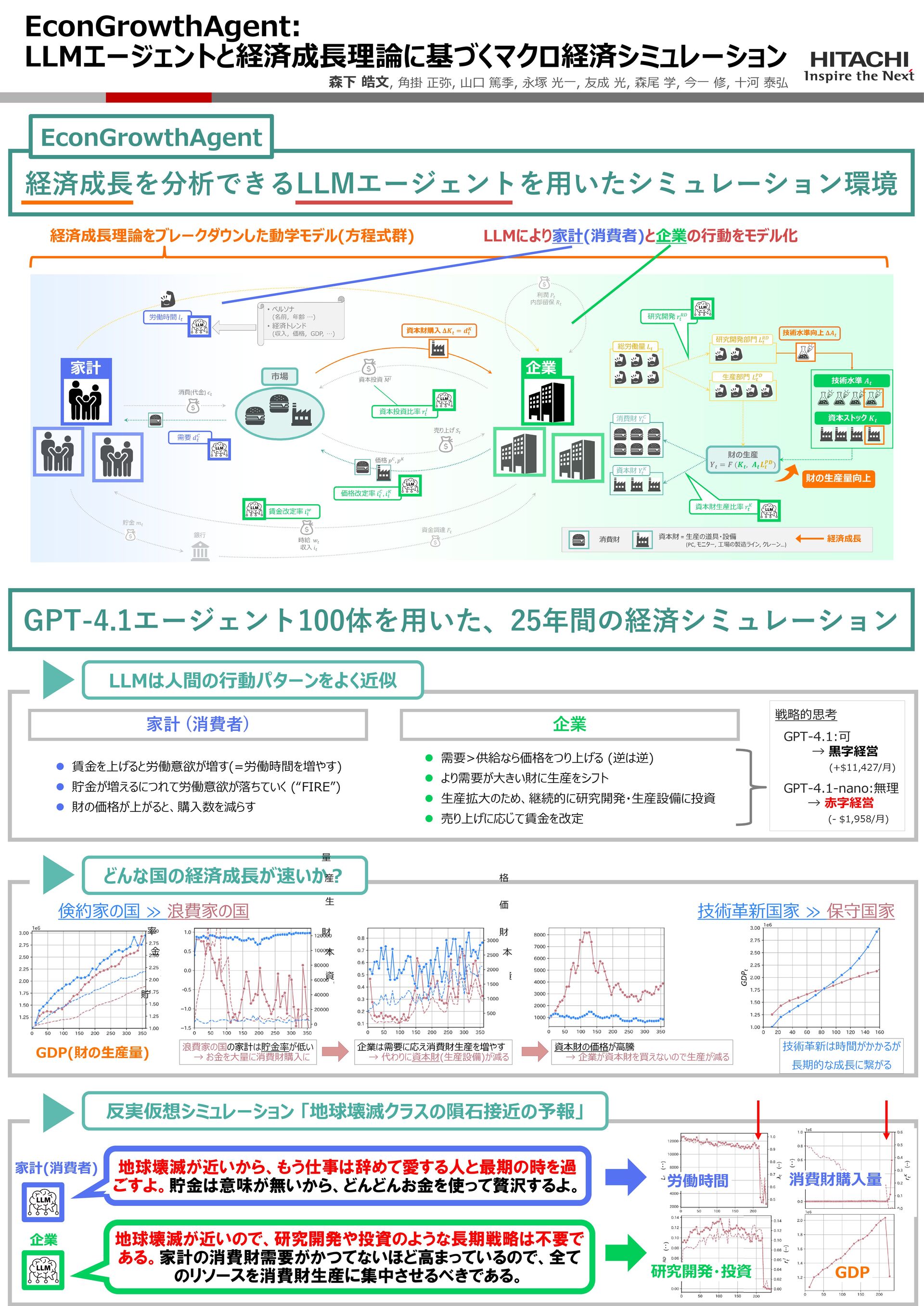

factors, “capital stock accumulation through 128 investment” and “technological innovation through R&D”, assuming given and fixed ratios for 129 investment (s) and R&D (r0). However, in reality, these factors arise from interactions among 130 micro-level decisions of economic agents, such as firms and households. Without this micro-level 131 lens, a comprehensive analysis of growth is impossible. 132 We therefore first break down growth theory into a system of dynamic equations describing how micro- 133 level decisions and other economic variables interact and evolve. We model capital accumulation 134 through a process where firms produce and sell capital goods, while other firms buy them to use in 135 their production. Similarly, we model technological innovation through firms allocating a portion 136 of labor to R&D, raising their technology levels. Furthermore, these decisions can be influenced by 137 those made within the same firms, as well as by other firms and households. For instance, funds for 138 purchasing capital goods come from previous sales, which depend on firm-set prices, competitors’ 139 prices, and household demand, while R&D labor depends on the labor supplied by households. Thus, 140 we enumerate a wide range of decision types for both firms and households, together with all relevant 141 interactions. 142 Then, we implement LLM agents to drive these dynamics with realistic decisions of households and 143 firms, creating an executable simulation environment named EconGrowthAgent (Figure 1). 144 3.1 LLM Agents 145 Assume NH household agents and NF firm agents. Each household h ∈ [1, NH] is assigned a 146 random persona prompt Pr(h)—including name, age, job, and residence—to approximate real-world 147 diversity. For decision-making, it receives a decision prompt DH listing decision items (e.g., “How 148 many goods to buy?”) and an economic trend prompt E(h) t providing variables up to timestep t 149 (month), such as income, goods prices and previous consumption, to support rational decisions. 150 For counterfactual simulations, it receives a counterfactual prompt Ct (e.g., “a novel infection X is 151 spreading”). We concatenate these into a single prompt PH(h) t = Pr(h) ⊕ DH ⊕ E(h) t ⊕ Ct to query 152 LLMs. 153 Likewise, each firm f ∈ [1, NF ] receives PF (f) t = Pr(f) ⊕ DF ⊕ E(f) t ⊕ Ct. E(f) t includes 154 firm-related variables (e.g., past demand and sales). See Appendix E for the details and LLM outputs. 155 4

{kind=link}

{kind=link}

{kind=link}