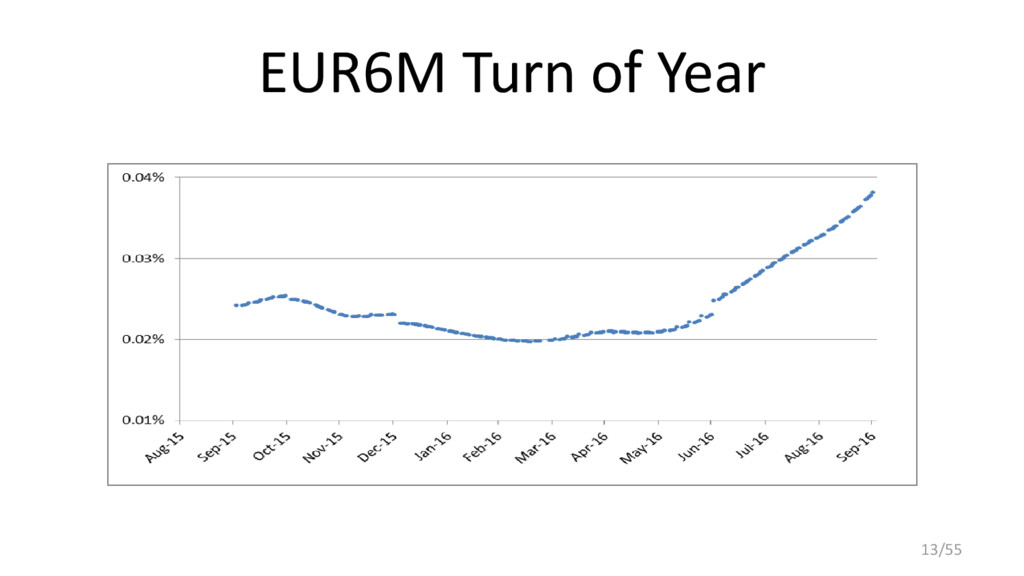

Presented at QuantLib User Meeting, London, July 12, 2016

Working Paper: http://ssrn.com/abstract=2696743

GitHub: https://github.com/paolomazzocchi/abcd_basis_spreads

Speaker Deck: https://speakerdeck.com/nando1970/the-abcd-of-interest-rate-basis-spreads

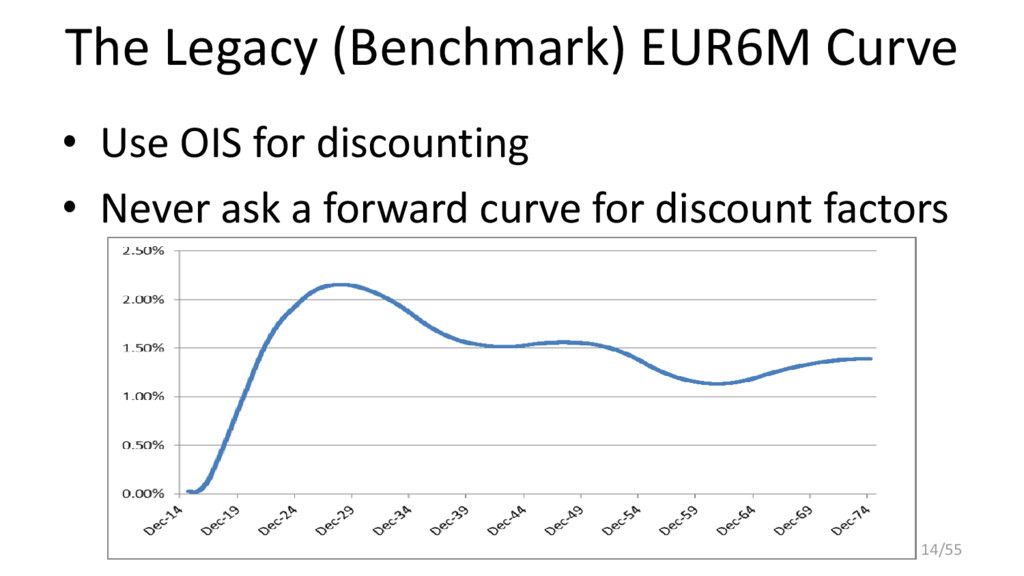

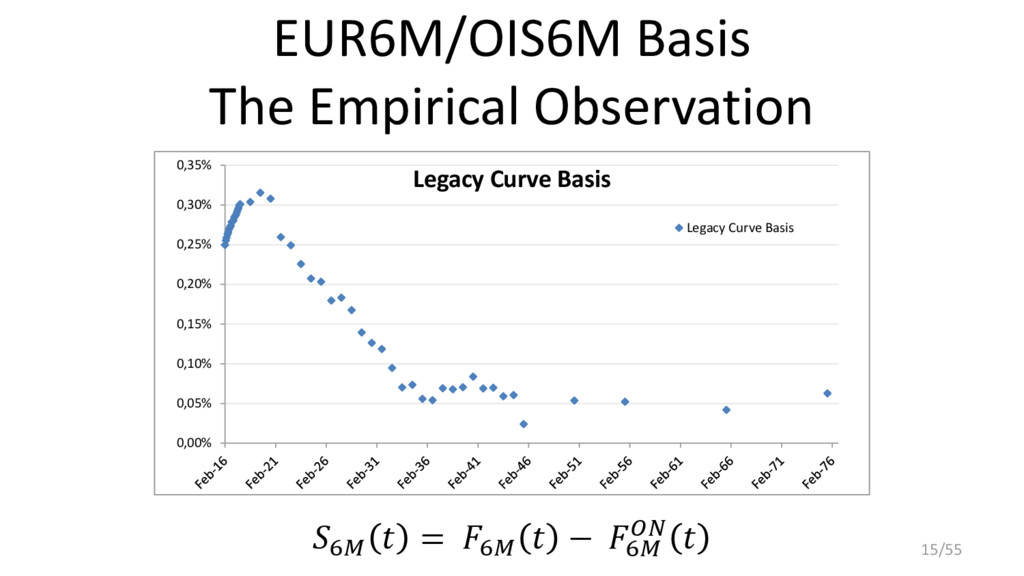

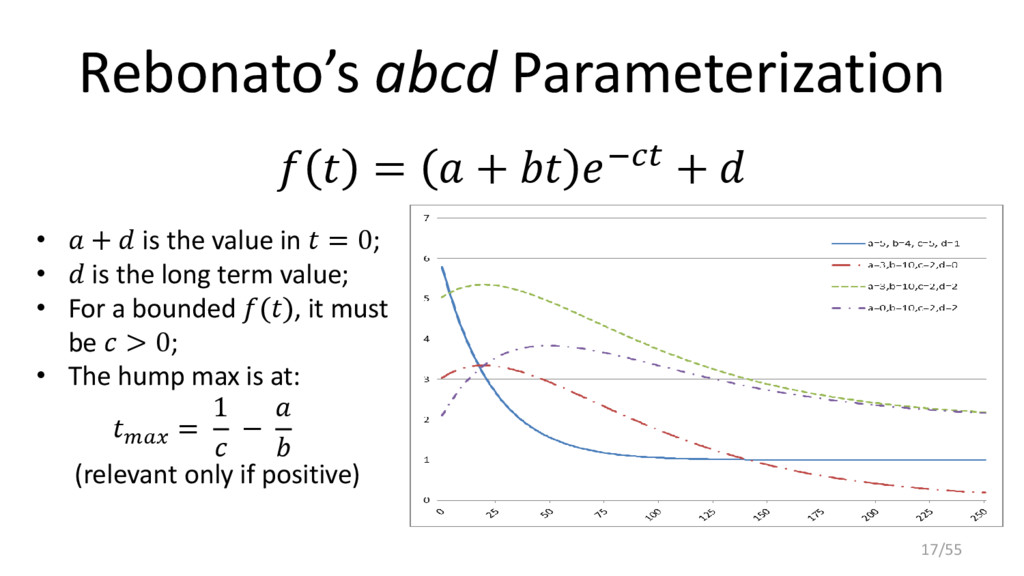

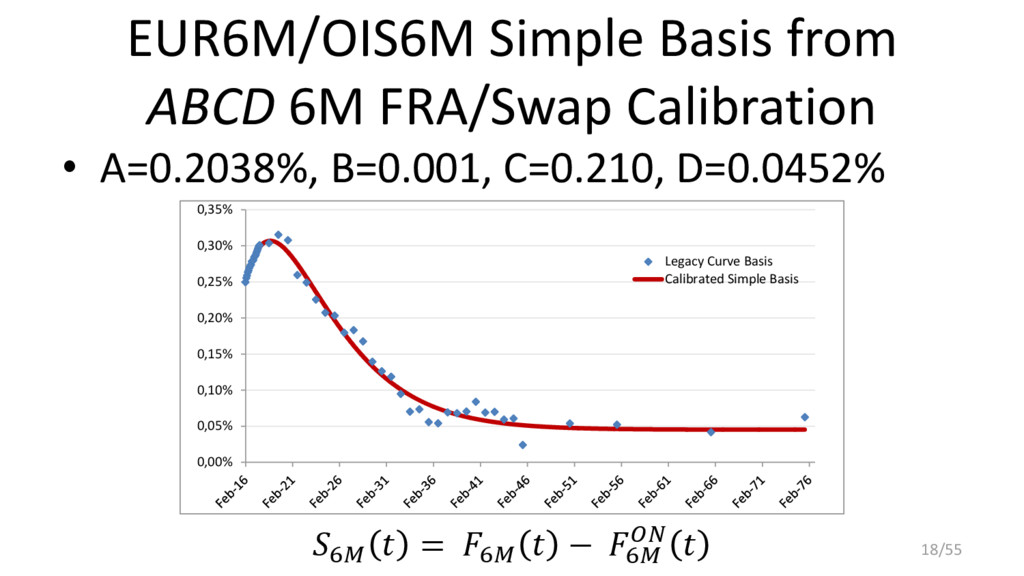

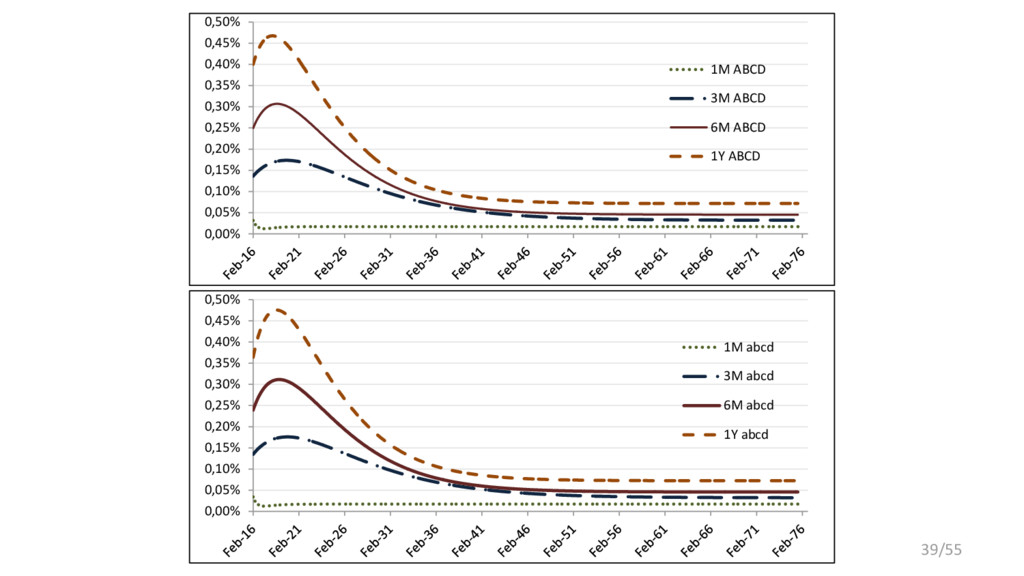

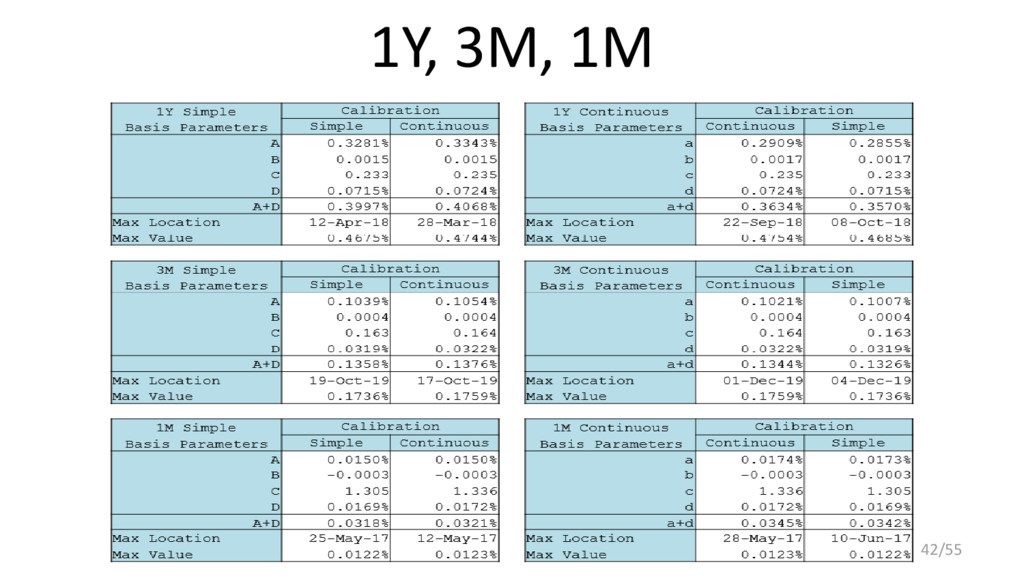

We show that forward rates can be modeled as abcd parametric tenor basis spreads over the underlying overnight rate curve. This is possible for both continuously and simply compounded forward rates, with a simple approximation for converting between the corresponding basis. Increasing interest-rate tenor dominance, as empirically observed, is recovered and can be structurally enforced using a robust methodology improvement based on relative basis between the most liquid tenors. The smoothness requirement is moved from forward rate curves to tenor basis curves, properly dealing with the market evidence of jumps in forward rates. In the case of continuously compounded tenor basis, pseudo-discount factors are also available. An implementation of this methodology is available in the QuantLib open-source project.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![EUR6M abcd Errors Exact-Fit with ∈ [0.9984, 1.0005] 37/55](https://files.speakerdeck.com/presentations/17891bdffcc449a681947b814a2e76f8/slide_36.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![EUR3M abcd Errors Exact-Fit with ∈ [0.9980, 1.0026] 43/55](https://files.speakerdeck.com/presentations/17891bdffcc449a681947b814a2e76f8/slide_42.jpg){kind=link}

![EUR1M abcd Errors Exact-Fit with ∈ [0.9994, 1.0020] 44/55](https://files.speakerdeck.com/presentations/17891bdffcc449a681947b814a2e76f8/slide_43.jpg){kind=link}

![EUR1Y abcd Errors Exact-Fit with ∈ [0.9998, 1.0019] 45/55](https://files.speakerdeck.com/presentations/17891bdffcc449a681947b814a2e76f8/slide_44.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}