Challenges Consuming Programmable Telecoms from the Developer’s Perspective

- App development: I just want to make a call

- Consuming APIs: It’s all fine as long as you know what you want and have done it before

- App development vs. Telecom App development

Presented 2019-11-19 at TADSummit in London, UK

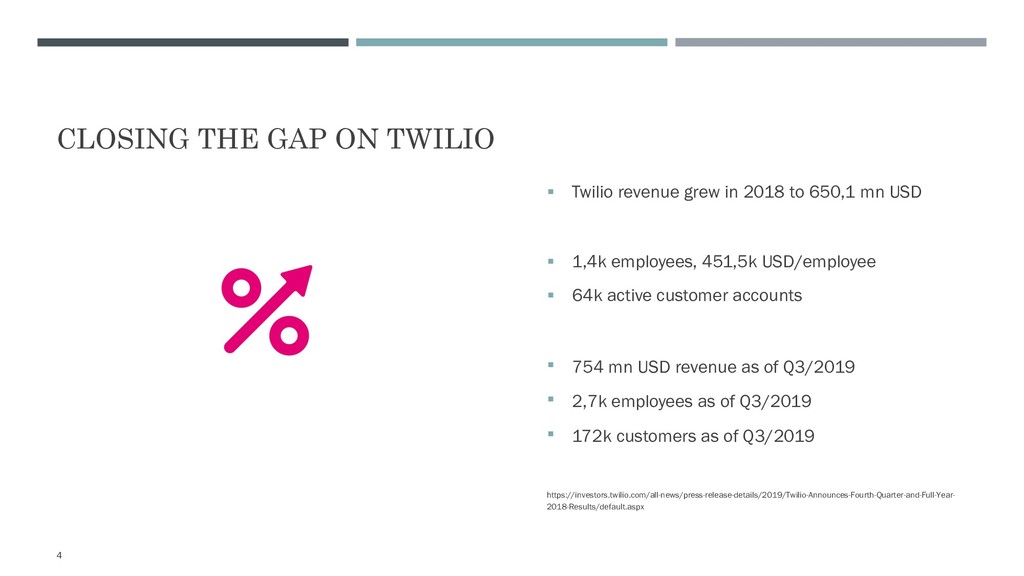

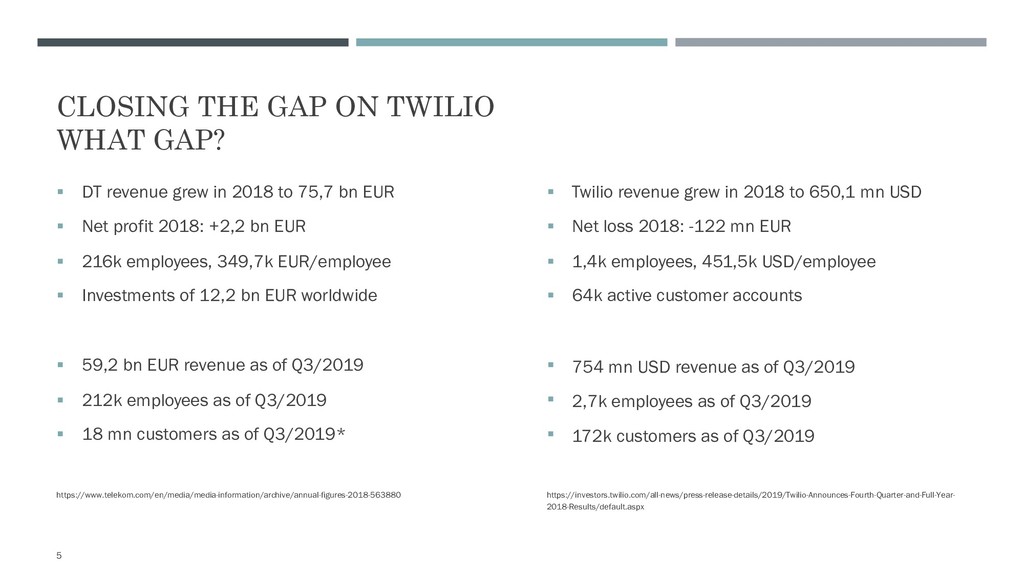

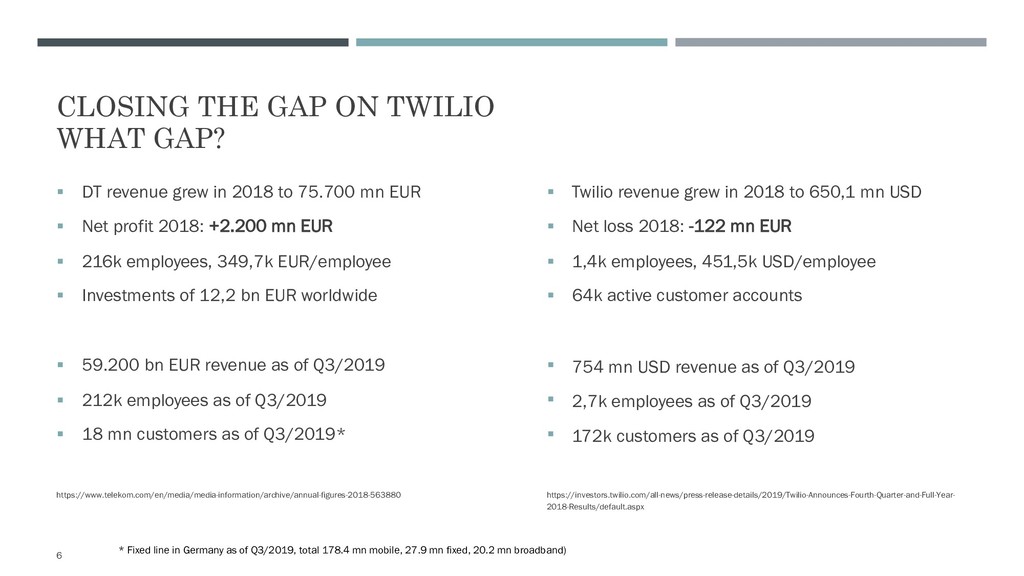

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}