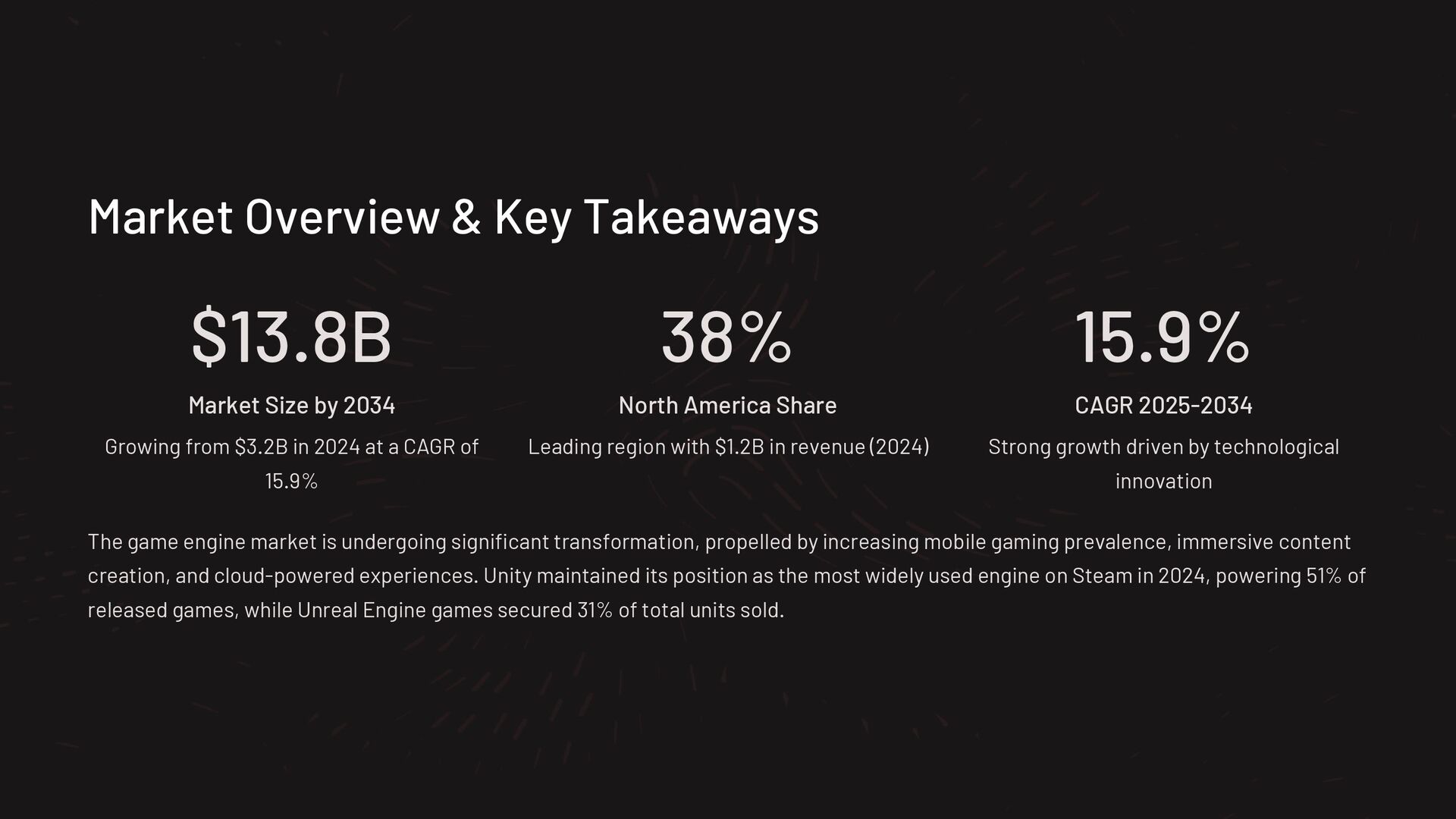

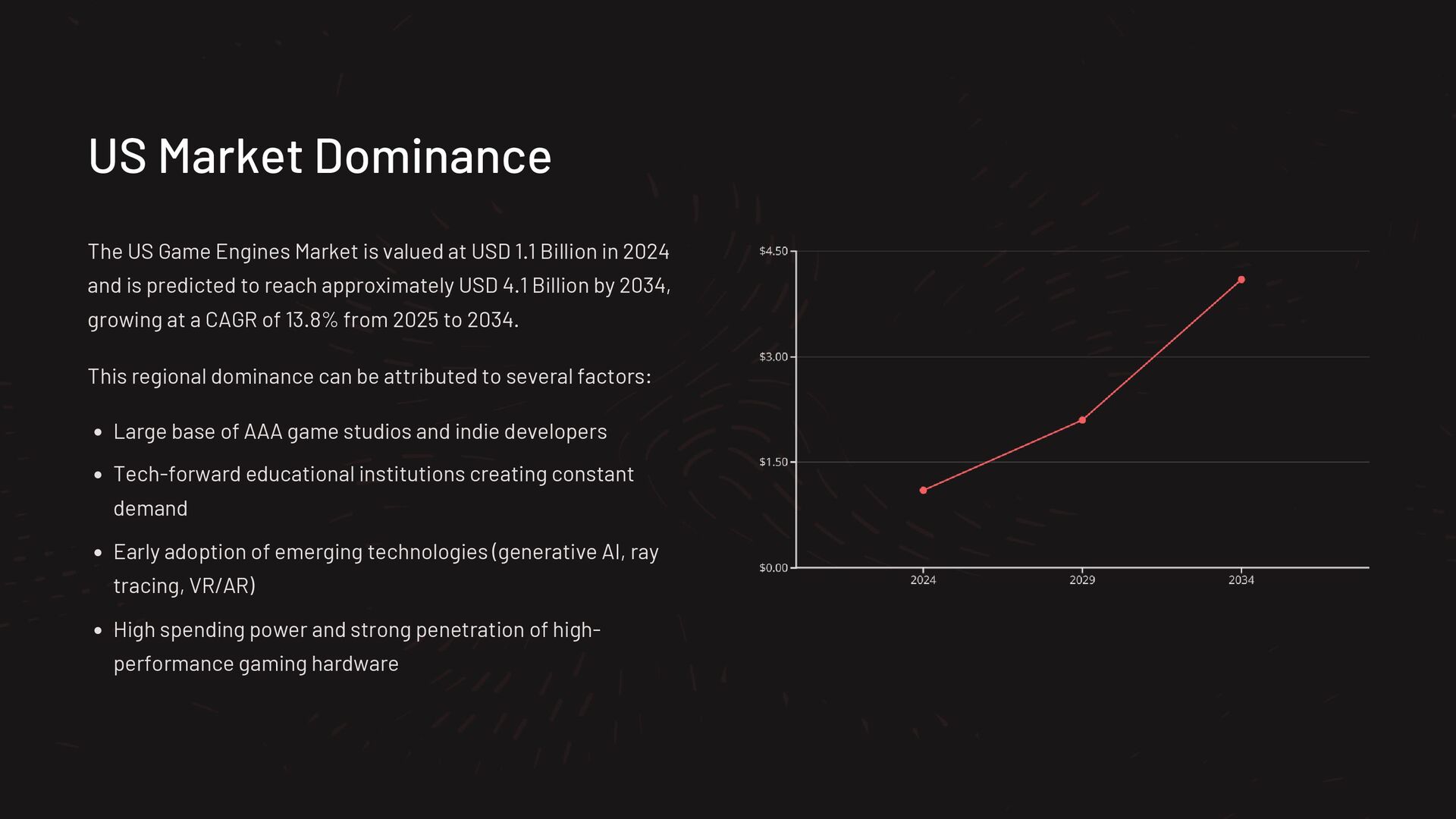

The global game engines market is projected to expand significantly, reaching approximately USD 13.8 Billion by 2034, up from USD 3.2 Billion in 2024, at a robust CAGR of 15.9% over the forecast period. North America led the global landscape, capturing over 38% of the total market, driven by a mature developer ecosystem and the presence of major gaming studios. The U.S. market alone generated USD 1.12 Billion, growing steadily at a CAGR of 13.8%, supported by increased investment in high-quality, immersive game content.

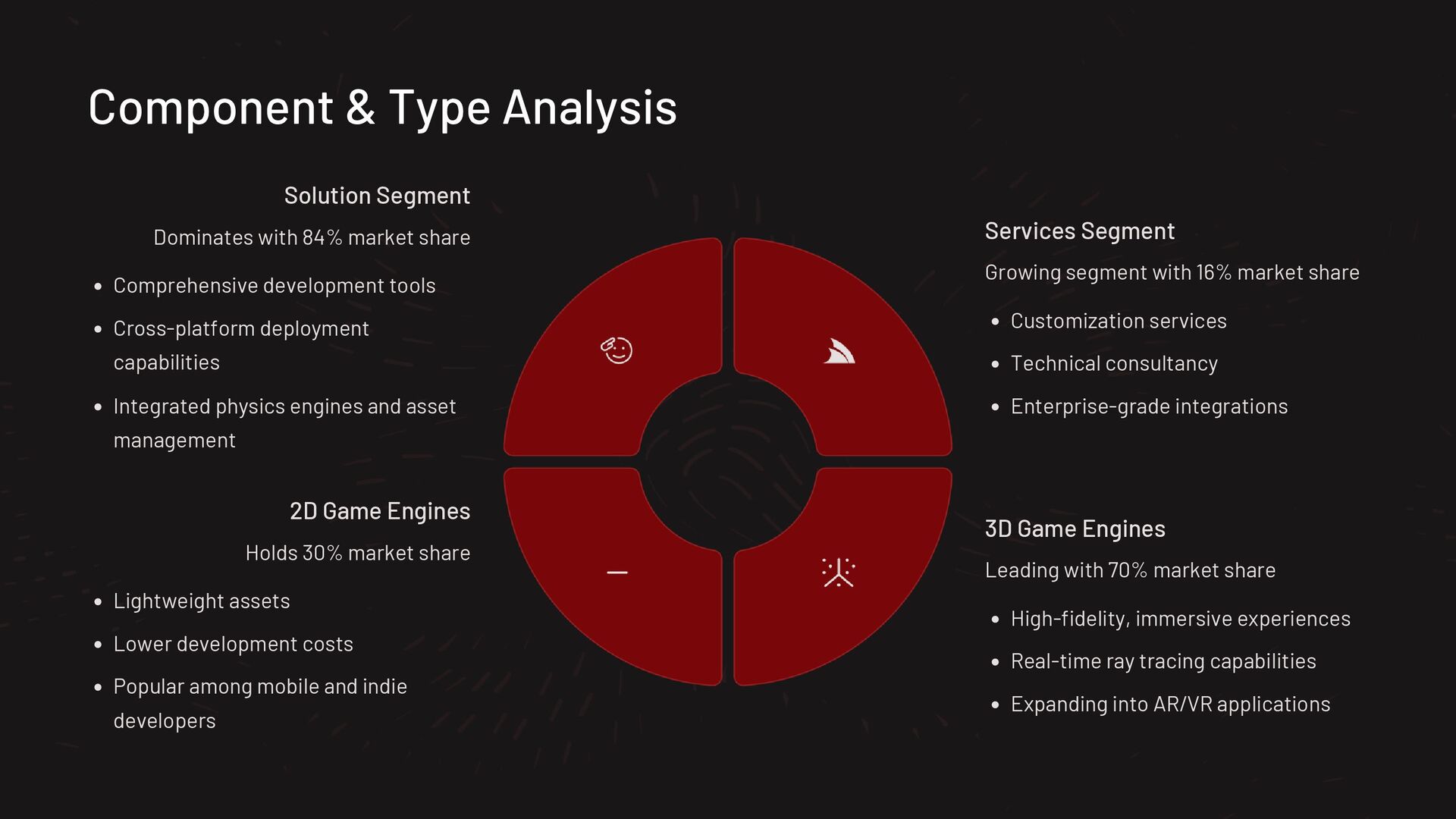

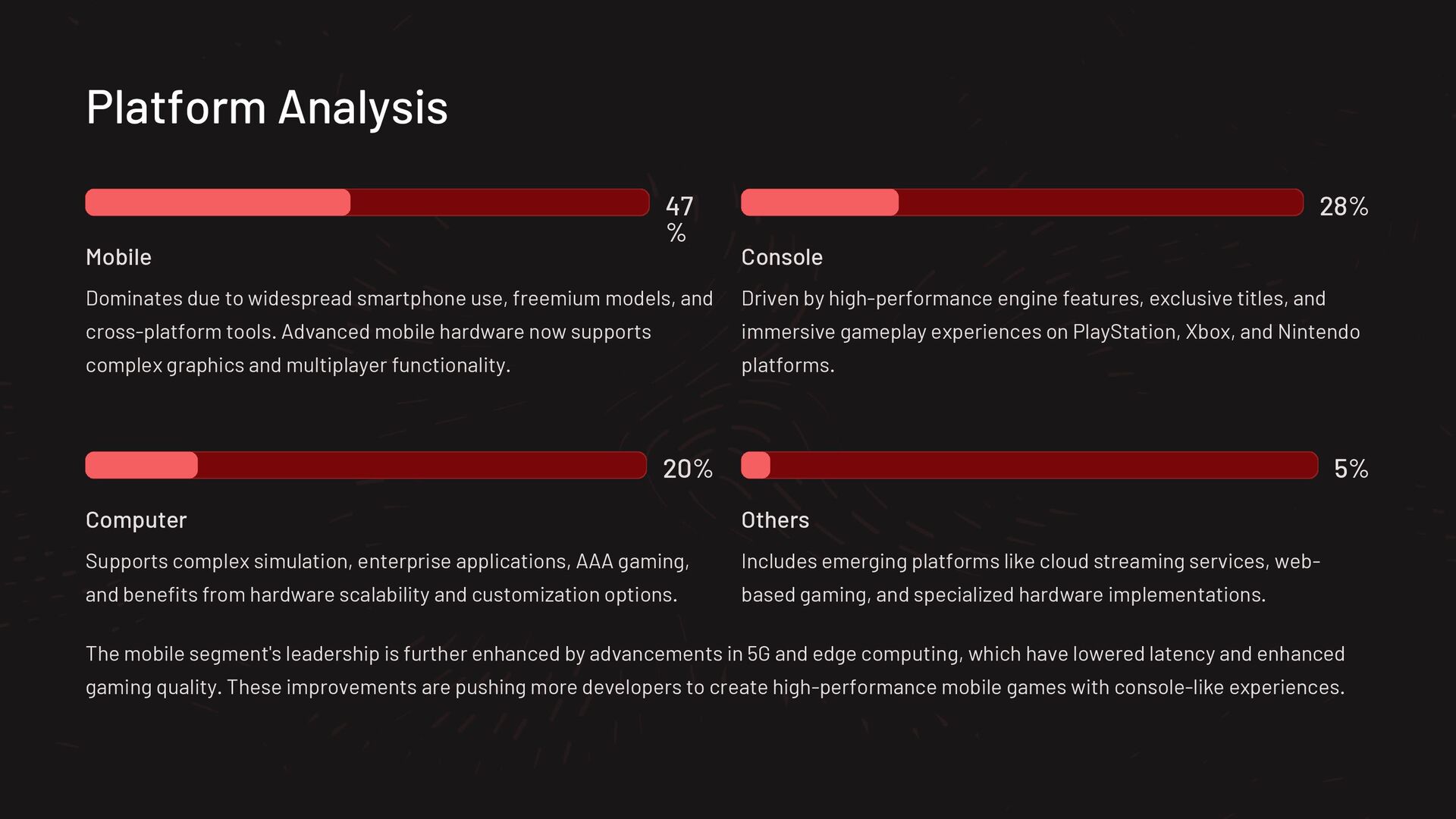

By component, the Solution segment dominated with an 84% share, as game developers favored comprehensive engine platforms that offer rendering, physics, and real-time simulation in a unified package. In terms of technology, 3D game engines held a dominant 70% share, reflecting a clear shift towards high-fidelity graphics and realistic environments that enhance user experience. Mobile platforms emerged as the largest segment, accounting for 47% of market share, driven by the explosive rise of mobile gaming, particularly in Asia-Pacific and emerging markets.

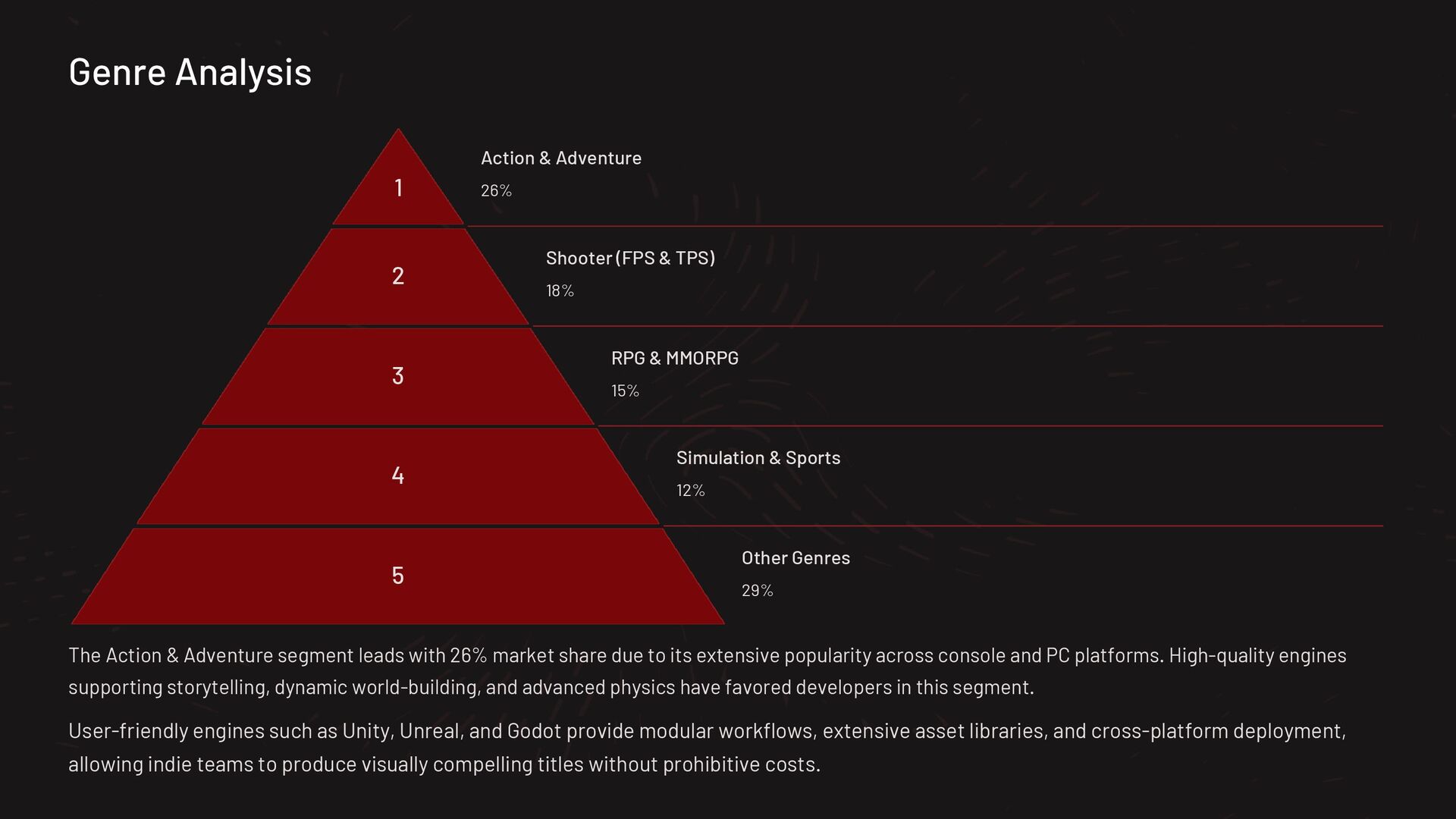

Among game genres, Action & Adventure led the market, contributing 26% share, as these titles attract large audiences through engaging narratives and dynamic gameplay. The rising demand for cross-platform compatibility, enhanced visual storytelling, and AI-driven content generation continues to shape the evolution of the game engine landscape globally.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}