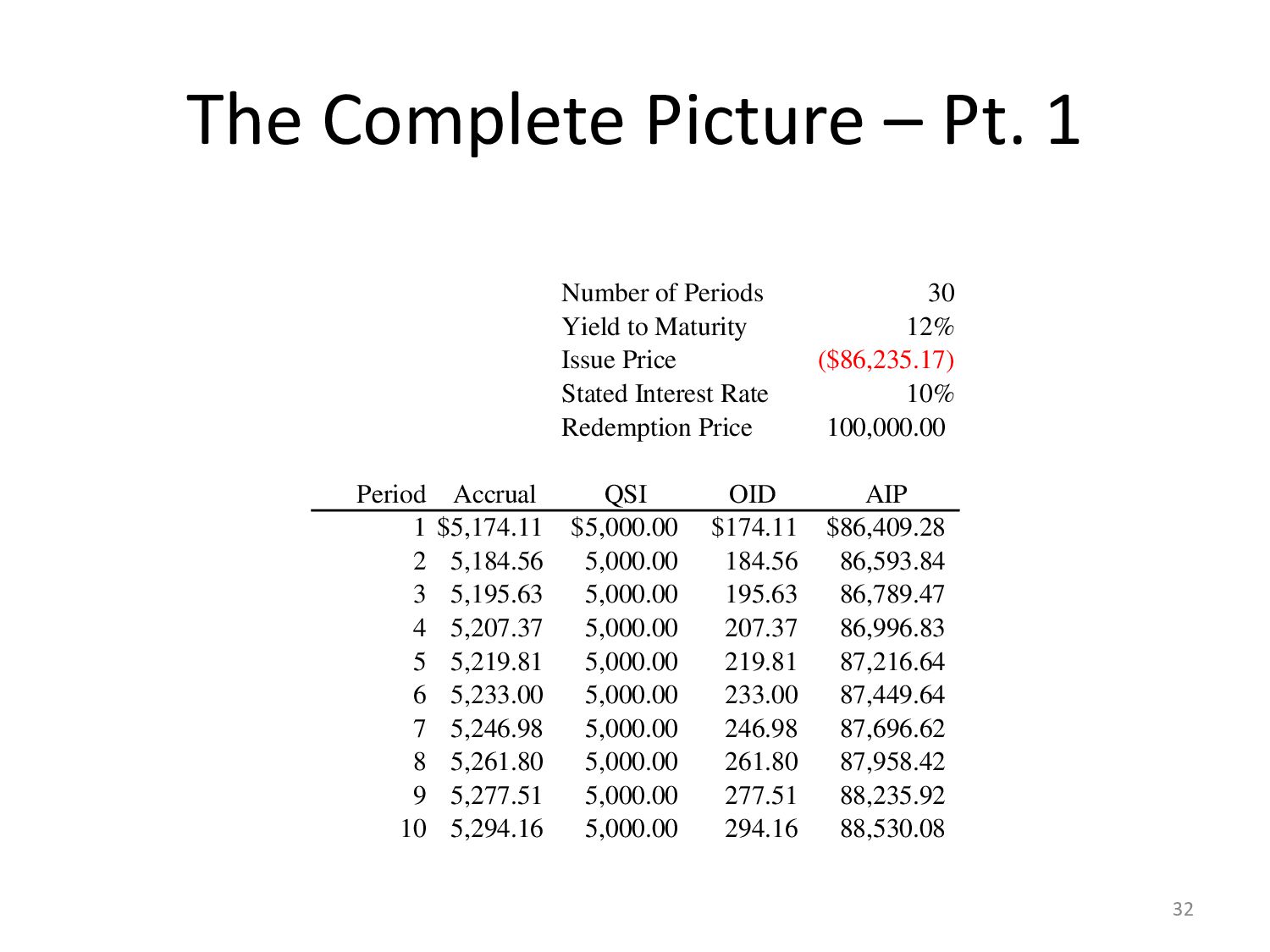

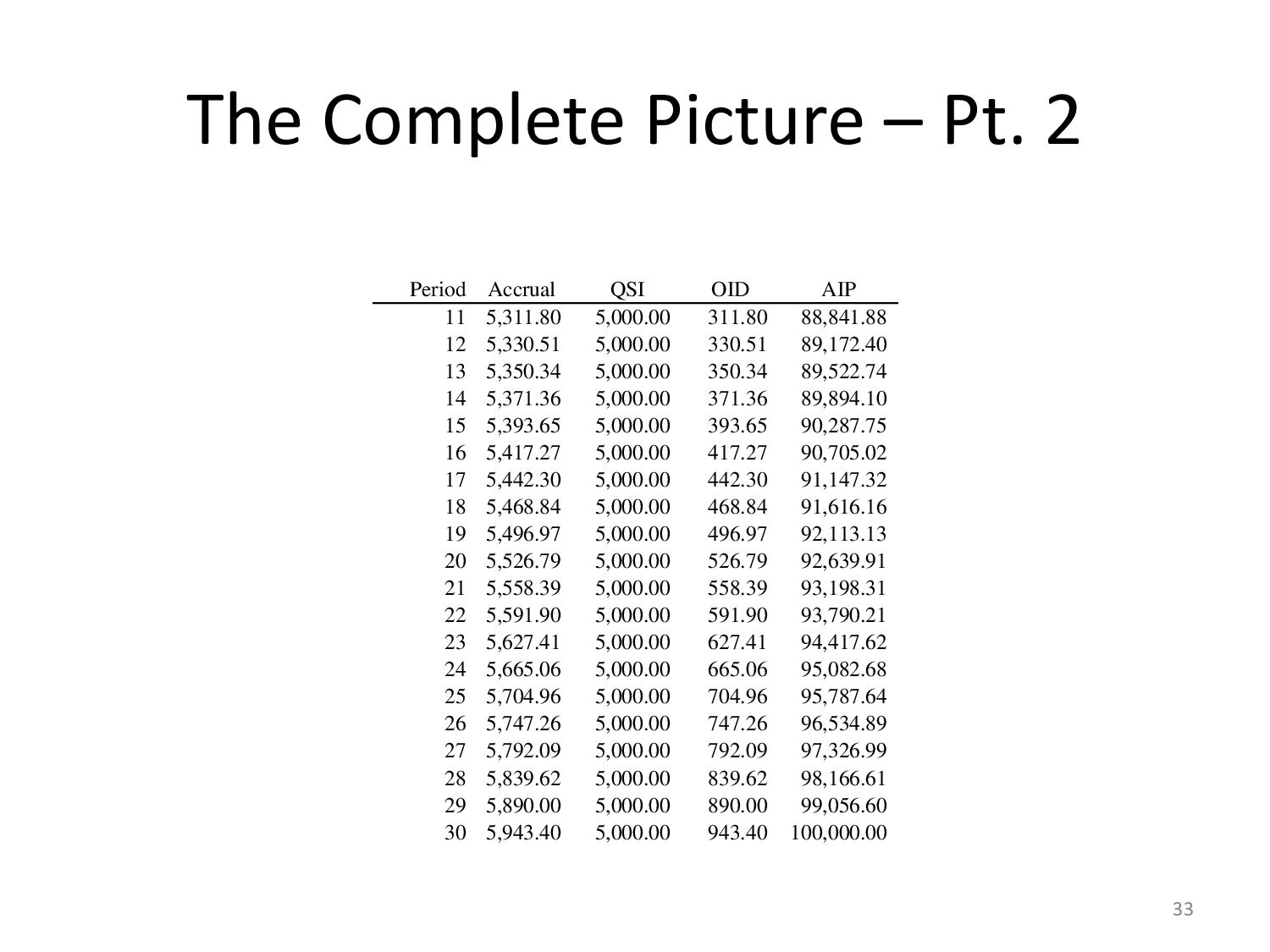

AIP 11 5,311.80 5,000.00 311.80 88,841.88 12 5,330.51 5,000.00 330.51 89,172.40 13 5,350.34 5,000.00 350.34 89,522.74 14 5,371.36 5,000.00 371.36 89,894.10 15 5,393.65 5,000.00 393.65 90,287.75 16 5,417.27 5,000.00 417.27 90,705.02 17 5,442.30 5,000.00 442.30 91,147.32 18 5,468.84 5,000.00 468.84 91,616.16 19 5,496.97 5,000.00 496.97 92,113.13 20 5,526.79 5,000.00 526.79 92,639.91 21 5,558.39 5,000.00 558.39 93,198.31 22 5,591.90 5,000.00 591.90 93,790.21 23 5,627.41 5,000.00 627.41 94,417.62 24 5,665.06 5,000.00 665.06 95,082.68 25 5,704.96 5,000.00 704.96 95,787.64 26 5,747.26 5,000.00 747.26 96,534.89 27 5,792.09 5,000.00 792.09 97,326.99 28 5,839.62 5,000.00 839.62 98,166.61 29 5,890.00 5,000.00 890.00 99,056.60 30 5,943.40 5,000.00 943.40 100,000.00 33

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}