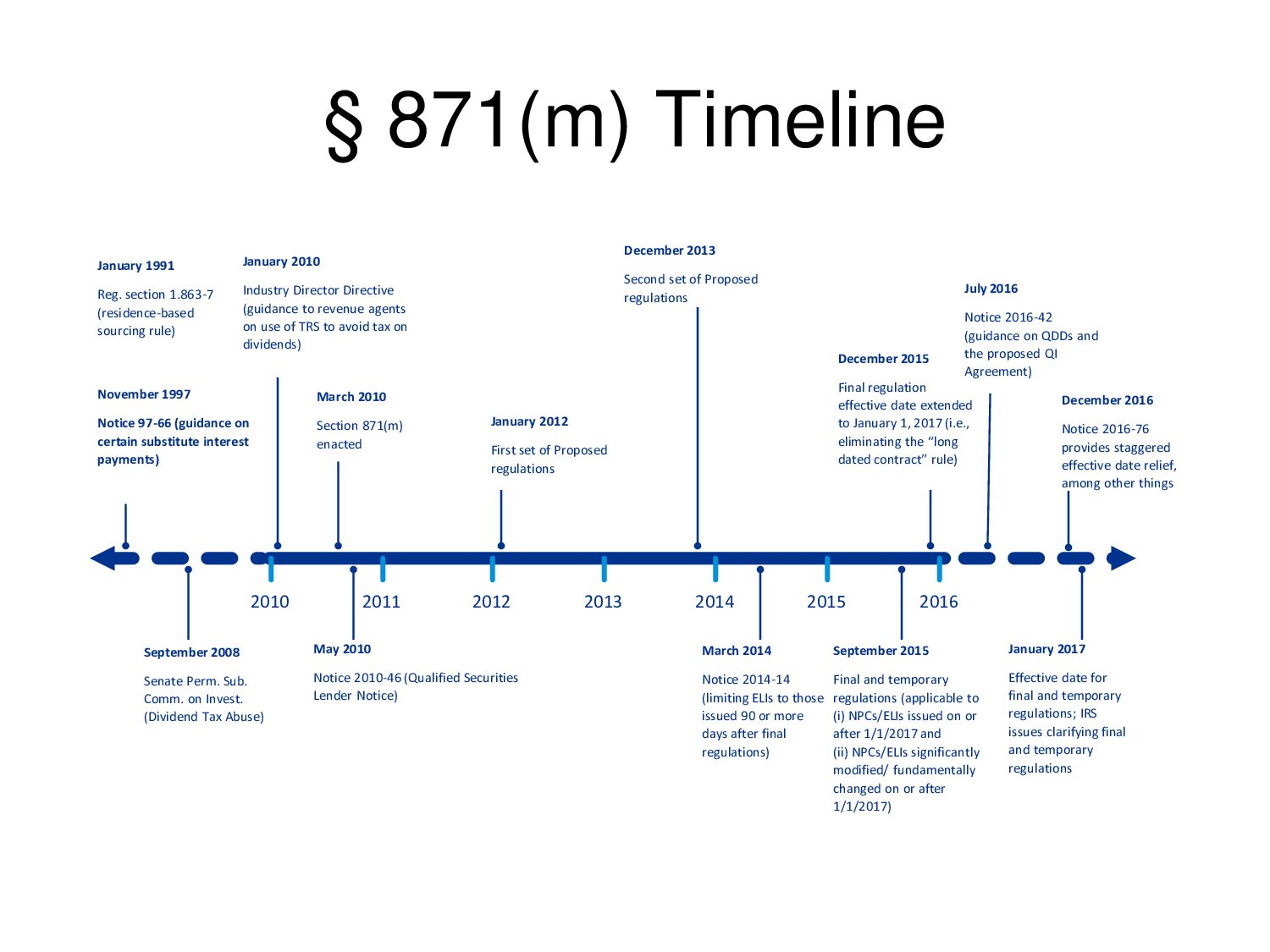

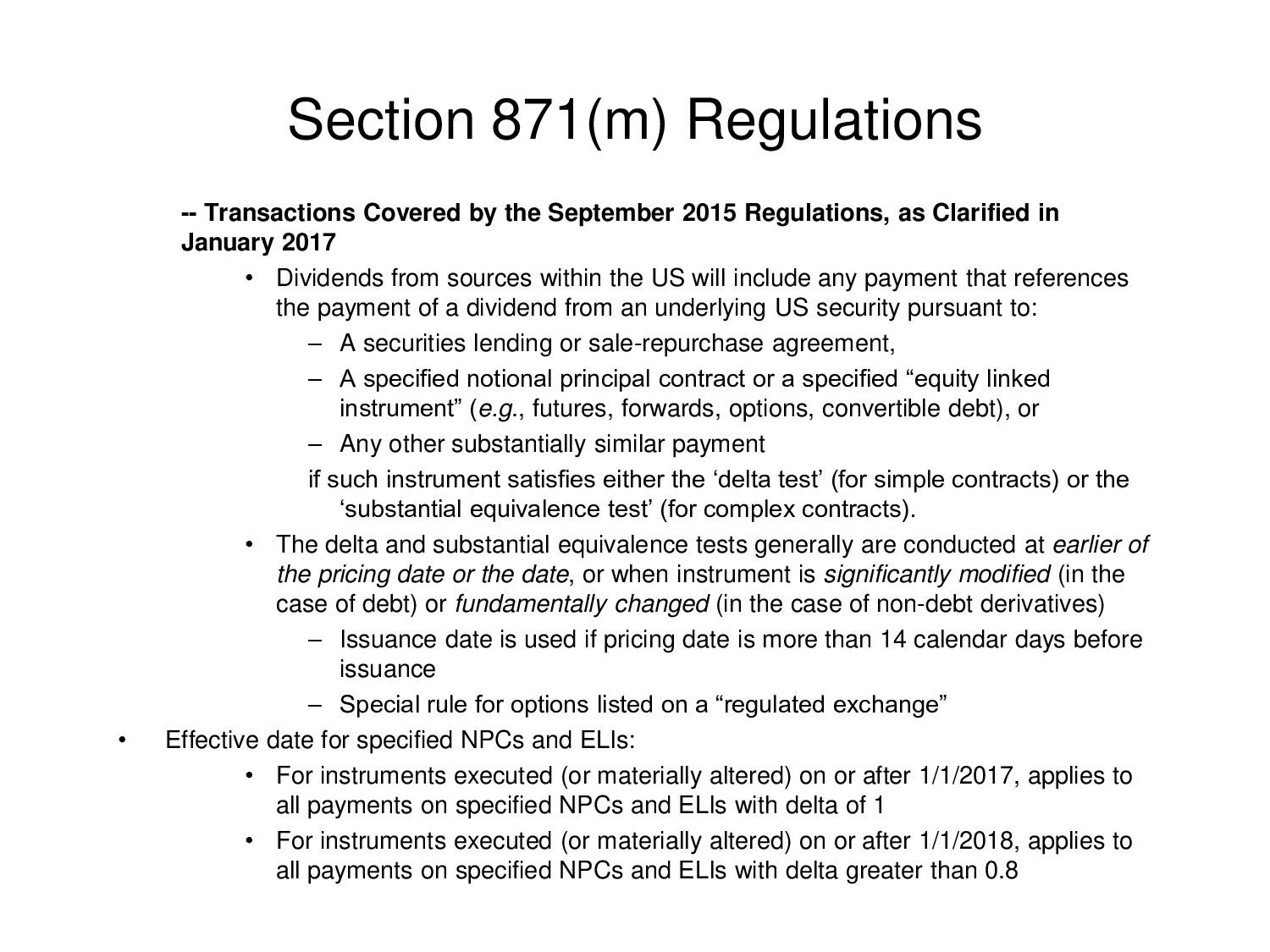

Regulations, as Clarified in January 2017 • Dividends from sources within the US will include any payment that references the payment of a dividend from an underlying US security pursuant to: – A securities lending or sale-repurchase agreement, – A specified notional principal contract or a specified “equity linked instrument” (e.g., futures, forwards, options, convertible debt), or – Any other substantially similar payment if such instrument satisfies either the ‘delta test’ (for simple contracts) or the ‘substantial equivalence test’ (for complex contracts). • The delta and substantial equivalence tests generally are conducted at earlier of the pricing date or the date, or when instrument is significantly modified (in the case of debt) or fundamentally changed (in the case of non-debt derivatives) – Issuance date is used if pricing date is more than 14 calendar days before issuance – Special rule for options listed on a “regulated exchange” • Effective date for specified NPCs and ELIs: • For instruments executed (or materially altered) on or after 1/1/2017, applies to all payments on specified NPCs and ELIs with delta of 1 • For instruments executed (or materially altered) on or after 1/1/2018, applies to all payments on specified NPCs and ELIs with delta greater than 0.8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}