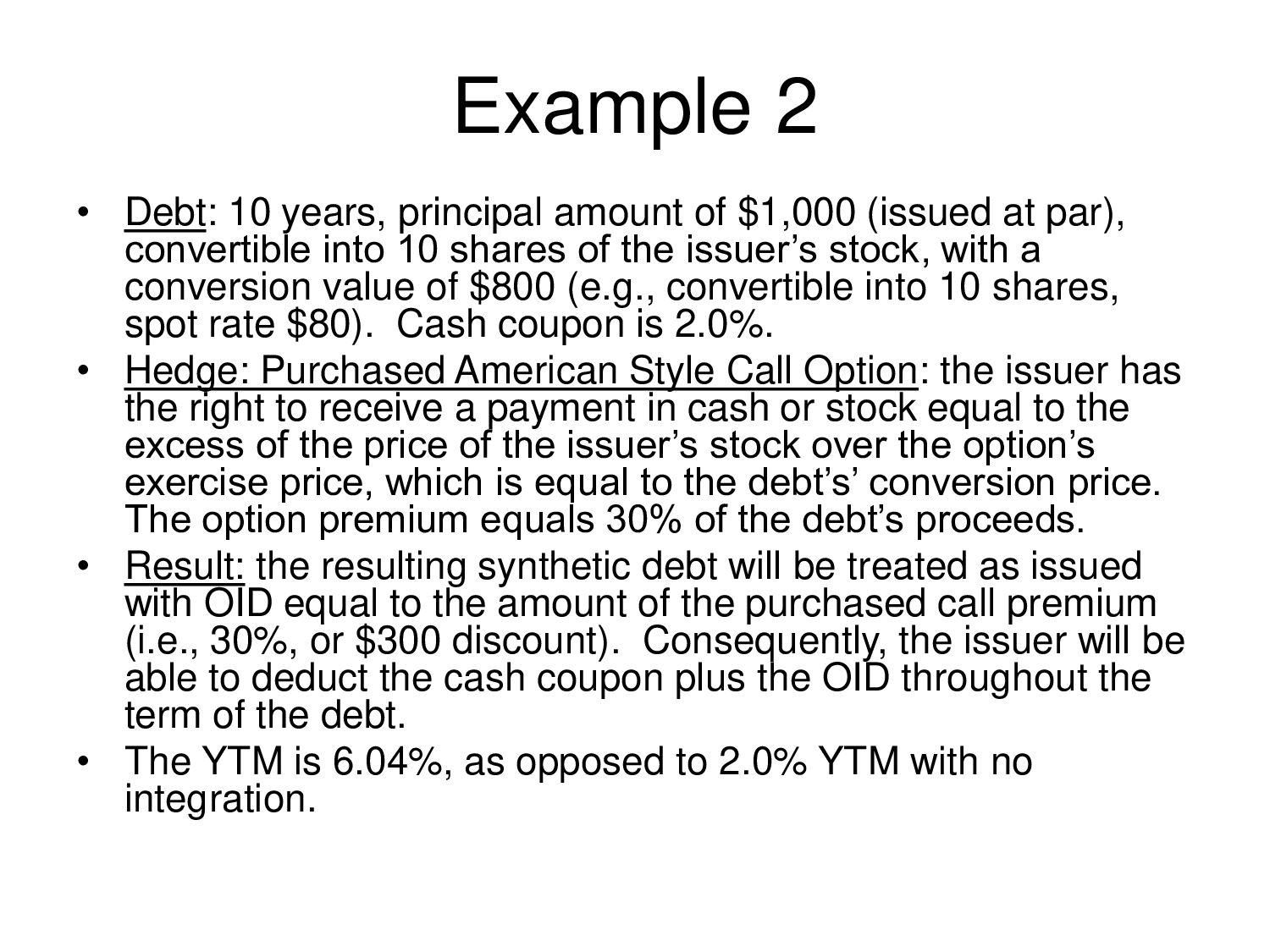

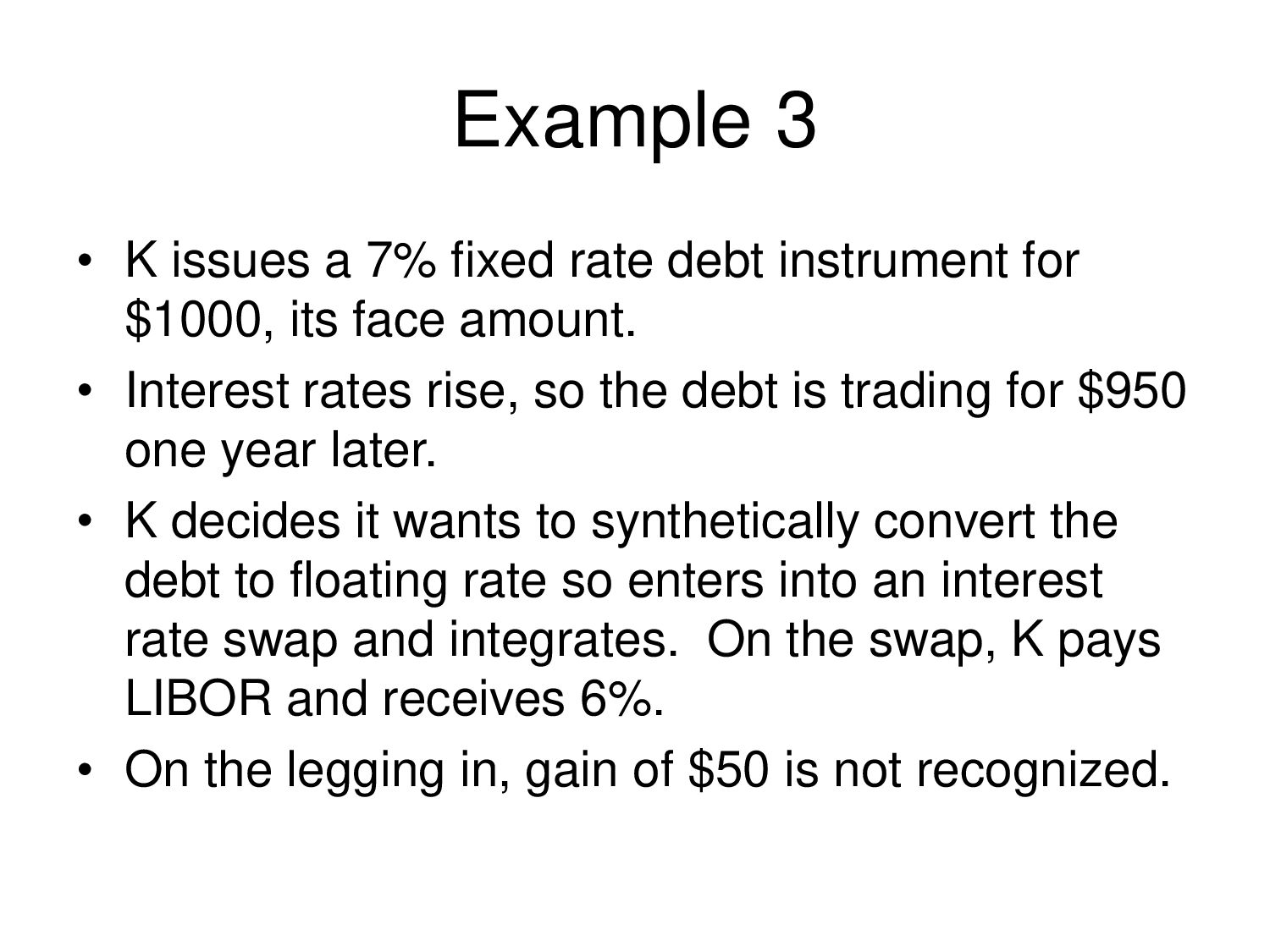

(issued at par), convertible into 10 shares of the issuer’s stock, with a conversion value of $800 (e.g., convertible into 10 shares, spot rate $80). Cash coupon is 2.0%. • Hedge: Purchased American Style Call Option: the issuer has the right to receive a payment in cash or stock equal to the excess of the price of the issuer’s stock over the option’s exercise price, which is equal to the debt’s’ conversion price. The option premium equals 30% of the debt’s proceeds. • Result: the resulting synthetic debt will be treated as issued with OID equal to the amount of the purchased call premium (i.e., 30%, or $300 discount). Consequently, the issuer will be able to deduct the cash coupon plus the OID throughout the term of the debt. • The YTM is 6.04%, as opposed to 2.0% YTM with no integration.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}