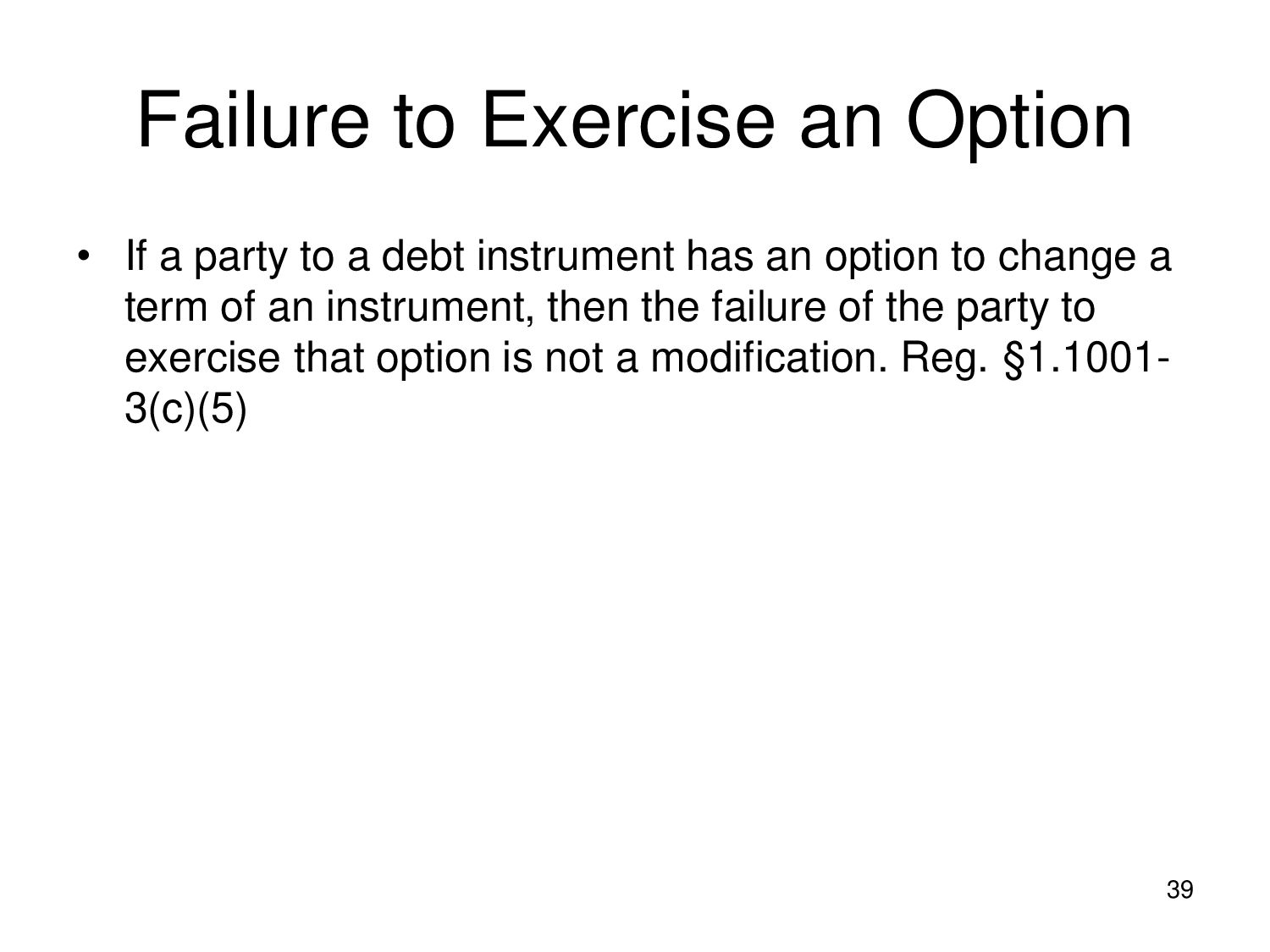

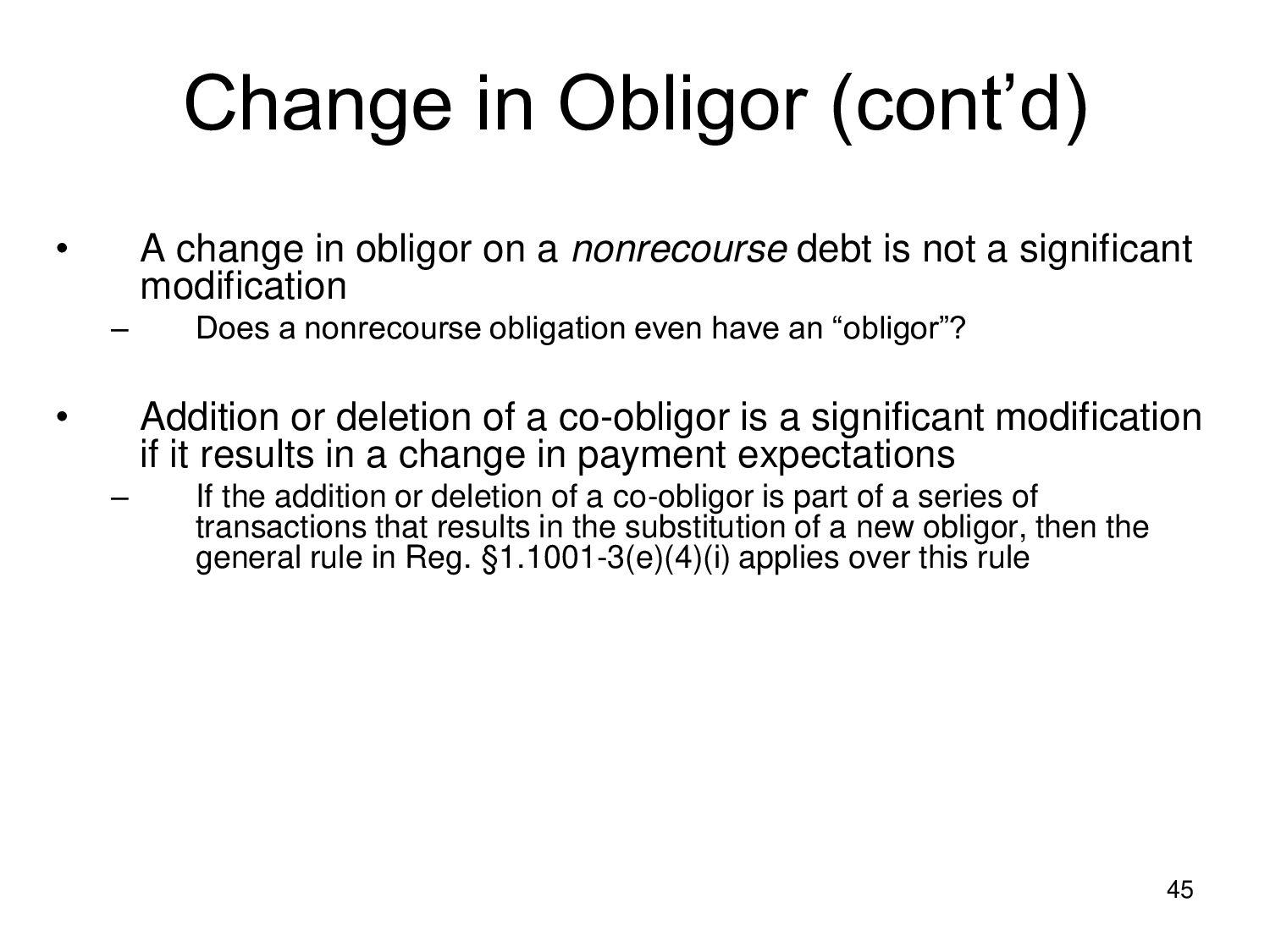

of the terms of a debt instrument generally are not considered modifications, even if they occur automatically or as a result of the exercise of a holder or issuer option to change a term of a debt instrument • Alterations that are considered modifications, even if they occur by operation of the terms of a debt instrument, include the following: (Reg. §1.1001-3(c)(2)) – Substitution of a new obligor, an addition or deletion of a co-obligor, or a change in the recourse nature of the debt; – Alterations that results in an instrument that is not debt, other than a holder’s option to convert a convertible debt to equity; and – Alterations arising from the exercise of an issuer or holder option, unless the option is “unilateral” and in the case of a holder option, the exercise of the option does not result in deferral of, or a reduction in, any scheduled payment of interest or principal • Unilateral if at the time of exercise, or as a result of exercise, the other party has no right to alter or terminate the instrument or put the instrument to a person who is related to the issuer; • Unilateral if the exercise does not require the consent or approval of the other party, a person related to the other party, or a court or arbitrator; and • Unilateral if the exercise does not requires consideration unless, on the issue date of the instrument, such consideration is a de minimis amount, a specified amount, or an amount based on a formula that uses objective financial information 37

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}