Living in the Post-COVID World and Finding Opportunity

A bit of research that we have recently published - living in the Post-COVID World and Finding Opportunity. Where can a business create the most value?

levels in most countries; there is an uncertainty in what to do and what strategy should organizations and Individuals undertake to survive. However, it is clear that the world will change and many things in it will be different. There will be many who lost, went bankrupt, destitute, but there will also be the winners, who adapted quicker and predicted the trends. May you live in interesting times - An English expression It will be a new world: - WORLD

of March, leading analytic agencies made claims about the rising expenditures on tech, the bets on digitization, and quantum technology. However, what came next is a Perfect Storm: Growing tension in the world (Chinese trade war, “Brexit”, …) Slowing of the Chinese economy; Falling of oil prices; Coronavirus pandemic; Not a single country was ready for a crisis at such scale. Economists estimate that it is commensurate to the Great Depression: The stop of the world economy (QUARANTINE); Medical crisis (not enough resources); Remote work en masse, pressure on online services. TECHNOLOGICAL TRENDS 2020 DIGITIZATION PRACTICAL AI SMART CITIES CYBER SECURITY INTERNET OF THINGS DISTRIBUTED REGISTRIES PRE CRISIS The Black Swan Theory

measures (relevant to both people and companies) 2 Understanding that the crisis is long-term and will bring significant change. But it is not forever; the crisis is not only a problem, but an opportunity. 3 Securing existing potential to prepare for the new world – Z World 4 Analyze trends and adjust the business- model Time to act is now 4 Analysis of trends and new business model

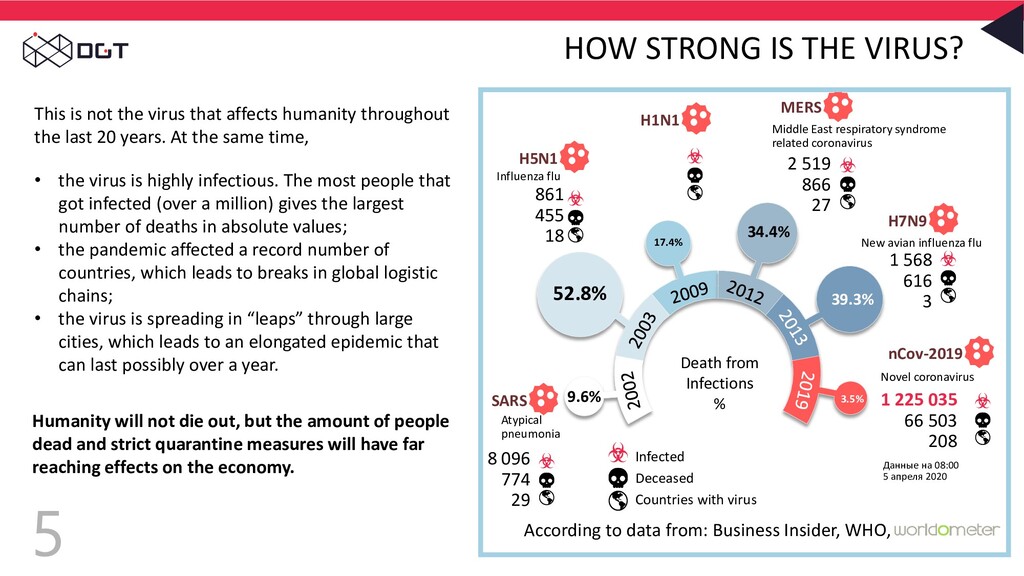

3.5% Death from Infections % nCov-2019 H7N9 MERS H1N1 H5N1 SARS Данные на 08:00 5 апреля 2020 1 225 035 66 503 208 Novel coronavirus 1 568 616 3 New avian influenza flu 2 519 866 27 Middle East respiratory syndrome related coronavirus 861 455 18 Influenza flu 8 096 774 29 Atypical pneumonia Infected Deceased Countries with virus According to data from: Business Insider, WHO, This is not the virus that affects humanity throughout the last 20 years. At the same time, • the virus is highly infectious. The most people that got infected (over a million) gives the largest number of deaths in absolute values; • the pandemic affected a record number of countries, which leads to breaks in global logistic chains; • the virus is spreading in “leaps” through large cities, which leads to an elongated epidemic that can last possibly over a year. Humanity will not die out, but the amount of people dead and strict quarantine measures will have far reaching effects on the economy.

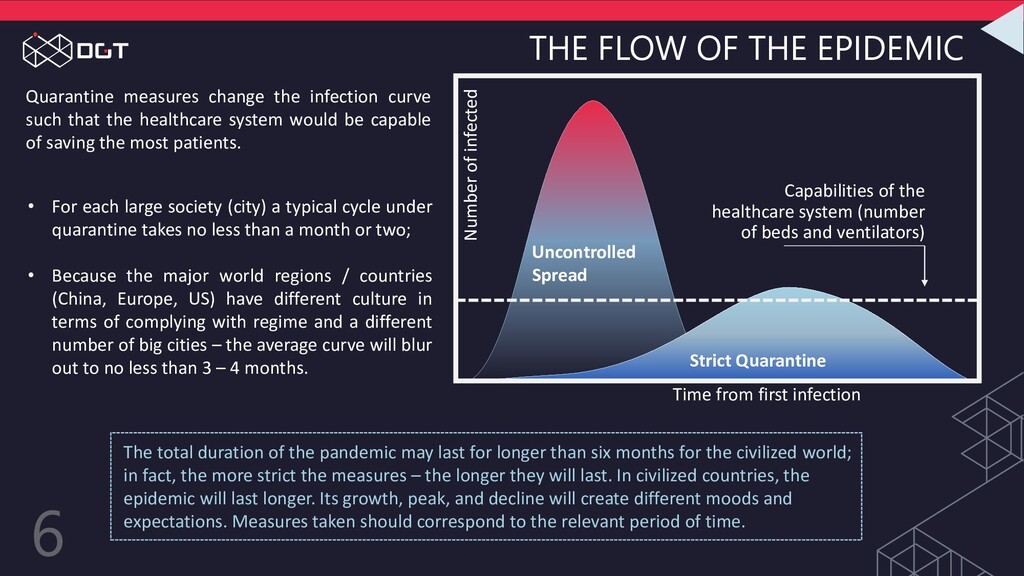

(number of beds and ventilators) Uncontrolled Spread Strict Quarantine Number of infected Time from first infection Quarantine measures change the infection curve such that the healthcare system would be capable of saving the most patients. • For each large society (city) a typical cycle under quarantine takes no less than a month or two; • Because the major world regions / countries (China, Europe, US) have different culture in terms of complying with regime and a different number of big cities – the average curve will blur out to no less than 3 – 4 months. The total duration of the pandemic may last for longer than six months for the civilized world; in fact, the more strict the measures – the longer they will last. In civilized countries, the epidemic will last longer. Its growth, peak, and decline will create different moods and expectations. Measures taken should correspond to the relevant period of time.

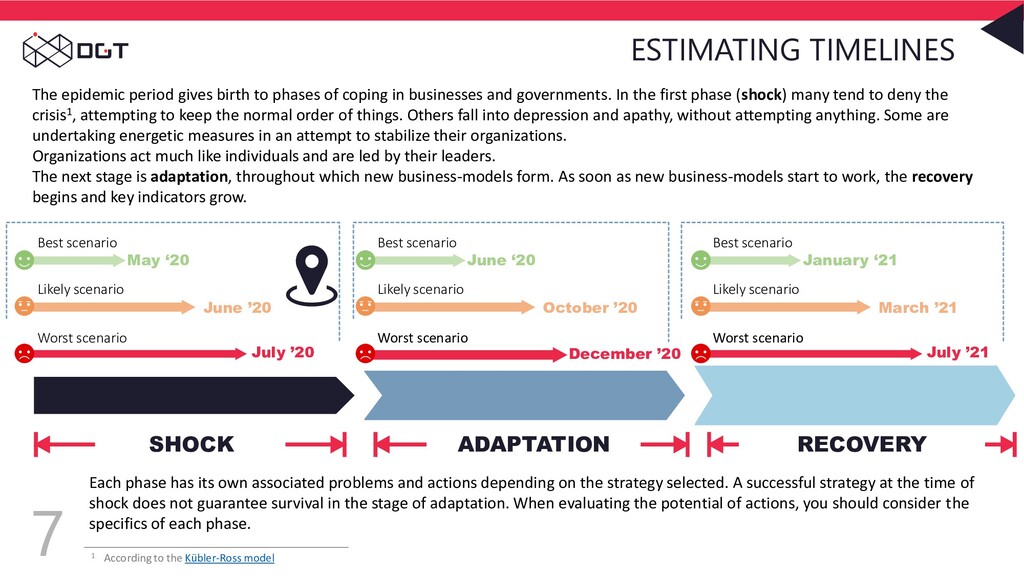

coping in businesses and governments. In the first phase (shock) many tend to deny the crisis1, attempting to keep the normal order of things. Others fall into depression and apathy, without attempting anything. Some are undertaking energetic measures in an attempt to stabilize their organizations. Organizations act much like individuals and are led by their leaders. The next stage is adaptation, throughout which new business-models form. As soon as new business-models start to work, the recovery begins and key indicators grow. SHOCK Best scenario Likely scenario Worst scenario May ‘20 June ’20 July ’20 1 According to the Kübler-Ross model Each phase has its own associated problems and actions depending on the strategy selected. A successful strategy at the time of shock does not guarantee survival in the stage of adaptation. When evaluating the potential of actions, you should consider the specifics of each phase. ADAPTATION Best scenario Likely scenario Worst scenario June ‘20 October ’20 December ’20 RECOVERY Best scenario Likely scenario Worst scenario January ‘21 March ’21 July ’21

are feeling psychological pressures. Work is generally not effective even for those who do try to work: people are expecting cuts, children are running around, and not everyone has a dedicated work space. The main consequence is the load bearing down on internet providers, cloud systems, chats, and videoconferencing systems. School children and students are transferring to distance education. Most businesses are on pause. Restaurants, movie theatres, malls are closed. In many places non-working days have been prolonged until the end of April – the small and medium business is teetering on the brink of bankruptcy. Existing online services – news, movies, etc. are in high demand. Distance learning is in high demand. Food delivery services are experiencing a spike. Significant load on videoconference platforms. - 1 - WORK FROM HOME

home that necessitates masks, aiding relatives… everything leads to an increase in demand for delivery services and reduction of expenditures on non- essentials (consumer economy). Most businesses are on pause. Restaurants, movie theatres, malls are closed. In many places non-working days have been prolonged until the end of April – the small and medium business is teetering on the brink of bankruptcy. Existing online services – news, movies, etc. are in high demand. Distance learning is in high demand. Food delivery services are experiencing a spike. Significant load on videoconference platforms. - 2 – SUPPORT CHANNELS

movies over the internet, read more books, while some began to learn more and use distance education Most businesses are on pause. Restaurants, movie theatres, malls are closed. In many places non-working days have been prolonged until the end of April – the small and medium business is teetering on the brink of bankruptcy. Existing online services – news, movies, etc. are in high demand. Distance learning is in high demand. Food delivery services are experiencing a spike. Significant load on videoconference platforms. - 3 - LEISURE

restaurants, and entertainment complexes are collapsing. Owners of small and mid-sized businesses are hoping for a miracle and are preparing for closures or layoffs. Governments are implementing total control, limiting the movement of citizens, urgently building hospitals, and purchasing supplies to manage the inflow of purchasers. Organizations with more than 100 employees are optimizing their expenses and are transferring to remote work: either having employees take vacation days (to win time), installing remote access services, developing an office-visit schedule, or laying people off. Throughout the first month, companies will be making the quintessential preparations for survival. Only quick measures will be considered, only urgent solutions taken in times of high uncertainty. Regular procedures, tenders (except insider ones) will all be postponed.

emails, VPN, document management system, installing or buying licenses for videoconferencing software: Skype, MS Team, Zoom… 2) Preparing layoffs and optimizing financial flows: review of contracts, optimizing rent, etc. The immediate reaction to the crisis will be to ensure the minimal set of services and actions that will allow the organization to survive. 3) Working out partnerships with lawyers – supporting current contracts, ensuring continuity in business and activity. MAIN OUTCOMES: A. For IT organizations, long-term contracts or potential investments will be “frozen”. It is possible that work will be conducted on existing contracts, however, supporting them requires offering buyers new methods of cooperation; B. In times of crisis, ready remote office solutions will be in the highest demand: videoconferences, incident management systems, cloud solutions (to support end users).

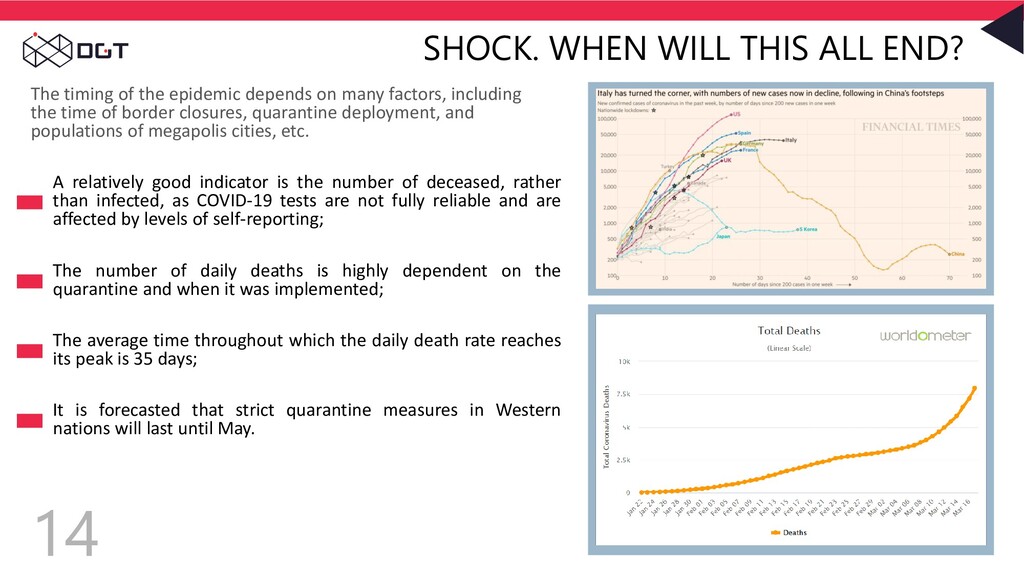

epidemic depends on many factors, including the time of border closures, quarantine deployment, and populations of megapolis cities, etc. A relatively good indicator is the number of deceased, rather than infected, as COVID-19 tests are not fully reliable and are affected by levels of self-reporting; The number of daily deaths is highly dependent on the quarantine and when it was implemented; The average time throughout which the daily death rate reaches its peak is 35 days; It is forecasted that strict quarantine measures in Western nations will last until May.

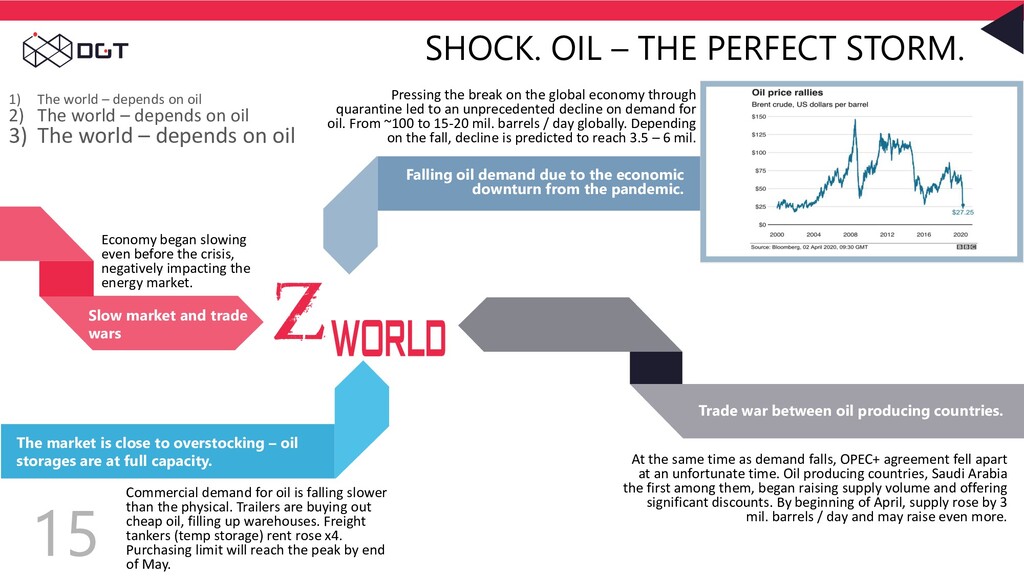

to the economic downturn from the pandemic. Trade war between oil producing countries. The market is close to overstocking – oil storages are at full capacity. Pressing the break on the global economy through quarantine led to an unprecedented decline on demand for oil. From ~100 to 15-20 mil. barrels / day globally. Depending on the fall, decline is predicted to reach 3.5 – 6 mil. At the same time as demand falls, OPEC+ agreement fell apart at an unfortunate time. Oil producing countries, Saudi Arabia the first among them, began raising supply volume and offering significant discounts. By beginning of April, supply rose by 3 mil. barrels / day and may raise even more. Commercial demand for oil is falling slower than the physical. Trailers are buying out cheap oil, filling up warehouses. Freight tankers (temp storage) rent rose x4. Purchasing limit will reach the peak by end of May. Economy began slowing even before the crisis, negatively impacting the energy market. Slow market and trade wars 1) The world – depends on oil 2) The world – depends on oil 3) The world – depends on oil

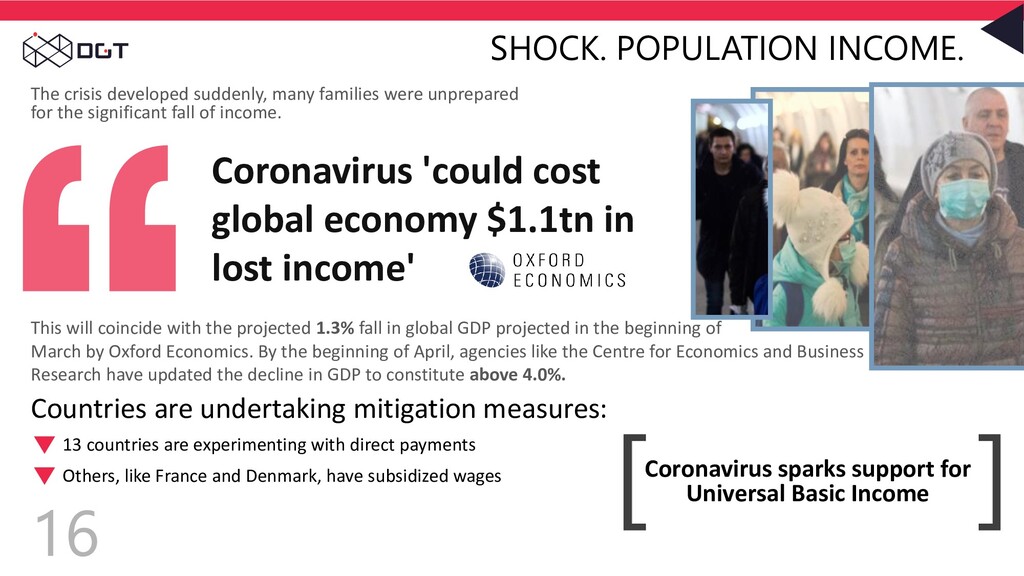

unprepared for the significant fall of income. Coronavirus 'could cost global economy $1.1tn in lost income' This will coincide with the projected 1.3% fall in global GDP projected in the beginning of March by Oxford Economics. By the beginning of April, agencies like the Centre for Economics and Business Research have updated the decline in GDP to constitute above 4.0%. Countries are undertaking mitigation measures: 13 countries are experimenting with direct payments Others, like France and Denmark, have subsidized wages Coronavirus sparks support for Universal Basic Income

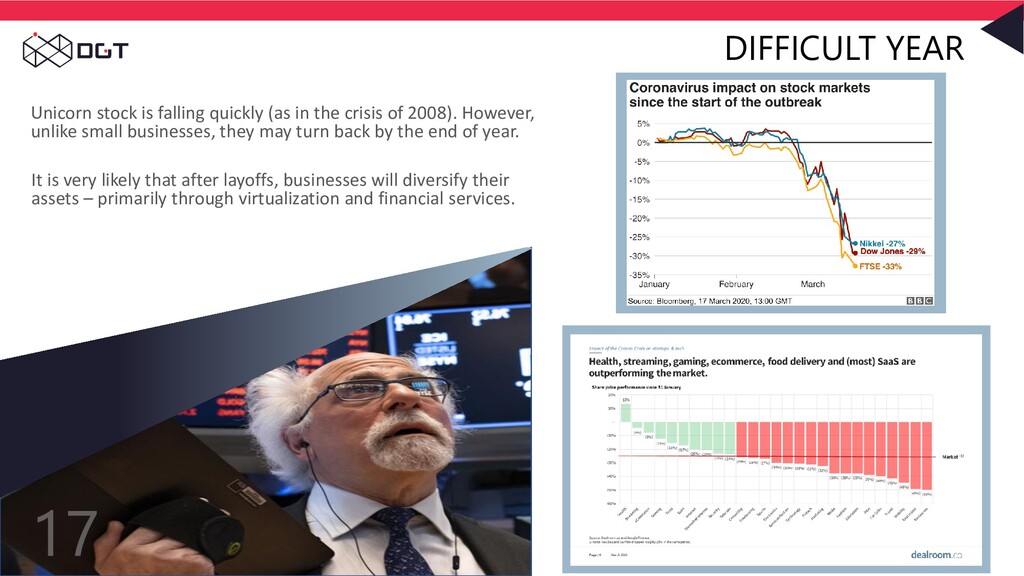

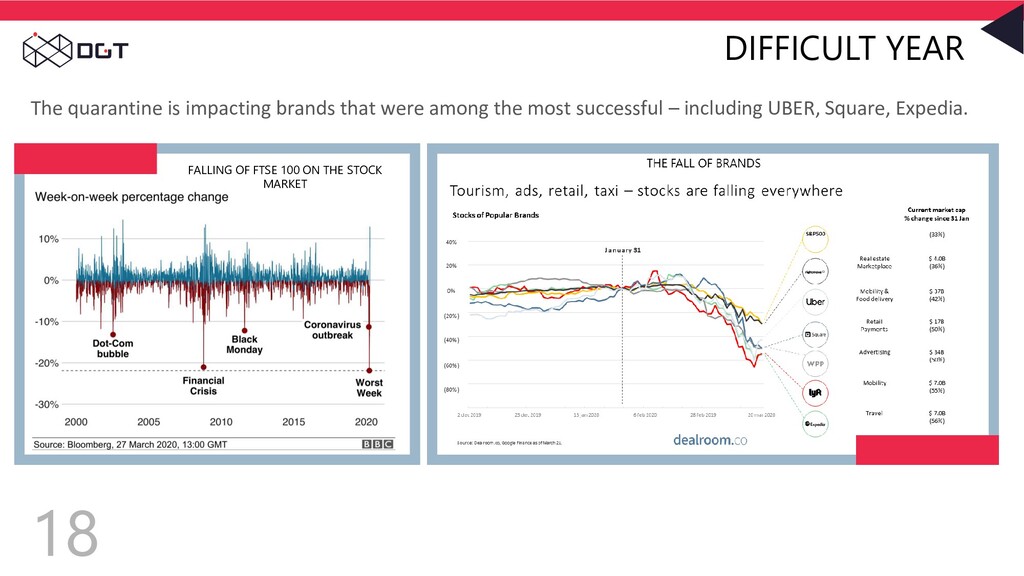

crisis of 2008). However, unlike small businesses, they may turn back by the end of year. It is very likely that after layoffs, businesses will diversify their assets – primarily through virtualization and financial services.

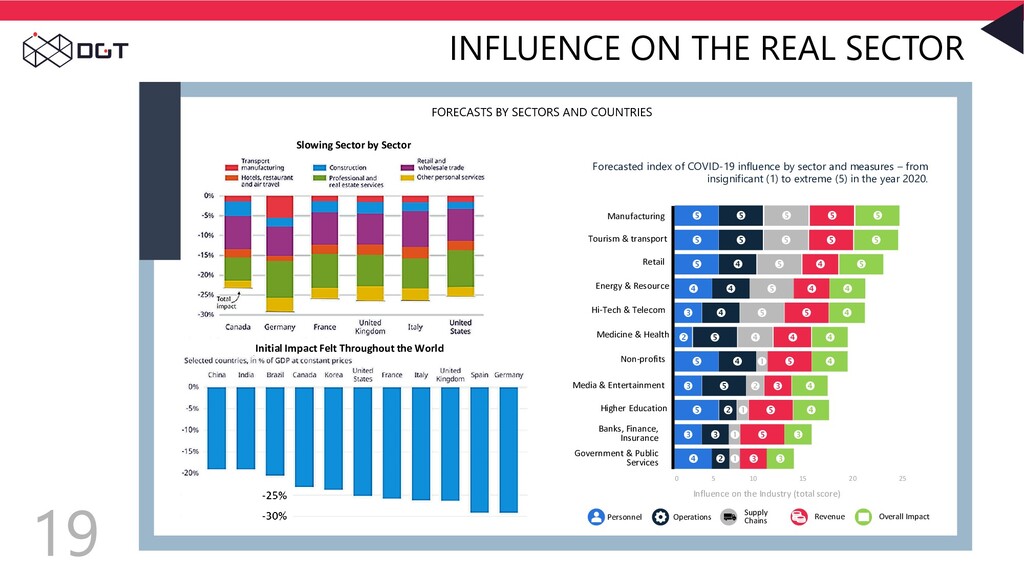

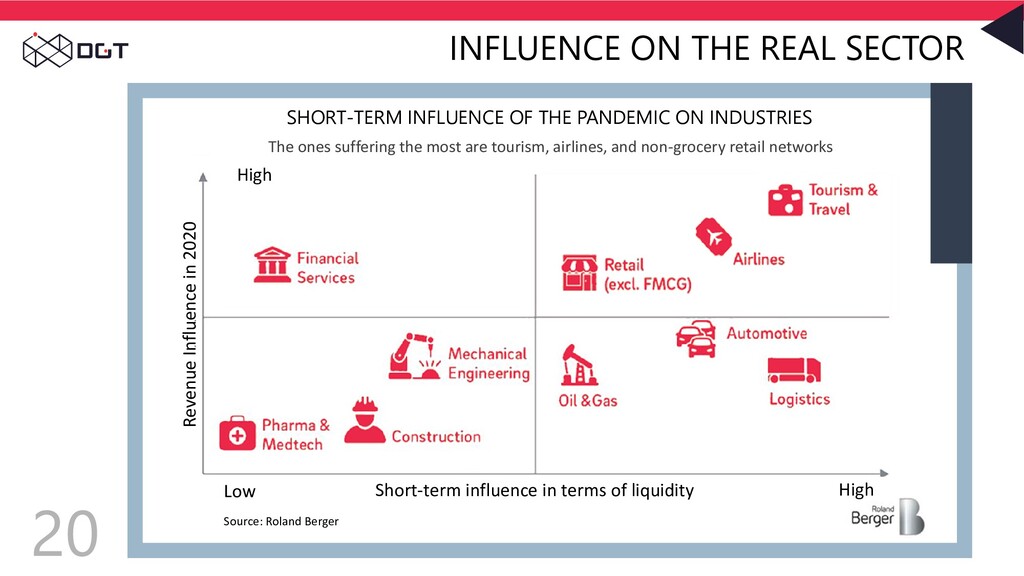

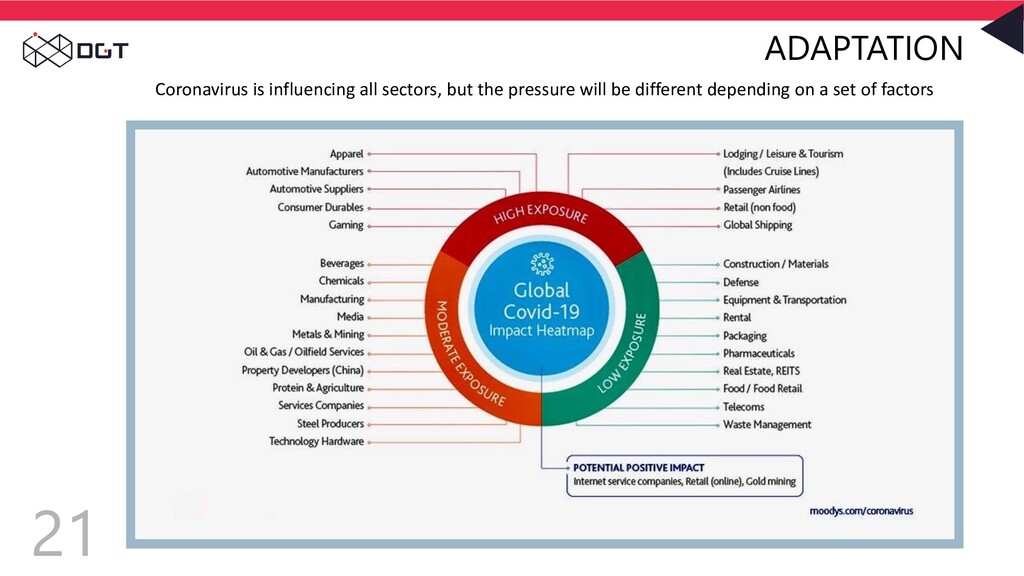

ON INDUSTRIES The ones suffering the most are tourism, airlines, and non-grocery retail networks Short-term influence in terms of liquidity Source: Roland Berger Revenue Influence in 2020 High Low High

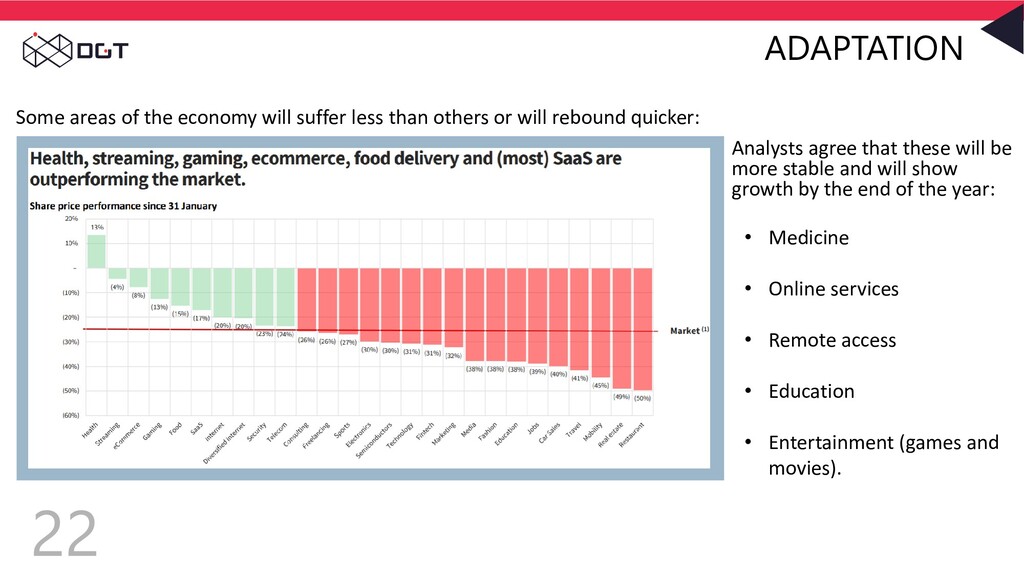

others or will rebound quicker: • Medicine • Online services • Remote access • Education • Entertainment (games and movies). Analysts agree that these will be more stable and will show growth by the end of the year:

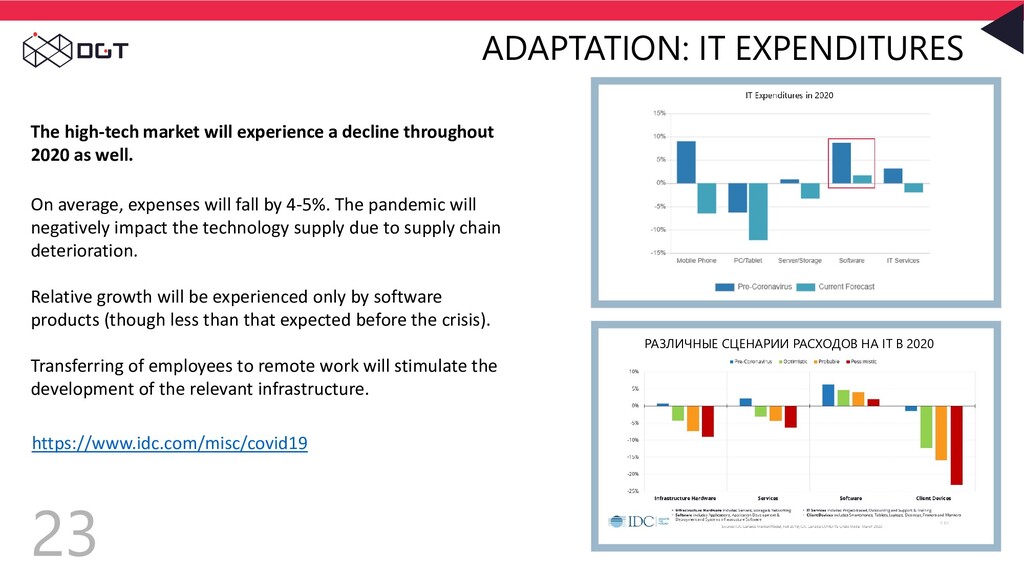

decline throughout 2020 as well. On average, expenses will fall by 4-5%. The pandemic will negatively impact the technology supply due to supply chain deterioration. Relative growth will be experienced only by software products (though less than that expected before the crisis). Transferring of employees to remote work will stimulate the development of the relevant infrastructure. РАЗЛИЧНЫЕ СЦЕНАРИИ РАСХОДОВ НА IT В 2020

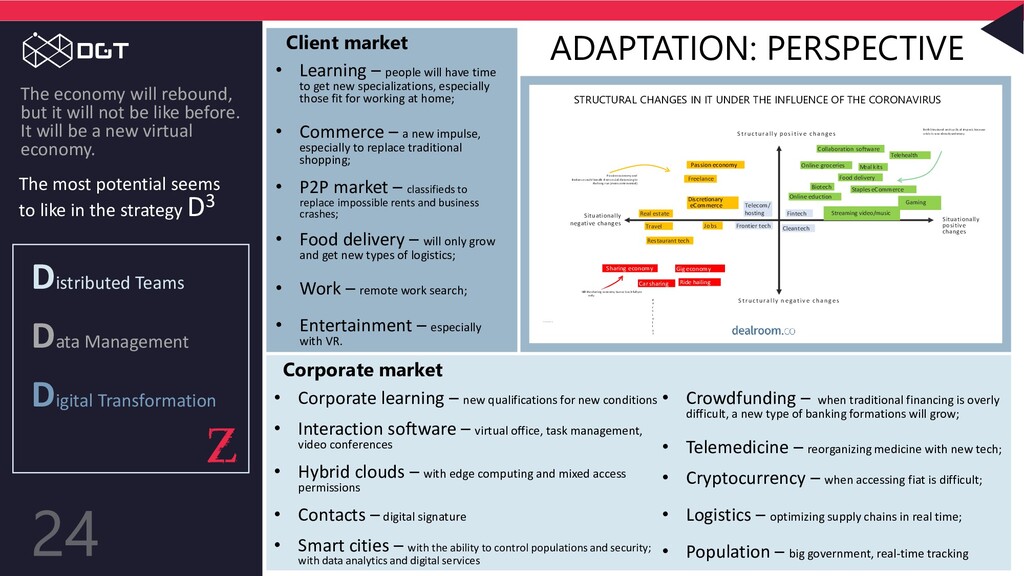

be like before. It will be a new virtual economy. Distributed Teams Data Management Digital Transformation Client market Corporate market • Learning – people will have time to get new specializations, especially those fit for working at home; • Commerce – a new impulse, especially to replace traditional shopping; • P2P market – classifieds to replace impossible rents and business crashes; • Food delivery – will only grow and get new types of logistics; • Work – remote work search; • Entertainment – especially with VR. • Corporate learning – new qualifications for new conditions • Interaction software – virtual office, task management, video conferences • Hybrid clouds – with edge computing and mixed access permissions • Contacts – digital signature • Smart cities – with the ability to control populations and security; with data analytics and digital services • Crowdfunding – when traditional financing is overly difficult, a new type of banking formations will grow; • Telemedicine – reorganizing medicine with new tech; • Cryptocurrency – when accessing fiat is difficult; • Logistics – optimizing supply chains in real time; • Population – big government, real-time tracking The most potential seems to like in the strategy D3 S ourc e:Dealroom .c o Structurally positive changes Structurally negative changes Situationally negative changes Food delivery Meal kits Online groceries Cleantech Ride hailing Car sharing Travel Collaboration software Jobs Freelance Restaurant tech Discretionary eCommerce Sharing economy Biotech Passion economy Gig economy Real estate Fintech Telecom/ hosting Frontier tech Staples eCommerce Both S tructural and cyclical impact,because crisis is was alreadyunderway W ill the sharing economy bunce back fullyor only p a r t i a l l y ? Online eduction Passion economy and freelance could benefit from social distancing in the long run (more controversial) Situationally positive changes Streaming video/music Gaming Telehealth STRUCTURAL CHANGES IN IT UNDER THE INFLUENCE OF THE CORONAVIRUS

model the future. The consensus is that it will be different: Virtual epoch: everything that could be done virtually – will be. The winners will be those who test and explore the associated creative possibilities. The future is in digital commerce Distributed teams

most value? During the gold rush its a good time to be in the pick and shovel business - Mark Twain Forget the old analytics. New trends are emerging that will affect the “hot spots” of 2020 and beyond: Remote Office Forget Renting Expenses P2P replacing small businesses Delivery channels of key importance Data informing business decisions P2P Market Remote HR Solutions Delivery Analytics

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![THE DAWN OF A NEW DAY [email protected]](https://files.speakerdeck.com/presentations/7b27aa7d1dab461caf1950bca1d2d14c/slide_25.jpg){kind=link}