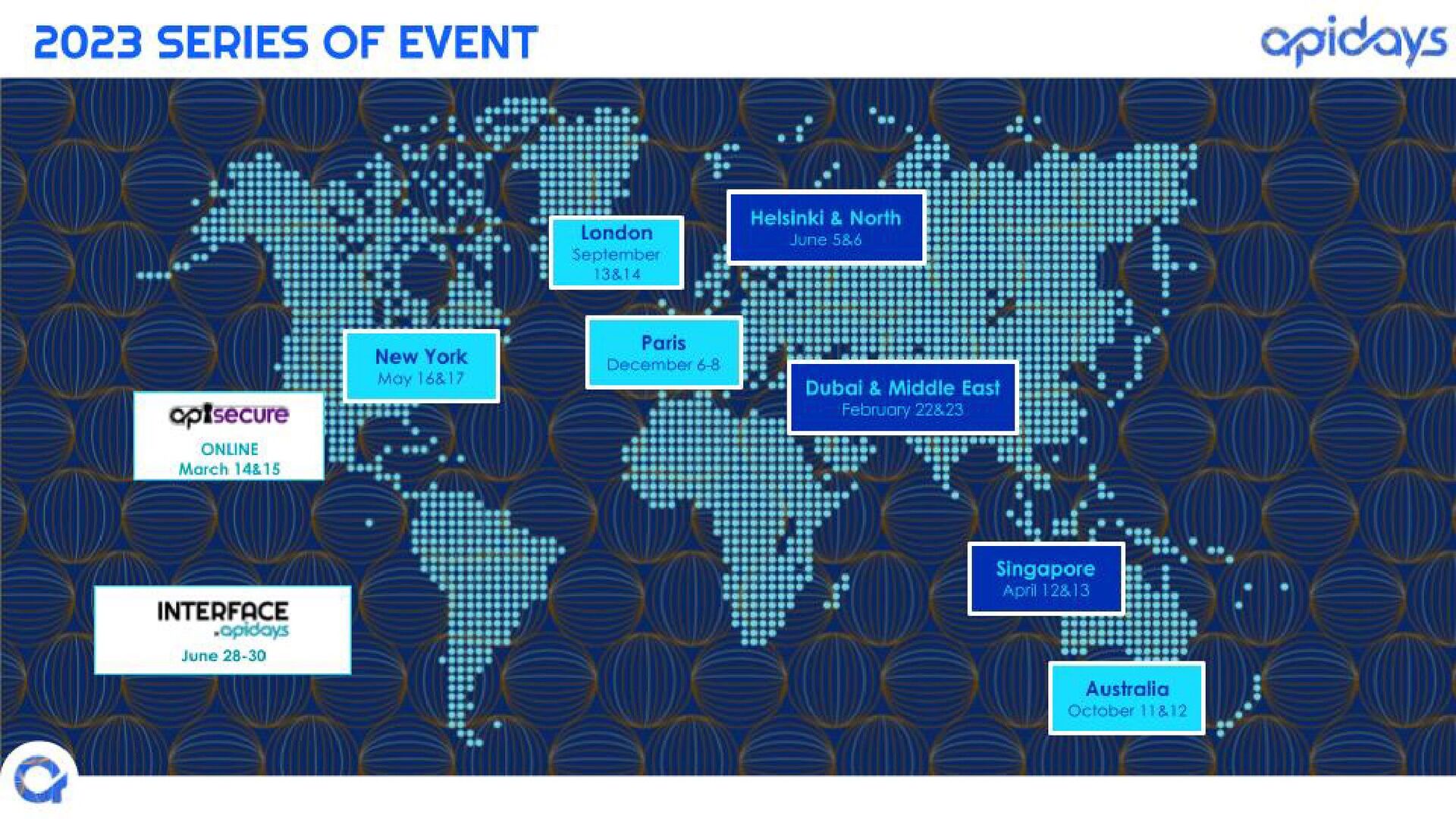

apidays New York 2023

APIs for Embedded Business Models: Finance, Healthcare, Retail, and Media

May 16 & 17, 2023

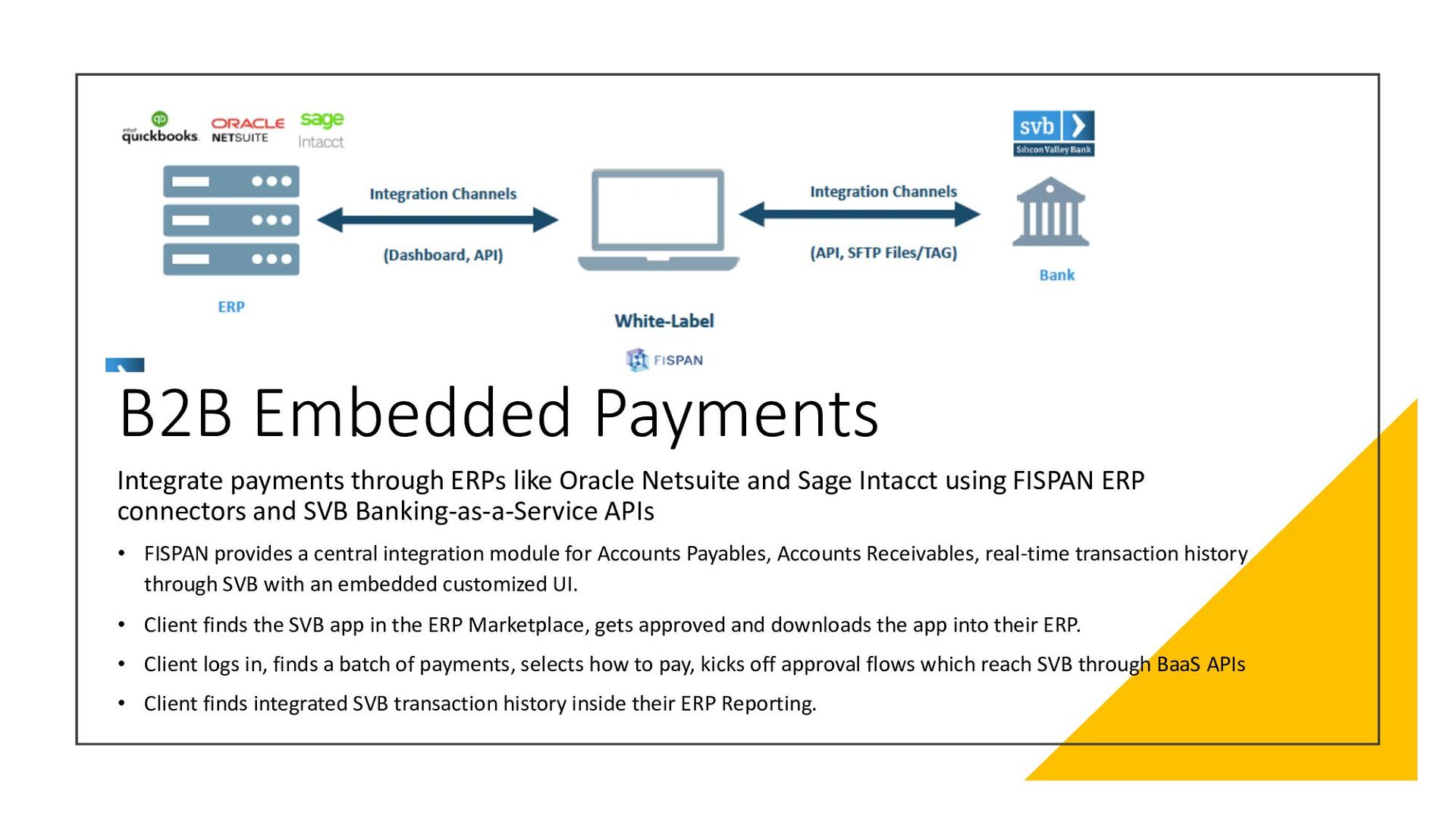

Embedded Payments in B2B and B2C use cases

Adrita Bhor, Senior Director of Product Management, Paypal

------

Check out our conferences at https://www.apidays.global/

Do you want to sponsor or talk at one of our conferences?

https://apidays.typeform.com/to/ILJeAaV8

Learn more on APIscene, the global media made by the community for the community:

https://www.apiscene.io

Explore the API ecosystem with the API Landscape:

https://apilandscape.apiscene.io/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}