ARE TRUSTS UNDER THREAT? NATASHA KAPP, Carey Olsen ANDREA McCOLL, Northern Trust SALEEM SHEIKH, GSC Solicitors ALISON VINE, Deloitte Offshore ALISON OZANNE, AO Hall (Moderator)

a highly fragmented sector § Approximately 150 trust and fund lead licences in Guernsey § Similar story in Jersey, Isle of Man, Luxembourg etc. § Much more fragmented than any other comparable financial services sub-sector (eg. life assurance, fund management, accountancy) § Commercial pressures push towards consolidation: § Economies of scale – shared compliance and other back office costs § Increased geographic footprint attractive to clients § Increased product range attractive to clients 7

consolidation § The onset of regulation from 1999 onwards had two effects § It introduced the compliance burden making it harder for the smaller players to operate profitably;; and § More importantly allowed third-party investors (predominantly private equity) to have full visibility on the underlying client base § Prior to the early 2000s, private equity investors were deterred from the sector because of lack of clarity on UBOs § 100% retrospective KYC removed the last barrier for PE to invest in the sector § The current wave of consolidation was triggered by the onset of regulation and has been gathering pace over the last 10 years 8

clients – strong client retention characteristics § High margins § Generally low capex § Strong cashflows § Potential to ‘buy and build’ in a consolidating sector 11

have a 10-year life time § Within a 10-year fund, the typical hold of an investment is 3 to 5 years – recently hold times have been longer § Target returns of 25% to 30% IRR § Alternatively to double an equity investment in 3 years or triple in 5 12

industry growth is good at 5% to 10% revenue growth pa § To achieve target fund returns of 25% to 30% IRR equity growth, value must be faster § Achieved by § Gearing the investment § Growing the profits § Increasing the multiple 13

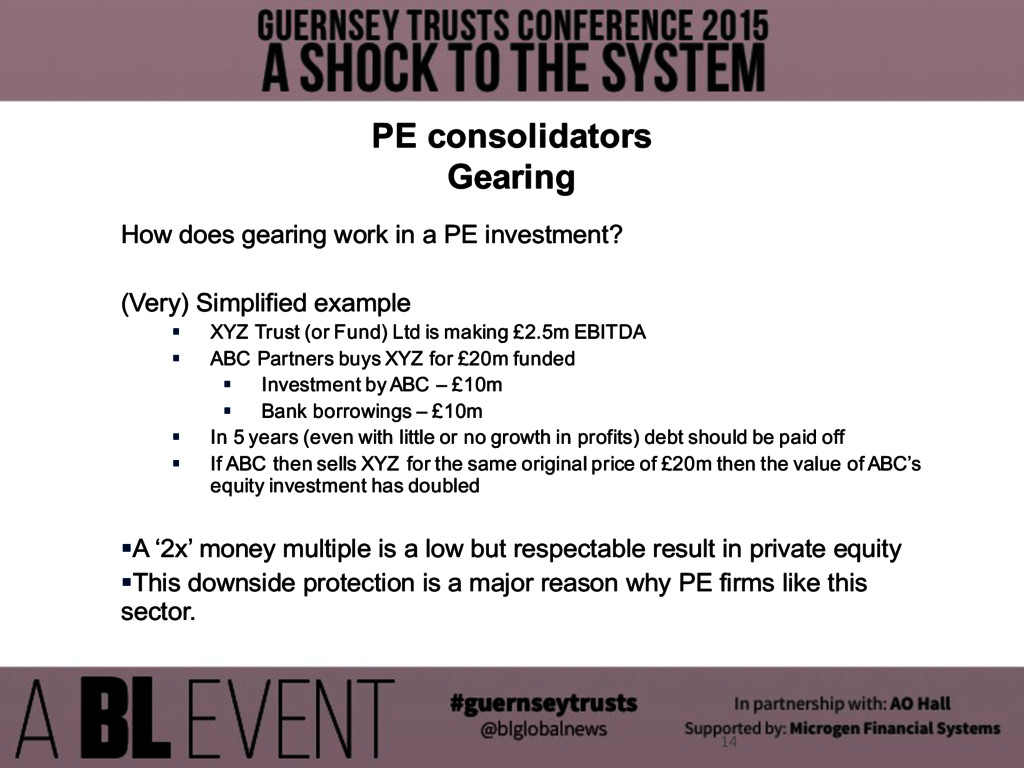

PE investment? (Very) Simplified example § XYZ Trust (or Fund) Ltd is making £2.5m EBITDA § ABC Partners buys XYZ for £20m funded § Investment by ABC – £10m § Bank borrowings – £10m § In 5 years (even with little or no growth in profits) debt should be paid off § If ABC then sells XYZ for the same original price of £20m then the value of ABC’s equity investment has doubled §A ‘2x’ money multiple is a low but respectable result in private equity §This downside protection is a major reason why PE firms like this sector.

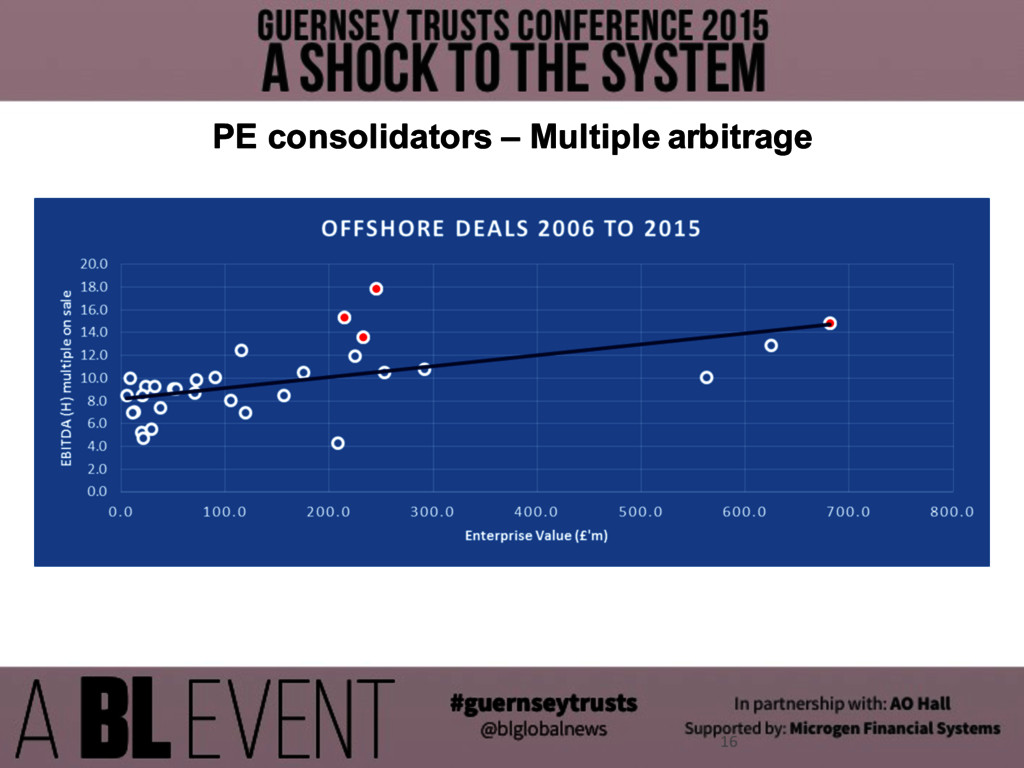

§ Local (‘in island’) acquisitions provide economies of scale – § strip out duplicated back office functions § increase margins § Acquisitions in new jurisdictions § Introduce new products and new markets § Enhance the attractiveness of the group itself to a buyer (increase the ‘exit multiple’) § Scale in itself is of benefit (multiple arbitrage) § Buy on a 6x and sell on a 10x 15

businesses? § Returns required by PE funds (25% IRR) are higher than the ‘natural’ returns of the sector § Pressure to enhance margins can lead to: • Accelerated price increases • Under investment in staff § Short PE fund time horizons leads to pressure to grow rapidly • Short-term investment decisions • Fast acquisition program • Limited opportunity for greenfield development § Change of ownership every few years • Disruptive for management and strategy 17

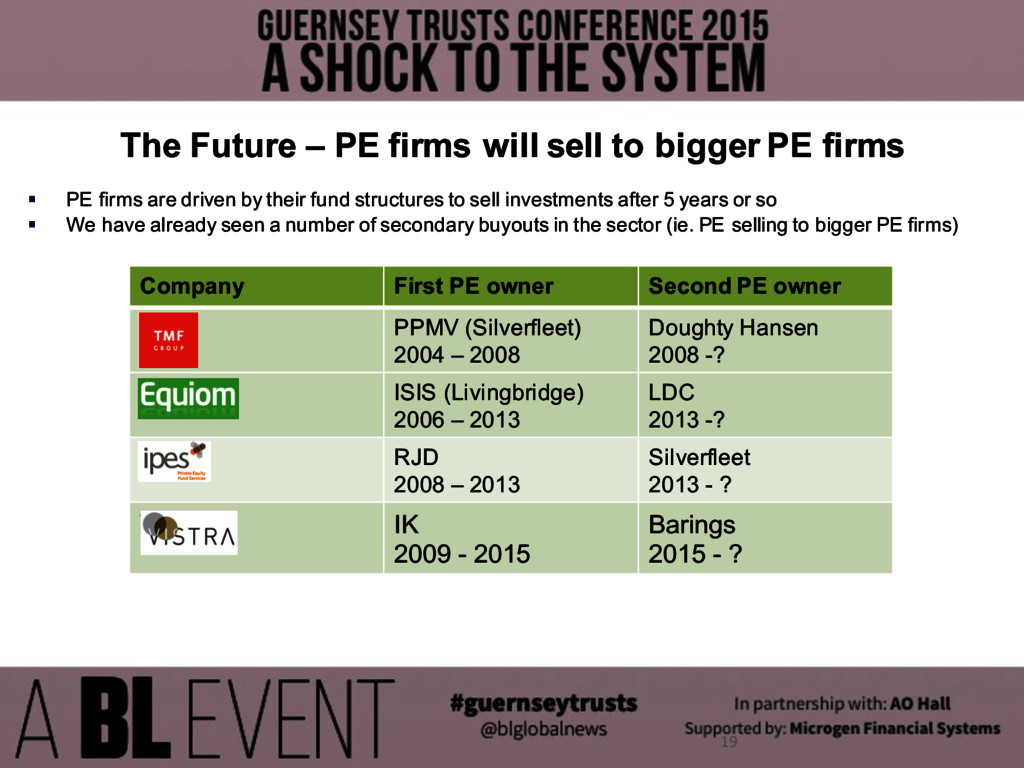

firms § PE firms are driven by their fund structures to sell investments after 5 years or so § We have already seen a number of secondary buyouts in the sector (ie. PE selling to bigger PE firms) 19 Company First PE owner Second PE owner TMF PPMV (Silverfleet) 2004 – 2008 Doughty Hansen 2008 -? Equiom ISIS (Livingbridge) 2006 – 2013 LDC 2013 -? IPES RJD 2008 – 2013 Silverfleet 2013 - ? Vistra IK 2009 - 2015 Barings 2015 - ?

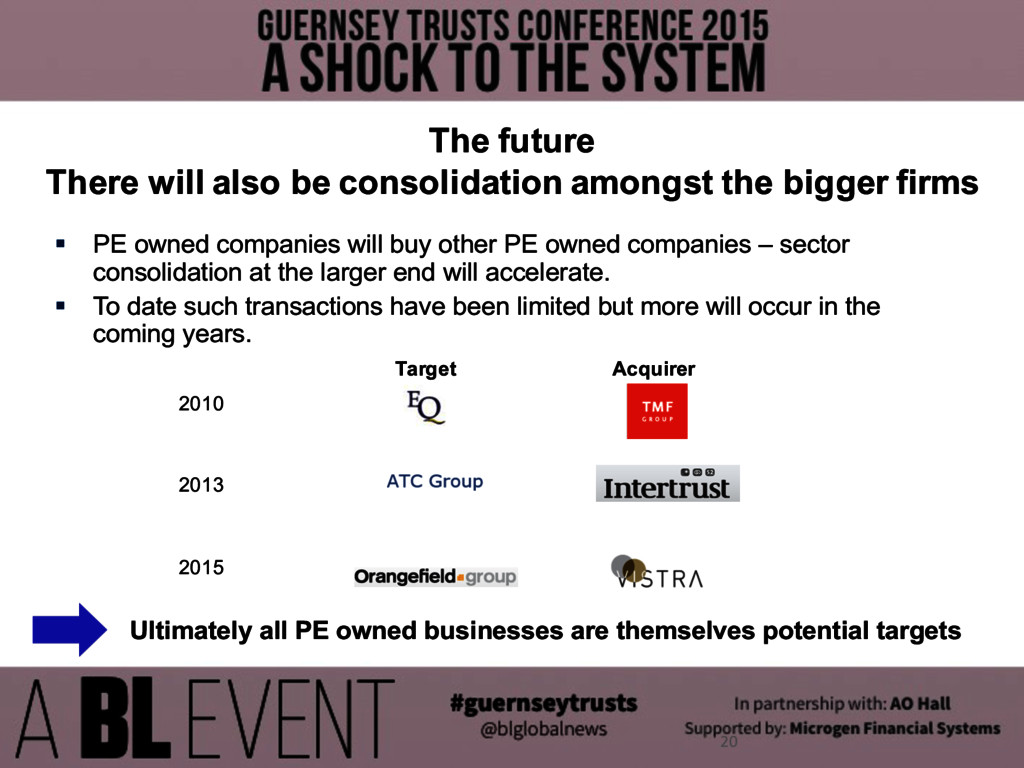

firms § PE owned companies will buy other PE owned companies – sector consolidation at the larger end will accelerate. § To date such transactions have been limited but more will occur in the coming years. 20 Target Acquirer 2010 2013 2015 Ultimately all PE owned businesses are themselves potential targets

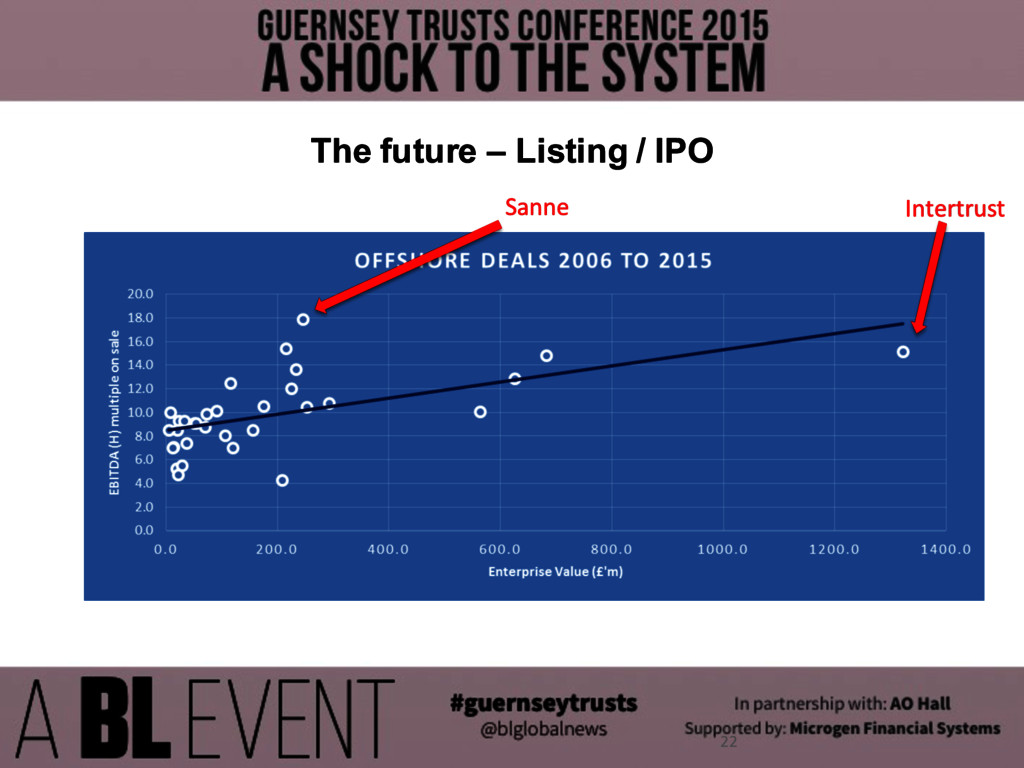

very good listed companies. § Strong cashflows – dividend yield § Good margins § Steady revenue growth § Now that Sanne and Intertrust have listed successfully others will follow § Listed trust companies can • Take a longer term view on certain investment decisions as they aren’t constrained by the PE fund lifetime • Provide staff with liquidity through listed paper • Use listed paper as an acquisition currency § The lower risk / return characteristics of the sector are arguably better suited to public markets than to PE ownership. § The listed market appears to value trust businesses differently than PE investors 21

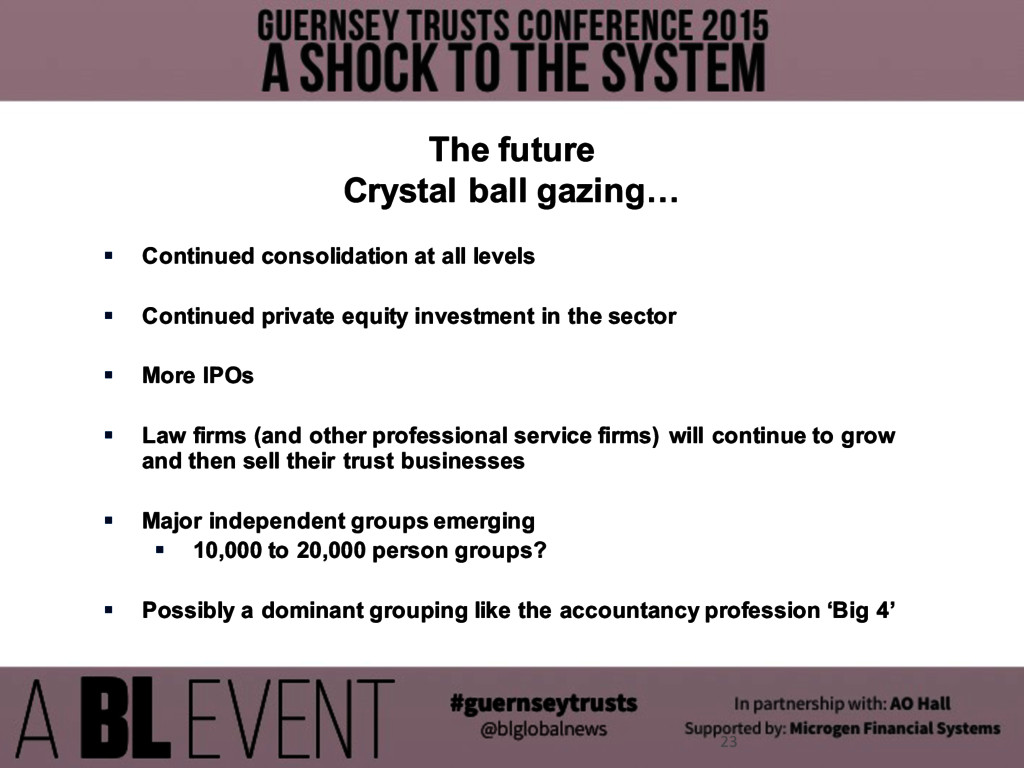

levels § Continued private equity investment in the sector § More IPOs § Law firms (and other professional service firms) will continue to grow and then sell their trust businesses § Major independent groups emerging § 10,000 to 20,000 person groups? § Possibly a dominant grouping like the accountancy profession ‘Big 4’ 23

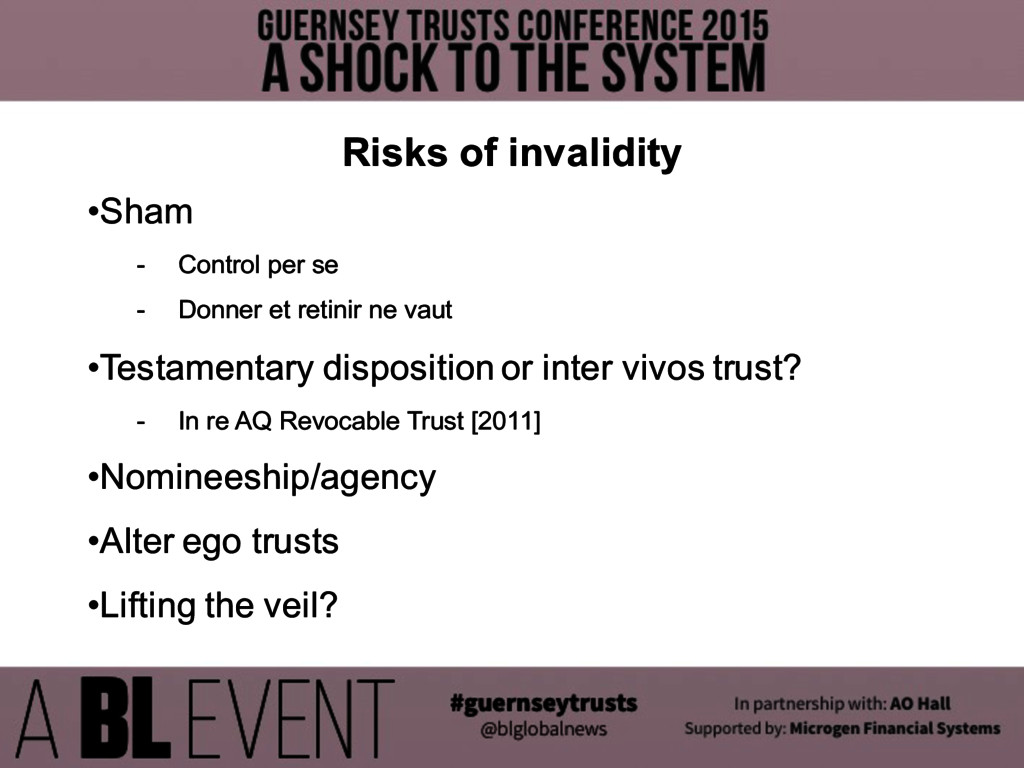

Donner et retinir ne vaut •Testamentary disposition or inter vivos trust? - In re AQ Revocable Trust [2011] •Nomineeship/agency •Alter ego trusts •Lifting the veil?

art.9A(1)(b) and ss.13/14 of the Cayman model • What powers can be reserved? • What is protected against? - Meaning of “validity” • Any or all of the powers

power/interest holder not trustee – no fiduciary duty on the power holder, subject to terms of trust – Re K Trust [2015] • SS.15 (2)(c) and (3) – effect on trustee’s liability for breach – residual liability? • Practical illustrations

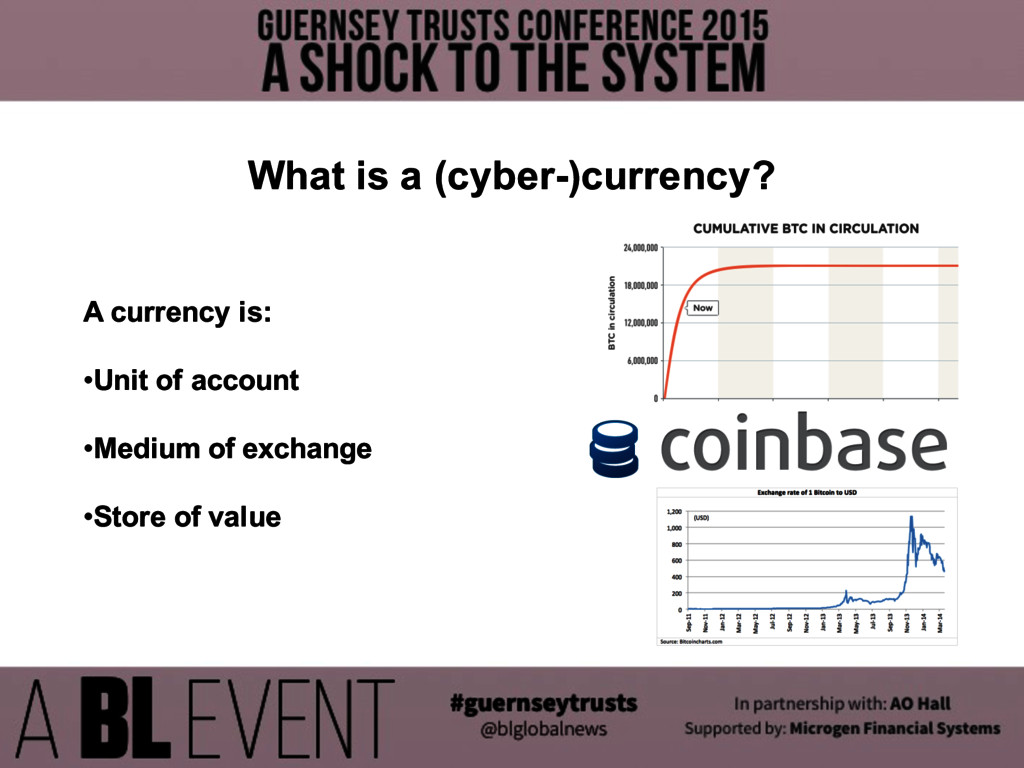

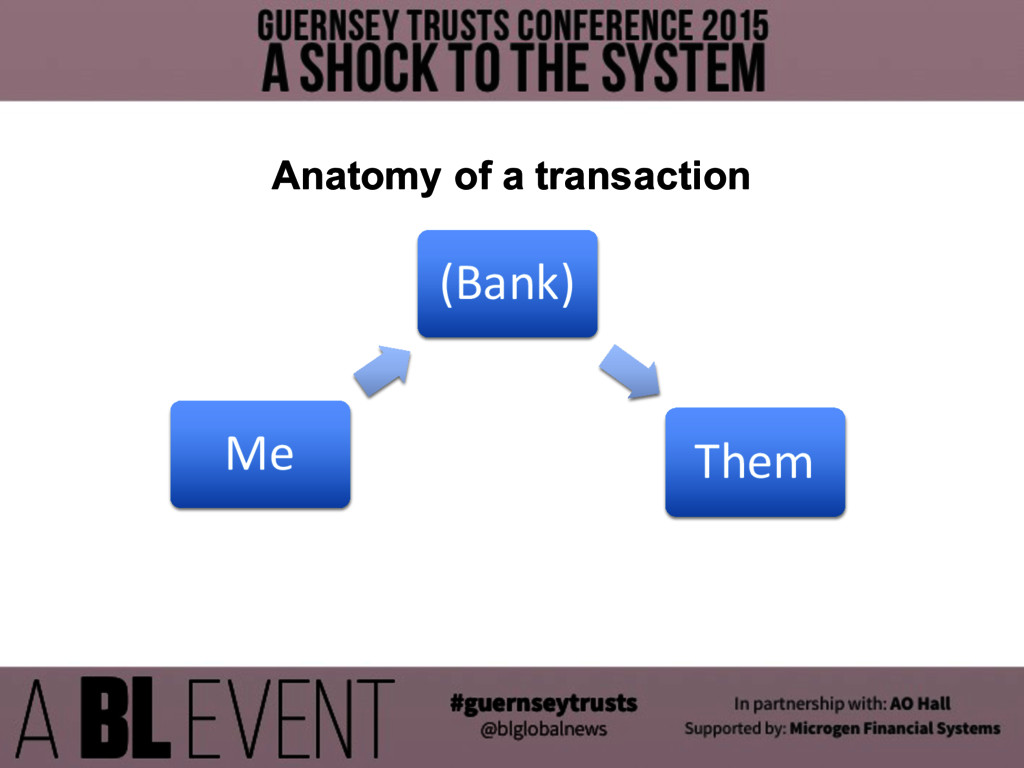

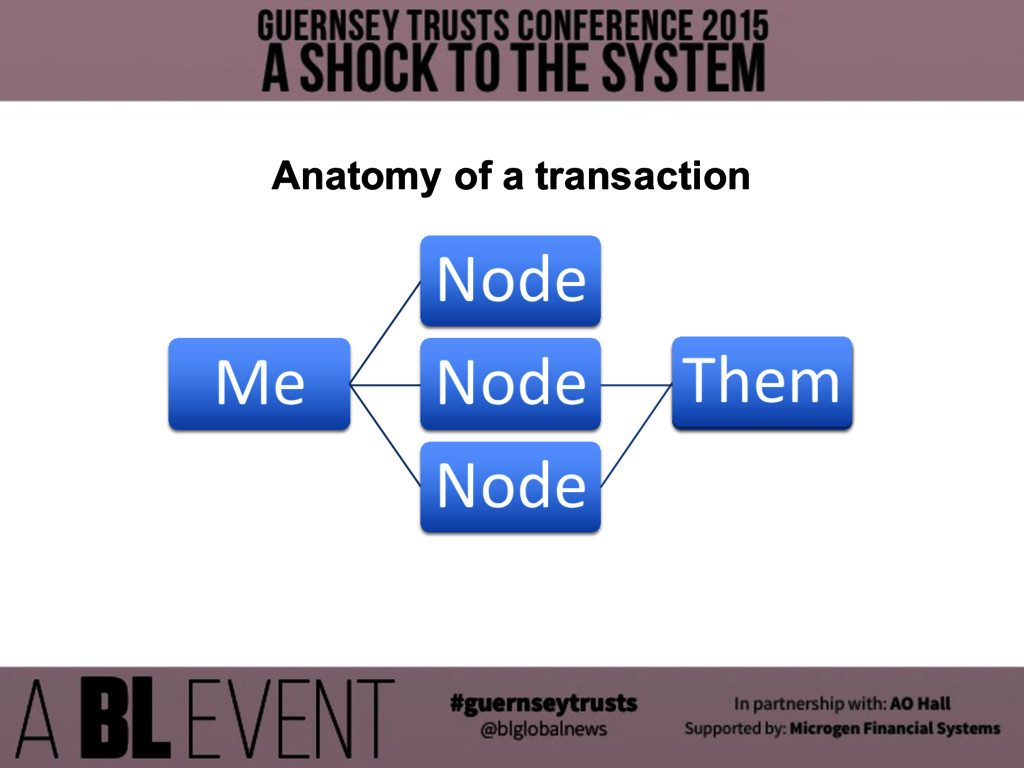

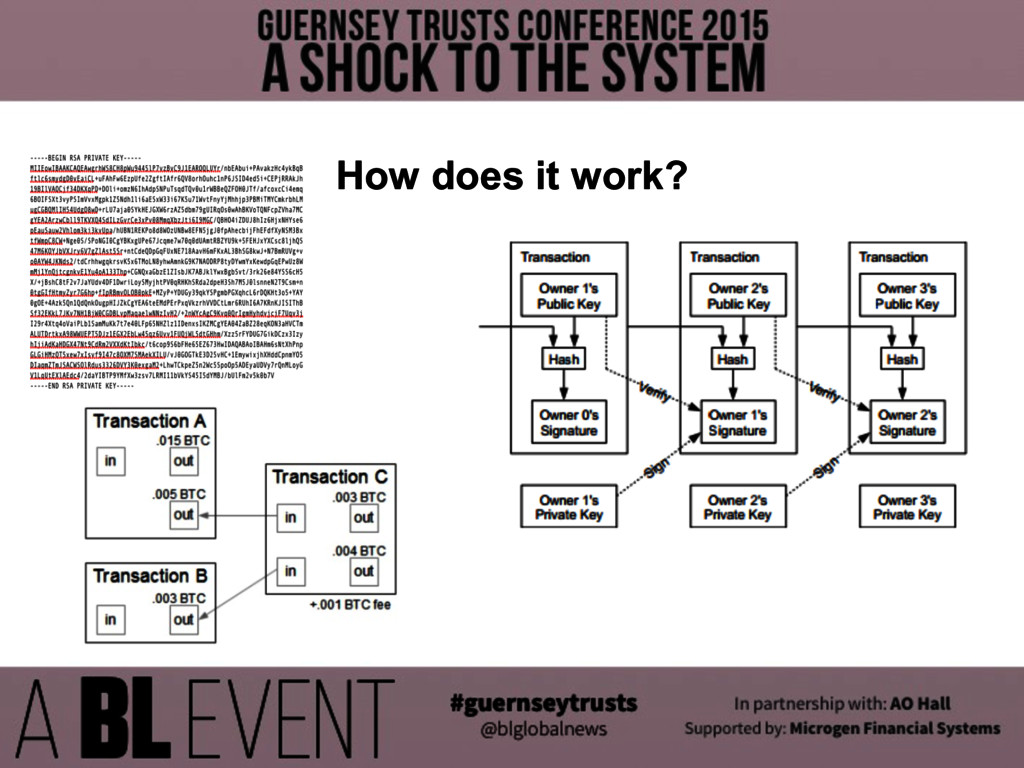

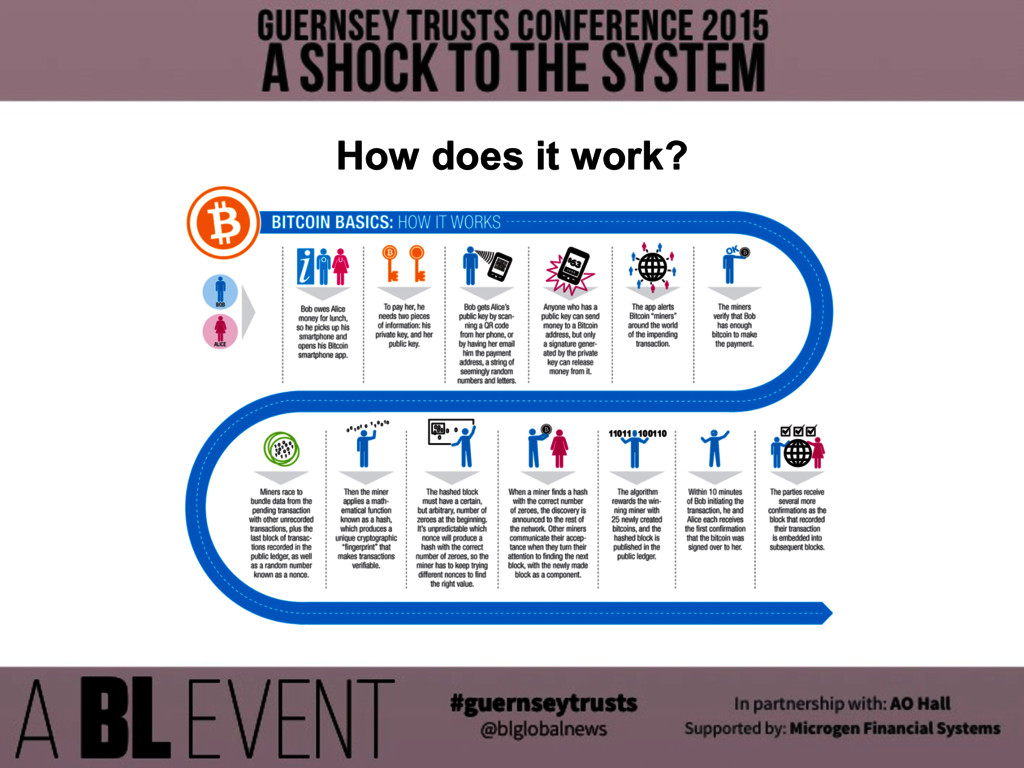

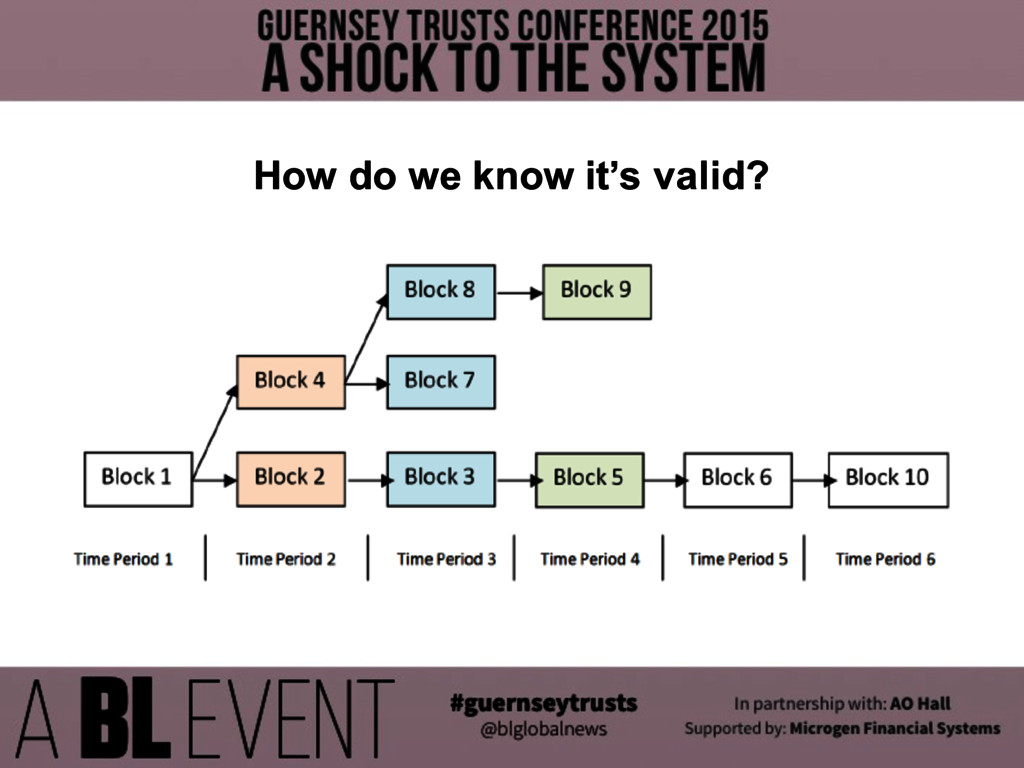

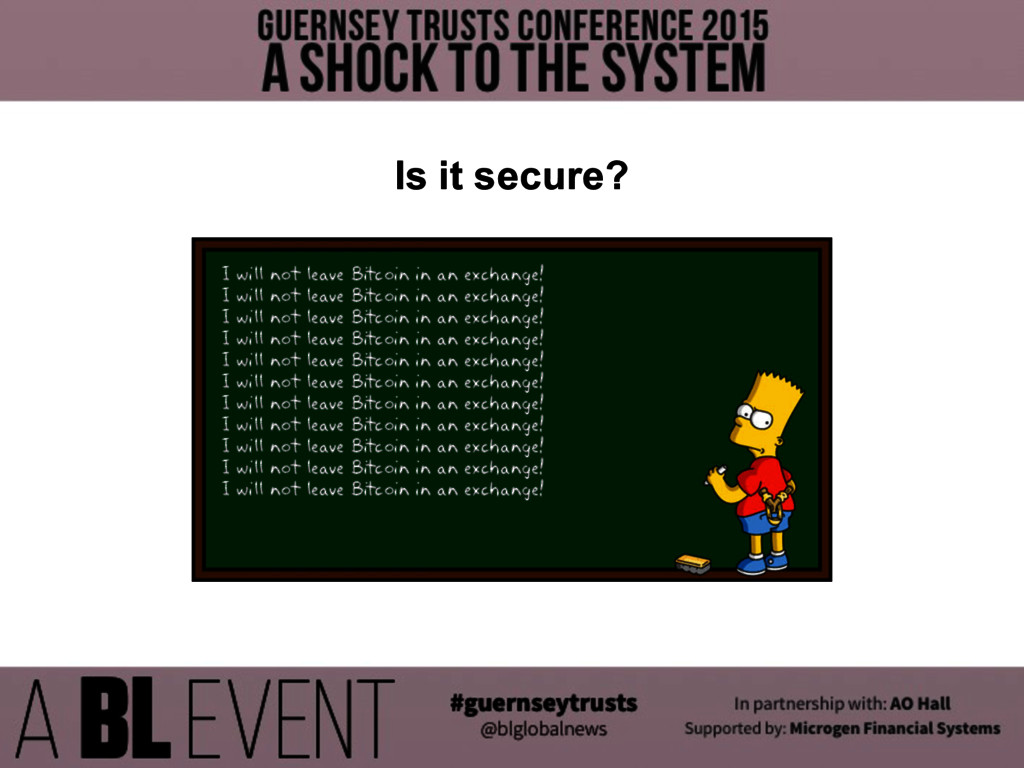

Is it secure? Bitcoin is a currency that lives in the world of computer code and can be sent anywhere in the world without racking up bank or exchange fees, and is then stored on a cellphone or hard drive until used again. Because the currency resides in code, it can also be lost when a hard drive crashes, or stolen if someone else accesses the keys to the code. http://www.newsweek.com/2014/03/14/face-behind-bitcoin-247957.html

What does the law say about them?— •Most commentary is from the regulatory and tax perspective •No direct authorities •So legal status needs to be worked out from first principles Cybercurrencies and Trusts

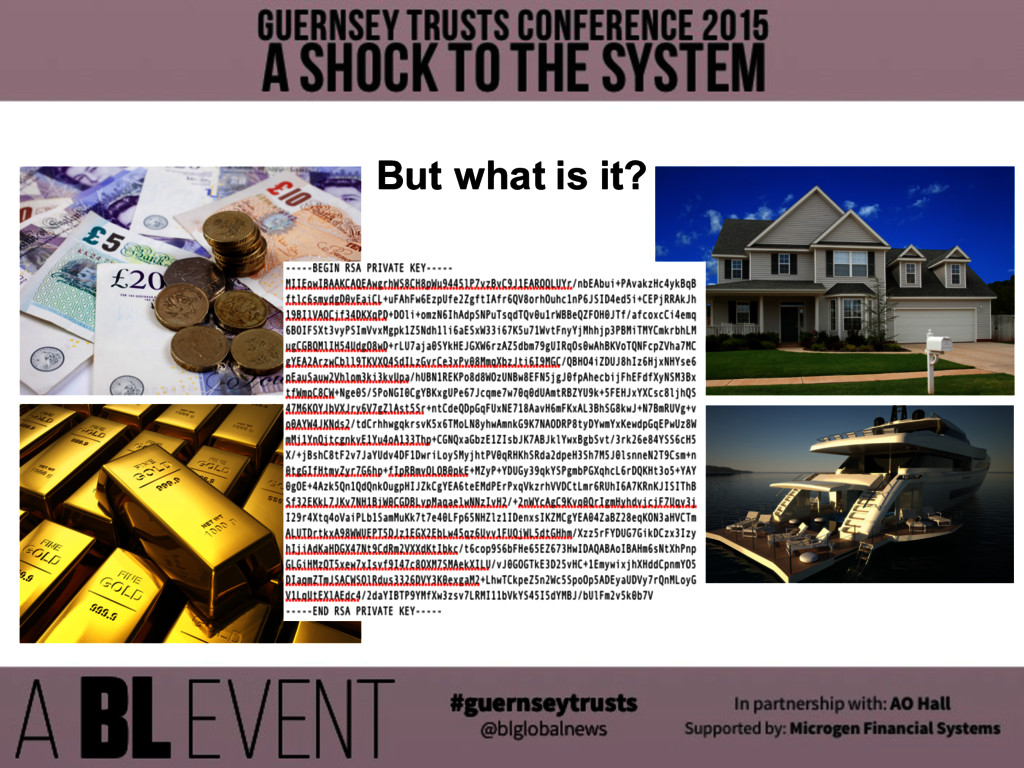

Why does it matter?— •“If you don’t understand it, you shouldn’t be in it” •If it’s not property you can’t hold it •If it’s not property you can’t “follow” or “trace” it •If it’s not money you can’t recover it as “money had and received” Cybercurrencies and Trusts

Are they money?— •No single definition of money •F.A. Mann’s definition in The Legal Aspects of Money •Comparison with state monetary systems •Comparison with local currencies Cybercurrencies and Trusts

Are they property?— •Not choses in possession (as state-issues coins are) •Not choses in action (as bank money is) •Is there a third category of private property? •Armstrong DLW GmBH v Winnington Networks Ltd (2012) •Your Response Ltd v Datastream Business Medial Ltd (2014) Cybercurrencies and Trusts

• Maintain communication and active listening • Even when bargaining with the devil coolly compare expected costs and benefits • Maintain the presumption in favour of negotiation Tips

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![• The traditional view - Re Astor’s ST [1952] •](https://files.speakerdeck.com/presentations/ff6dac9f437a409f8f3d6eb787964ad4/slide_24.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}