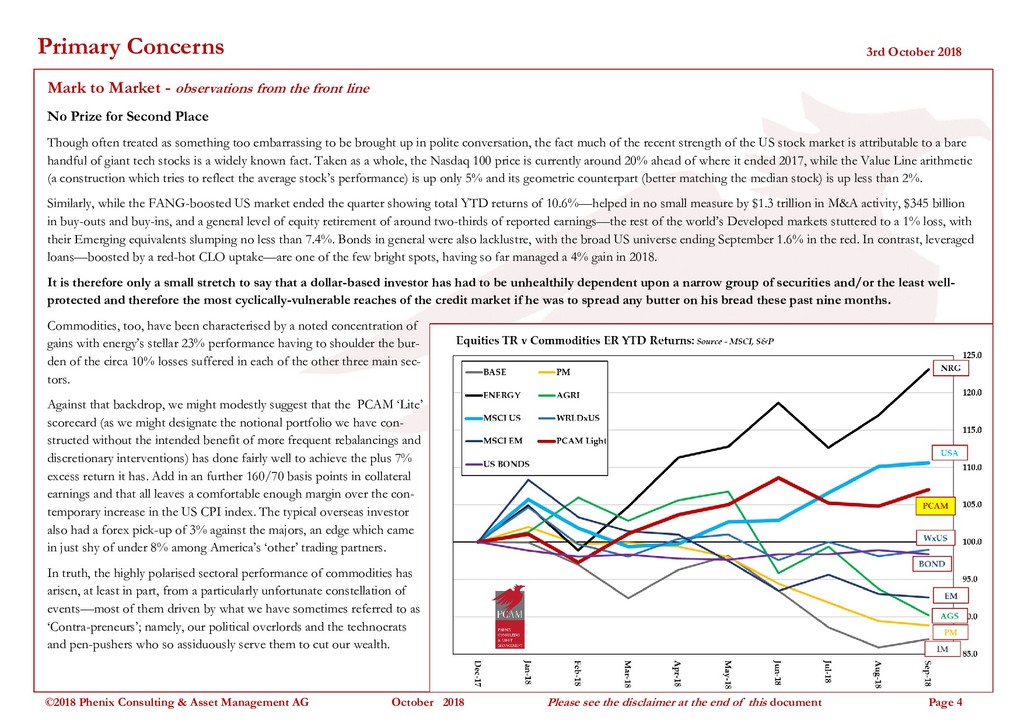

Take away US stocks and world equities have been going nowhere. Take away the FANG stocks - not to mention all that M&A, LBOs & buybacks - and US stocks have gone nowhere. Bonds are something Miss Prism will surely not wish us to discuss in Cecily's earshot. So commodites - and energy in particular - it is!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}