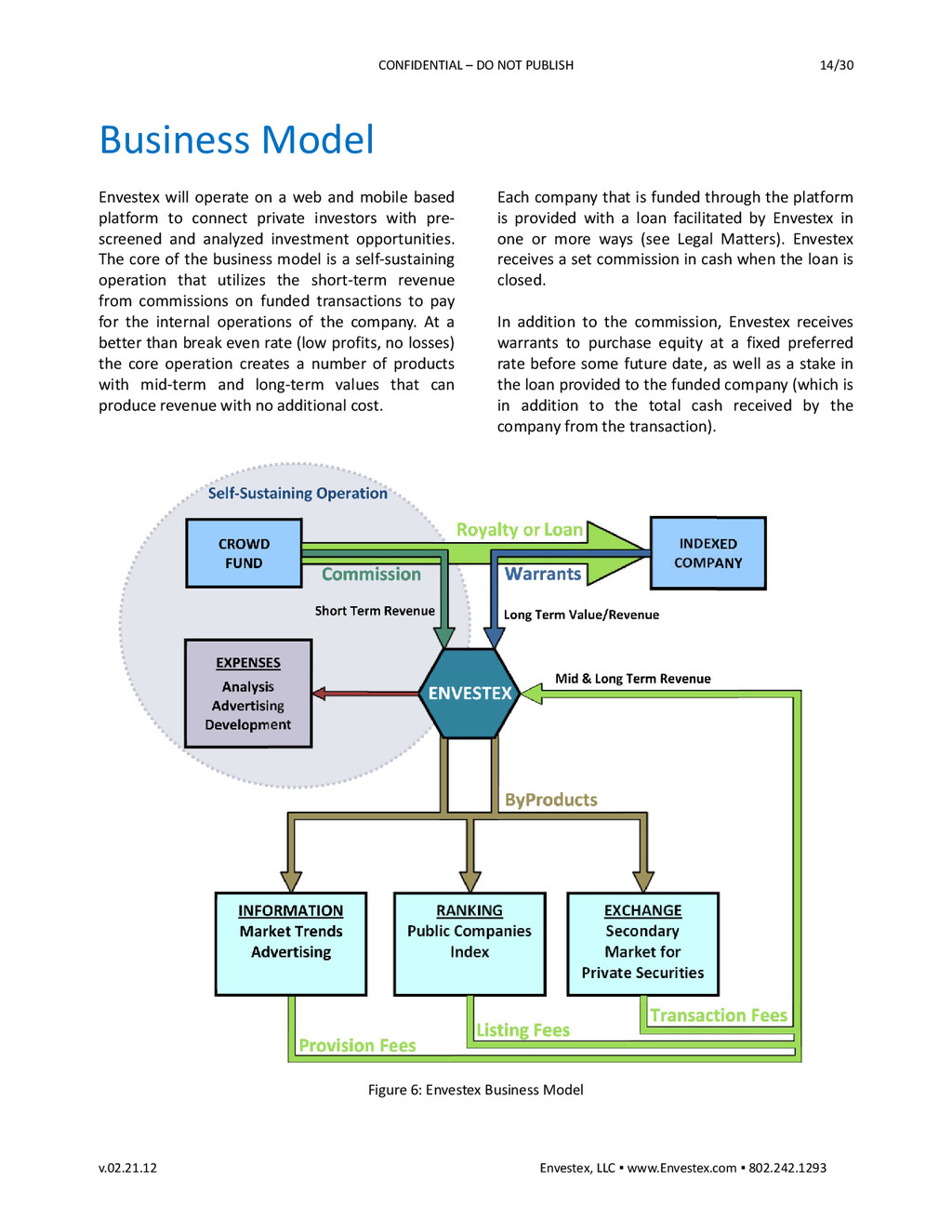

www.Envestex.com ▪ 802.242.1293 Directly from the loan funding transaction, Envestex receives a commission in the range of 5% to 10% which is scaled according to the total amount of the transaction. Larger transactions have lower commission rates. The goal is to use the commission only to pay for the operational expense associated with processing and funding the transaction. In doing so, we keep the rates lower than average brokers (although we are not “brokers”) and focus on making money on the future value of the company and transactional benefits. This puts Envestex in direct alignment with both the investors and the companies: when the companies do well, everyone benefits. We then have a vested interest in doing everything that we can to promote and help the company to be successful, including continued support through the network with regard to business connections and advertising. In addition to the real cash received as commission, Envestex takes a stake in the loan itself, equal to the commission. For example, when a company is funded for 500,000, Envestex receives a 7.5% commission in cash, and an additional 7.5% is added to the loan principal owed amount. So, when the loan reaches maturity, it will have 537,500 in principal plus whatever interest has been accrued to that date. Again, this invests Envestex in the success of the company. Royalty Based Financing While there are a number of ways to deal with potential legal issues with ESLs (see Legal Matters section), one cheap and easy method is to look at an alternative funding method. Royalty based financing (RBF) is a simple method for funding that can provide some significant advantages over usual methods and even the ESL. In RBF, the company seeking funding is still provided with a loan, but rather than waiting for the loan to mature and/or default before investors receive repayment, the company provides a percentage of its monthly revenue stream to the lenders until a pre-set maximum amount is reached (3 to 5 times financed amount). The RBF loan is not secured with equity. It is simply a right to revenue up to a specified amount. The company can retain complete control. The downside for the company is that the cost of capital is higher and definite. For the investor, it means a cap on the amount they can make. However, being able to get monthly payments fast reduces the risk of total loss and reduces the total time required to get paid back (see Competition and Competitive Advantage section). Warrants Along with the real commission and additional principal allocated, Envestex will obtain the right to purchase 5% of each funded company at a fixed rate of 1/5 of the transaction amount for up to 7 years from the time of the funding transaction. For example, for a transaction amount of 500,000, Envestex will have the right to purchase 5% of the funded company for 100,000. That right can be exercised at any time and would only be exercised based on careful assessment of the funded company. In the case that it is exercised, it may be used as a typical option would. However, a buyer for the private securities would most likely need to be determined before exercise. Byproducts During the time following the funding transaction, Envestex will keep a running tab on the companies’ progress in achieving their financial and environmental goals. The information will be available to all investors in the network. The GreenVX Index and all other investment data will be updated as regularly as possible. Investors are provided with an on-going tally of the environmental benefit (or potential benefit) that their investment is accumulating and they can post progress of their investments to twitter, facebook, linkedin, etc. to share with their friends and colleagues. Traffic through the website can easily be targeted for specific advertising, generating additional revenue. Additionally, the information gathered through investor funding can be utilized to

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}