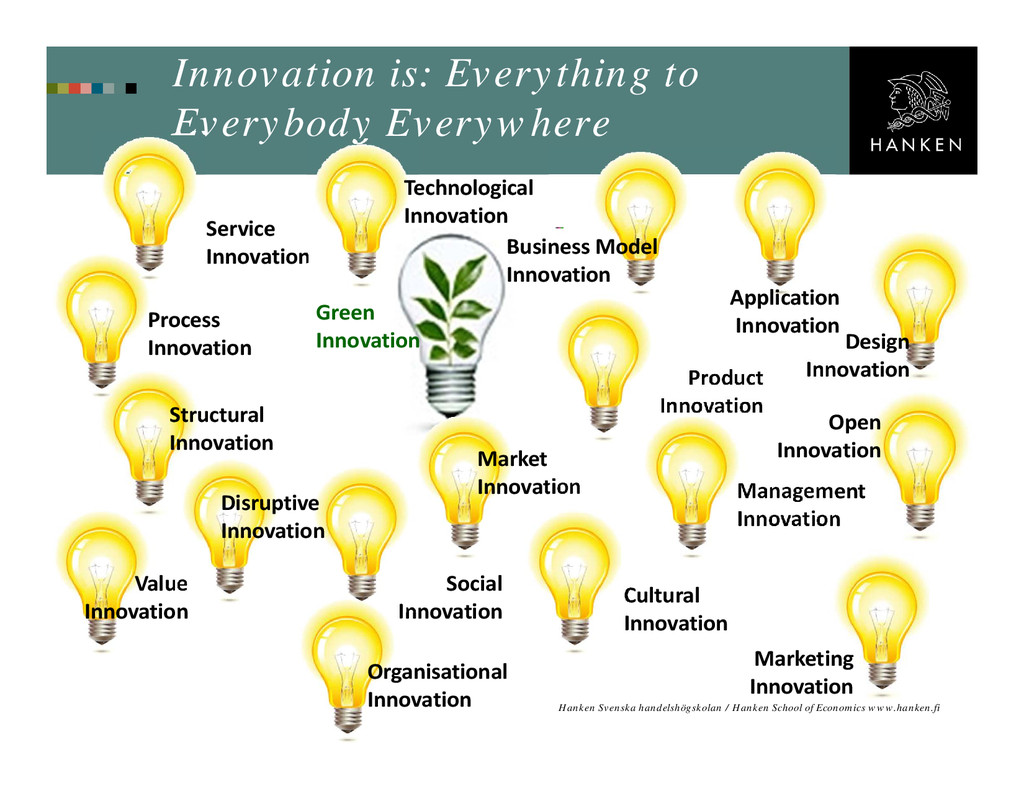

Hanken School of Economics www.hanken.fi Cultural Innovation Process Innovation Market Innovation Structural Innovation Management Innovation Product Innovation Social Innovation Value Innovation Service Innovation Design Innovation Marketing Innovation Business Model Innovation Open Innovation Green Innovation Organisational Innovation Disruptive Innovation Application Innovation Technological Innovation

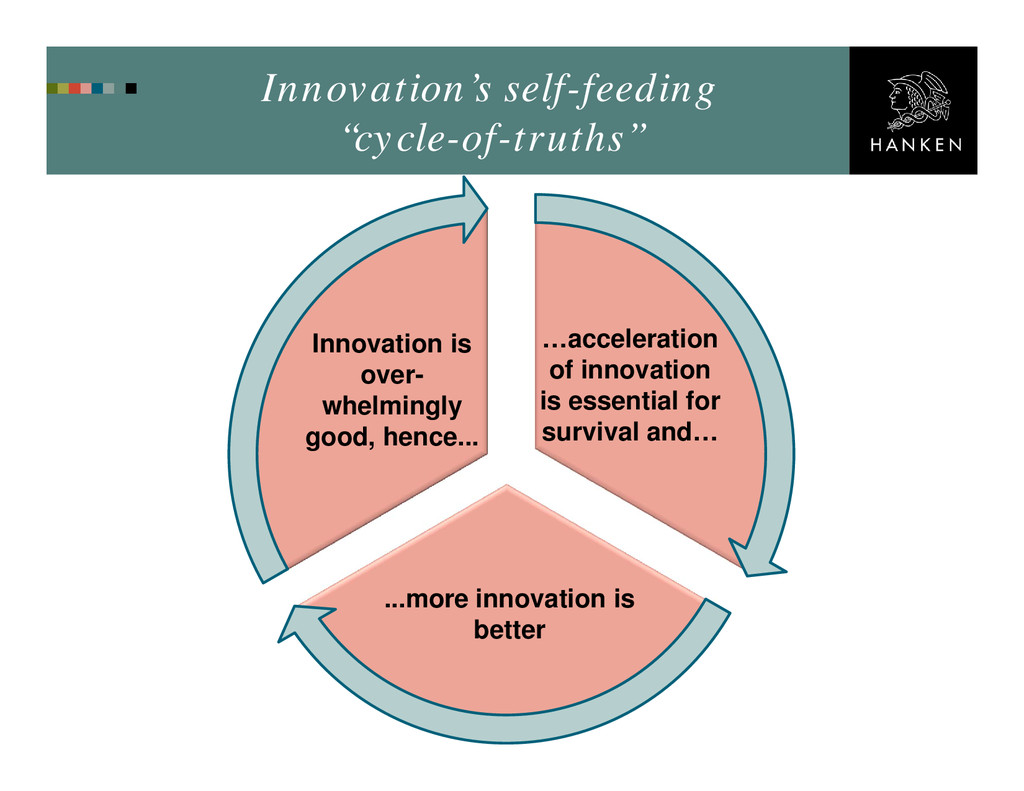

region) More innovation is better Innovation is over- whelmingly good Three themes of the book The nature of innovation is systemic There are unintended consequences of every innovation Innovation has become an uncontested ideology in the West

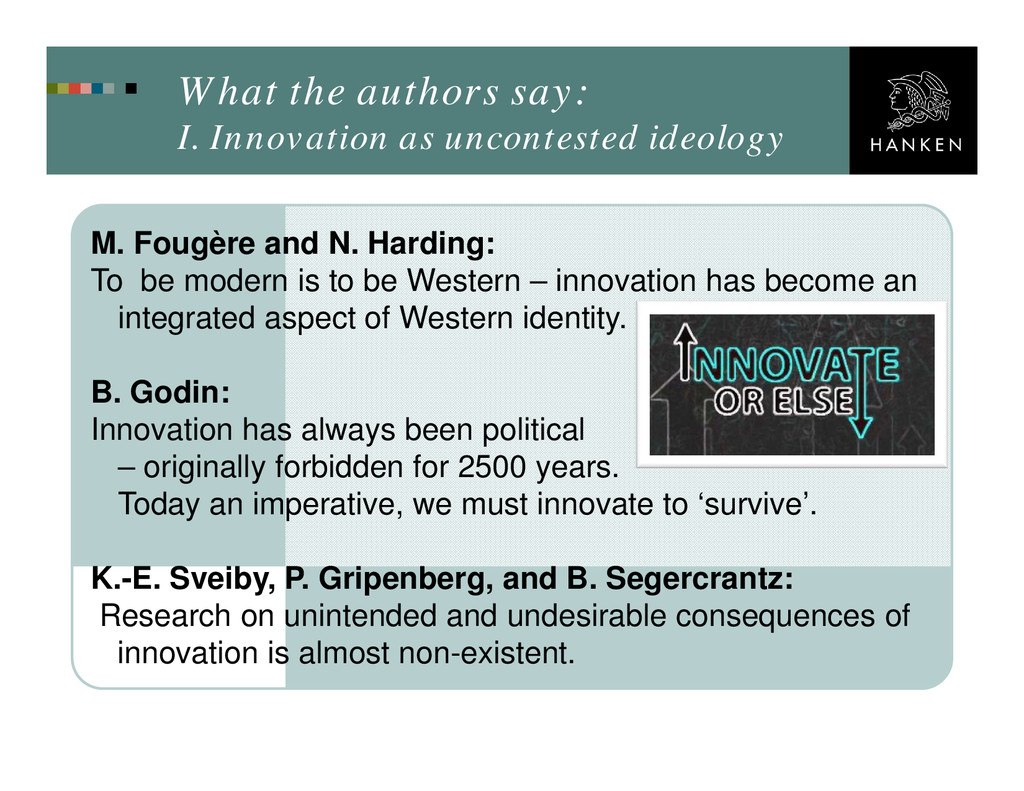

Fougère and N. Harding: To be modern is to be Western – innovation has become an integrated aspect of Western identity. B. Godin: Innovation has always been political – originally forbidden for 2500 years. Today an imperative, we must innovate to ‘survive’. K.-E. Sveiby, P. Gripenberg, and B. Segercrantz: Research on unintended and undesirable consequences of innovation is almost non-existent.

Hasu, K.-H. Leitner, N. Solitander, and U. Varblane: The innovation imperative: acceleration of innovation is both socially desirable for developing areas, and a mechanism of greed and unsustainability for global enterprises. K.-E. Sveiby: Radical innovations alter the context and lead to temporary incompetence that increase the risk for negative consequences. K.-H. Leitner: Weak signals for opting out of the innovation race: no- innovation, pseudo-innovation and eco-innovation.

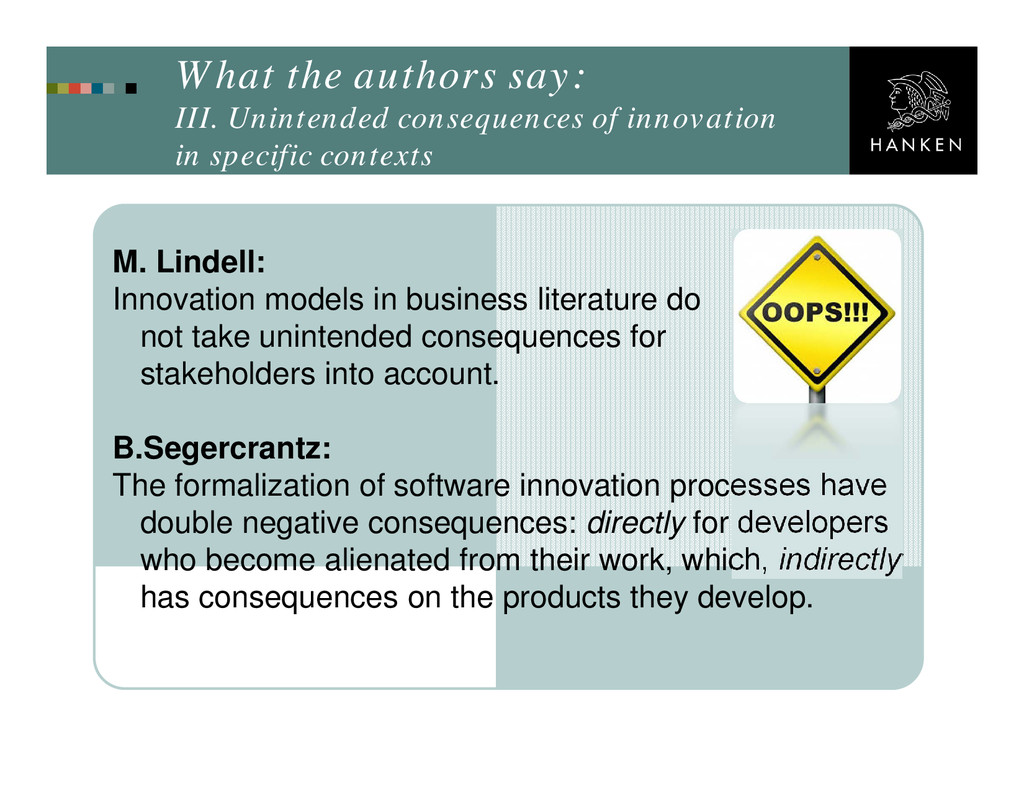

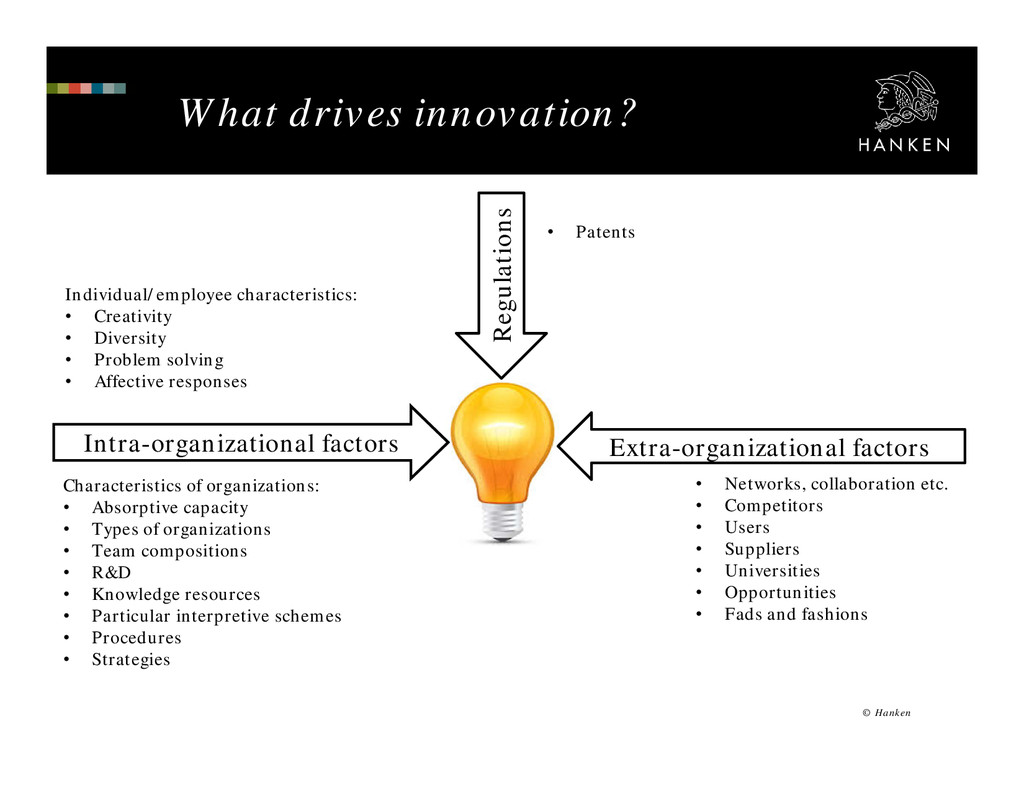

specific contexts M. Lindell: Innovation models in business literature do not take unintended consequences for stakeholders into account. B.Segercrantz: The formalization of software innovation processes have double negative consequences: directly for developers who become alienated from their work, which, indirectly has consequences on the products they develop.

specific contexts Canibano, O. Basilio, and M.P. Sanchez: Organizational innovations distort work boundaries. This induces multitasking and intensifies and accelerates the work pace. This lead to reduced employee well- being: stress, anxiety and pressures. M. Matsumoto and K. Kawajiri: The indirect effects of ICT on CO2 emissions: Transfer of production from industrialized to developing countries with much lower CO2 efficiency increases the total CO2 emissions.

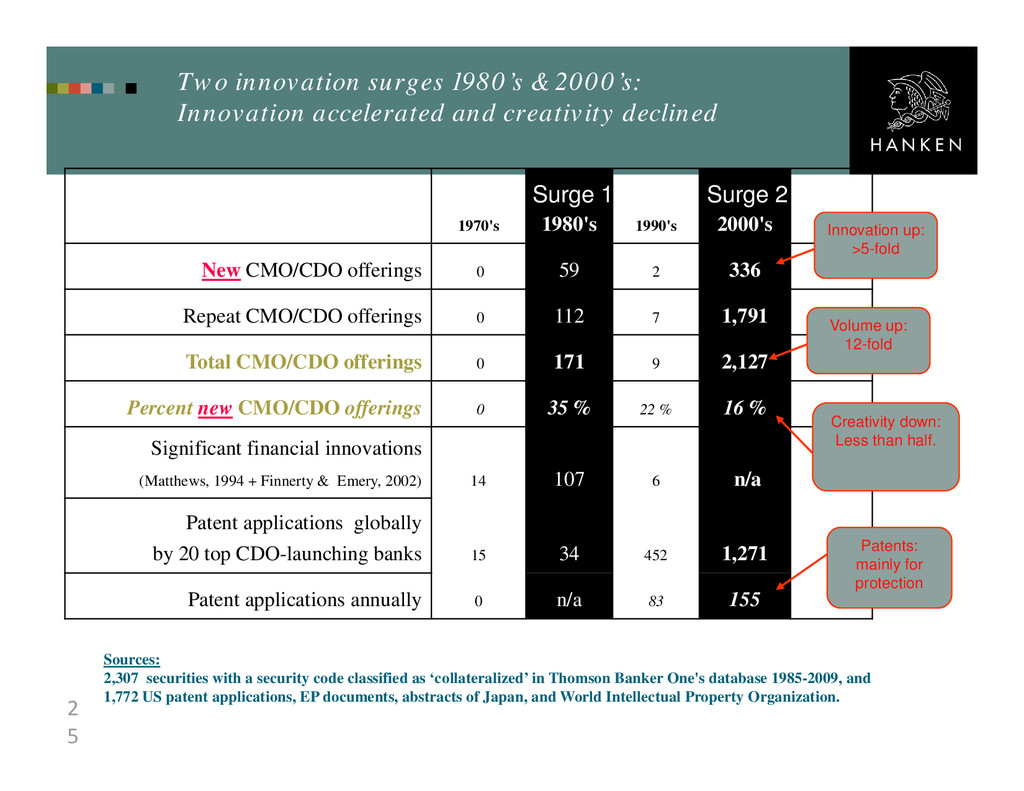

The net beneficial effects of innovation for society are reduced by its undesirable effects. Firms and innovators reap the economic benefits. No evidence that innovation, incl. its non-economic effects and indirect consequences are good for society as a whole. 2. Myth: Acceleration of innovation is essential for survival (firm, country, region). Two surges of financial innovation were highly instrumental in the lead up to the Global Financial Crisis. Speeding up became dumbing down. 3. Myth: More innovation is better. Innovation may merely multiply the effects of an inherently flawed design (due to path dependency). Hanken Svenska handelshögskolan / Hanken School of Economics www.hanken.fi

routinized Less than 0.5% discuss other consequences than the intended positive effects. Concern: Negative effects of innovation may be increasing. Negative effects and indirect consequences are neglected by research funding bodies Acceleration of innovation is encouraged on all levels in society ICT-enabled innovation is systemic - local effects become global Huge unexploited potential: Explore how to reduce negative and unintended effects of innovation. This will improve the net effects for society. Hanken Svenska handelshögskolan / Hanken School of Economics www.hanken.fi

old theories: the future of theorizing about innovation in complex adaptive systems European Centre for Living Technology, ECLT, Venice May 5th 2014 Karl Erik Sveiby

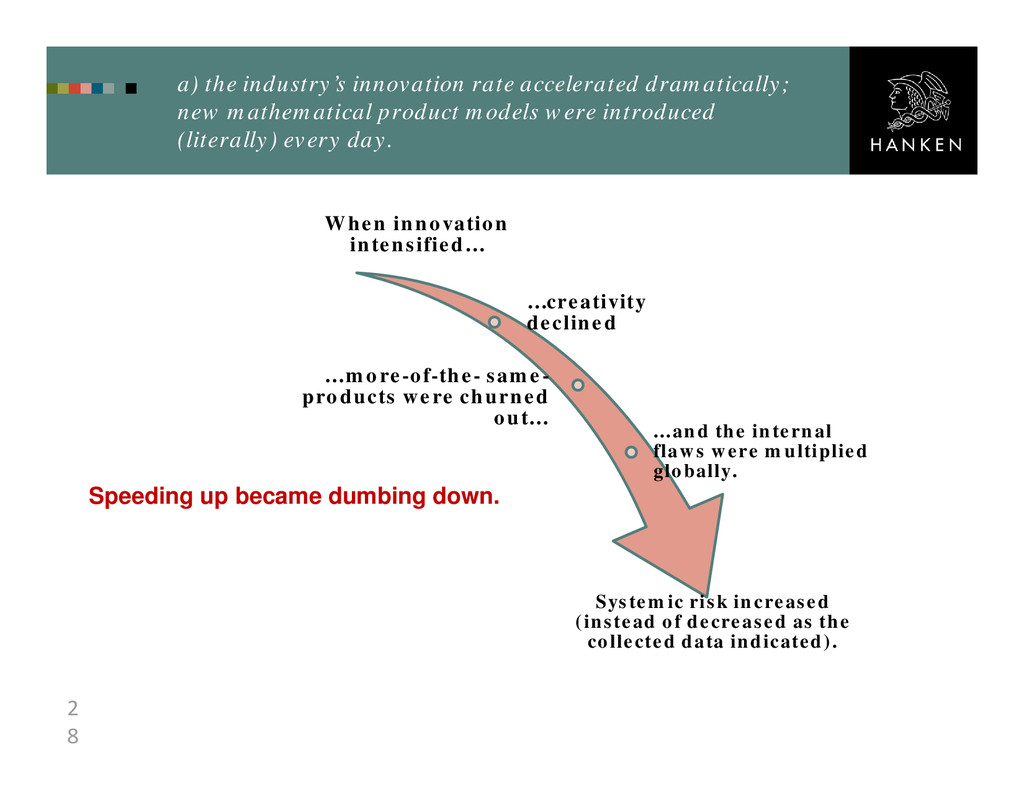

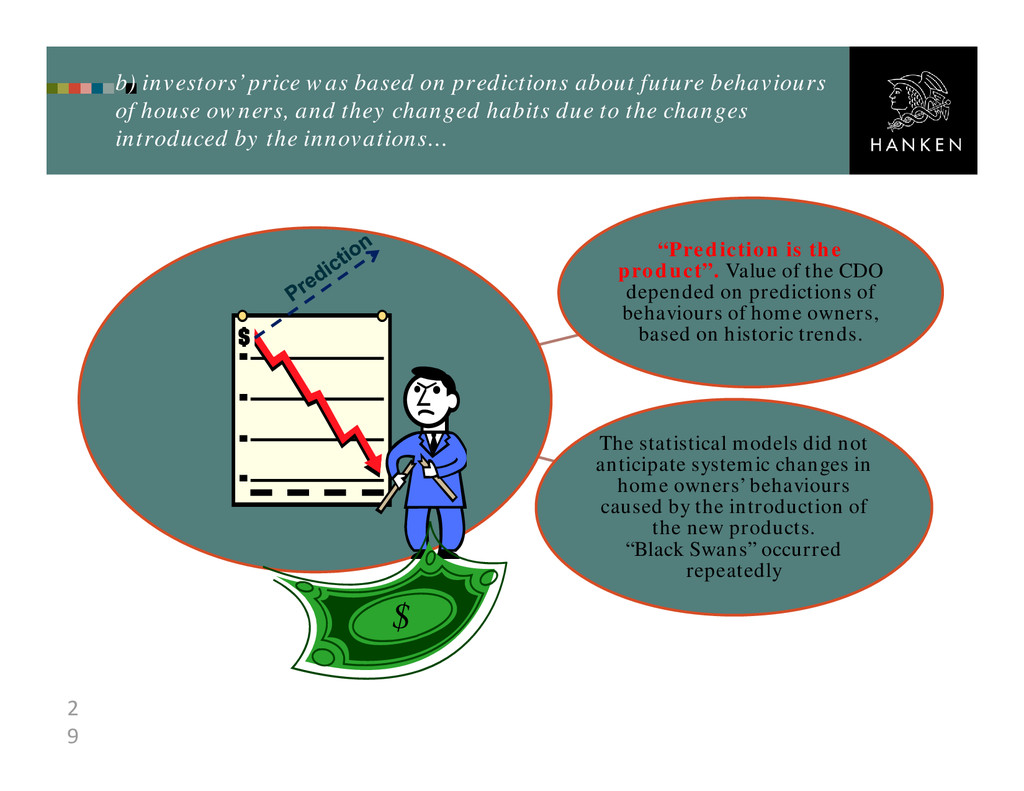

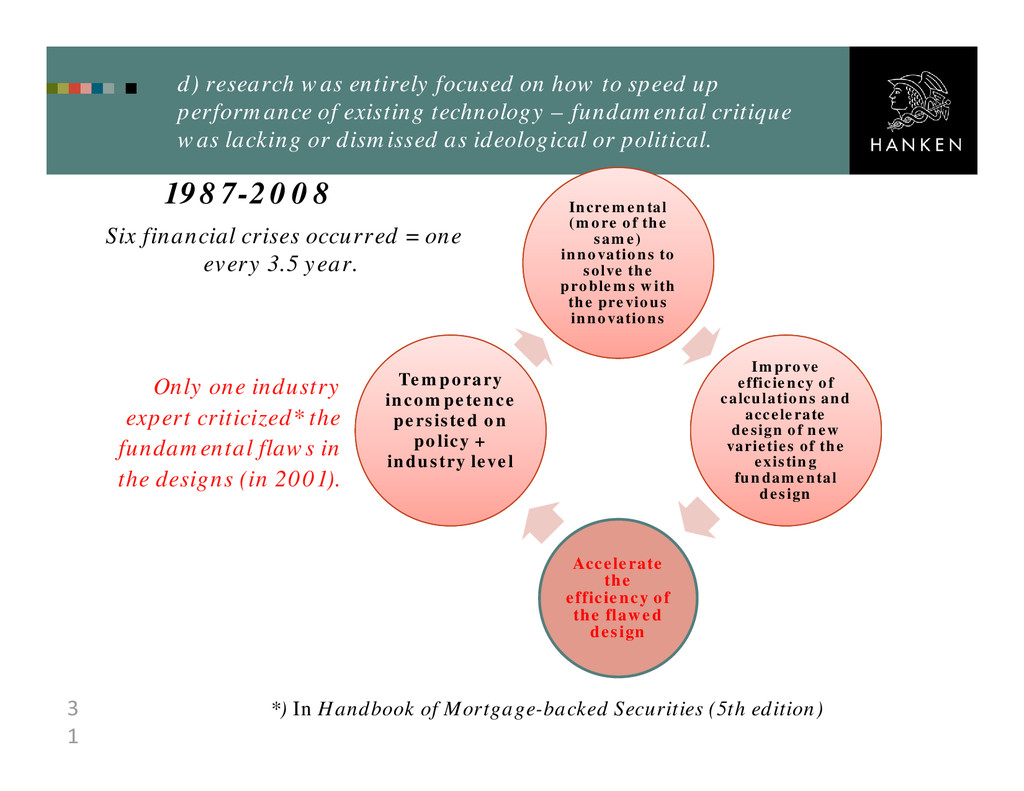

» a) by banks to develop new financial products; » b) by investors to predict the outcome of their investments; » c) by regulators in order to monitor of the markets, and; » d) by researchers to analyse the industry and build better theory. Despite all the data, most of them were caught by the crash 2008. Why? » The securitization innovation + ICT created dramatic systemic change in the financial industry's structure from 1983 onwards: » a) the industry’s innovation rate accelerated dramatically; new mathematical product models were introduced (literally) every day. » b) investors’ price was based on predictions about future behaviours of house owners, and they changed habits due to changes in banking industry… » c) regulators were blind; data collected were based on outdated view of the industry structure. » d) research was focused on how to improve performance of existing technology – fundamental critique was lacking or dismissed as ideological or political.

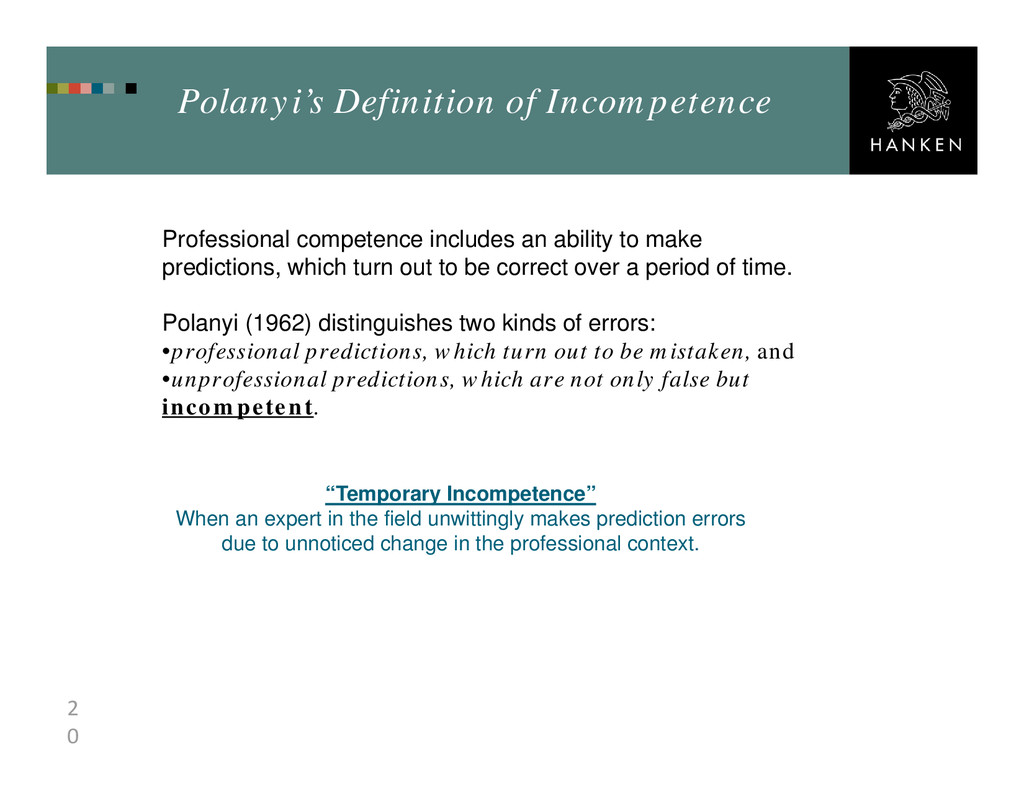

to act in a (professional) context From Polanyi 1962 •Competence (Michael Polanyi 1962) •Unintended consequences (Robert K. Merton 1936) •Stakeholder theory (R.E. Freeman 1984) Theories:

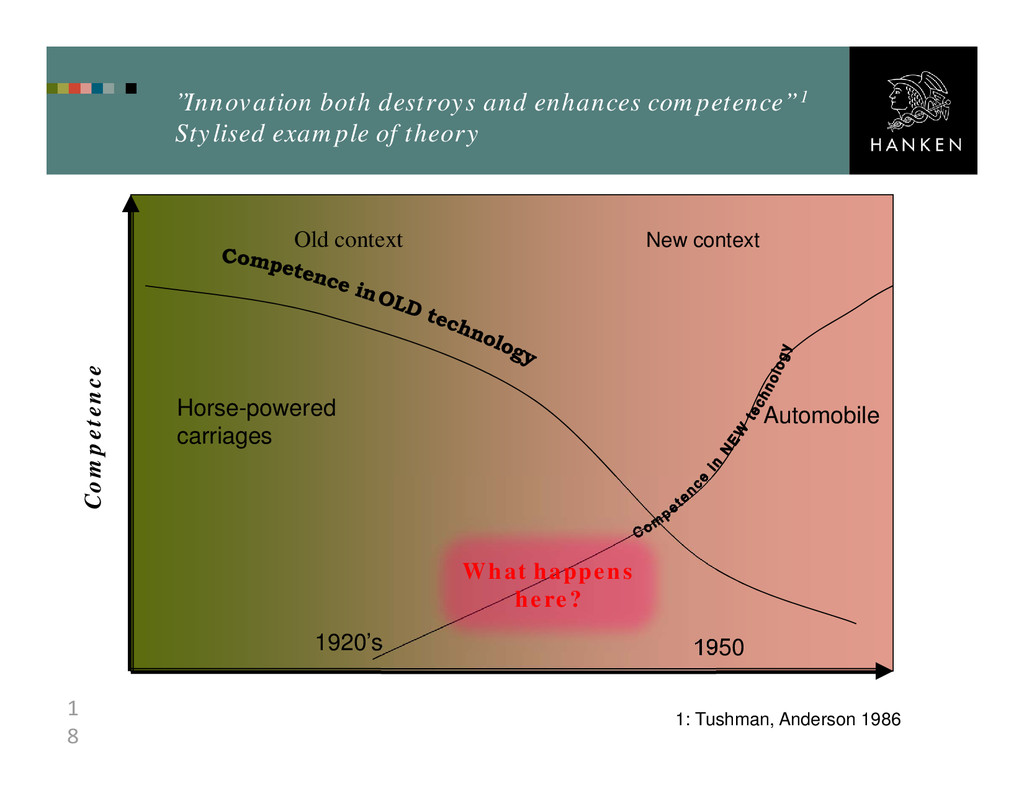

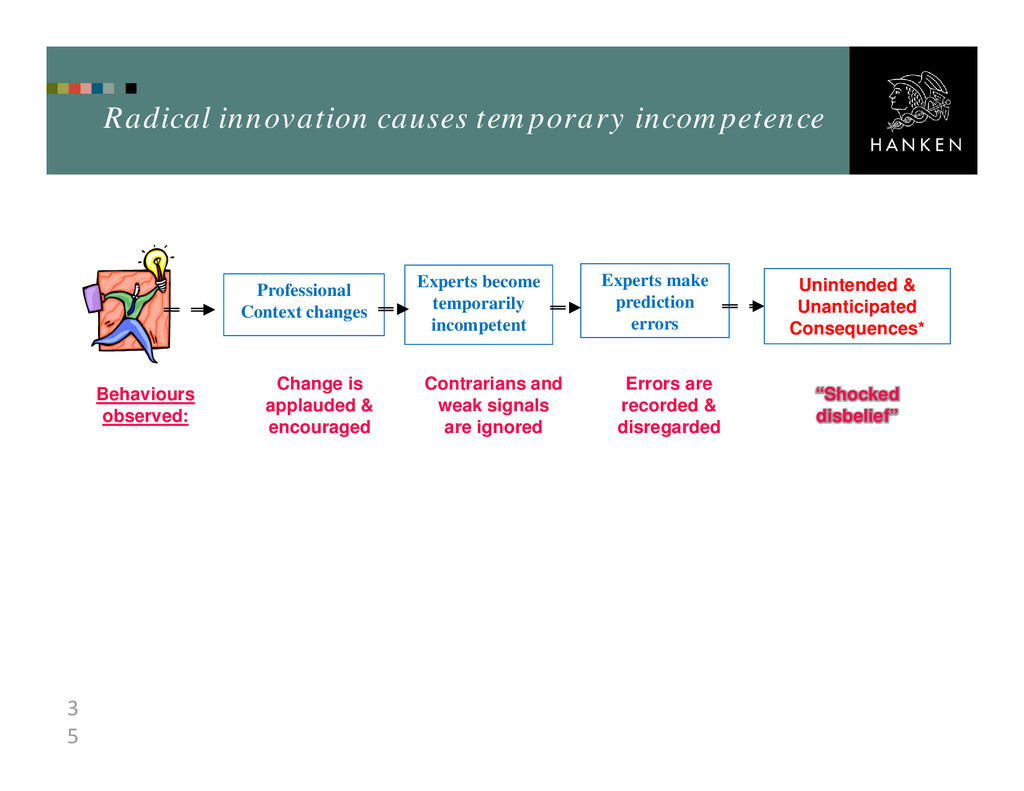

ability to make predictions, which turn out to be correct over a period of time. Polanyi (1962) distinguishes two kinds of errors: •professional predictions, which turn out to be mistaken, and •unprofessional predictions, which are not only false but incompetent. “Temporary Incompetence” When an expert in the field unwittingly makes prediction errors due to unnoticed change in the professional context.

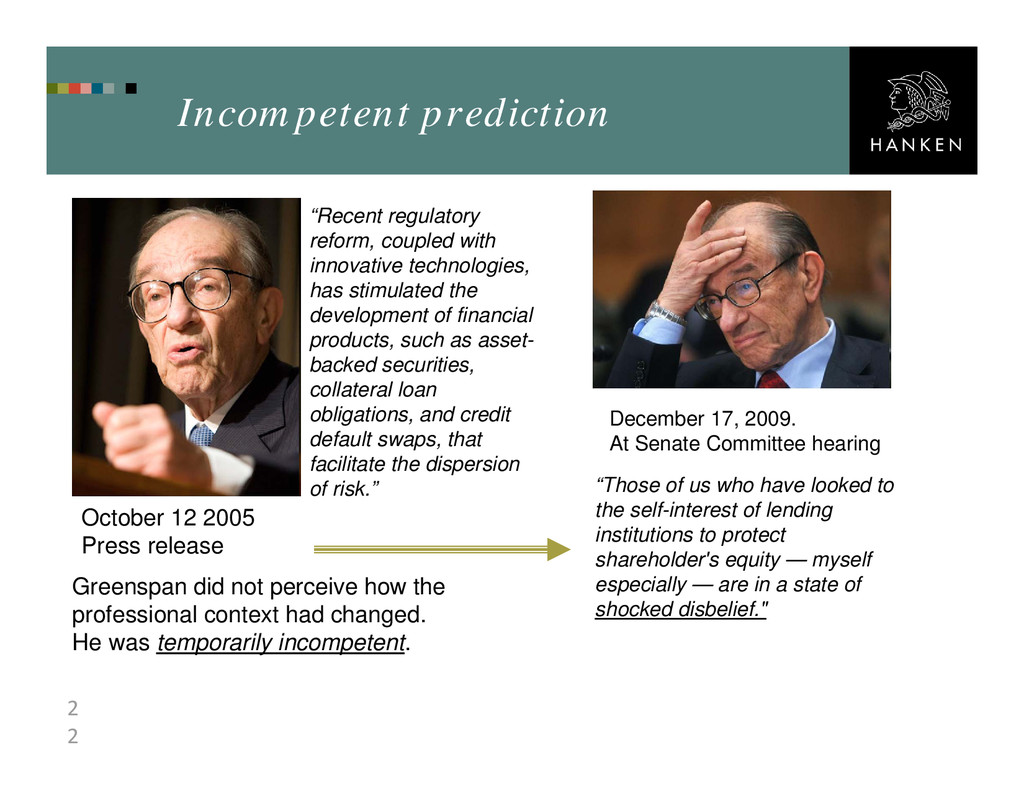

hearing “Those of us who have looked to the self-interest of lending institutions to protect shareholder's equity — myself especially — are in a state of shocked disbelief." “Recent regulatory reform, coupled with innovative technologies, has stimulated the development of financial products, such as asset- backed securities, collateral loan obligations, and credit default swaps, that facilitate the dispersion of risk.” October 12 2005 Press release Greenspan did not perceive how the professional context had changed. He was temporarily incompetent.

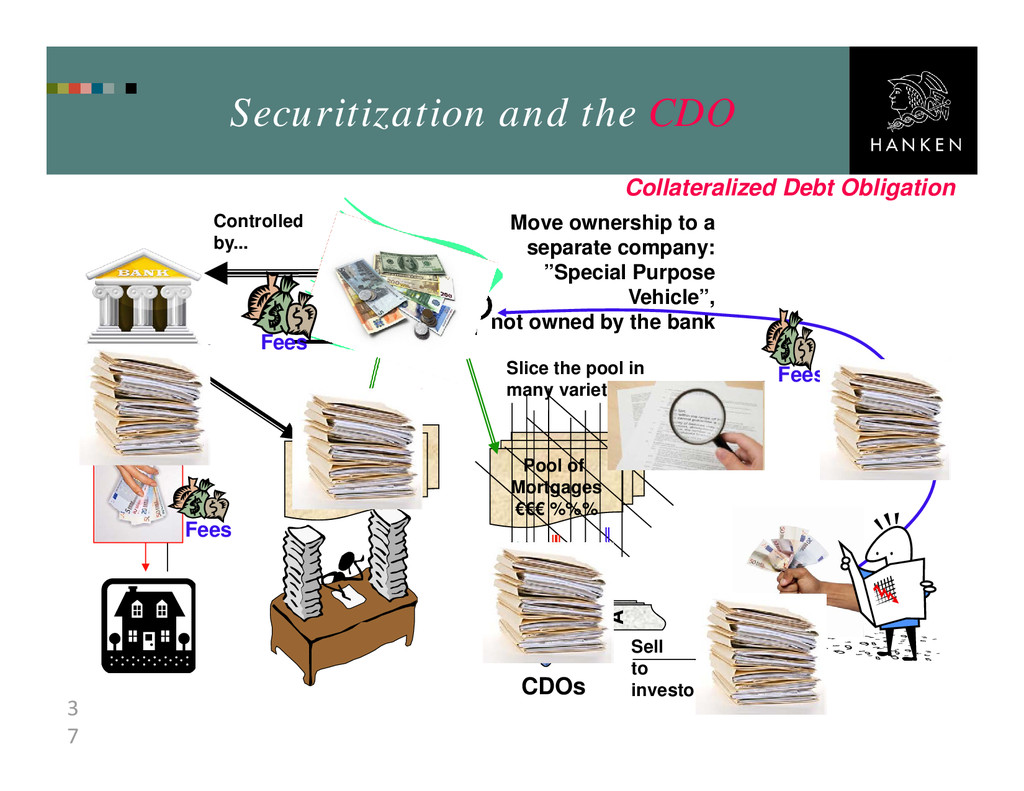

EP documents, etc. •264 chapters in 6 editions of the Handbook of Mortgage-backed Securities •Newspaper articles covering 1980 – 2008. Focus and Data Focus of Study: Securitization - A financial technology to design new securities. The Collateralized Debt Obligation ”CDO” - One of the products developed with securitization.

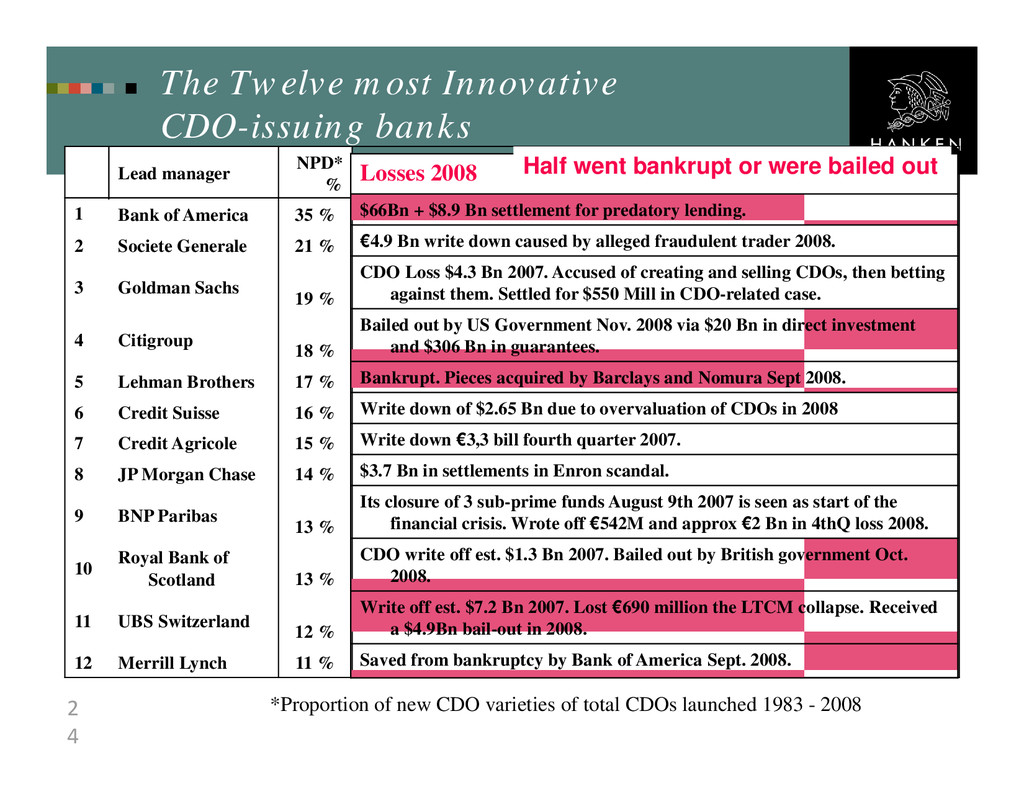

Switzerland 11 13 % Royal Bank of Scotland 10 13 % BNP Paribas 9 14 % JP Morgan Chase 8 15 % Credit Agricole 7 16 % Credit Suisse 6 17 % Lehman Brothers 5 18 % Citigroup 4 19 % Goldman Sachs 3 21 % Societe Generale 2 35 % Bank of America 1 NPD* % Lead manager The Twelve most Innovative CDO-issuing banks Losses 2008 $66Bn + $8.9 Bn settlement for predatory lending. €4.9 Bn write down caused by alleged fraudulent trader 2008. CDO Loss $4.3 Bn 2007. Accused of creating and selling CDOs, then betting against them. Settled for $550 Mill in CDO-related case. Bailed out by US Government Nov. 2008 via $20 Bn in direct investment and $306 Bn in guarantees. Bankrupt. Pieces acquired by Barclays and Nomura Sept 2008. Write down of $2.65 Bn due to overvaluation of CDOs in 2008 Write down €3,3 bill fourth quarter 2007. $3.7 Bn in settlements in Enron scandal. Its closure of 3 sub-prime funds August 9th 2007 is seen as start of the financial crisis. Wrote off €542M and approx €2 Bn in 4thQ loss 2008. CDO write off est. $1.3 Bn 2007. Bailed out by British government Oct. 2008. Write off est. $7.2 Bn 2007. Lost €690 million the LTCM collapse. Received a $4.9Bn bail-out in 2008. Saved from bankruptcy by Bank of America Sept. 2008. Half went bankrupt or were bailed out *Proportion of new CDO varieties of total CDOs launched 1983 - 2008

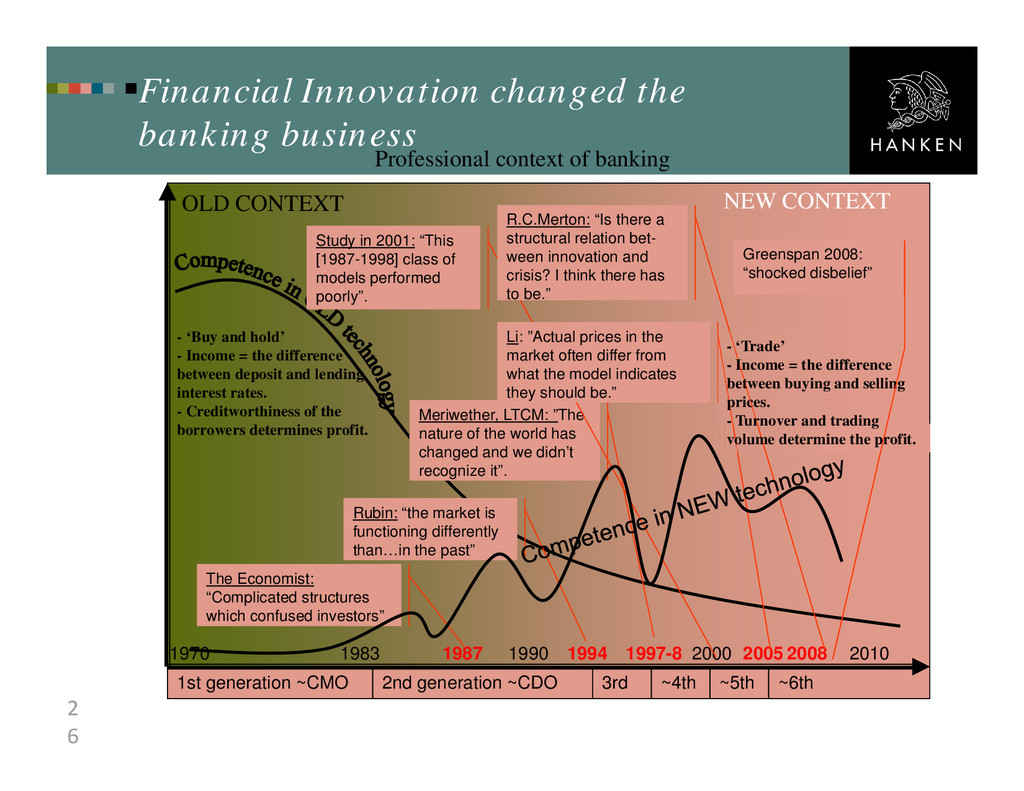

2 6 Financial Innovation changed the banking business Professional context of banking New Context 1970 2010 1983 1990 2000 1987 1994 1997-8 2008 2005 OLD CONTEXT NEW CONTEXT The Economist: “Complicated structures which confused investors” Rubin: “the market is functioning differently than…in the past” Meriwether, LTCM: ”The nature of the world has changed and we didn’t recognize it”. Study in 2001: “This [1987-1998] class of models performed poorly”. Li: ”Actual prices in the market often differ from what the model indicates they should be.” R.C.Merton: “Is there a structural relation bet- ween innovation and crisis? I think there has to be.” - ‘Trade’ - Income = the difference between buying and selling prices. - Turnover and trading volume determine the profit. - ‘Buy and hold’ - Income = the difference between deposit and lending interest rates. - Creditworthiness of the borrowers determines profit. Greenspan 2008: “shocked disbelief”

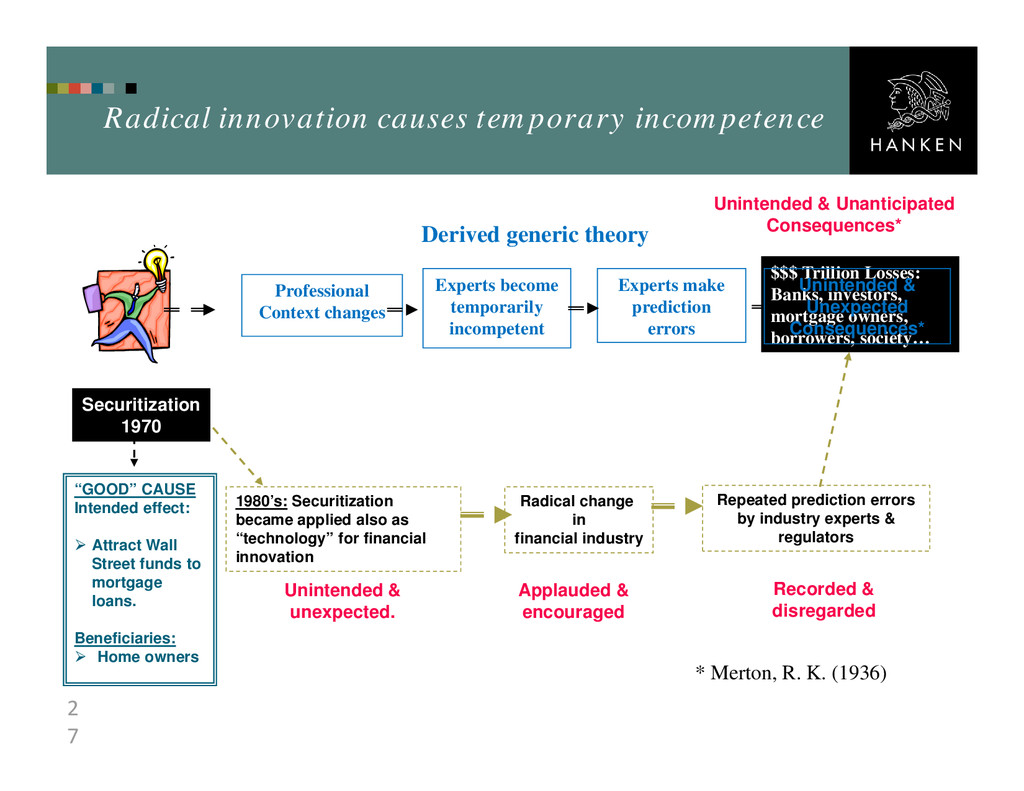

Banks, investors, mortgage owners, borrowers, society… Unintended & Unanticipated Consequences* 1980’s: Securitization became applied also as “technology” for financial innovation Repeated prediction errors by industry experts & regulators Radical innovation causes temporary incompetence Experts become temporarily incompetent Professional Context changes Experts make prediction errors “GOOD” CAUSE Intended effect: Attract Wall Street funds to mortgage loans. Beneficiaries: Home owners * Merton, R. K. (1936) Derived generic theory Unintended & unexpected. Applauded & encouraged Recorded & disregarded Unintended & Unexpected Consequences* Securitization 1970

mathematical product models were introduced (literally) every day. When innovation intensified… …creativity declined ...more-of-the- same- products were churned out... ...and the internal flaws were multiplied globally. Systemic risk increased (instead of decreased as the collected data indicated). Speeding up became dumbing down.

future behaviours of house owners, and they changed habits due to the changes introduced by the innovations… “Prediction is the product”. Value of the CDO depended on predictions of behaviours of home owners, based on historic trends. The statistical models did not anticipate systemic changes in home owners’ behaviours caused by the introduction of the new products. “Black Swans” occurred repeatedly $

on outdated view of the industry structure. Unexpected: Securitization rapidly changed the professional context. Industry statistics lagged behind the change, therefore… …masses of irrelevant data were collected, analysed, and reported… …systemic effects on the financial industry were not perceived for 15 years (until mid 1990’s): Temporary incompetence persisted on policy + industry level

speed up performance of existing technology – fundamental critique was lacking or dismissed as ideological or political. Incremental (more of the same) innovations to solve the problems with the previous innovations Improve efficiency of calculations and accelerate design of new varieties of the existing fundamental design Accelerate the efficiency of the flawed design Temporary incompetence persisted on policy + industry level *) In Handbook of Mortgage-backed Securities (5th edition) Only one industry expert criticized* the fundamental flaws in the designs (in 2001). Six financial crises occurred = one every 3.5 year. 1987-2008

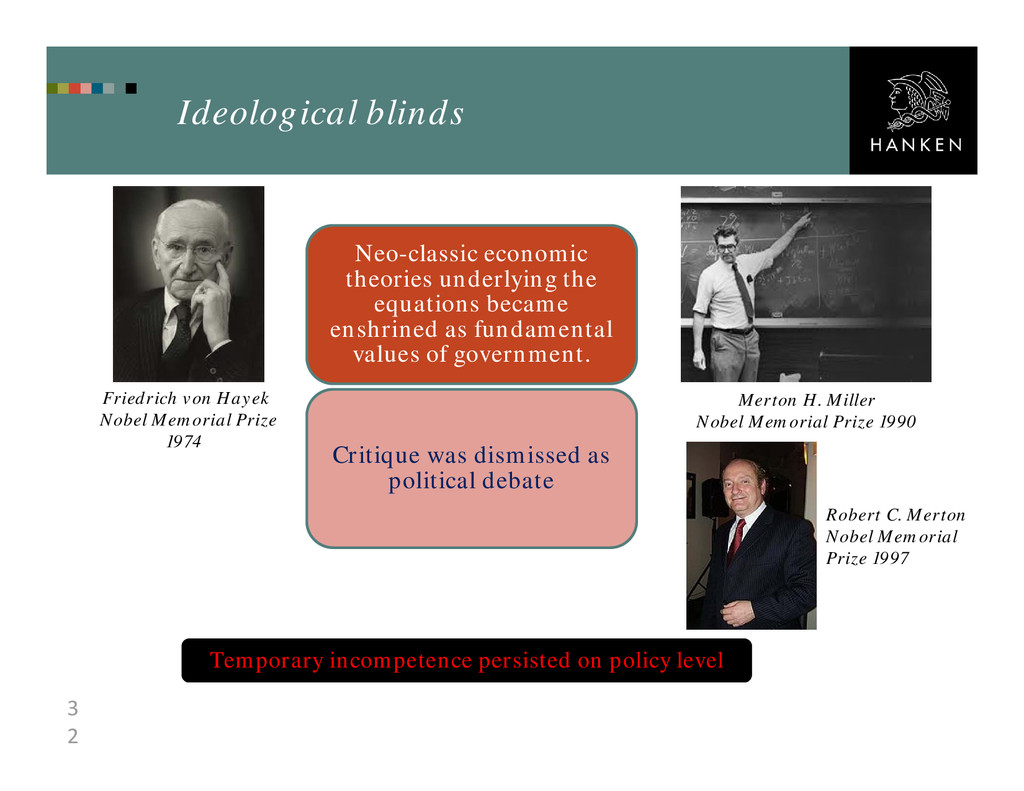

became enshrined as fundamental values of government. Critique was dismissed as political debate Temporary incompetence persisted on policy level Friedrich von Hayek Nobel Memorial Prize 1974 Merton H. Miller Nobel Memorial Prize 1990 Robert C. Merton Nobel Memorial Prize 1997

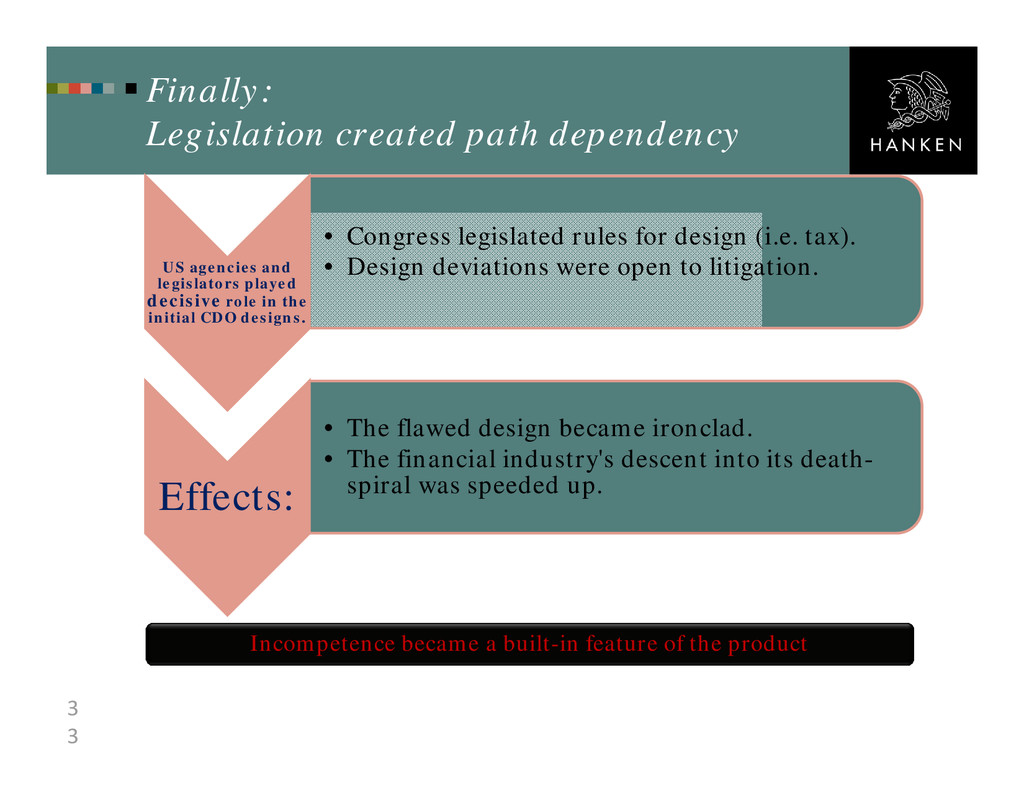

legislators played decisive role in the initial CDO designs. • Congress legislated rules for design (i.e. tax). • Design deviations were open to litigation. Effects: • The flawed design became ironclad. • The financial industry's descent into its death- spiral was speeded up. Incompetence became a built-in feature of the product

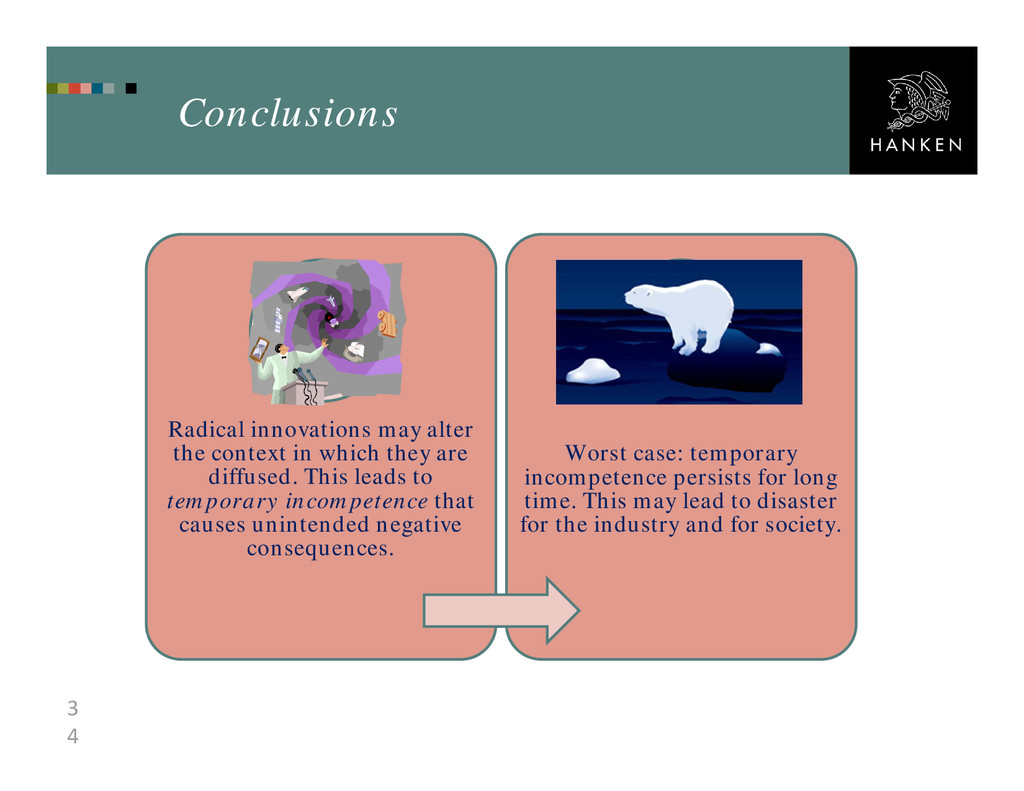

which they are diffused. This leads to temporary incompetence that causes unintended negative consequences. Worst case: temporary incompetence persists for long time. This may lead to disaster for the industry and for society.

incompetent Professional Context changes Experts make prediction errors Contrarians and weak signals are ignored Change is applauded & encouraged Errors are recorded & disregarded Unintended & Unanticipated Consequences* “Shocked disbelief” Behaviours observed:

societal consequences. Should Leaders care? Learnings from the case 1. Change attitude: from Pro-innovation Biased to Neutral: Innovation has both desirable and undesirable consequences. Innovation is not always the solution to a problem. It may merely multiply the effects of an inherently flawed design due to path dependencies and systemic effects. 2. Expand: Think outside the box of your own firm The net effect of an innovation is what counts. What is good for the firm short term may turn back upon it via society or others in the industry. Innovations based on ICT have unpredictable systemic effects globally. 3. Accelerate with care: There is an unknown “speed limit” in your industry We do know that speeding can be costly for both industry and society. Shift from Marathon running to Interval training: make reflexive breaks. 4. Reflect: Some suggested questions for reducing temporary incompetence: To reduce herding: Is the whole industry embracing the same new technology? To reduce myopia: Are there weak signals that suggest opportunities elsewhere? To reduce group-think: Are there contrarian thinkers assigned to the innovation teams? To reduce blindness: Are we measuring the new with the instruments of the old? To reduce power of knowledge: Is one small group of experts driving our direction?

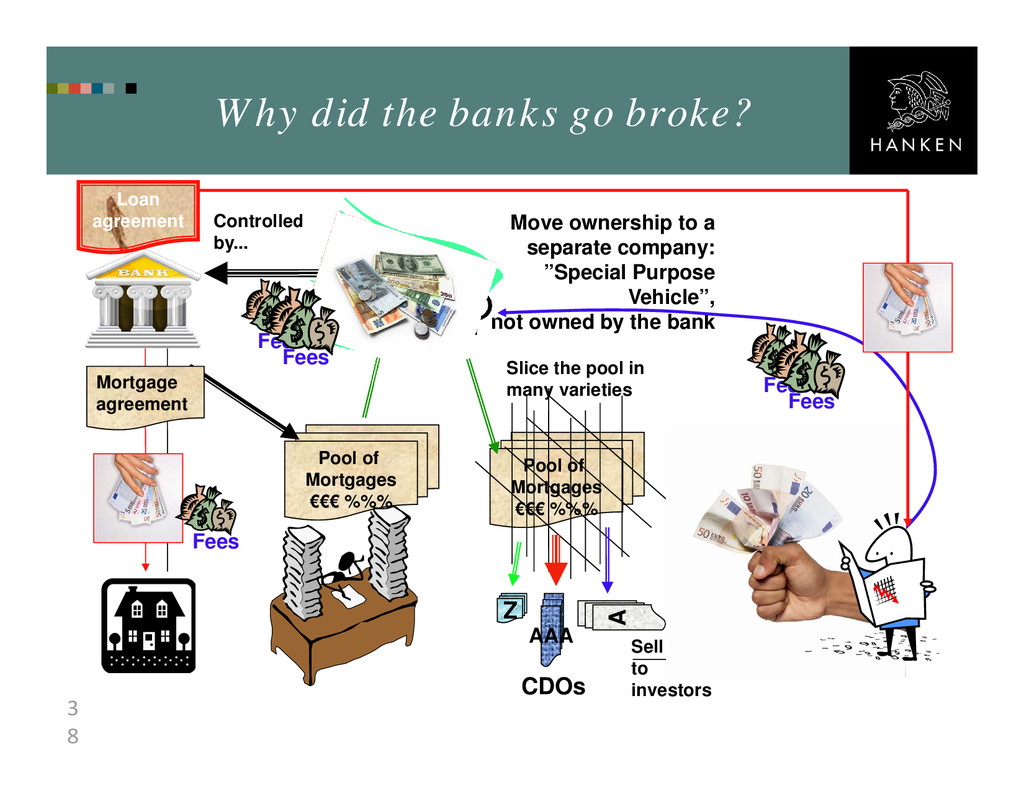

%%% Move ownership to a separate company: ”Special Purpose Vehicle”, not owned by the bank Pool of Mortgages €€€ %%% Slice the pool in many varieties Sell to investors Z AAA A Controlled by... Mortgage agreement CDOs Fees Fees Fees Collateralized Debt Obligation

Mortgages €€€ %%% Move ownership to a separate company: ”Special Purpose Vehicle”, not owned by the bank Pool of Mortgages €€€ %%% Slice the pool in many varieties Sell to investors Z AAA A Controlled by... Mortgage agreement CDOs Loan agreement Fees Fees Fees Fees Fees

of mortgage-backed securities (1-6th ed.). New York: Mcgraw-Hill. » Freeman, R. E. (1984). Strategic management: A stakeholder approach. Boston:Pitman. » Merton, R. K. (1936). The unanticipated consequences of purposive social action. American Sociological Review, 1, 894–904. » Polanyi, M. (1962). Personal knowledge: Towards a post-critical philosophy. Chicago: University of Chicago Press. » Sveiby, KE.; Gripenberg, P, Segercrantz, B. (2012). Challenging the Innovation Paradigm. New York:Routledge. » Tushman, M. L., & Anderson, P. (1986). Technological discontinuities and organizational environments. Administrative Science Quarterly, 31, 439–446.

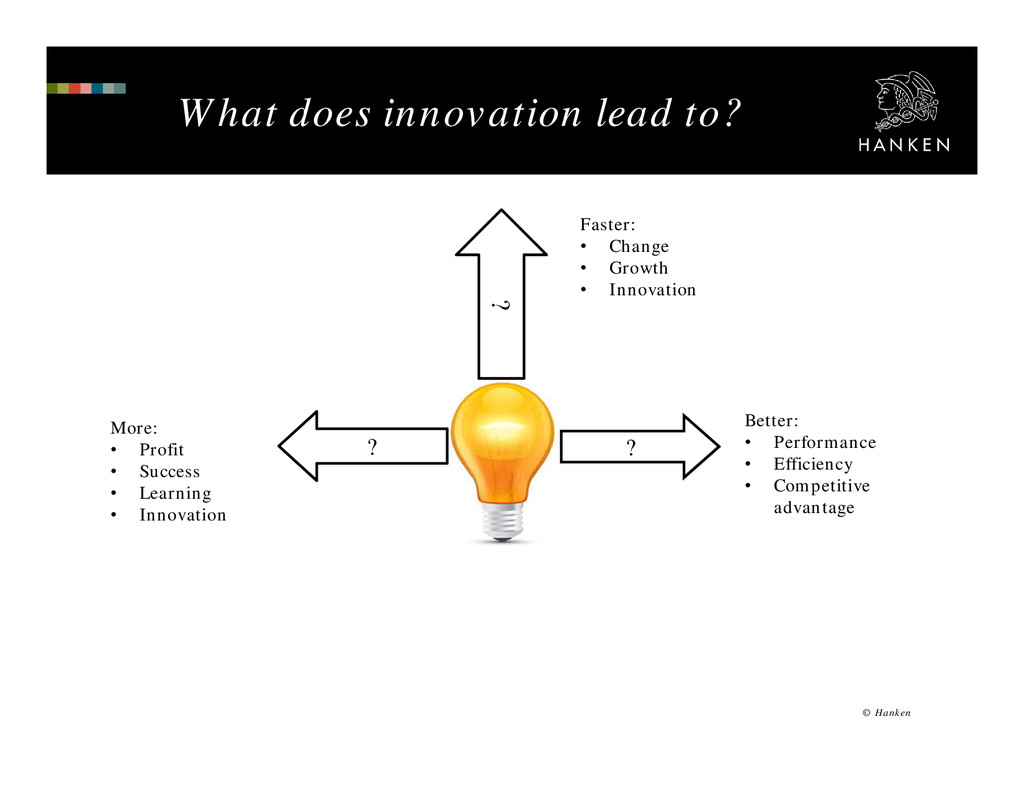

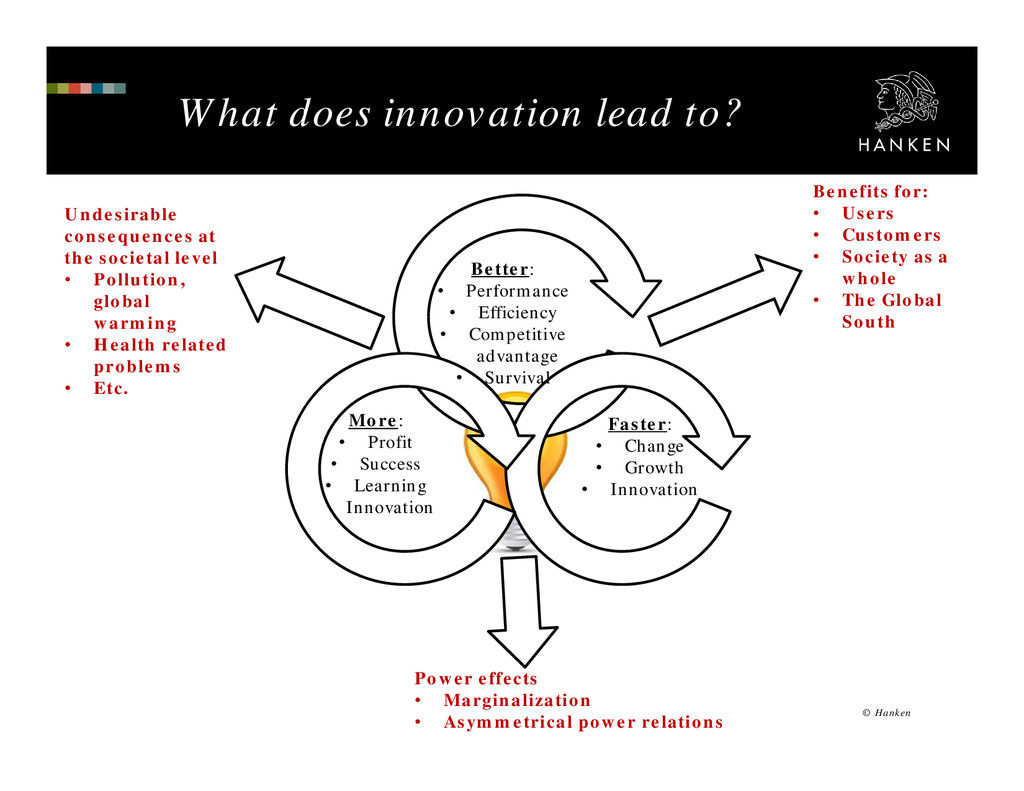

• Success • Learning • Innovation Faster: • Change • Growth • Innovation Better: • Performance • Efficiency • Competitive advantage • Survival Undesirable consequences at the societal level • Pollution, global warming • Health related problems • Etc. Benefits for: • Users • Customers • Society as a whole • The Global South Power effects • Marginalization • Asymmetrical power relations

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}