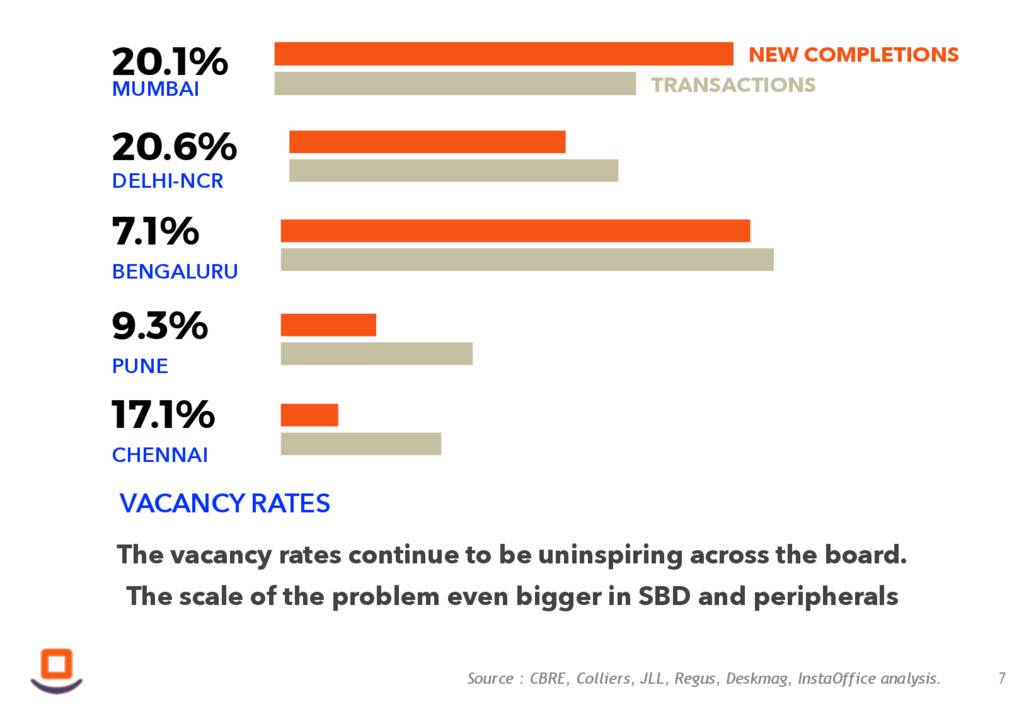

RATES 7 20.6% DELHI-NCR 7.1% BENGALURU 9.3% PUNE 17.1% CHENNAI 20.1% MUMBAI NEW COMPLETIONS TRANSACTIONS The vacancy rates continue to be uninspiring across the board. The scale of the problem even bigger in SBD and peripherals

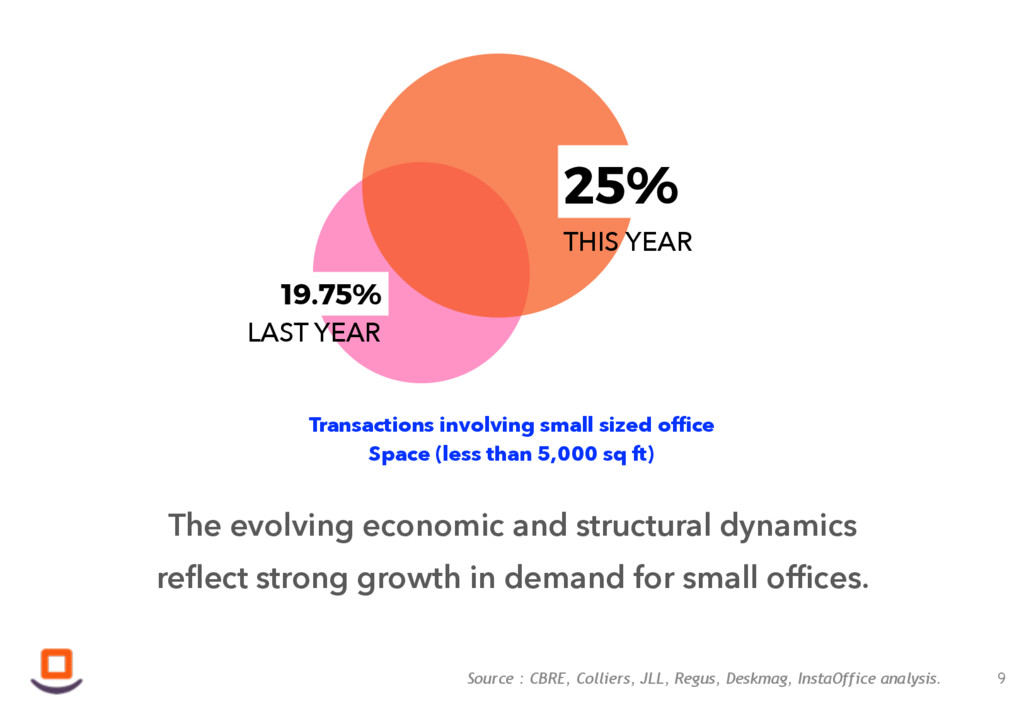

evolving economic and structural dynamics reflect strong growth in demand for small offices. Transactions involving small sized office Space (less than 5,000 sq ft) 9 LAST YEAR 19.75% 25% THIS YEAR

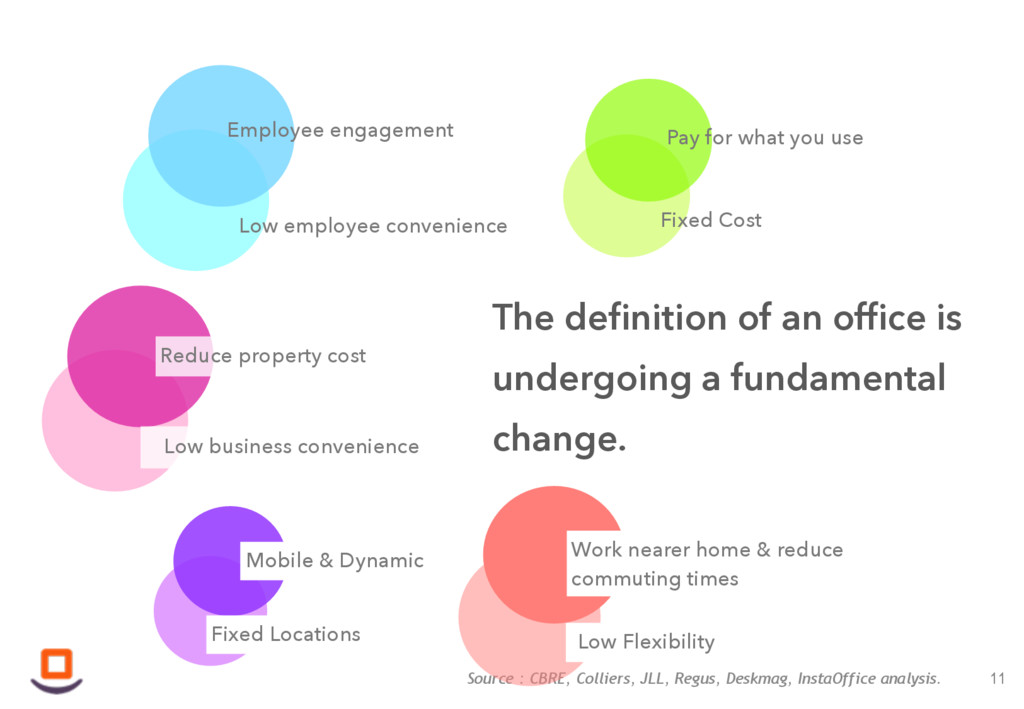

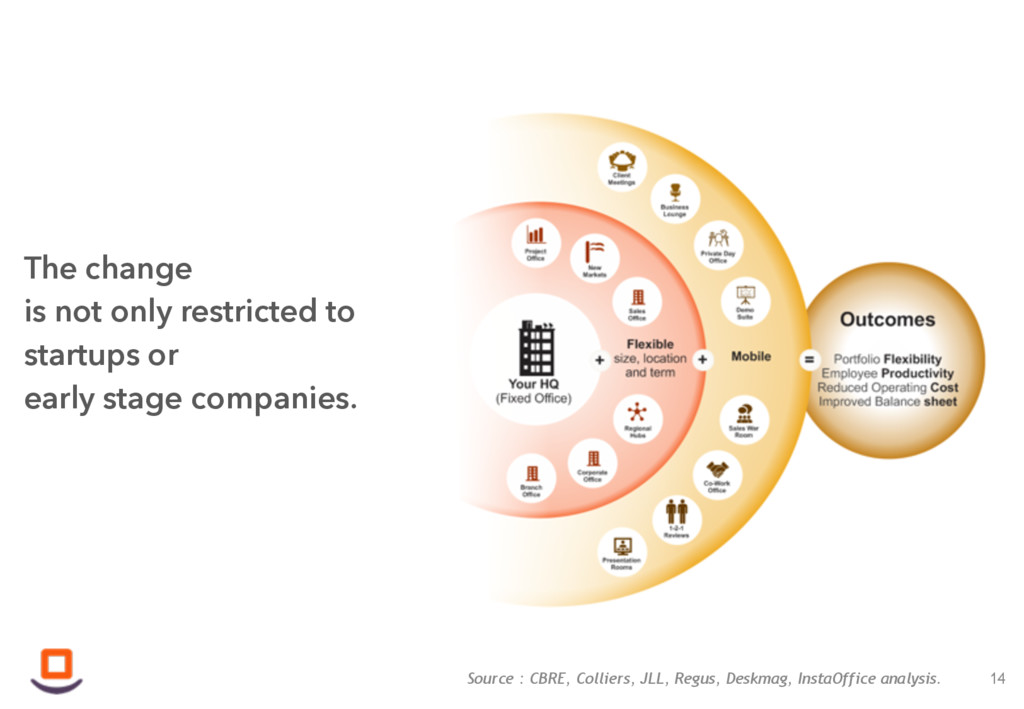

definition of an office is undergoing a fundamental change. 11 Mobile & Dynamic Fixed Locations Pay for what you use Fixed Cost Employee engagement Low employee convenience Reduce property cost Low business convenience Work nearer home & reduce commuting times Low Flexibility

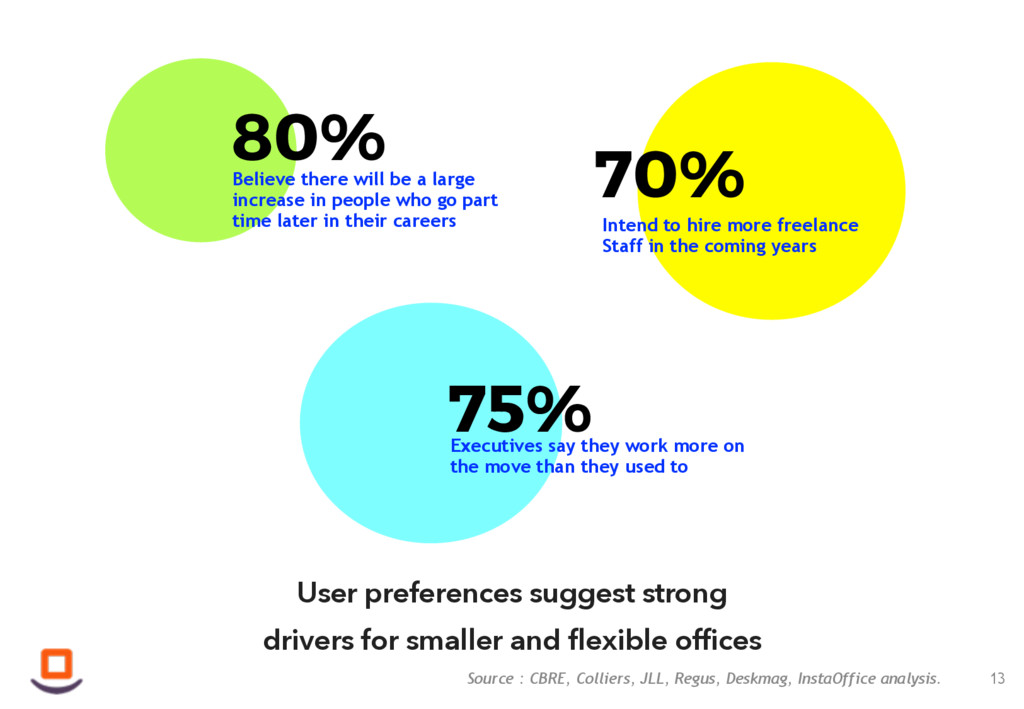

preferences suggest strong drivers for smaller and flexible offices 13 80% Believe there will be a large increase in people who go part time later in their careers 75% Executives say they work more on the move than they used to 70% Intend to hire more freelance Staff in the coming years

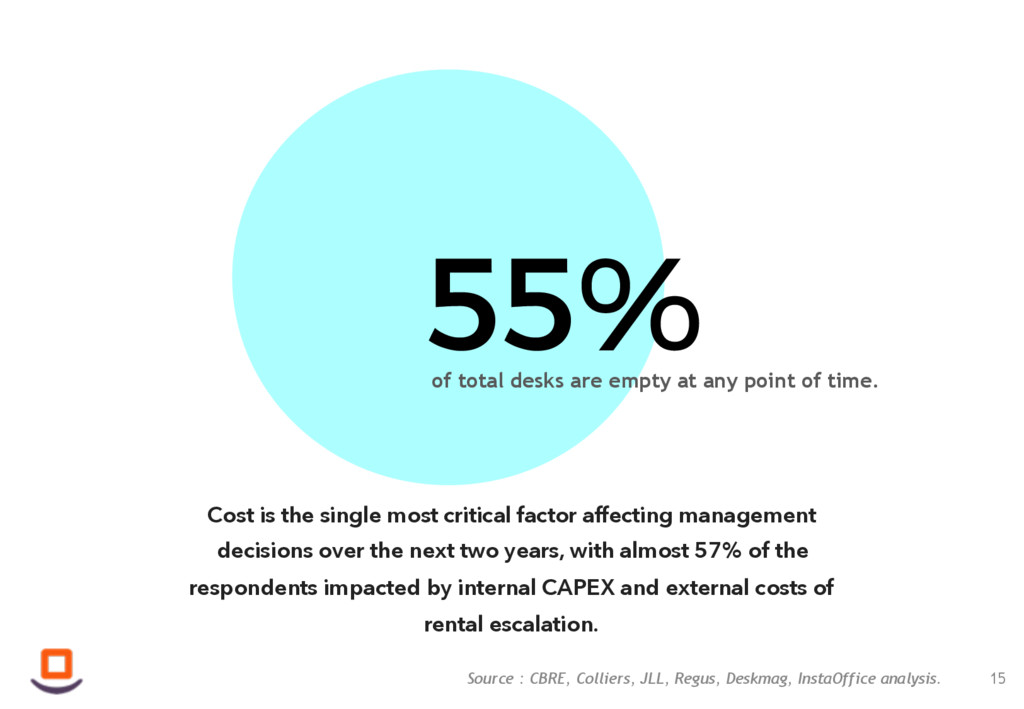

55% of total desks are empty at any point of time. Cost is the single most critical factor affecting management decisions over the next two years, with almost 57% of the respondents impacted by internal CAPEX and external costs of rental escalation.

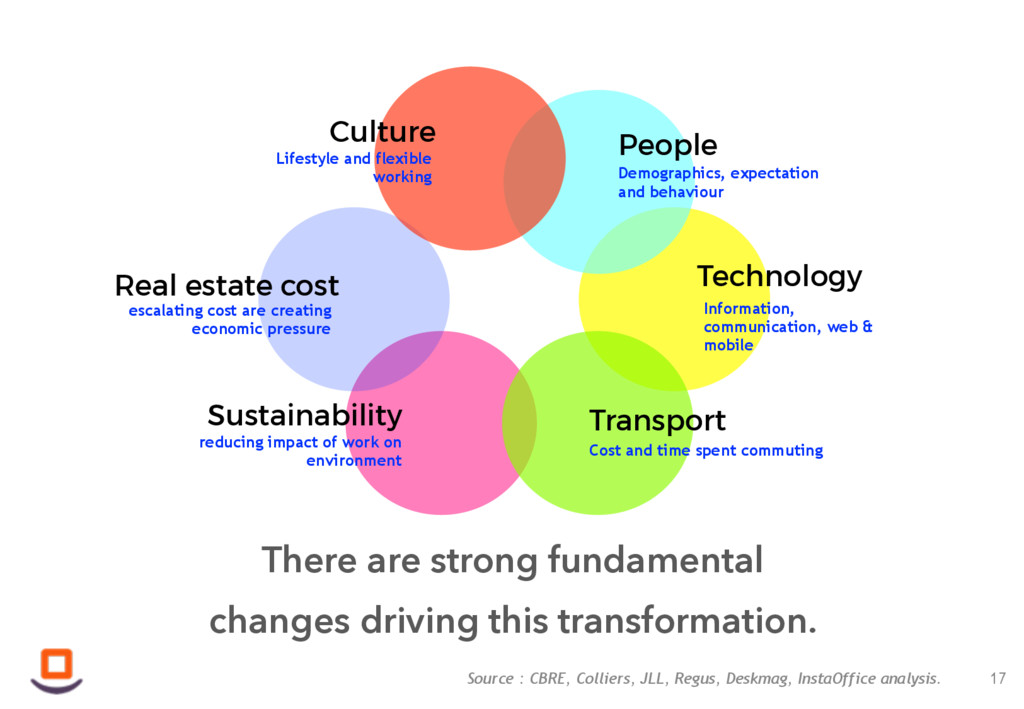

are strong fundamental changes driving this transformation. 17 Sustainability reducing impact of work on environment Technology Information, communication, web & mobile Transport Cost and time spent commuting People Demographics, expectation and behaviour Real estate cost escalating cost are creating economic pressure Culture Lifestyle and flexible working

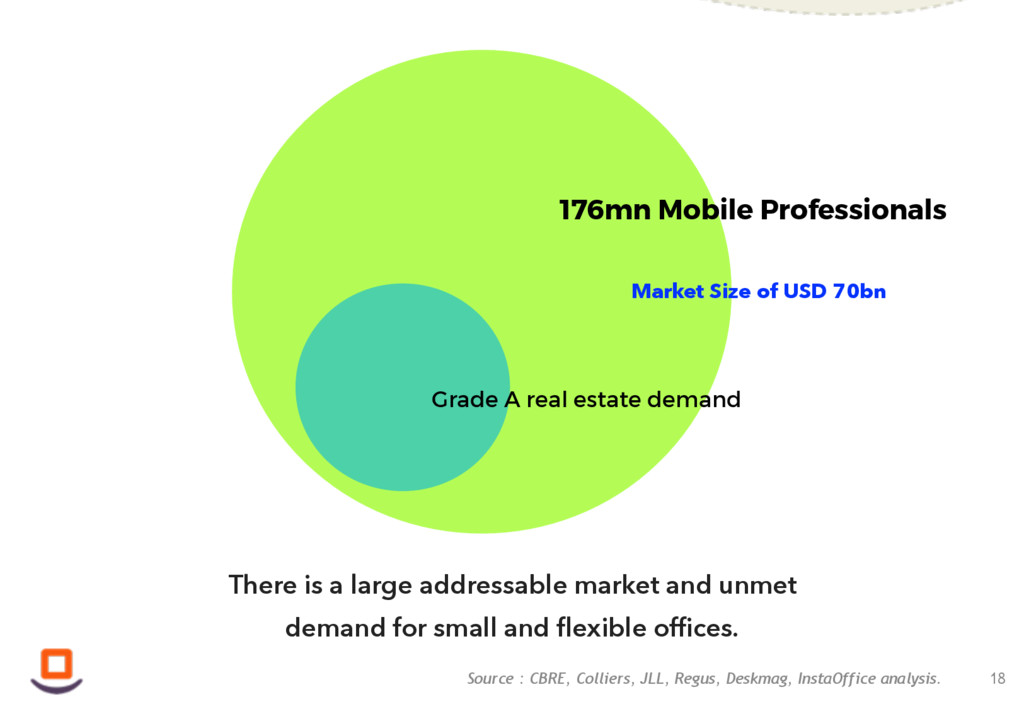

is a large addressable market and unmet demand for small and flexible offices. 18 176mn Mobile Professionals Grade A real estate demand Market Size of USD 70bn

"Process of industrial mutation that incessantly revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one" Creative Destruction Joseph Schumpeter

in office occupancy costs by over 50%... 20 Capital costs and one time office setup expenses Fit Outs Furniture and Furnishing Technology Infrastructure Deposits for Rent and CAM Commissions Rent Maintenance Charge Housekeeping and Security Receptions, Admin and IT staff Internet & Communications Insurance Utilities Basic Consumables / Beverages Repairs and Refurbishment Recurring Variable Costs Recurring Fixed Costs, irrespective of the size of the team and changing office space needs User doesn’t need to bear any Capex or Fixed Costs Reduction of over 50% in occupancy costs One single price paid on Per Seat basis (Scalable and Flexible) Conventional Lease Coworking Model

utilization of the office inventory, generating higher rental yields for the landlords. Super Area 5,000 sq. ft. 5,000 sq. ft. Rent (INR / sq. ft.) INR 55 / sq. ft. – Super Area / Desk – 65 sq. ft. Number of Desks – 76 Average Revenue per Desk – INR 14,000 Landlord’s Share 100% 30% Revenue p.m. for the Landlords INR 275,000 INR 319,200 Marketing Cost / Commissions 1 month – Average Long Term Utilization 75% 90% Annual Revenue 2,268,750 3,447,360 Annual Surplus – INR 1,178,610 Conventional Lease InstaOffice Model Higher Floor Efficiency Includes all extra services Better Monetization Increase of over 50% Methodology: InstaOffice shares Gross Revenue with the real estate partners / landlords. In other models, we take a percentage of the Gross Revenue, while Opex and Capex are borne by the landlord. 21

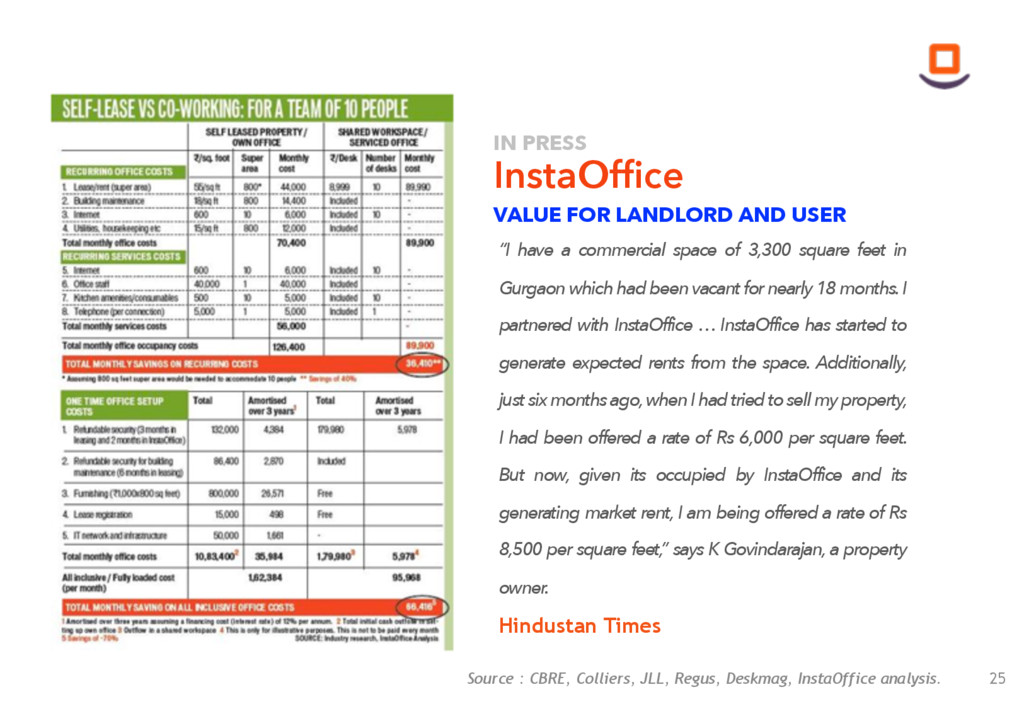

VALUE FOR LANDLORD AND USER “I have a commercial space of 3,300 square feet in Gurgaon which had been vacant for nearly 18 months. I partnered with InstaOffice … InstaOffice has started to generate expected rents from the space. Additionally, just six months ago, when I had tried to sell my property, I had been offered a rate of Rs 6,000 per square feet. But now, given its occupied by InstaOffice and its generating market rent, I am being offered a rate of Rs 8,500 per square feet,” says K Govindarajan, a property owner. Hindustan Times InstaOffice IN PRESS

Immediate Monetisation Poor rental yields Positive net absorption Long vacancy periods Communities Hierarchies Scalability Large floor plates C R E AT I N G VA L U E F O R M E M B E R & L A N D LO R D S InstaOffice Pay per use Fixed Office Spend

This presentation above may include forecasts, projections and other predictive statements that represent InstaOffice’s assumptions and expectations in light of currently available information. These forecasts, etc., are based on industry trends, circumstances involving clients and other factors, and they involve risks, variables and uncertainties. The actual performance results may differ from those projected above. Consequently, no guarantee is presented or implied as to the accuracy of specific forecasts, projections or predictive statements contained above. The information contained within this document is proprietary to InstaOffice and it reserves the right to all information provided. The recipient agrees not to distribute, share or use any part of the material without express written permission of InstaOffice. The recipient would treat this material as Confidential Information. 28

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}