Drillinginfo International's Regional Managers offered detailed overviews of Argentina, Colombia and Australia's Oil & Gas markets at our annual World Members Meeting. For more information, visit http://info.diiinfo.com/

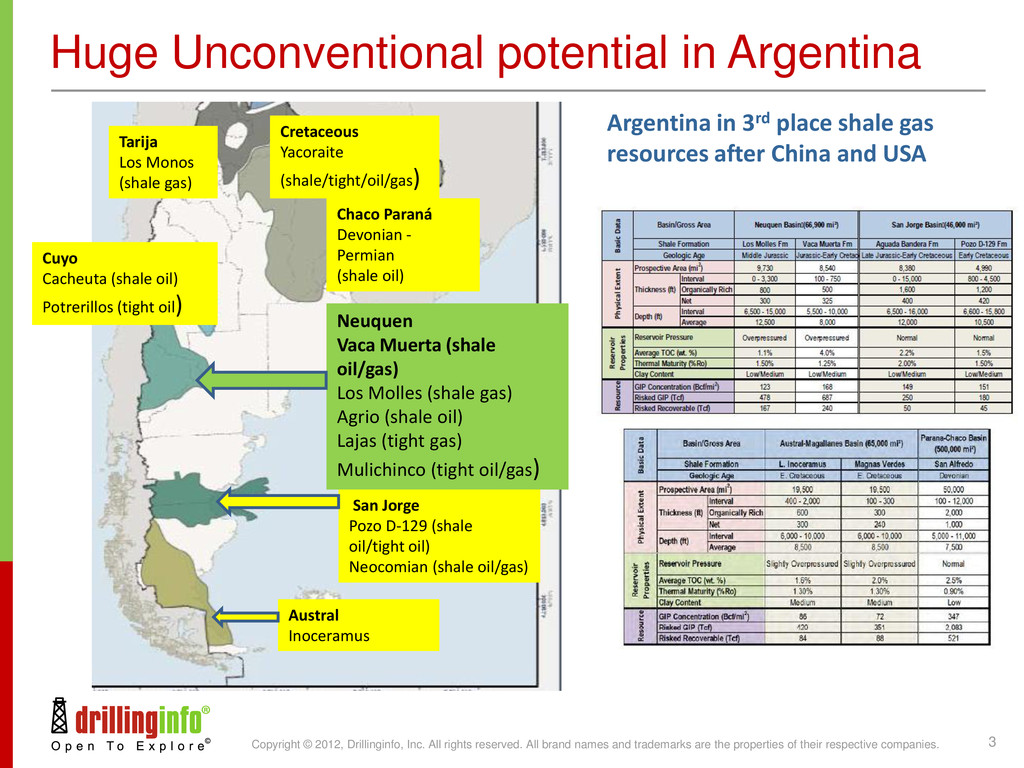

names and trademarks are the properties of their respective companies. 3 Huge Unconventional potential in Argentina Tarija Los Monos (shale gas) Cretaceous Yacoraite (shale/tight/oil/gas) Chaco Paraná Devonian - Permian (shale oil) Neuquen Vaca Muerta (shale oil/gas) Los Molles (shale gas) Agrio (shale oil) Lajas (tight gas) Mulichinco (tight oil/gas) Cuyo Cacheuta (shale oil) Potrerillos (tight oil) San Jorge Pozo D-129 (shale oil/tight oil) Neocomian (shale oil/gas) Austral Inoceramus Argentina in 3rd place shale gas resources after China and USA

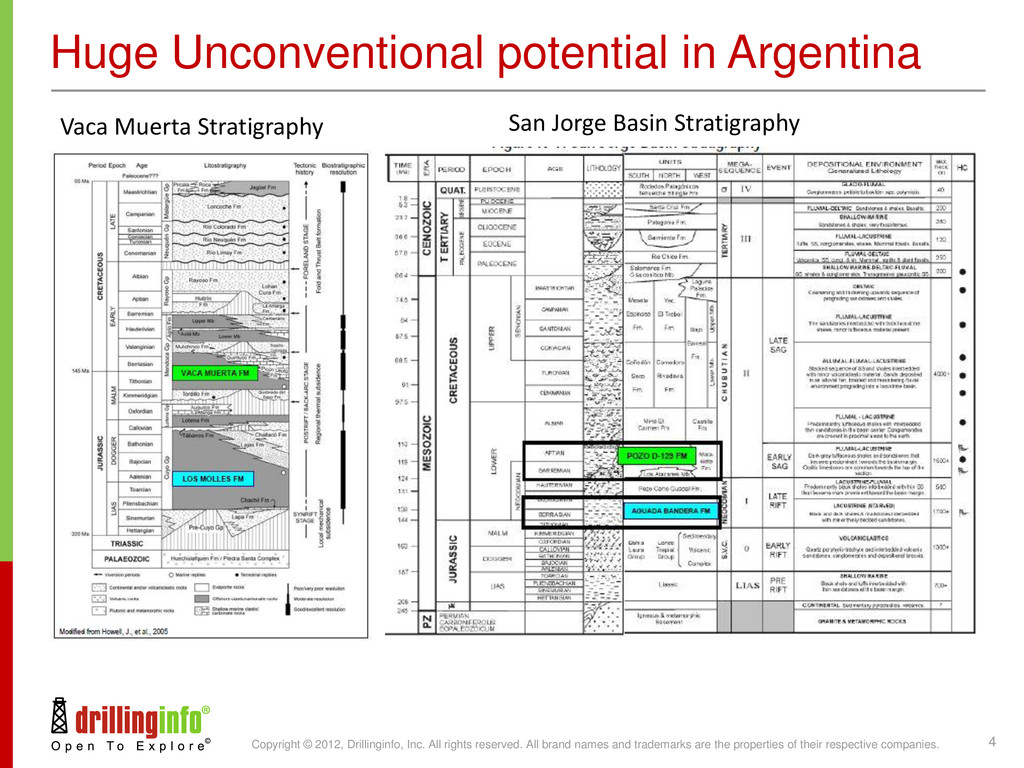

names and trademarks are the properties of their respective companies. 4 Huge Unconventional potential in Argentina Vaca Muerta Stratigraphy San Jorge Basin Stratigraphy

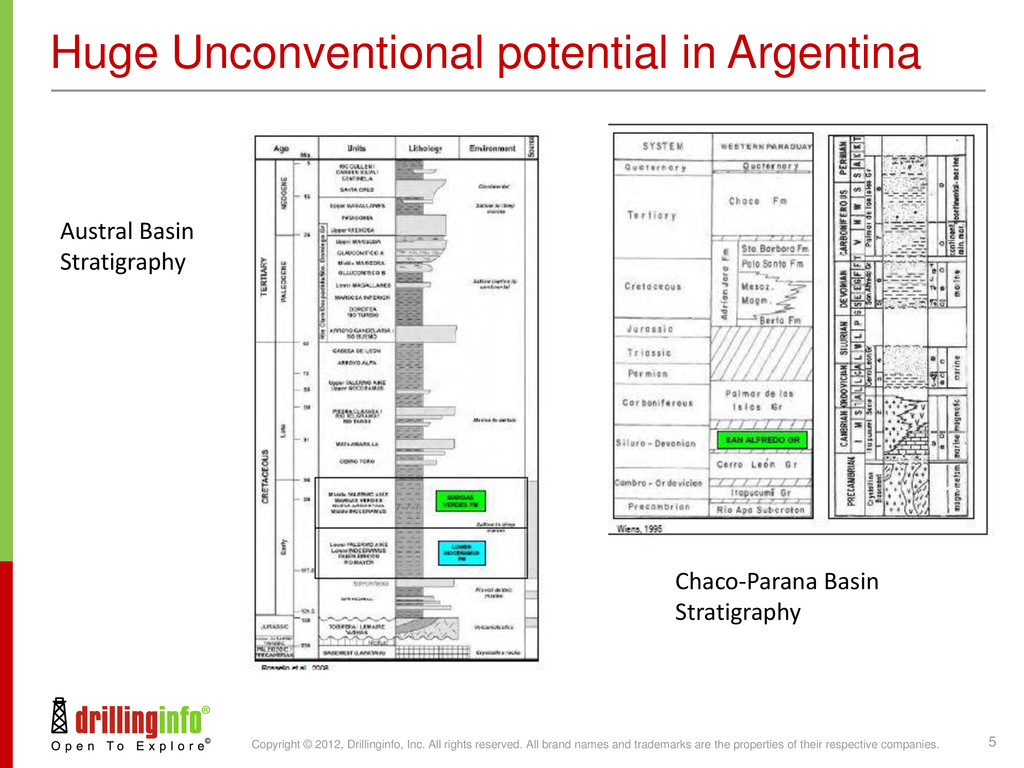

names and trademarks are the properties of their respective companies. 5 Huge Unconventional potential in Argentina Austral Basin Stratigraphy Chaco-Parana Basin Stratigraphy

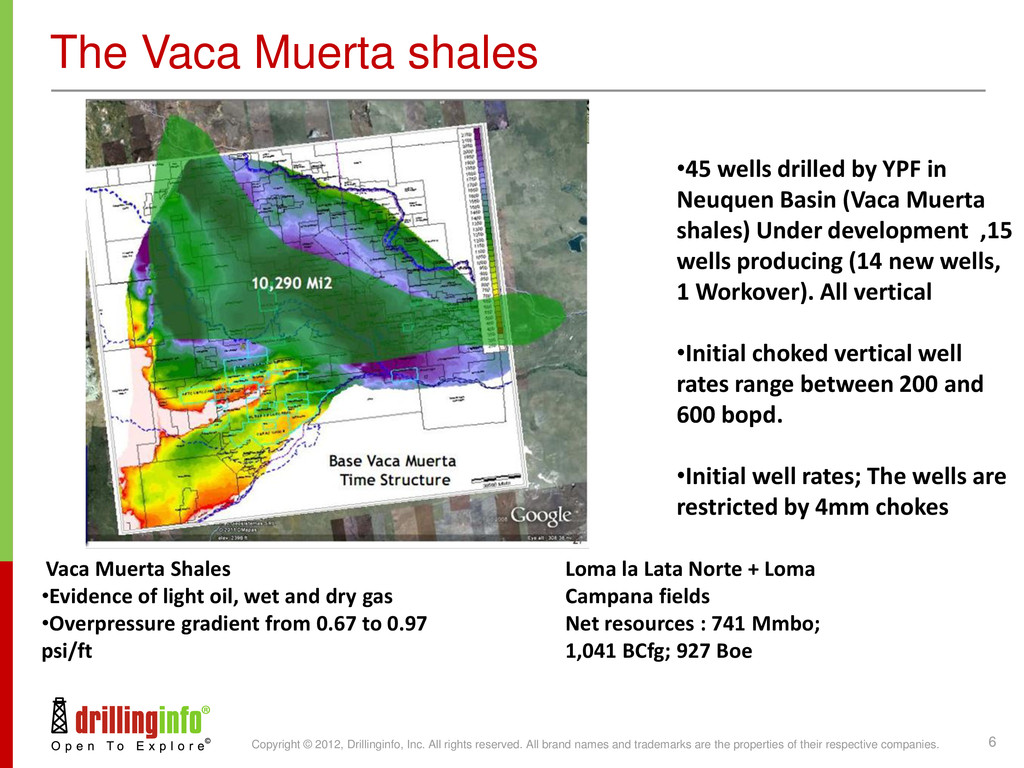

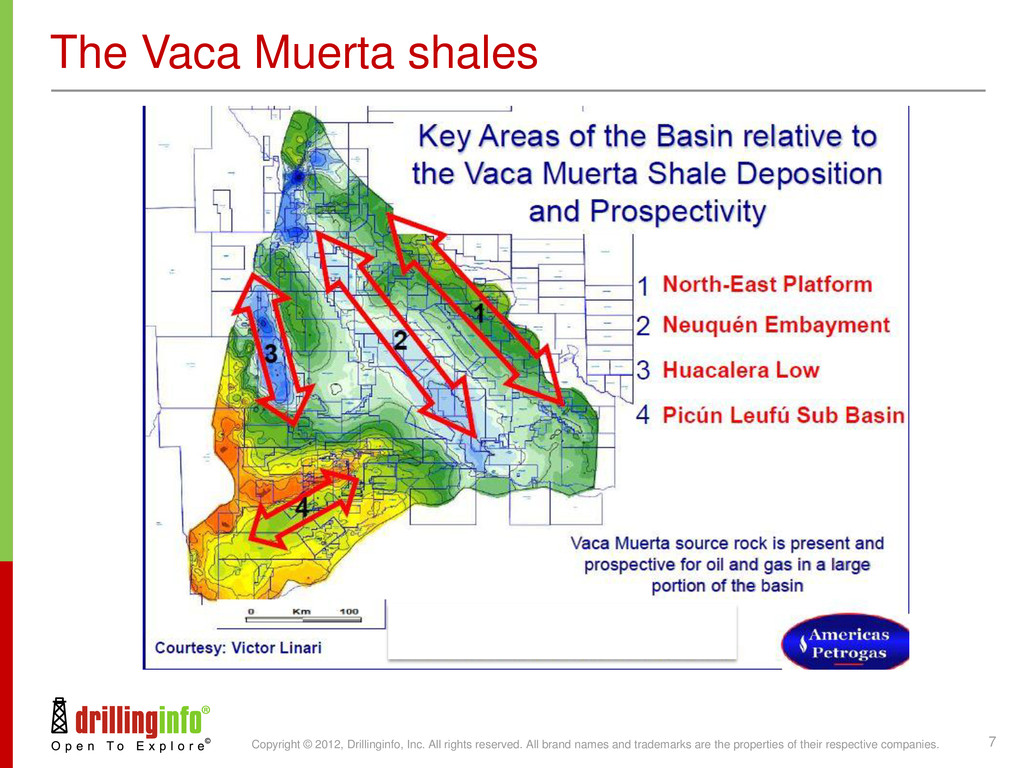

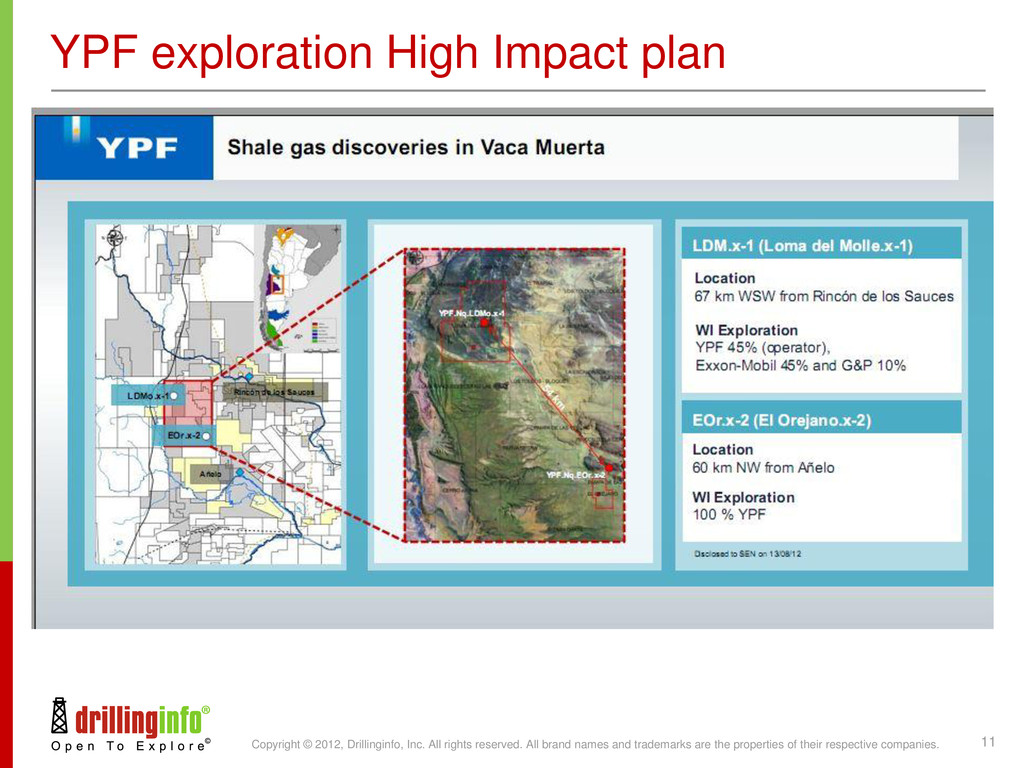

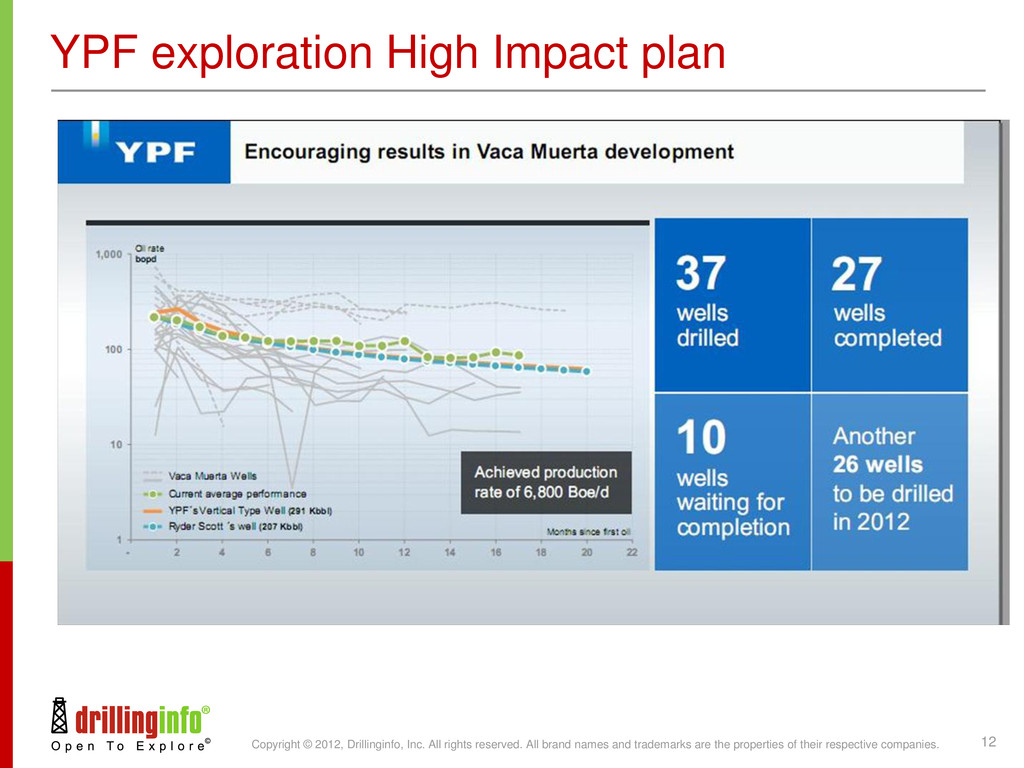

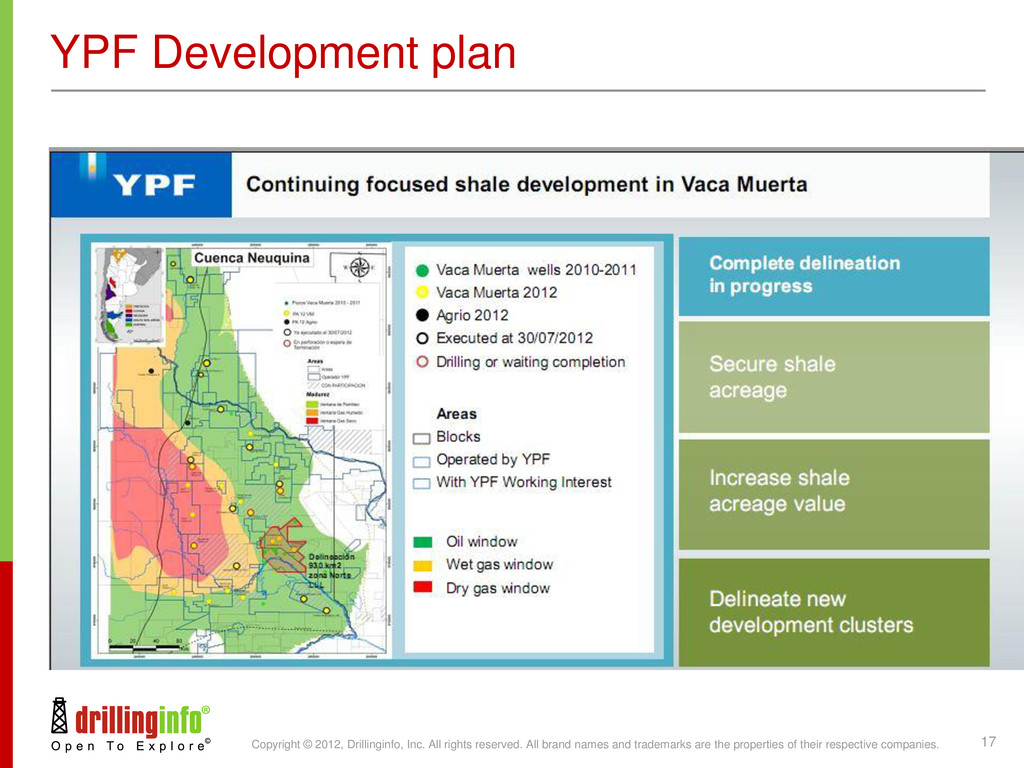

names and trademarks are the properties of their respective companies. 6 The Vaca Muerta shales Vaca Muerta Shales •Evidence of light oil, wet and dry gas •Overpressure gradient from 0.67 to 0.97 psi/ft •45 wells drilled by YPF in Neuquen Basin (Vaca Muerta shales) Under development ,15 wells producing (14 new wells, 1 Workover). All vertical •Initial choked vertical well rates range between 200 and 600 bopd. •Initial well rates; The wells are restricted by 4mm chokes Loma la Lata Norte + Loma Campana fields Net resources : 741 Mmbo; 1,041 BCfg; 927 Boe

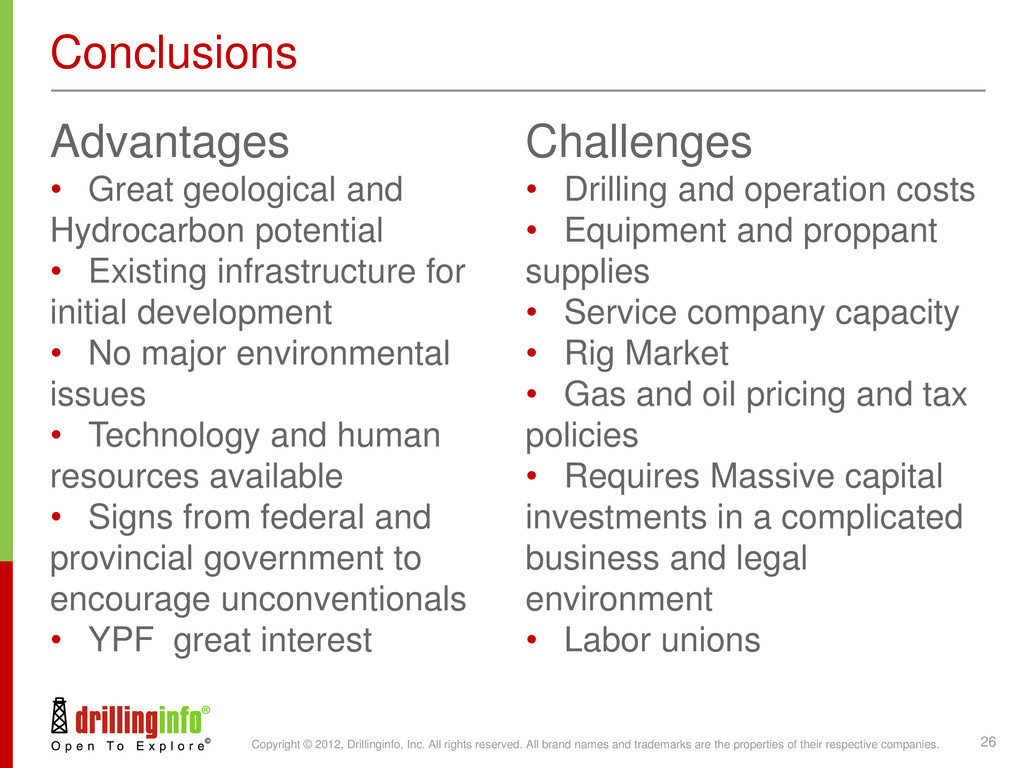

names and trademarks are the properties of their respective companies. 26 Conclusions Advantages • Great geological and Hydrocarbon potential • Existing infrastructure for initial development • No major environmental issues • Technology and human resources available • Signs from federal and provincial government to encourage unconventionals • YPF great interest Challenges • Drilling and operation costs • Equipment and proppant supplies • Service company capacity • Rig Market • Gas and oil pricing and tax policies • Requires Massive capital investments in a complicated business and legal environment • Labor unions

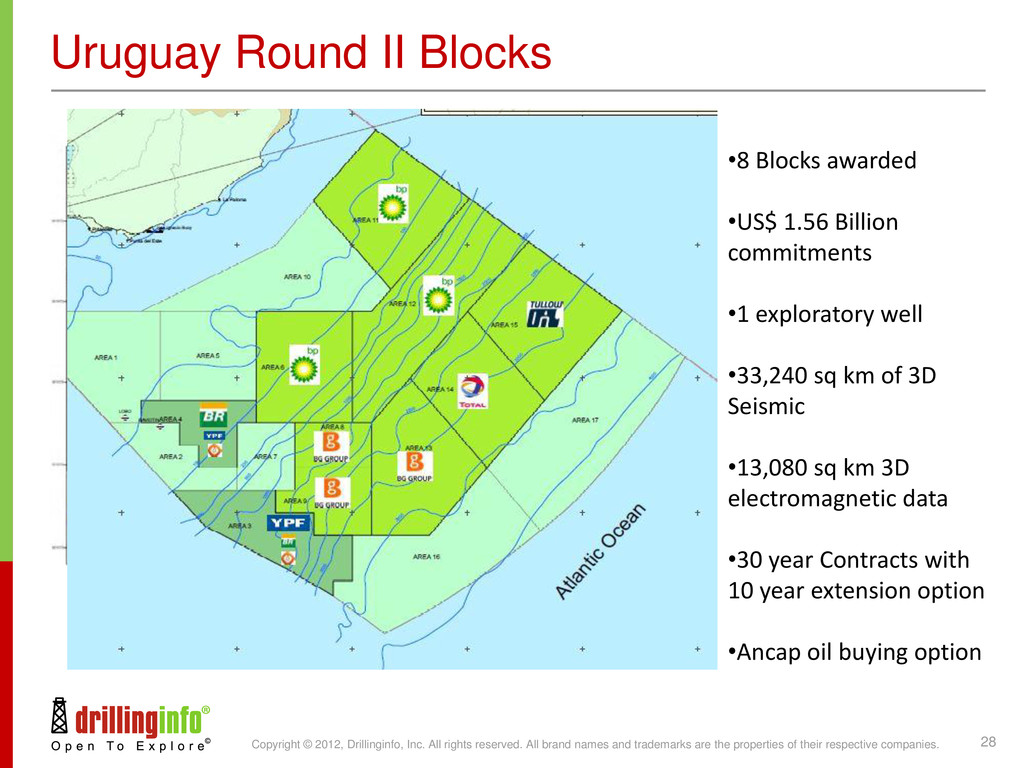

names and trademarks are the properties of their respective companies. 28 Uruguay Round II Blocks •8 Blocks awarded •US$ 1.56 Billion commitments •1 exploratory well •33,240 sq km of 3D Seismic •13,080 sq km 3D electromagnetic data •30 year Contracts with 10 year extension option •Ancap oil buying option

names and trademarks are the properties of their respective companies. 31 After a remarkable turnaround . . . Photo: Claudio Bartolini . . . where is Colombia headed next?

names and trademarks are the properties of their respective companies. 32 2003: A Nearly Perfect Storm President Alvaro Uribe vows to make Colombia safe, saying, ‘without peace there is no investment.’ Rapidly declining oil production spurs Colombia to follow Brazilian model. ANH created to regulate industry. Association Contracts with mandatory Ecopetrol participation replaced by E&P Contracts. Incentives implemented for licensing. State oil company Ecopetrol becomes an E&P company, free to explore in Colombia and elsewhere.

names and trademarks are the properties of their respective companies. 33 The Good, the Bad, the Ugly Peru: Initiates similar incentives Brazil: Despite opening to IOCs in 1996, Petrobras continues to dominate exploration and licensing Argentina: mandates commodity price controls in wake of 2001-2002 currency collapse Venezuela: Under President Hugo Chavez, exploration nearly grinds to a halt. His dismantling of PDVSA leaves thousands of seasoned South American explorers looking for work Ecuador and Bolivia: Chavez’s Bolivarian Revolution spreads

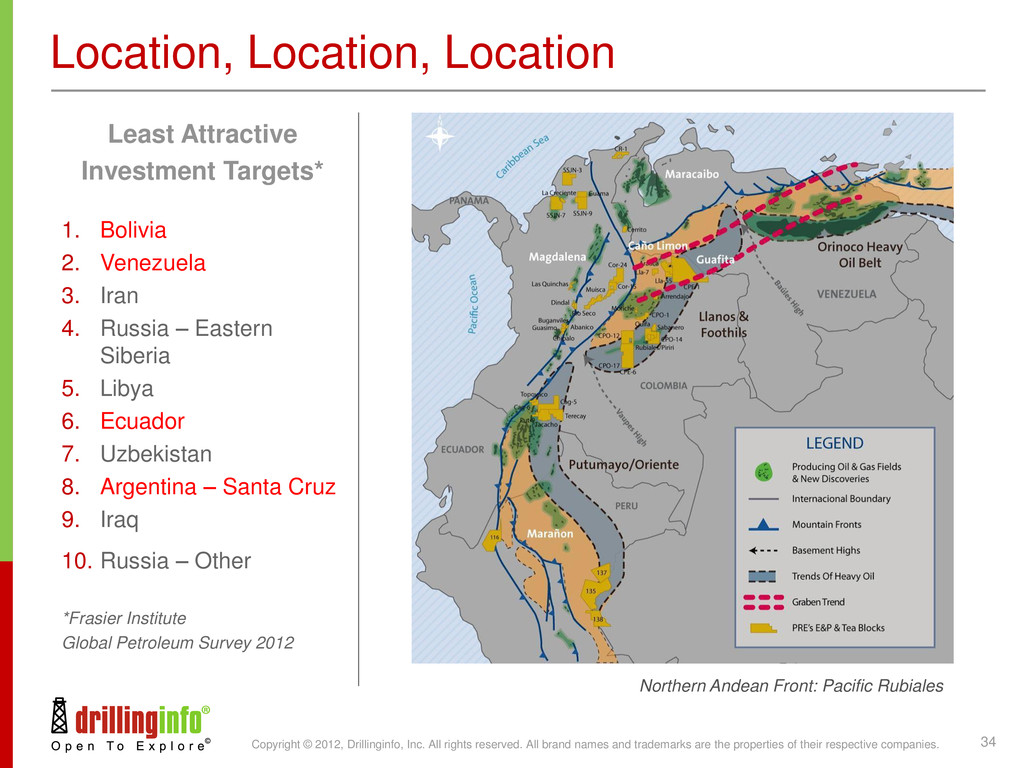

names and trademarks are the properties of their respective companies. 34 Location, Location, Location Least Attractive Investment Targets* 1. Bolivia 2. Venezuela 3. Iran 4. Russia – Eastern Siberia 5. Libya 6. Ecuador 7. Uzbekistan 8. Argentina – Santa Cruz 9. Iraq 10. Russia – Other *Frasier Institute Global Petroleum Survey 2012 Northern Andean Front: Pacific Rubiales

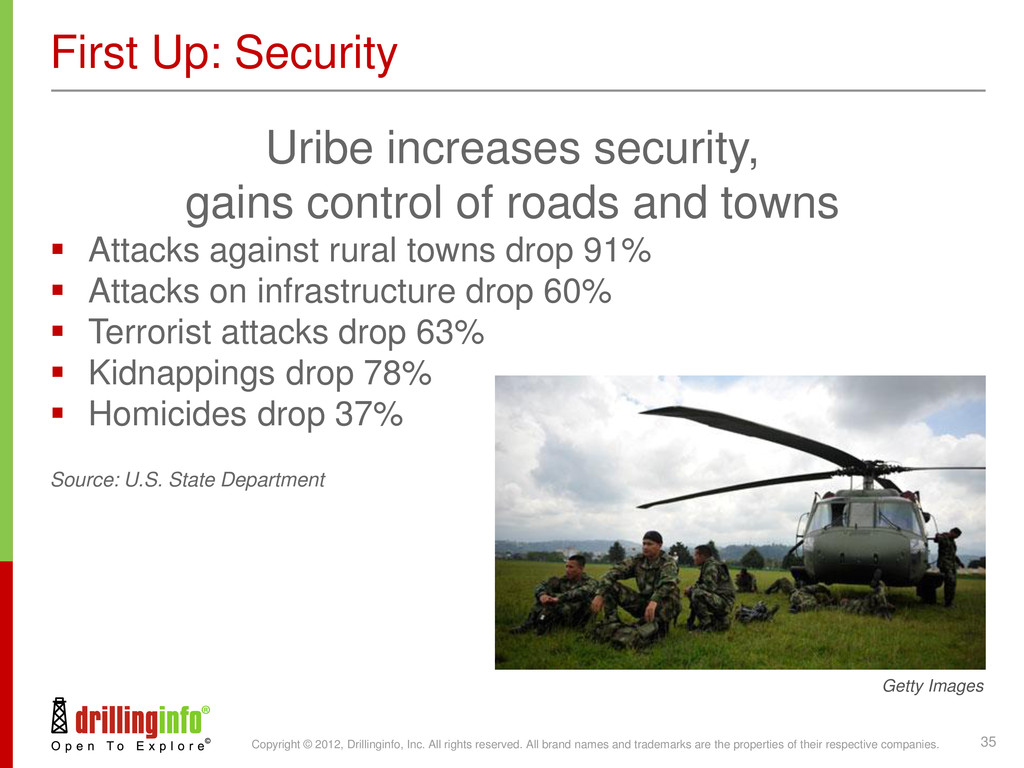

names and trademarks are the properties of their respective companies. 35 First Up: Security Uribe increases security, gains control of roads and towns Attacks against rural towns drop 91% Attacks on infrastructure drop 60% Terrorist attacks drop 63% Kidnappings drop 78% Homicides drop 37% Source: U.S. State Department Getty Images

names and trademarks are the properties of their respective companies. 36 Second Up: Investment The National Hydrocarbons Agency is created by Decree-law 1760 on June 16, 2003, as a special administrative unit within Colombia’s Mines and Energy Ministry.

names and trademarks are the properties of their respective companies. 37 Sanctity of Contracts ANH offers first-come, first-serve licenses and then in 2007 adds bid rounds or ‘rondas’ 6-year exploration & production contracts 18-24-month technical evaluation agreements Royalty rate reduced from fixed 20% to sliding scale of 5-25% Government’s take on profits flexible and competitive No signature or discovery bonuses Depreciation period reduced from 10 to 5 years Colombia takes pride in its history of never breaking a contract

names and trademarks are the properties of their respective companies. 38 Number of New Contracts Soar As of July 9, 2012, 255 Active, 14 Suspended Contracts Source: 0 10 20 30 40 50 60 70 80 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 TEA E&P AC

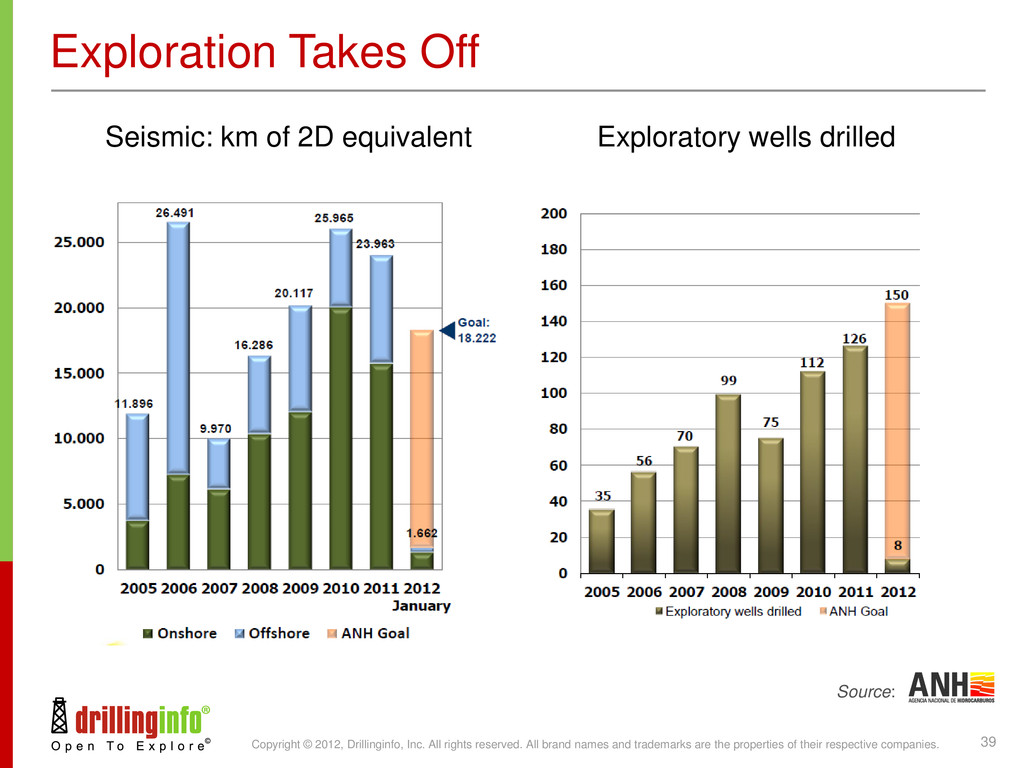

names and trademarks are the properties of their respective companies. 39 Exploration Takes Off Seismic: km of 2D equivalent Exploratory wells drilled Source:

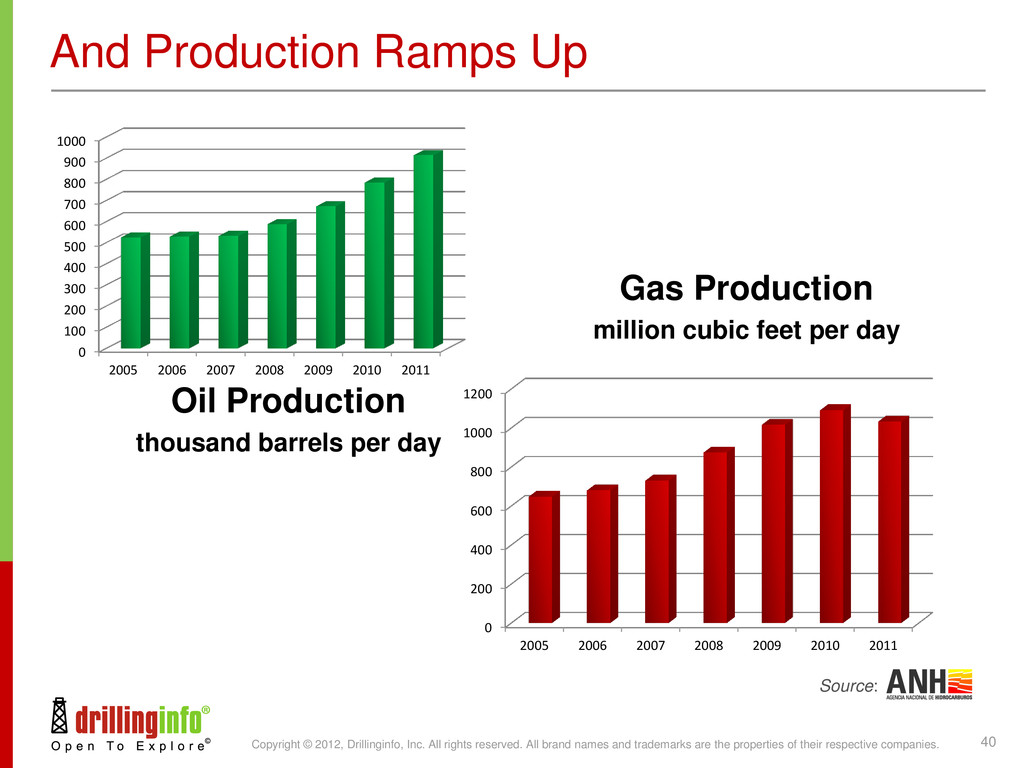

names and trademarks are the properties of their respective companies. 40 And Production Ramps Up Oil Production thousand barrels per day Gas Production million cubic feet per day Source:: 0 100 200 300 400 500 600 700 800 900 1000 2005 2006 2007 2008 2009 2010 2011 0 200 400 600 800 1000 1200 2005 2006 2007 2008 2009 2010 2011

names and trademarks are the properties of their respective companies. 41 New Explorers Arrive Connection Often based in Calgary Traded on the Toronto Stock Exchange Some staffed by ex-PDVSA management The Canadian/Venezuelan Connection

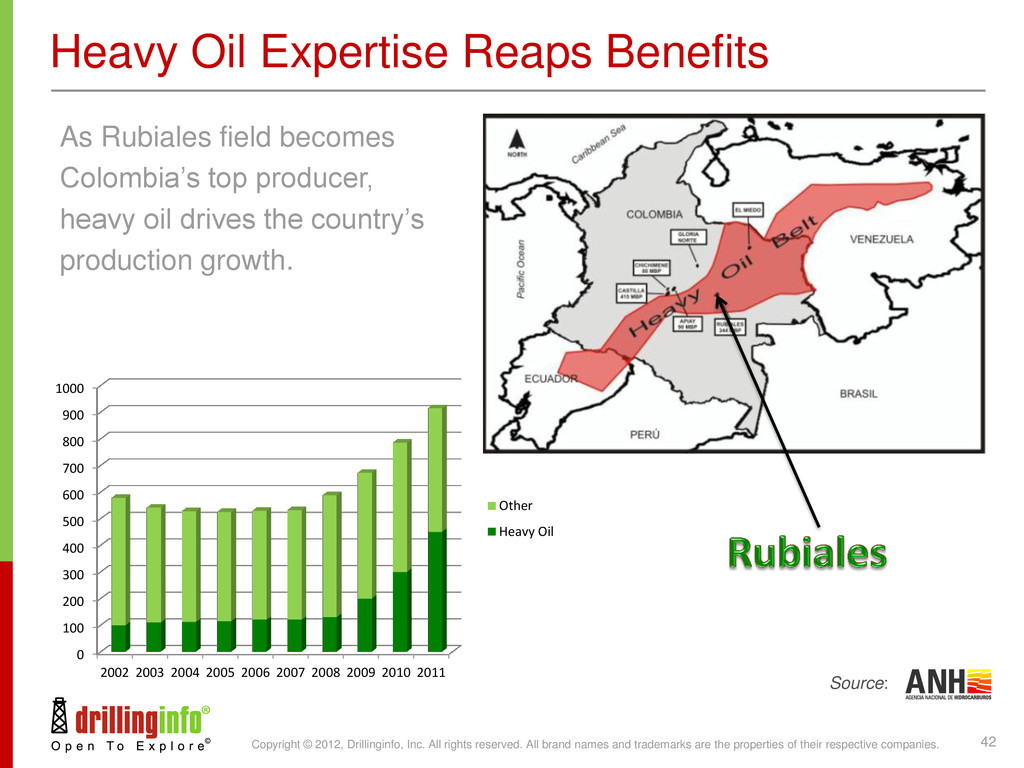

names and trademarks are the properties of their respective companies. 42 Heavy Oil Expertise Reaps Benefits As Rubiales field becomes Colombia’s top producer, heavy oil drives the country’s production growth. Source: 0 100 200 300 400 500 600 700 800 900 1000 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Other Heavy Oil

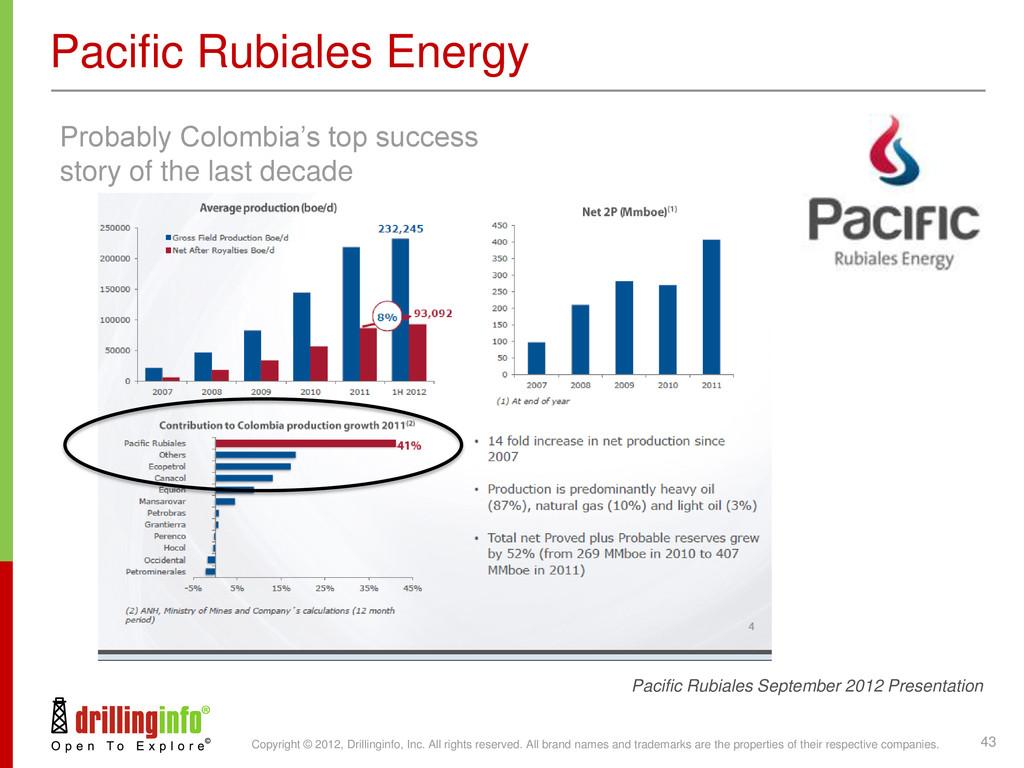

names and trademarks are the properties of their respective companies. 43 Pacific Rubiales Energy Probably Colombia’s top success story of the last decade Pacific Rubiales September 2012 Presentation

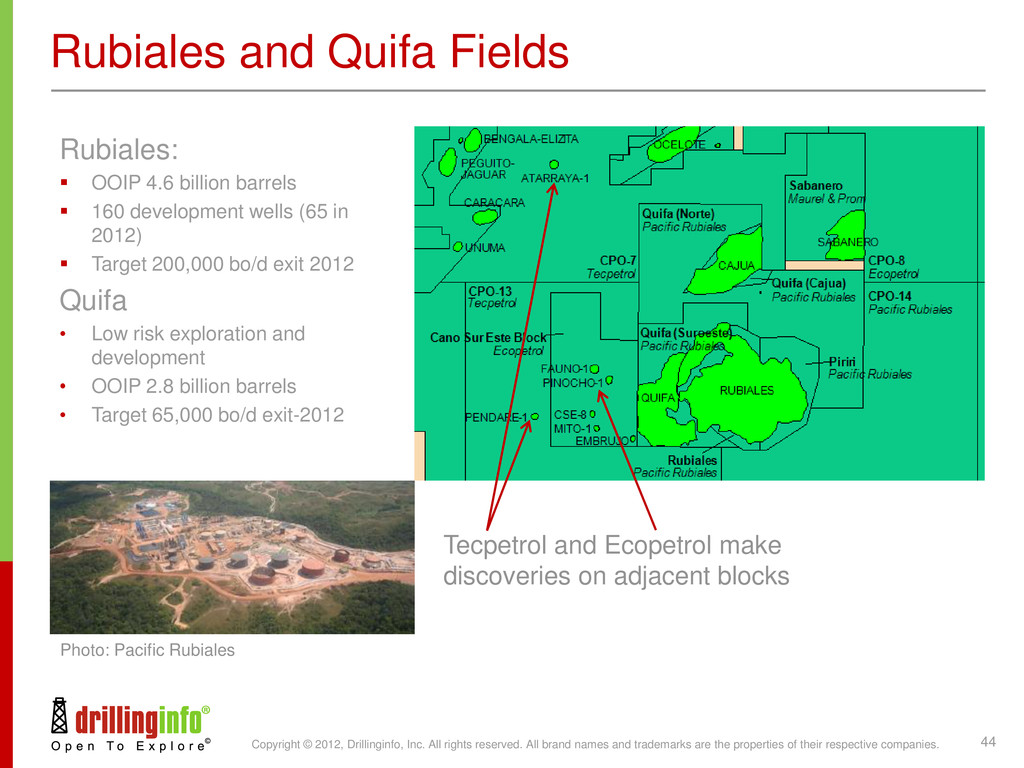

names and trademarks are the properties of their respective companies. 44 Rubiales and Quifa Fields Rubiales: OOIP 4.6 billion barrels 160 development wells (65 in 2012) Target 200,000 bo/d exit 2012 Quifa • Low risk exploration and development • OOIP 2.8 billion barrels • Target 65,000 bo/d exit-2012 Tecpetrol and Ecopetrol make discoveries on adjacent blocks Photo: Pacific Rubiales

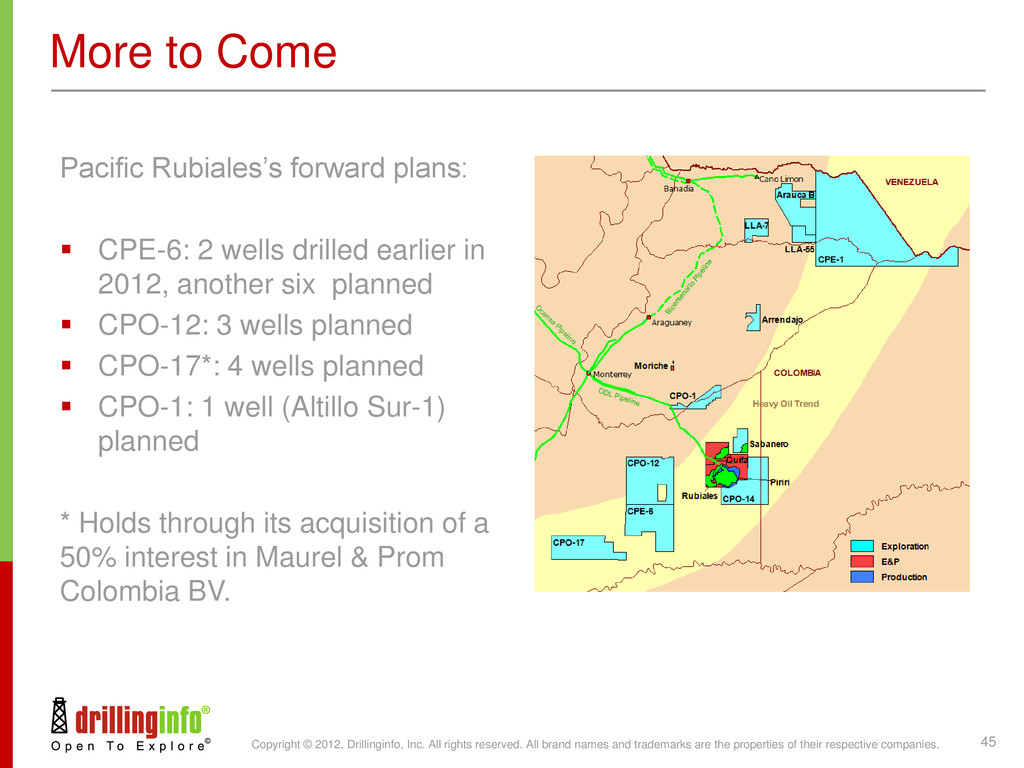

names and trademarks are the properties of their respective companies. 45 More to Come Pacific Rubiales’s forward plans: CPE-6: 2 wells drilled earlier in 2012, another six planned CPO-12: 3 wells planned CPO-17*: 4 wells planned CPO-1: 1 well (Altillo Sur-1) planned * Holds through its acquisition of a 50% interest in Maurel & Prom Colombia BV.

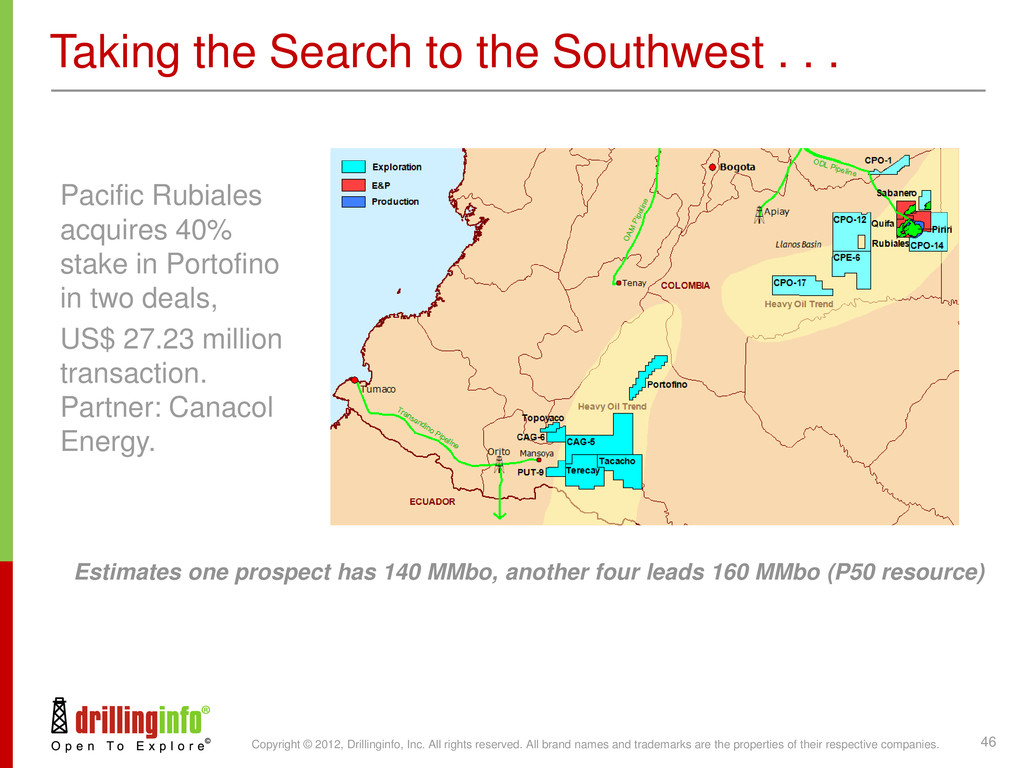

names and trademarks are the properties of their respective companies. 46 Taking the Search to the Southwest . . . Pacific Rubiales acquires 40% stake in Portofino in two deals, US$ 27.23 million transaction. Partner: Canacol Energy. Estimates one prospect has 140 MMbo, another four leads 160 MMbo (P50 resource)

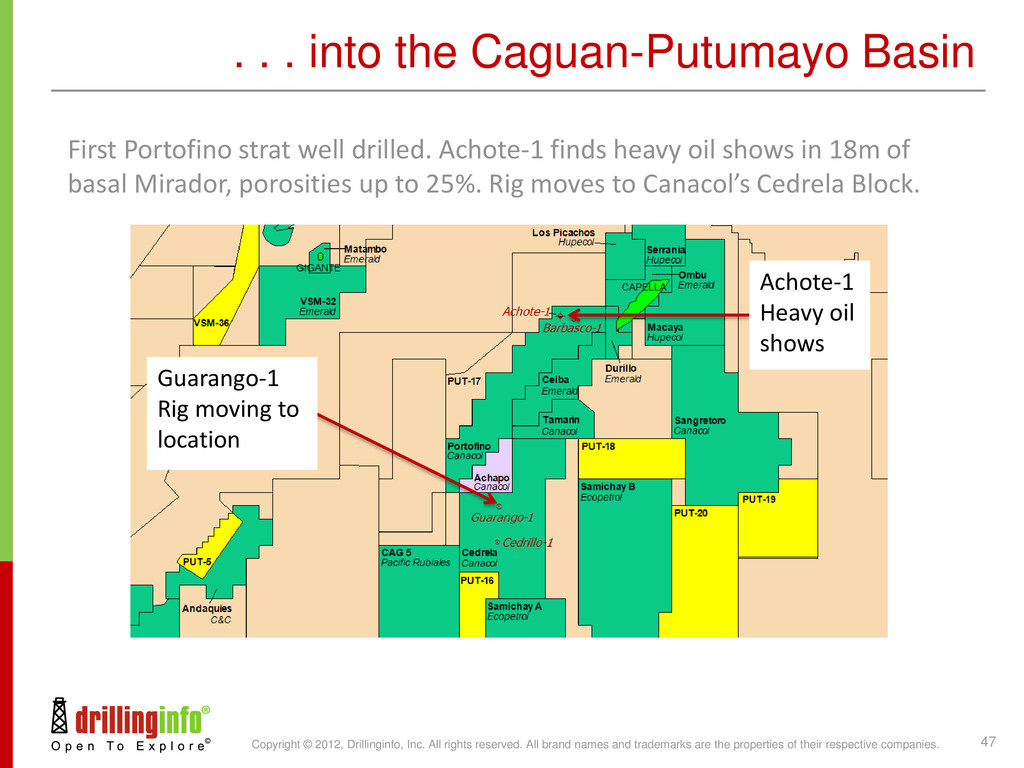

names and trademarks are the properties of their respective companies. 47 . . . into the Caguan-Putumayo Basin First Portofino strat well drilled. Achote-1 finds heavy oil shows in 18m of basal Mirador, porosities up to 25%. Rig moves to Canacol’s Cedrela Block. Achote-1 Heavy oil shows Guarango-1 Rig moving to location

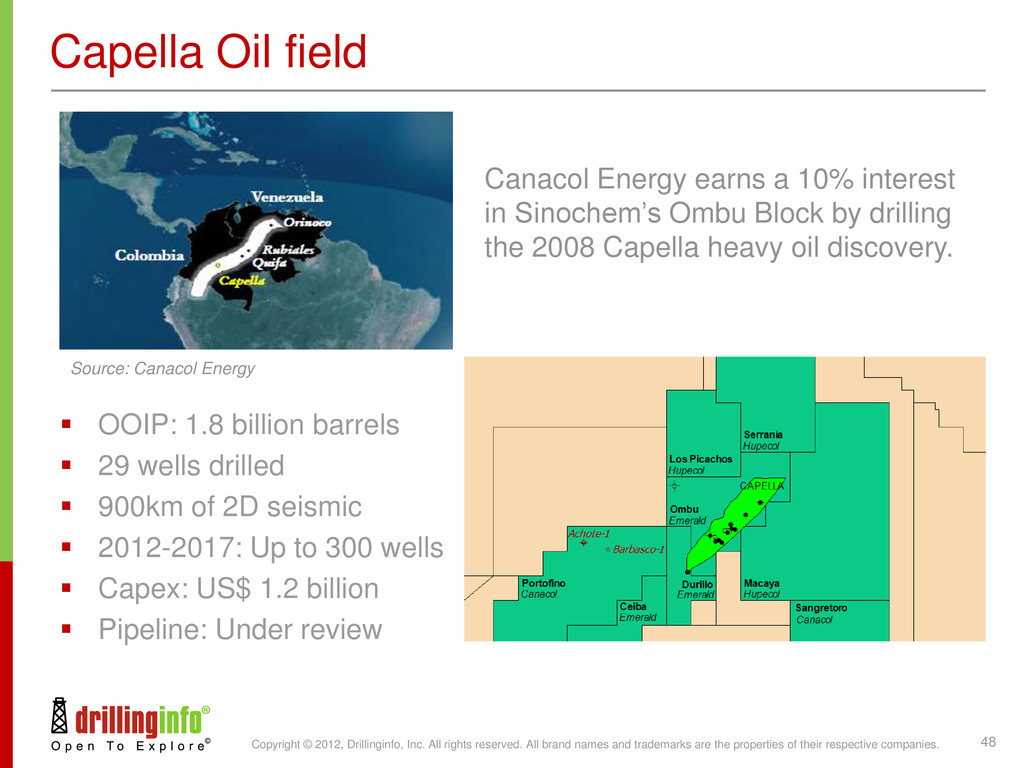

names and trademarks are the properties of their respective companies. 48 Capella Oil field OOIP: 1.8 billion barrels 29 wells drilled 900km of 2D seismic 2012-2017: Up to 300 wells Capex: US$ 1.2 billion Pipeline: Under review Canacol Energy earns a 10% interest in Sinochem’s Ombu Block by drilling the 2008 Capella heavy oil discovery. Source: Canacol Energy

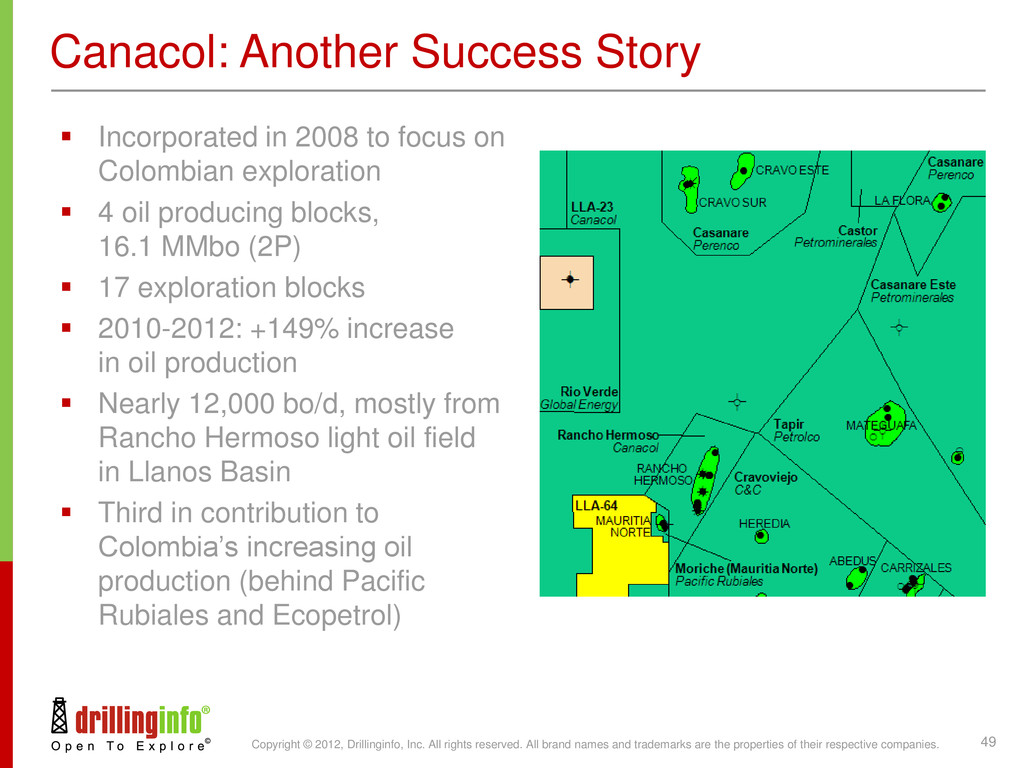

names and trademarks are the properties of their respective companies. 49 Canacol: Another Success Story Incorporated in 2008 to focus on Colombian exploration 4 oil producing blocks, 16.1 MMbo (2P) 17 exploration blocks 2010-2012: +149% increase in oil production Nearly 12,000 bo/d, mostly from Rancho Hermoso light oil field in Llanos Basin Third in contribution to Colombia’s increasing oil production (behind Pacific Rubiales and Ecopetrol)

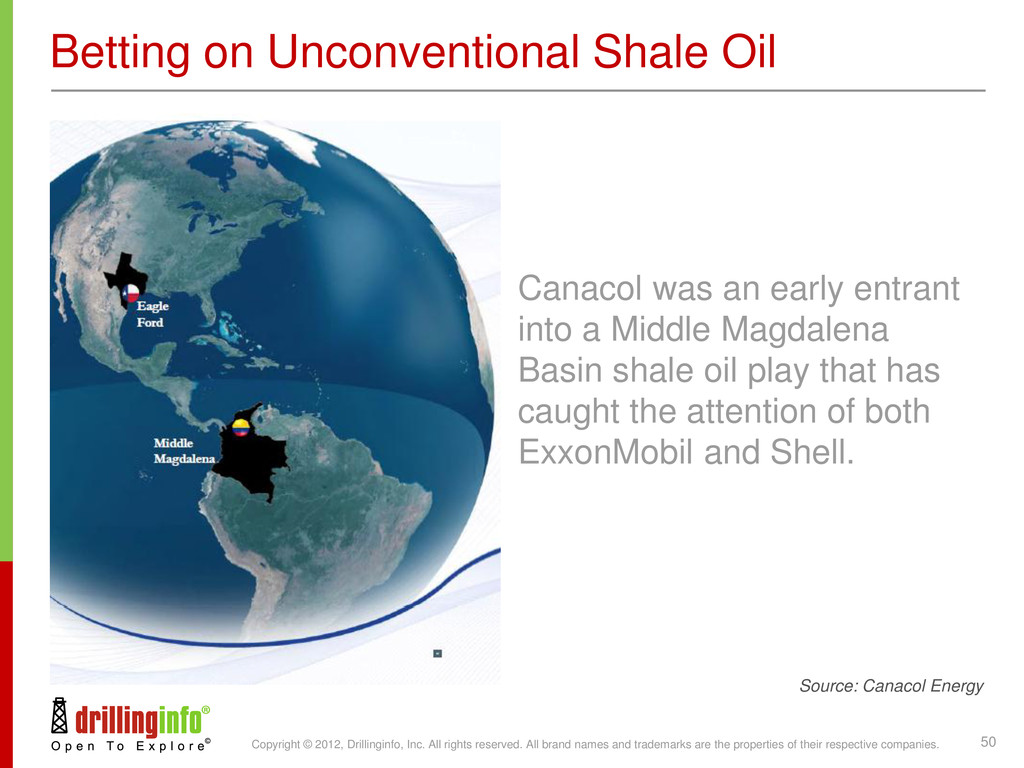

names and trademarks are the properties of their respective companies. 50 Betting on Unconventional Shale Oil Canacol was an early entrant into a Middle Magdalena Basin shale oil play that has caught the attention of both ExxonMobil and Shell. Source: Canacol Energy

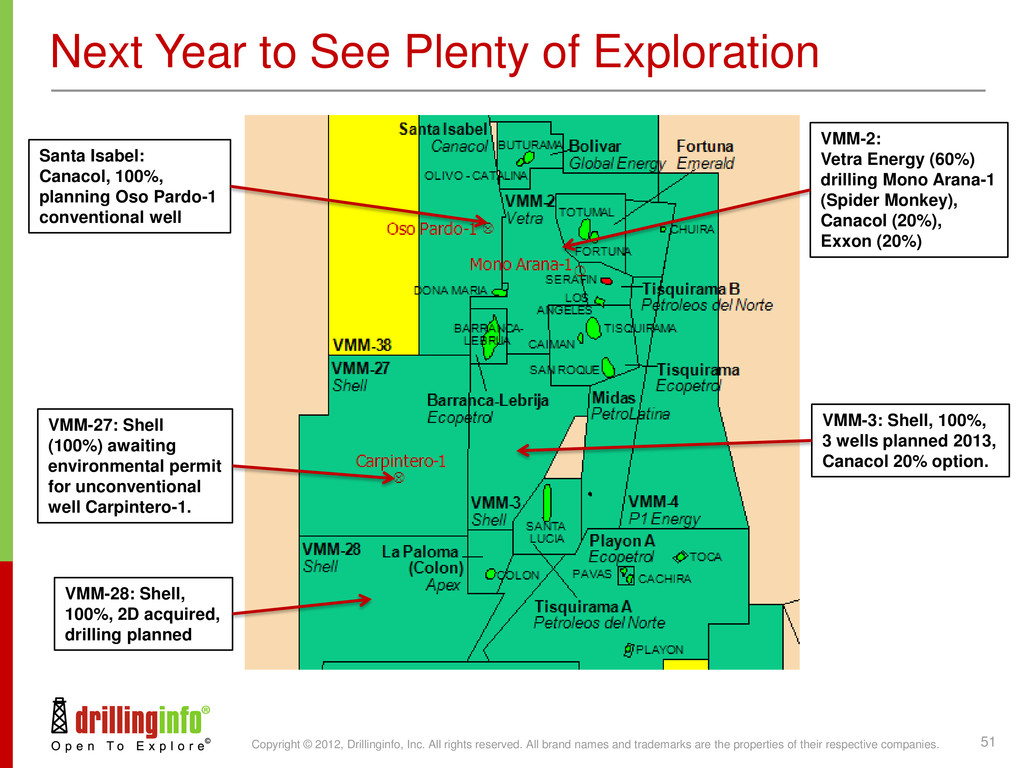

names and trademarks are the properties of their respective companies. 51 Next Year to See Plenty of Exploration VMM-2: Vetra Energy (60%) drilling Mono Arana-1 (Spider Monkey), Canacol (20%), Exxon (20%) Santa Isabel: Canacol, 100%, planning Oso Pardo-1 conventional well VMM-3: Shell, 100%, 3 wells planned 2013, Canacol 20% option. VMM-28: Shell, 100%, 2D acquired, drilling planned VMM-27: Shell (100%) awaiting environmental permit for unconventional well Carpintero-1.

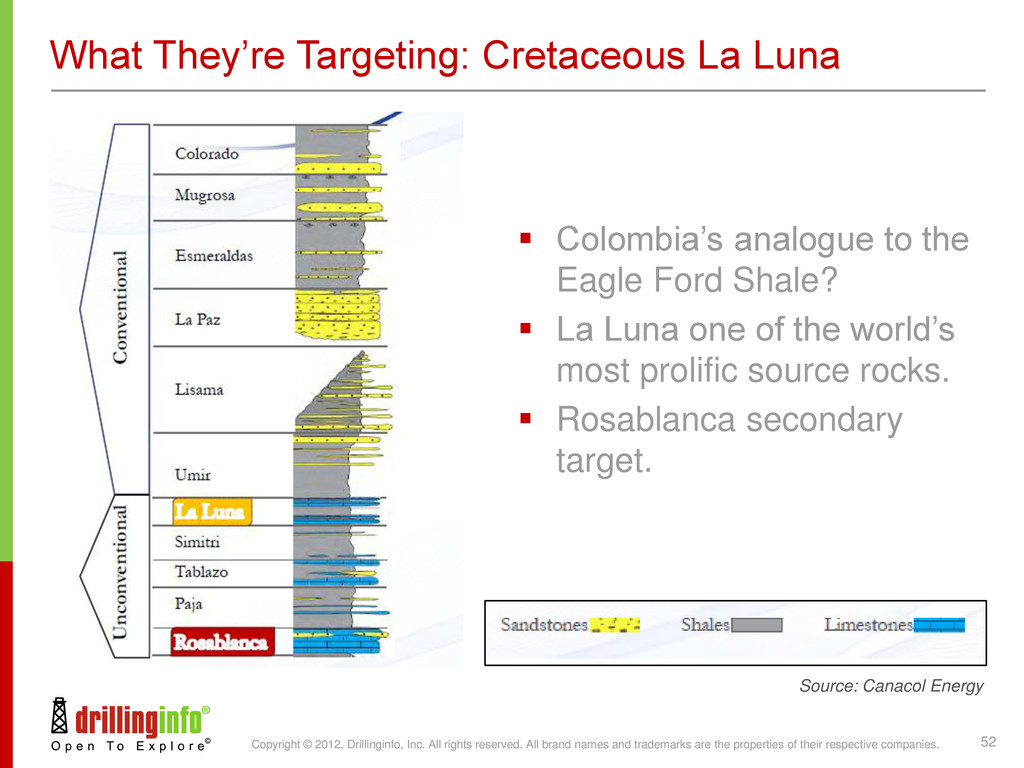

names and trademarks are the properties of their respective companies. 52 What They’re Targeting: Cretaceous La Luna Colombia’s analogue to the Eagle Ford Shale? La Luna one of the world’s most prolific source rocks. Rosablanca secondary target. Source: Canacol Energy

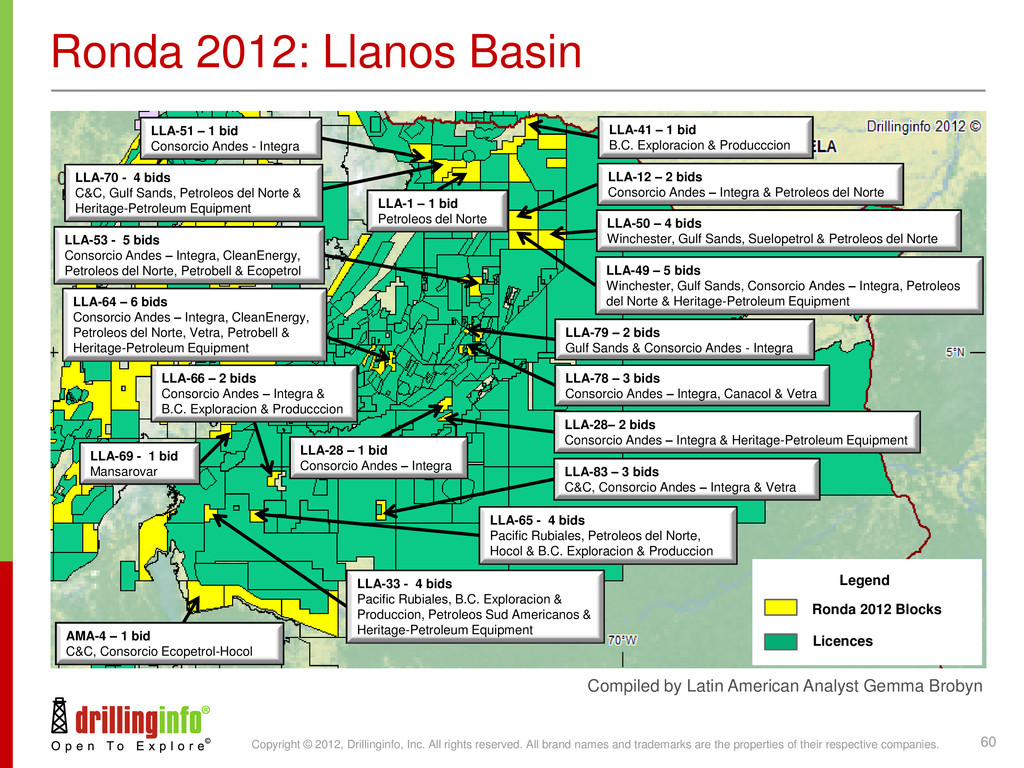

names and trademarks are the properties of their respective companies. 53 Why unconventionals in Colombia? Colombia once again striving to be ahead of the curve 31 blocks in Ronda 2012 with potential for unconventionals Offers special terms for unconventional exploration – a first outside the U.S. 40% discount on royalties New windfall profits tax: US$ 81 Longer license terms Other operators targeting unconventionals in other basins Nexen in Eastern Cordillera, gas in the Cretaceous Chipaque, Une and Tibasosa/Fomeque shales Azabache Energy, Lower Magdalena Basin, gas in Porquero and Cienaga de Oro Pacific Rubiales successfully fractures two unconventional gas wells in the Lower Magdalena Basin

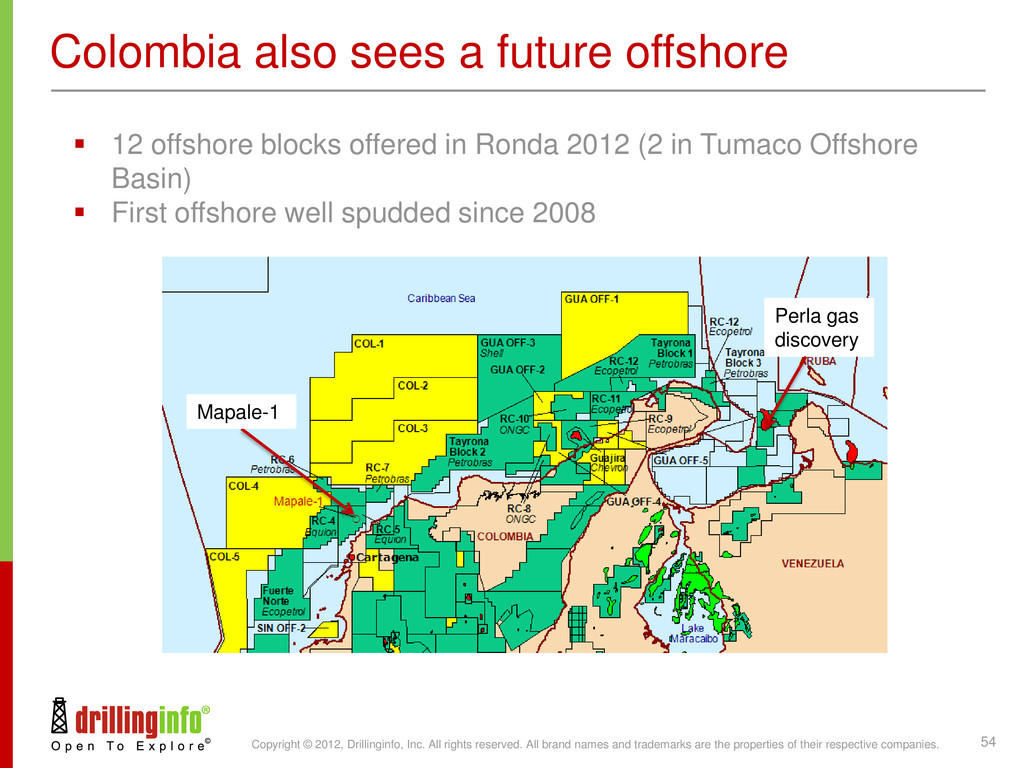

names and trademarks are the properties of their respective companies. 54 Colombia also sees a future offshore 12 offshore blocks offered in Ronda 2012 (2 in Tumaco Offshore Basin) First offshore well spudded since 2008 Perla gas discovery Mapale-1

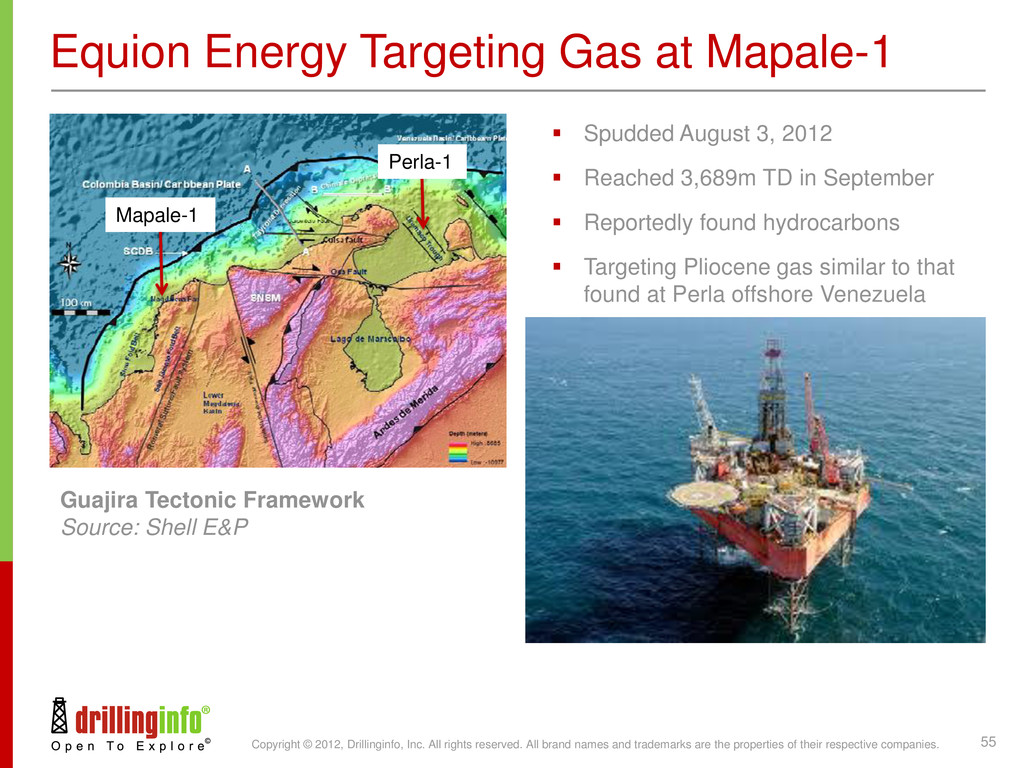

names and trademarks are the properties of their respective companies. 55 Equion Energy Targeting Gas at Mapale-1 Spudded August 3, 2012 Reached 3,689m TD in September Reportedly found hydrocarbons Targeting Pliocene gas similar to that found at Perla offshore Venezuela Guajira Tectonic Framework Source: Shell E&P Mapale-1 Perla-1

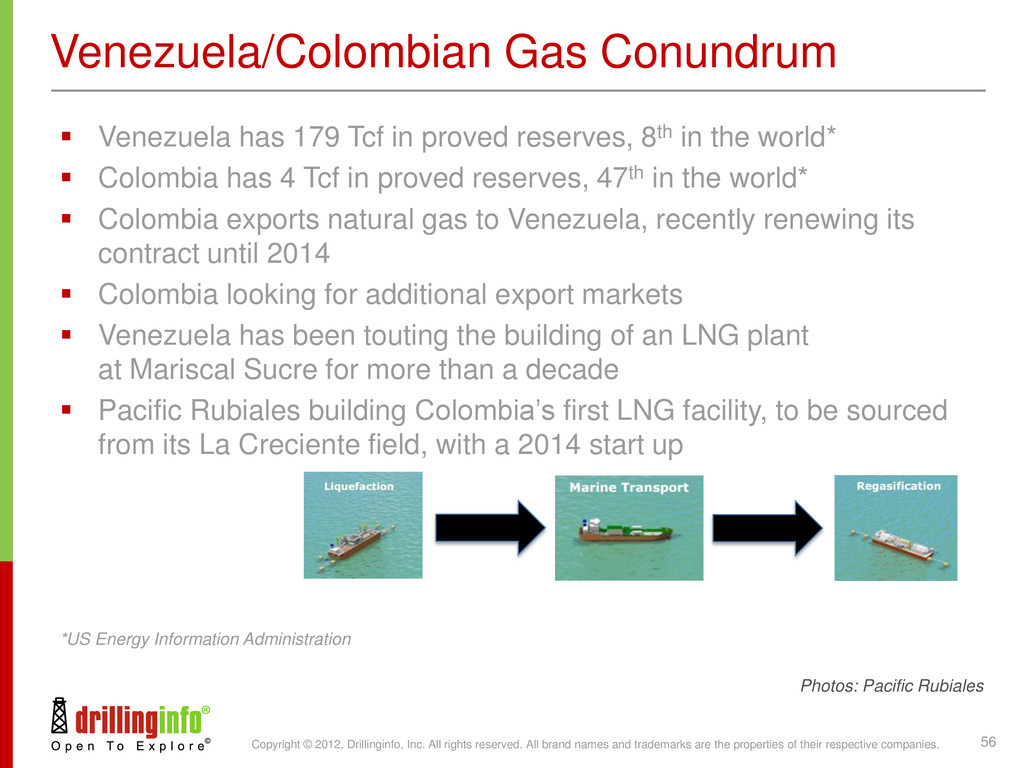

names and trademarks are the properties of their respective companies. 56 Venezuela/Colombian Gas Conundrum Venezuela has 179 Tcf in proved reserves, 8th in the world* Colombia has 4 Tcf in proved reserves, 47th in the world* Colombia exports natural gas to Venezuela, recently renewing its contract until 2014 Colombia looking for additional export markets Venezuela has been touting the building of an LNG plant at Mariscal Sucre for more than a decade Pacific Rubiales building Colombia’s first LNG facility, to be sourced from its La Creciente field, with a 2014 start up *US Energy Information Administration Photos: Pacific Rubiales

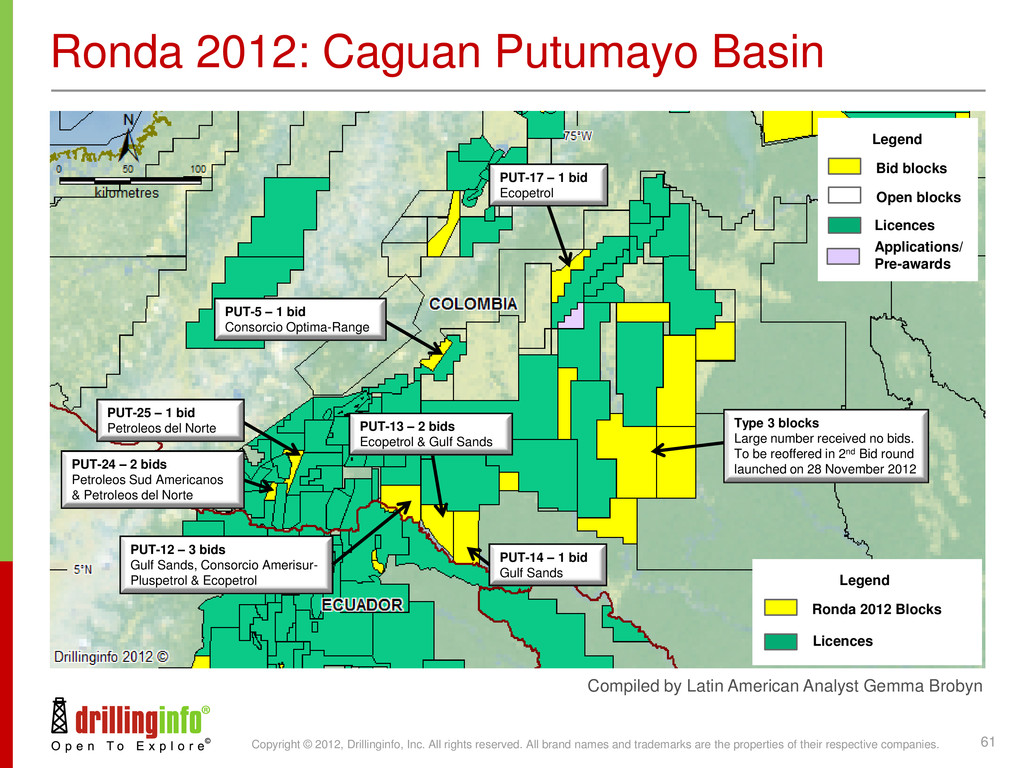

names and trademarks are the properties of their respective companies. 61 Ronda 2012: Caguan Putumayo Basin Compiled by Latin American Analyst Gemma Brobyn Legend Bid blocks Licences Applications/ Pre-awards Open blocks PUT-5 – 1 bid Consorcio Optima-Range PUT-25 – 1 bid Petroleos del Norte PUT-24 – 2 bids Petroleos Sud Americanos & Petroleos del Norte PUT-12 – 3 bids Gulf Sands, Consorcio Amerisur- Pluspetrol & Ecopetrol PUT-13 – 2 bids Ecopetrol & Gulf Sands PUT-14 – 1 bid Gulf Sands PUT-17 – 1 bid Ecopetrol Type 3 blocks Large number received no bids. To be reoffered in 2nd Bid round launched on 28 November 2012 Legend Ronda 2012 Blocks Licences

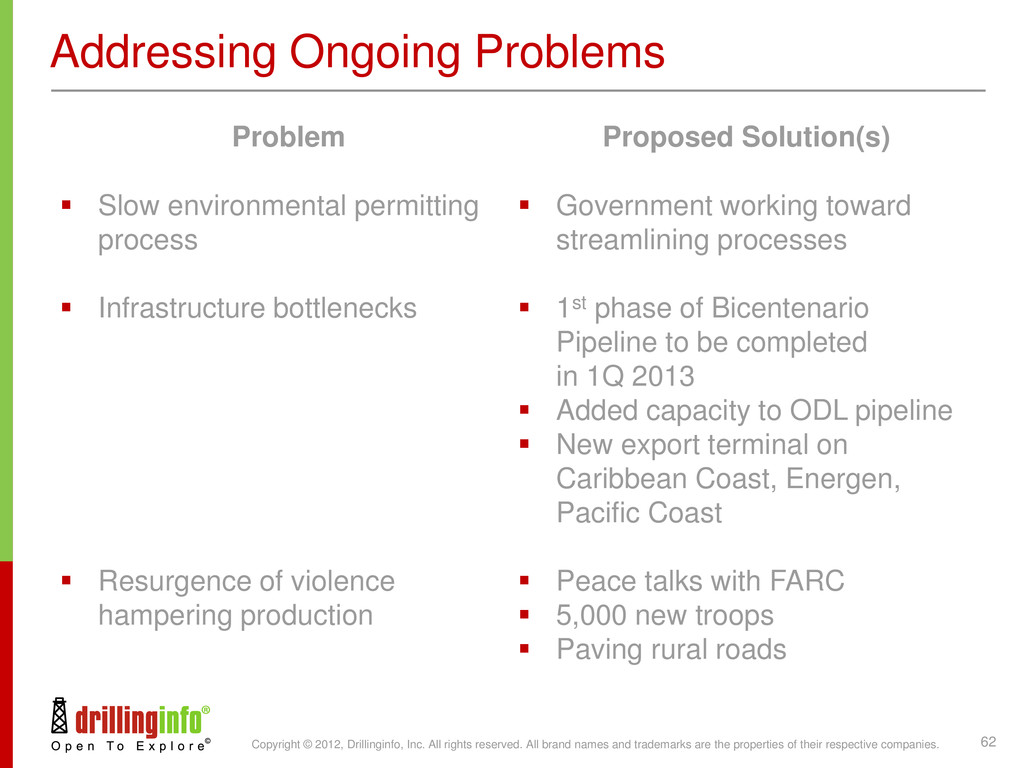

names and trademarks are the properties of their respective companies. 62 Addressing Ongoing Problems Problem Slow environmental permitting process Infrastructure bottlenecks Resurgence of violence hampering production Proposed Solution(s) Government working toward streamlining processes 1st phase of Bicentenario Pipeline to be completed in 1Q 2013 Added capacity to ODL pipeline New export terminal on Caribbean Coast, Energen, Pacific Coast Peace talks with FARC 5,000 new troops Paving rural roads

names and trademarks are the properties of their respective companies. 63 An invitation to Cartagena in 2013 Photo: Claudio Bartolini Save the dates September 8-11, 2013 Cartagena, Colombia For information contact: [email protected] International Conference & Exhibition

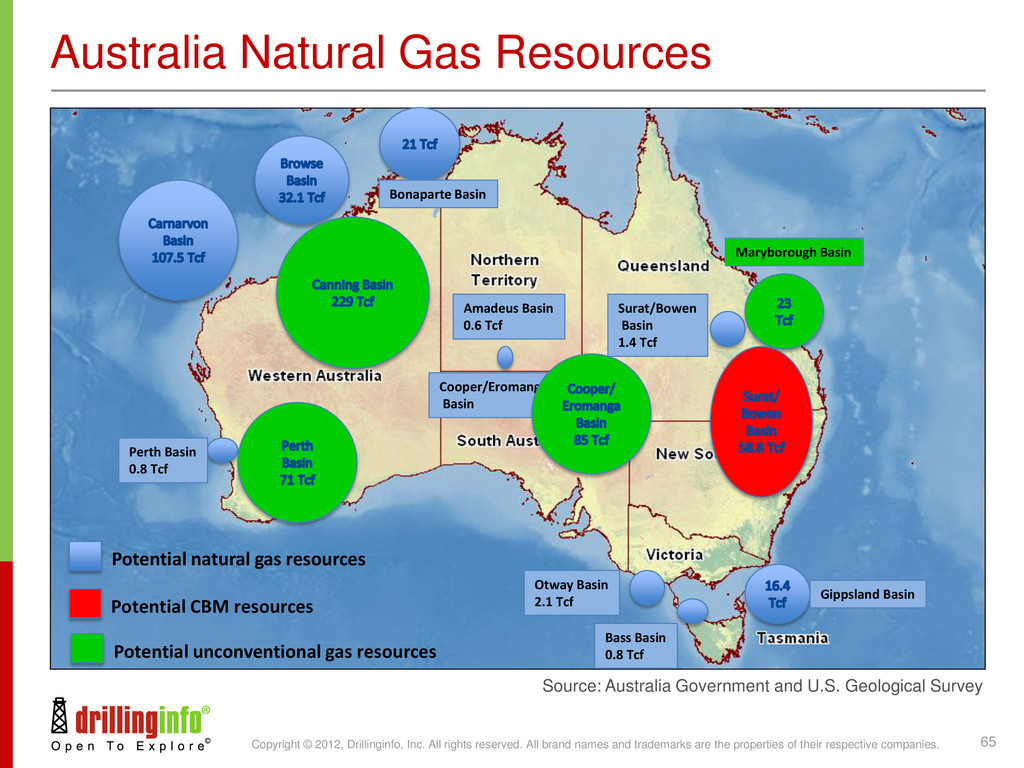

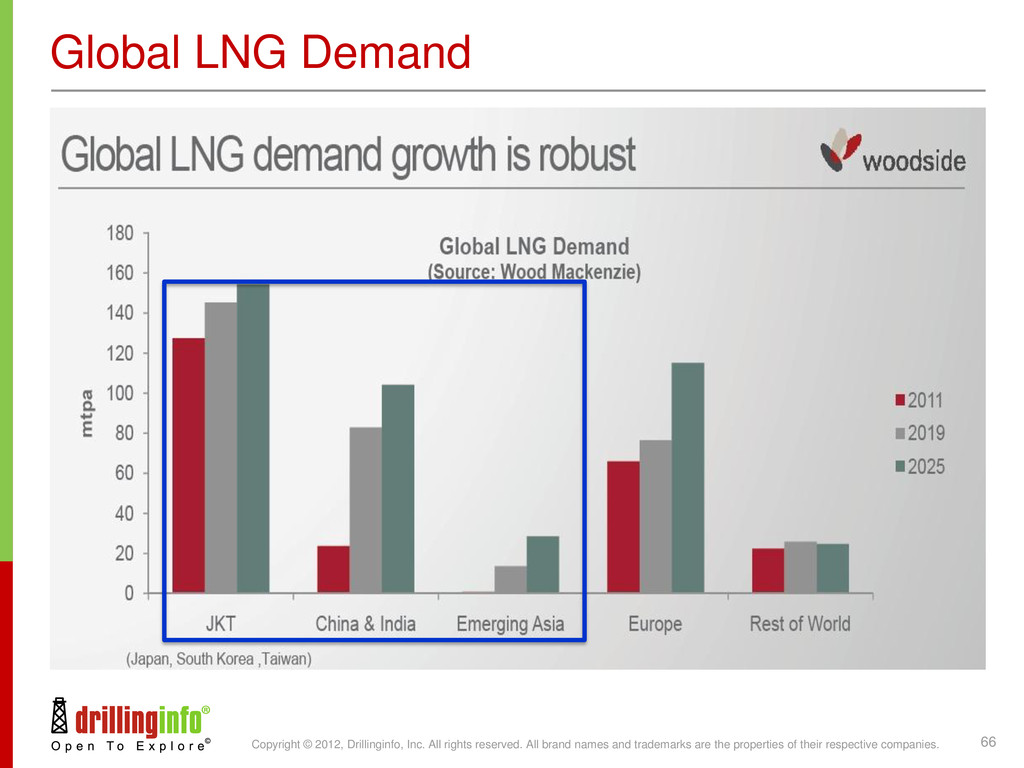

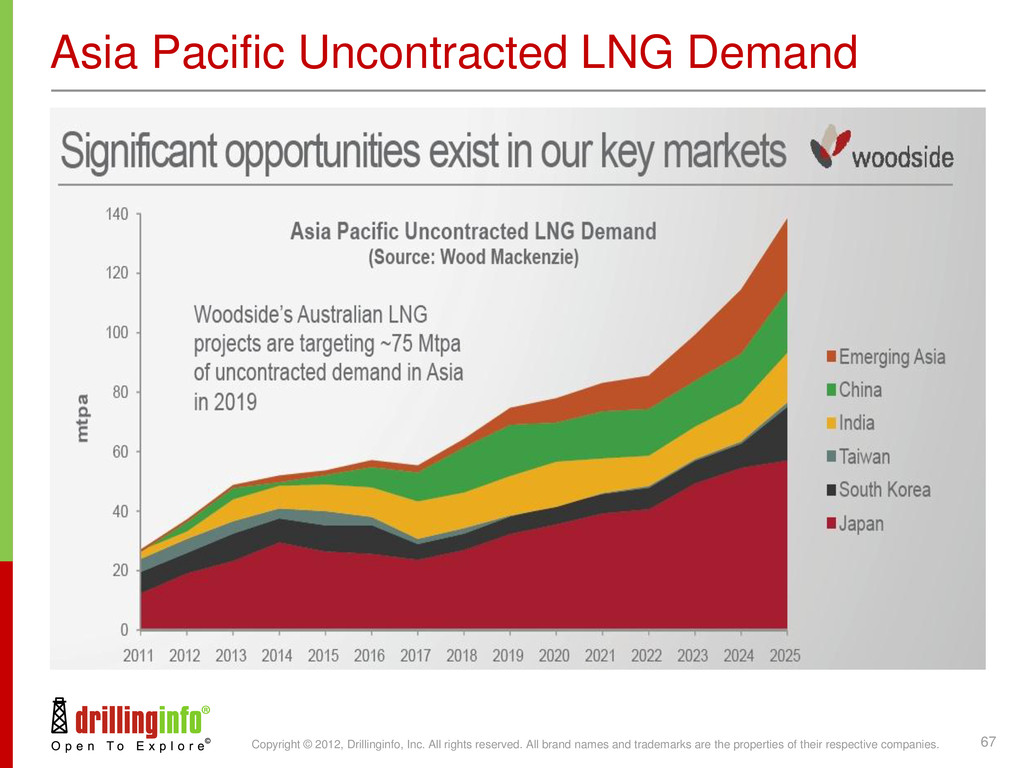

names and trademarks are the properties of their respective companies. 65 Australia Natural Gas Resources Source: Australia Government and U.S. Geological Survey Bonaparte Basin Gippsland Basin Otway Basin 2.1 Tcf Bass Basin 0.8 Tcf Perth Basin 0.8 Tcf Amadeus Basin 0.6 Tcf Cooper/Eromanga Basin Surat/Bowen Basin 1.4 Tcf Maryborough Basin Potential natural gas resources Potential unconventional gas resources Potential CBM resources

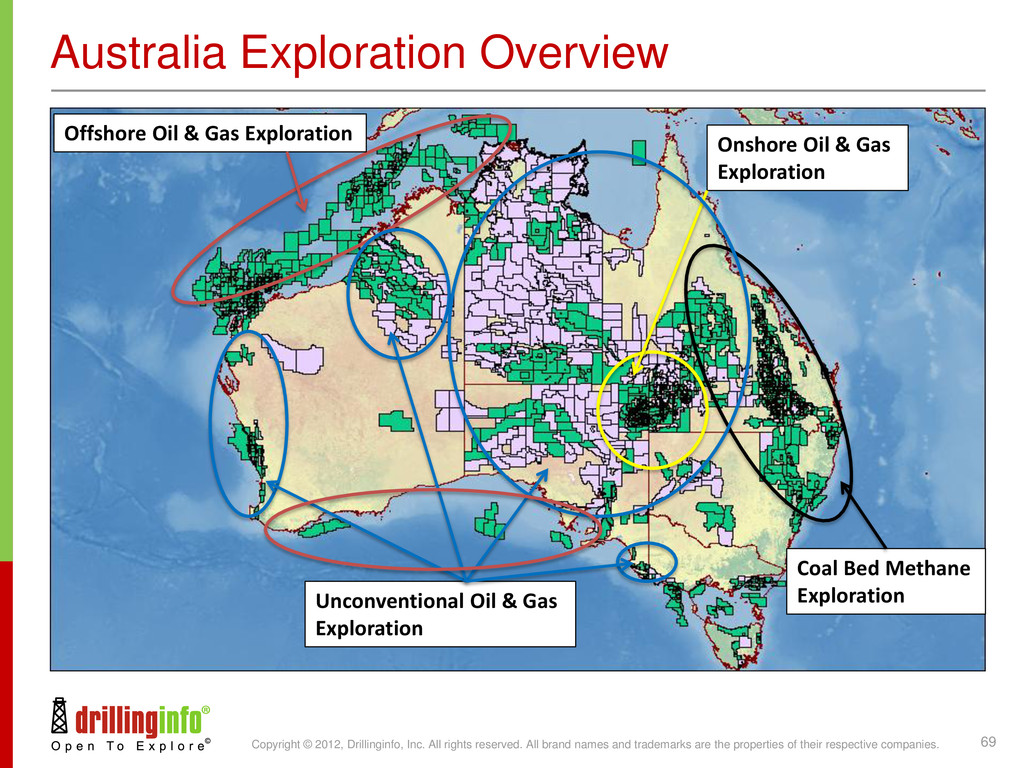

names and trademarks are the properties of their respective companies. 69 Australia Exploration Overview Coal Bed Methane Exploration Unconventional Oil & Gas Exploration Offshore Oil & Gas Exploration Onshore Oil & Gas Exploration

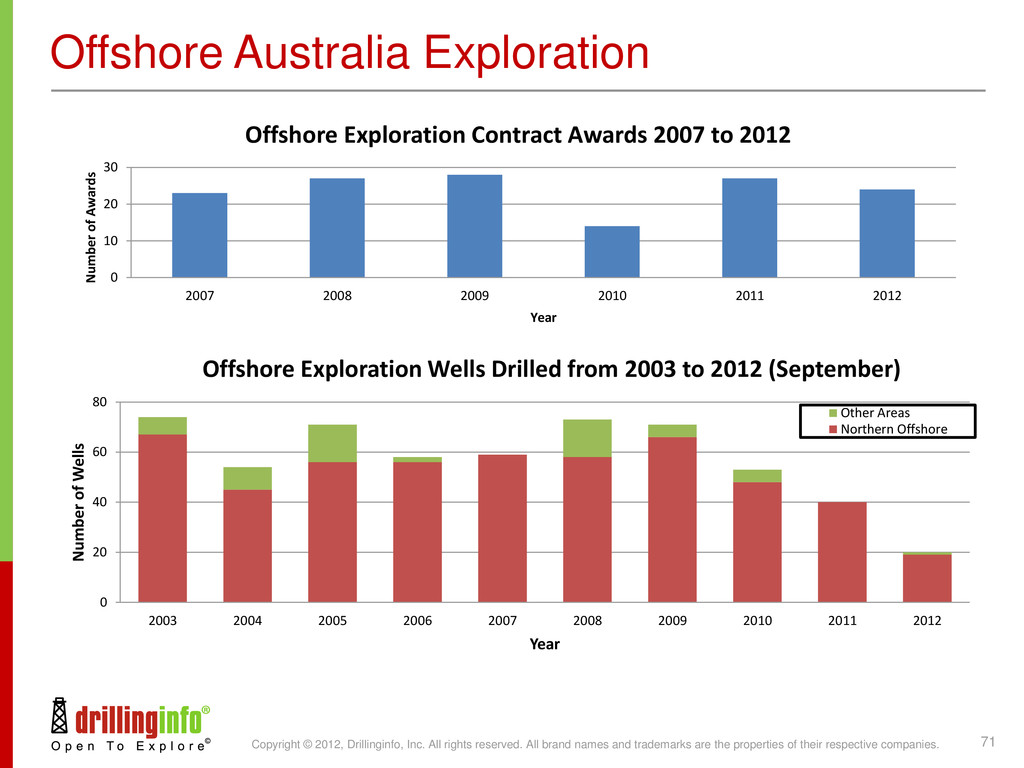

names and trademarks are the properties of their respective companies. 71 Offshore Australia Exploration 0 20 40 60 80 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Number of Wells Year Other Areas Northern Offshore 0 10 20 30 2007 2008 2009 2010 2011 2012 Number of Awards Year Offshore Exploration Contract Awards 2007 to 2012 Offshore Exploration Wells Drilled from 2003 to 2012 (September)

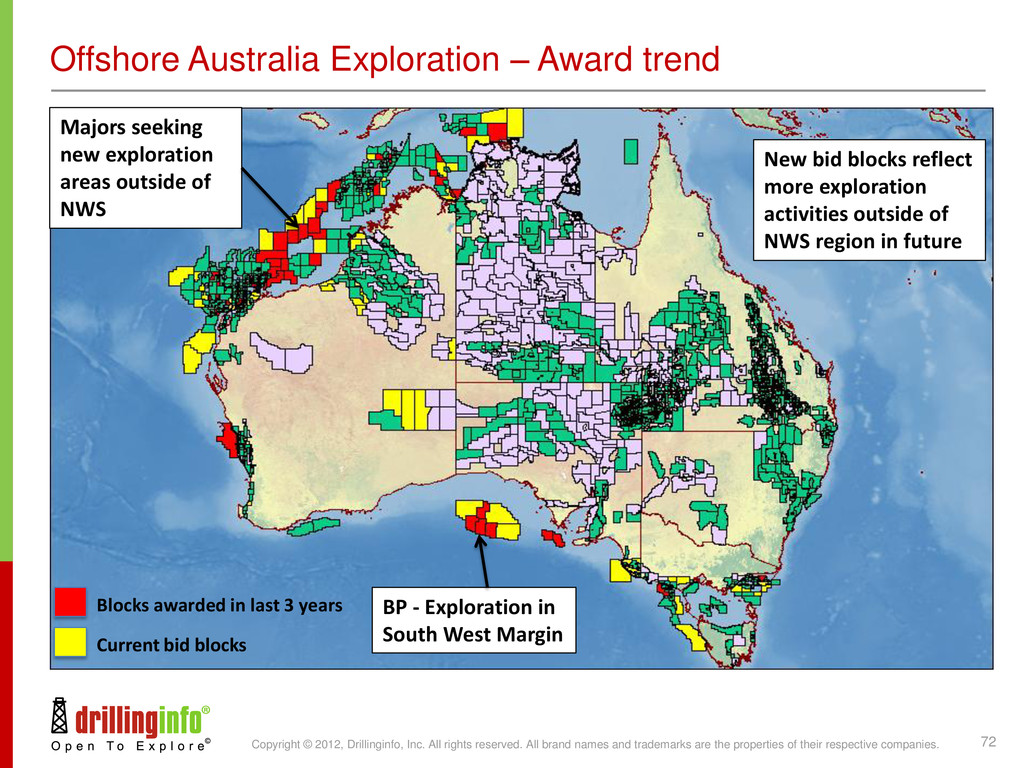

names and trademarks are the properties of their respective companies. 72 Offshore Australia Exploration – Award trend BP - Exploration in South West Margin Majors seeking new exploration areas outside of NWS New bid blocks reflect more exploration activities outside of NWS region in future Blocks awarded in last 3 years Current bid blocks

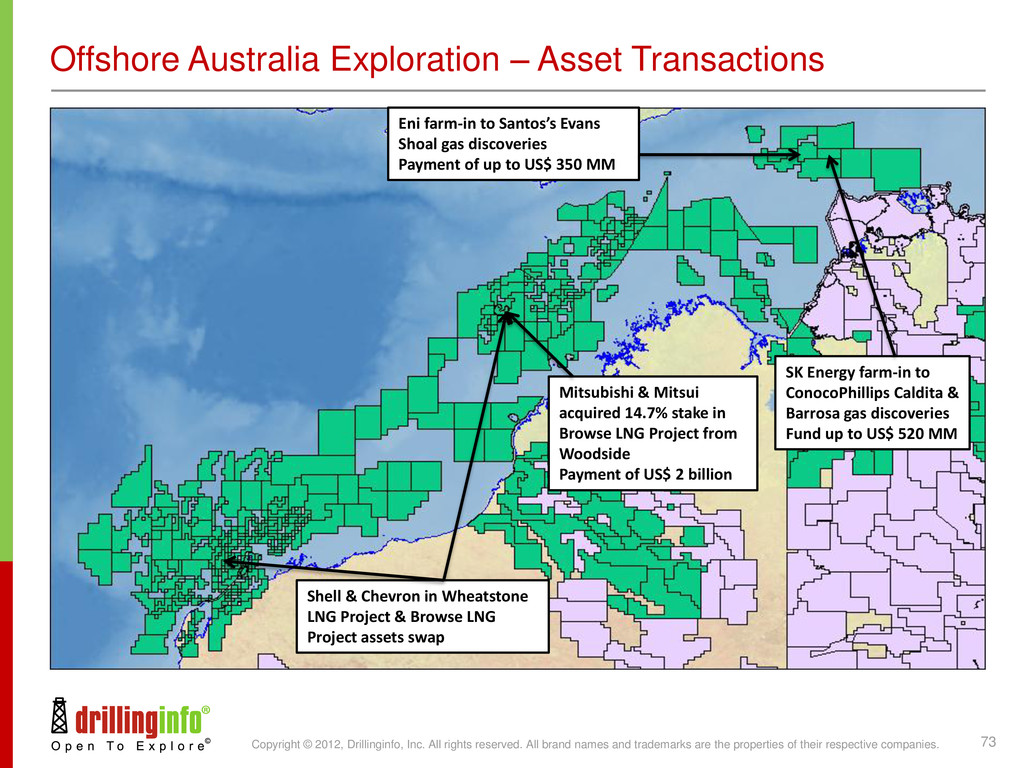

names and trademarks are the properties of their respective companies. 73 Offshore Australia Exploration – Asset Transactions SK Energy farm-in to ConocoPhillips Caldita & Barrosa gas discoveries Fund up to US$ 520 MM Eni farm-in to Santos’s Evans Shoal gas discoveries Payment of up to US$ 350 MM Mitsubishi & Mitsui acquired 14.7% stake in Browse LNG Project from Woodside Payment of US$ 2 billion Shell & Chevron in Wheatstone LNG Project & Browse LNG Project assets swap

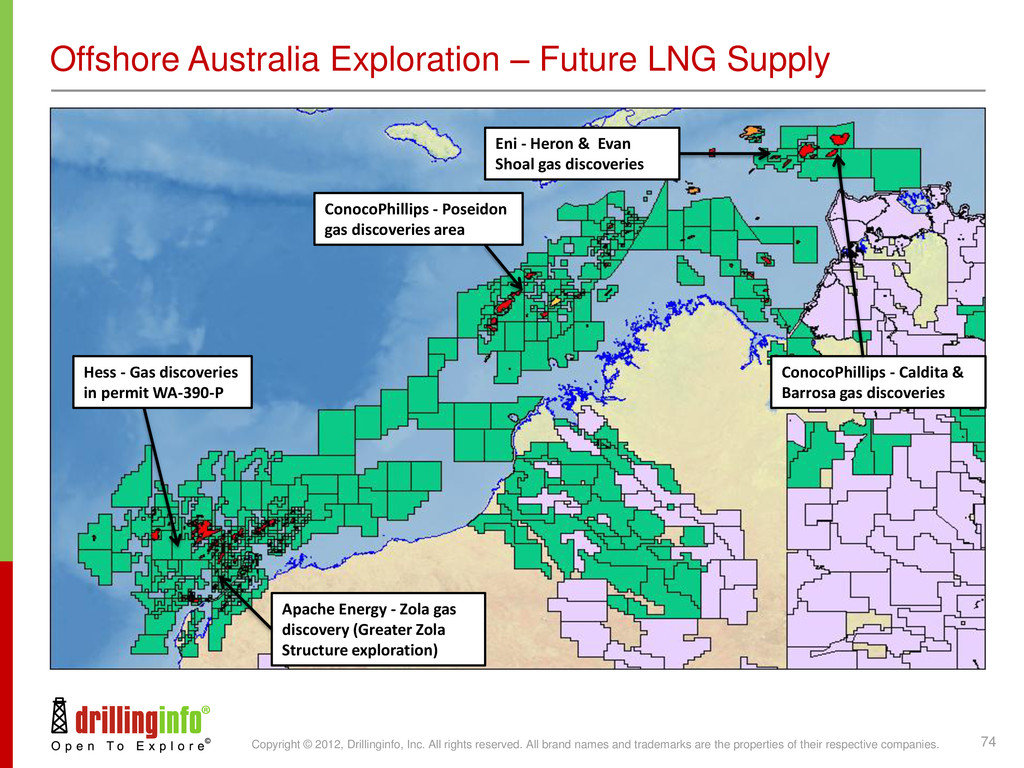

names and trademarks are the properties of their respective companies. 74 Offshore Australia Exploration – Future LNG Supply ConocoPhillips - Caldita & Barrosa gas discoveries Eni - Heron & Evan Shoal gas discoveries ConocoPhillips - Poseidon gas discoveries area Hess - Gas discoveries in permit WA-390-P Apache Energy - Zola gas discovery (Greater Zola Structure exploration)

names and trademarks are the properties of their respective companies. 75 Offshore Australia Exploration - Remarks Majors have been consolidating their assets in the last few years leading to lower exploration drilling activities. Exploration activities offshore going forward to increase especially outside of the NWS region. High level of M&A and asset transaction activities going forward especially with Asian NOCs securing energy supply.

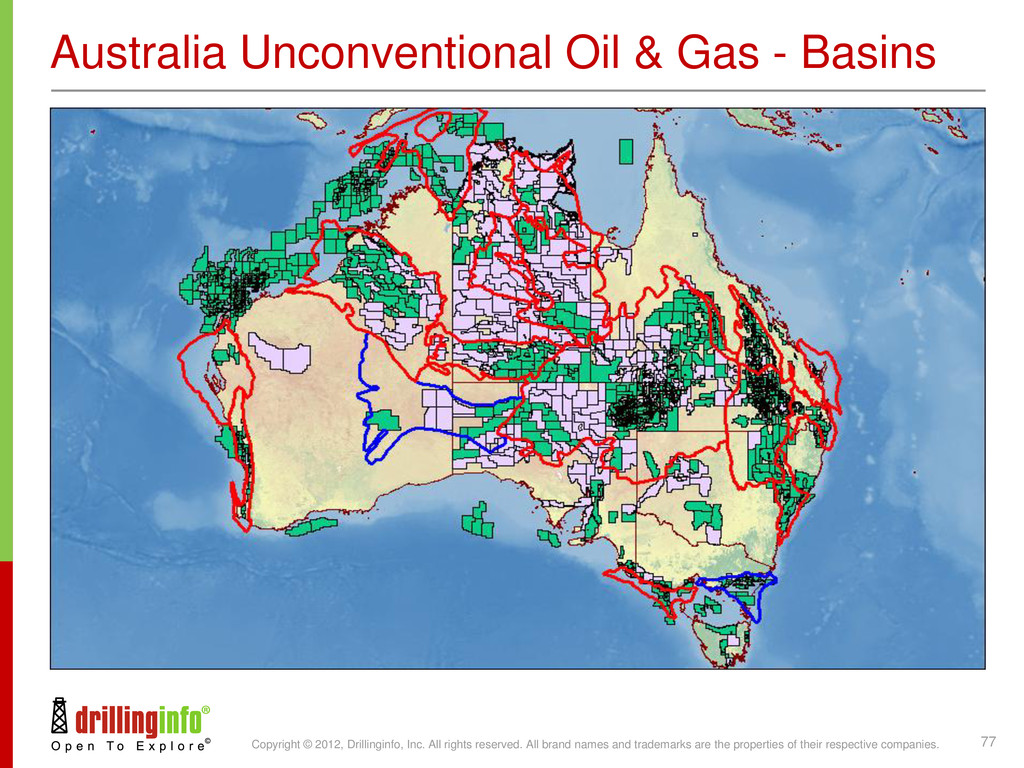

names and trademarks are the properties of their respective companies. 77 Australia Unconventional Oil & Gas - Basins Tight Gas Basins in Australia Shale Oil & Gas Basins in Australia

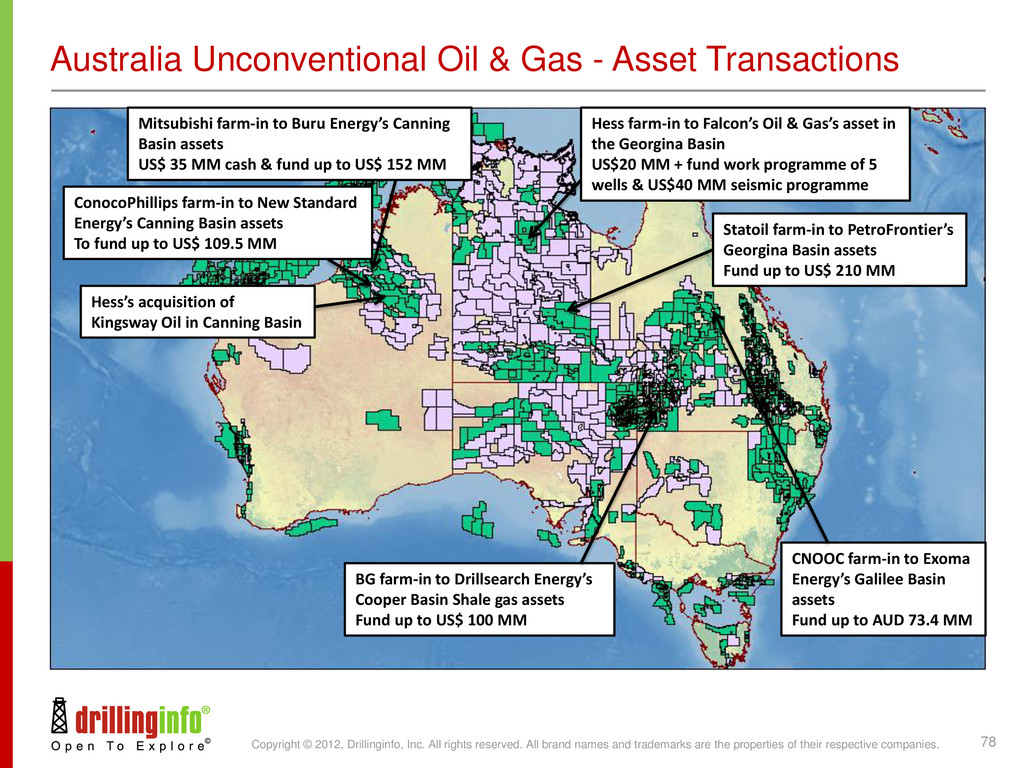

names and trademarks are the properties of their respective companies. 78 Australia Unconventional Oil & Gas - Asset Transactions Mitsubishi farm-in to Buru Energy’s Canning Basin assets US$ 35 MM cash & fund up to US$ 152 MM ConocoPhillips farm-in to New Standard Energy’s Canning Basin assets To fund up to US$ 109.5 MM Hess’s acquisition of Kingsway Oil in Canning Basin Hess farm-in to Falcon’s Oil & Gas’s asset in the Georgina Basin US$20 MM + fund work programme of 5 wells & US$40 MM seismic programme Statoil farm-in to PetroFrontier’s Georgina Basin assets Fund up to US$ 210 MM BG farm-in to Drillsearch Energy’s Cooper Basin Shale gas assets Fund up to US$ 100 MM CNOOC farm-in to Exoma Energy’s Galilee Basin assets Fund up to AUD 73.4 MM

names and trademarks are the properties of their respective companies. 79 Australia Unconventional Oil & Gas – Exploration update Eromanga/Cooper Basin – Santos, Beach Energy, Senex Energy Most active basin with proven shale gas reserves – Santos confirmed the piping of the gas from the unconventional Moomba 191 vertical well into the gathering system (tested 2.6 mmcfg/d from the Roseneath, Epsilon & Murteree (REM) shale reservoirs) Hydraulic fracture stimulations for more wells to commence in later part of the year Horizontal unconventional wells drilling to start in later part of the year Canning Basin – Buru & Mitsubishi, ConocoPhillips & New Standard Energy Ungani oil discovery while targeting unconventional gas exploration (up to 1 MMbo) Discovered a significant tight gas accumulation – Appraisal work ongoing with the Valhalla tight gas discovery Commenced drilling first shale gas exploration well Georgina Basin – Hess & Falcon Oil & Gas, PetroFroniter & Statoil Hydraulic fracture stimulation of three horizontal wells taken place in shale gas reservoir Awaiting testing results with log data and core samples confirming the existence of oil in the Lower Arthur Creek Shale and Thorntonia Carbonate Formations

names and trademarks are the properties of their respective companies. 80 Australia Unconventional Oil & Gas – Exploration Update Perth Basin – AWE Ltd, Northwest Energy Hydraulic fracture stimulation of three vertical wells taken place in both tight gas and shale gas reservoirs Successful flow tested oil, gas & condensate with testing ongoing Galilee Basin – Exoma Energy & CNOOC Extensive drilling underway to gather information on the Toolebuc Shale for laboratory testing of oil and gas maturity and generation Encouraging results so far with most wells encountering background oil and gas while drilling McArthur Basin – Armour Energy One horizontal well drilled to target shale reservoir which flowed gas to surface from the Barney Creek Shale and the Coxvo Dolomite Formations No hydraulic fracture stimulation taken place

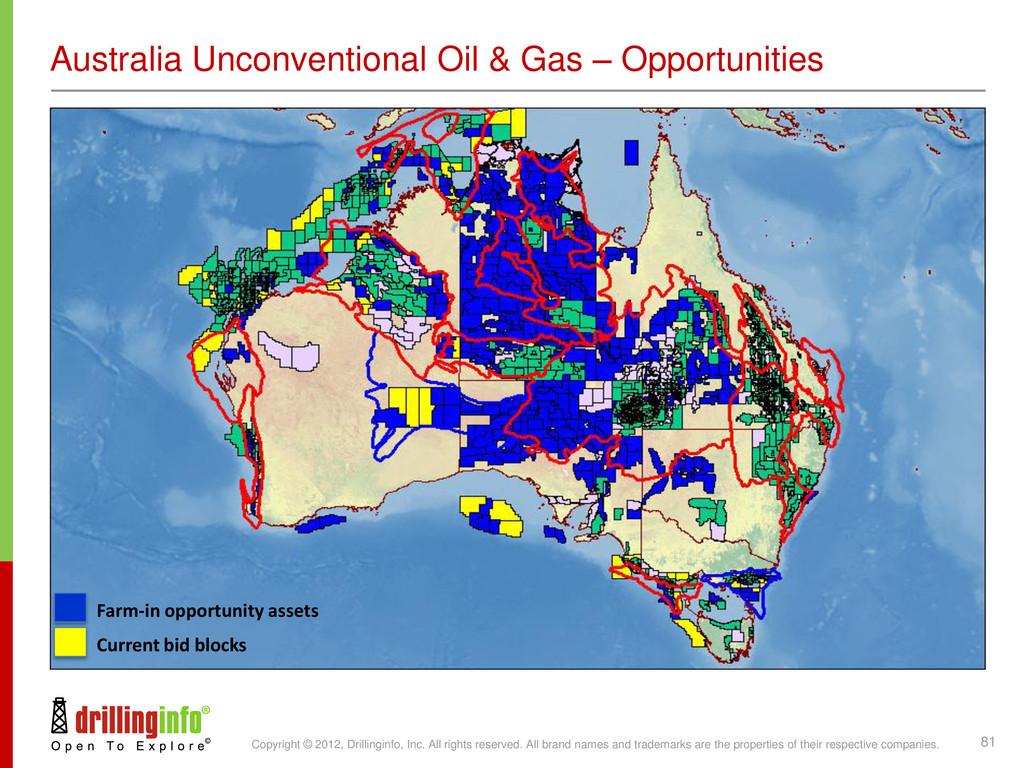

names and trademarks are the properties of their respective companies. 81 Australia Unconventional Oil & Gas – Opportunities Current bid blocks Farm-in opportunity assets

names and trademarks are the properties of their respective companies. 82 Australia Unconventional Oil & Gas - Remarks Unconventional exploration is still in an infancy stage in Australia Unconventional exploration activities is set to increase in the coming years Most areas with unconventional exploration potential have been licensed but lots of opportunities for entry

names and trademarks are the properties of their respective companies. 83 High cost of equipment and labour Lack of infrastructure like pipelines & roads Strict environmental / HSE Native Title Act can delay operations Australia Exploration Challenges High cost of equipment and labour Lack of infrastructure like pipelines & roads Strict environmental / HSE Native Title Act can delay operations Major Australia Oil & Gas pipeline Major Australia Oil & Gas pipeline

names and trademarks are the properties of their respective companies. 84 High cost of equipment and labour Lack of infrastructure like pipelines & roads Strict environmental / HSE Native Title Act can delay operations Australia Exploration Challenges High cost of equipment and labour Lack of infrastructure like pipelines & roads Strict environmental / HSE Native Title Act can delay operations Thank you

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}