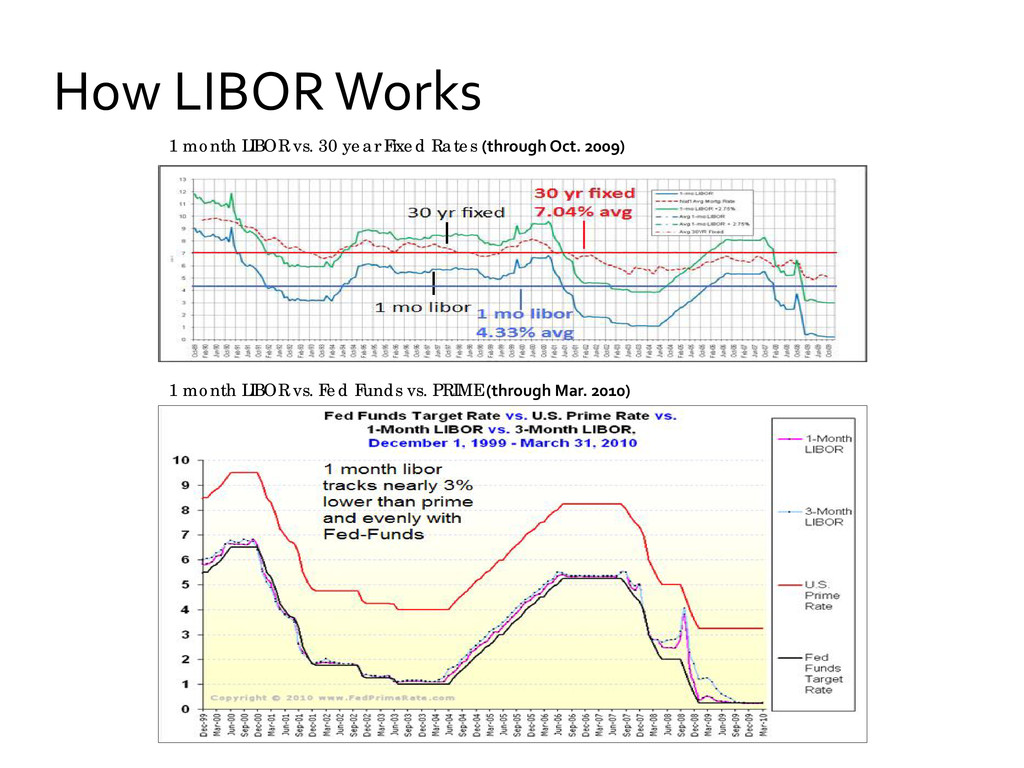

system adopted LIBOR as a much needed benchmark for short-term, interbank loans. The LIBOR rates are now globally recognized indexes used for pricing many types of consumer and corporate loans, debt instruments and debt securities across the globe. LIBOR is the average interest rate charged when banks in the London interbank money market borrow unsecured funds from each other. There are many different LIBOR rates (maturities range from overnight to 12 months) for numerous currencies, including Eurodollars. A Eurodollar is an American dollar on deposit in any bank outside the United States, and is therefore not subject to regulation by the U.S. Federal Reserve. LIBOR rates are fixed every UK business day by the international media company Thomson Reuters, in association with the British Bankers' Association (BBA), a not-for-profit trade association. Just before 11:00 a.m. GMT, the BBA polls a specific panel of highly reputable, high-volume banks which participate in the London wholesale money market. The BBA finds out the rate at which each bank on the panel could borrow Eurodollars from other banks, for specific maturities. The BBA figures out the central tendency -- the interquartile mean -- for each maturity, then publishes these rates at about 11:30 a.m. GMT. Three American banks are included in the panel surveyed by the BBA for Eurodollar fixing: Citibank, Bank of America and JP Morgan Chase. There are also 13 non-U.S. banks surveyed for Eurodollar fixing in London, bringing the total Eurodollar panel count to 16. To get the interquartile mean for each maturity, the BBA starts with the 16 rates, discards the four lowest and four highest rates, then determines the average of the remaining 8 rates. • Will we see Carter-era rates? Very doubtful. Now more countries are all competing on the global market, which is far more robust, minimizing the chance that domestic interest rates will ever reach those stratospheric levels again. • Inflation? Tight labor markets and wage growth, 9.7% unemployment, and idle factories with plenty of inventory means we're not likely to see any measurable move with the Fed Funds Target Rate or 1 month Libor rates for "an extended period of time." • How does the 1 month LIBOR move? Mortgage rates move with MBS pricing in the short term, but the market for MBS is absolutely connected to the larger debt market. The Fed only meets about 6 times annually and when they do move the target rate up they do it by 25 bps on average. The average rate of increase since the early 90's is only +1.45% per year, or +12 basis points per month. The average duration of the last 3 rising rate trends is 26 months. So looking at history, the facts are that rates move up at a gradual pace following inflationary driven monetary policy. (see graphs below) • Low Rate vs. Low Balance Reducing what you owe is a bigger hedge to interest costs. Reducing rate on an amortized loan is may reduce your monthly payment, but has a significantly less effect than focusing on lowering your balance. • Example: a 15 year fixed at 9% or a 30 year fixed at 5% both at $400,000 - the 15 year fixed would save about $43,000 in interest and 15 years. Rate has the least to do with saving time and money.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}