only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Dayna Guest FLDP-Intern, Enterprise Planning Emily Widdison FLDP-Intern, External GAAP Reporting Nikki de Castro FLDP-Intern, HIMCO Finance Taylor Ross FLDP-Intern, Specialty Casualty August 3, 2012 The Hartford’s General Liability Insurance Business

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 2 Objectives Current Landscape • Outline current landscape of The Hartford’s General Liability focus Middle Market Key General Liability Specialty General Liability Specialty Casualty Specialty Programs General Liability National Accounts General Liability Discover Best Practices • Discover best practices within focus segments and offer potential opportunities to leverage these best practices among The Hartford’s General Liability Insurance Business Identify Potential Opportunities to Drive Profitable Growth • Emphasize how capitalizing on these opportunities will be beneficial to The Hartford’s long term profitability and growth

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 3 Recommendations Leverage existing Education and Marketing best practices of the General Liability line, with a focus on Communication across business segments Communication: Leverage capabilities across all business segments Education: Build upon and enhance current training offerings at The Hartford and elaborate on the potential for learning opportunities stemming from communication recommendations Marketing: Highlight existing strengths across the General Liability segments and couple them with our recommendations.

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Commercial Markets Middle Market • Enables medium-sized companies to stay focused on their business by providing 360 degrees of protection Key Accounts • Offers property, workers’ compensation, General Liability, commercial auto and umbrella protection Specialty GL • Focuses on liability coverage of accounts Specialty Commercial • Serves agent and end-buyer needs with the right product and risk management options for their specific exposures and circumstances National Accounts • Provides account tailored insurance products and risk management services Specialty Programs • Concentrates on specialized insurance programs 4

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 5 General Liability • Insurance protection appropriate for all business sizes and industries designed to provide coverage in the event of negligence or oversight in a location, service, or product that is provided to the public • One of the core policies protecting business’ from potential lawsuits and mitigating a companies liability exposure • Coverage ranges from slip and fall accidents to slander and copyright infringement Bodily Injury and Property Damage Liability Personal and Advertising Injuries Medical Payments Damage to Premises Rented to You Employment Practices Liability Additional Insured

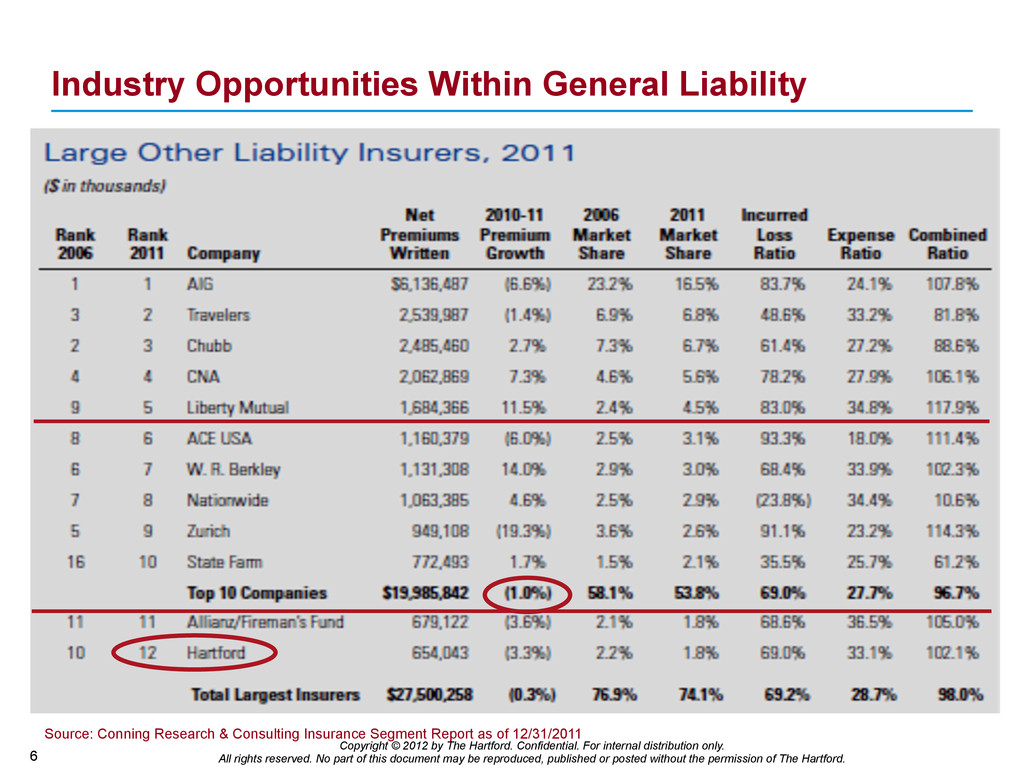

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Industry Opportunities Within General Liability 6 Source: Conning Research & Consulting Insurance Segment Report as of 12/31/2011

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 7 The Hartford’s Potential Options The Hartford’s General Liability Push Product Expansion with Existing Core Competencies Enhance Existing Core Competencies then Push Product Expansion

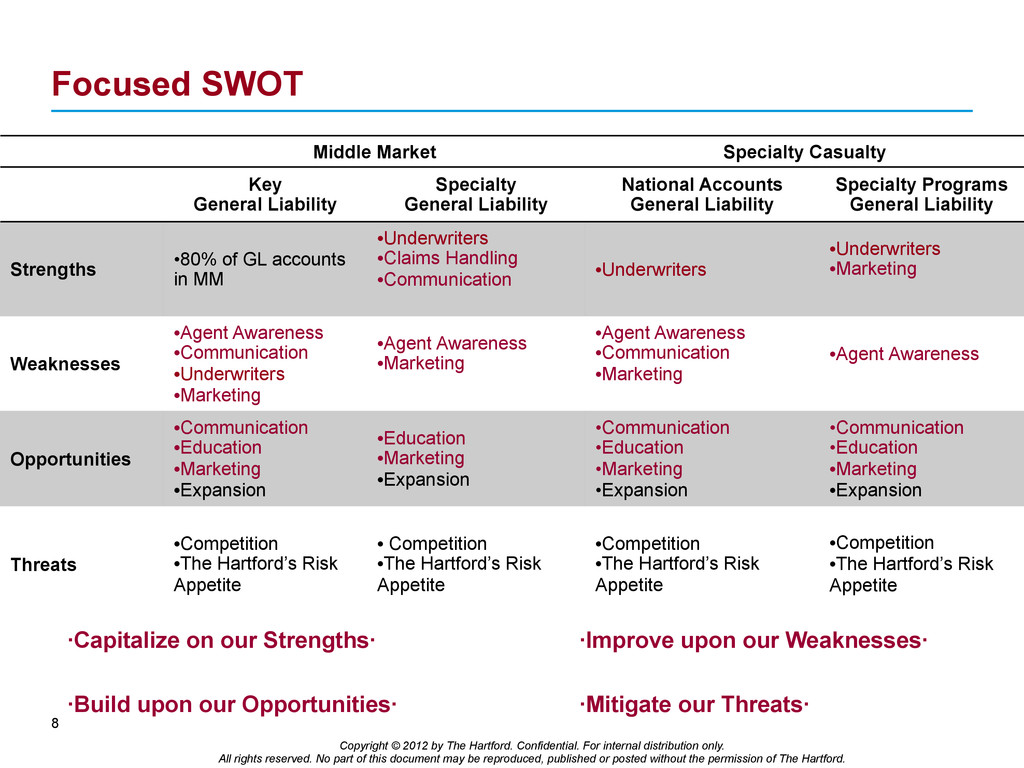

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 8 Focused SWOT Middle Market Specialty Casualty Key General Liability Specialty General Liability National Accounts General Liability Specialty Programs General Liability Strengths • 80% of GL accounts in MM • Underwriters • Claims Handling • Communication • Underwriters • Underwriters • Marketing Weaknesses • Agent Awareness • Communication • Underwriters • Marketing • Agent Awareness • Marketing • Agent Awareness • Communication • Marketing • Agent Awareness Opportunities • Communication • Education • Marketing • Expansion • Education • Marketing • Expansion • Communication • Education • Marketing • Expansion • Communication • Education • Marketing • Expansion Threats • Competition • The Hartford’s Risk Appetite • Competition • The Hartford’s Risk Appetite • Competition • The Hartford’s Risk Appetite • Competition • The Hartford’s Risk Appetite ·Capitalize on our Strengths· ·Improve upon our Weaknesses· ·Build upon our Opportunities· ·Mitigate our Threats·

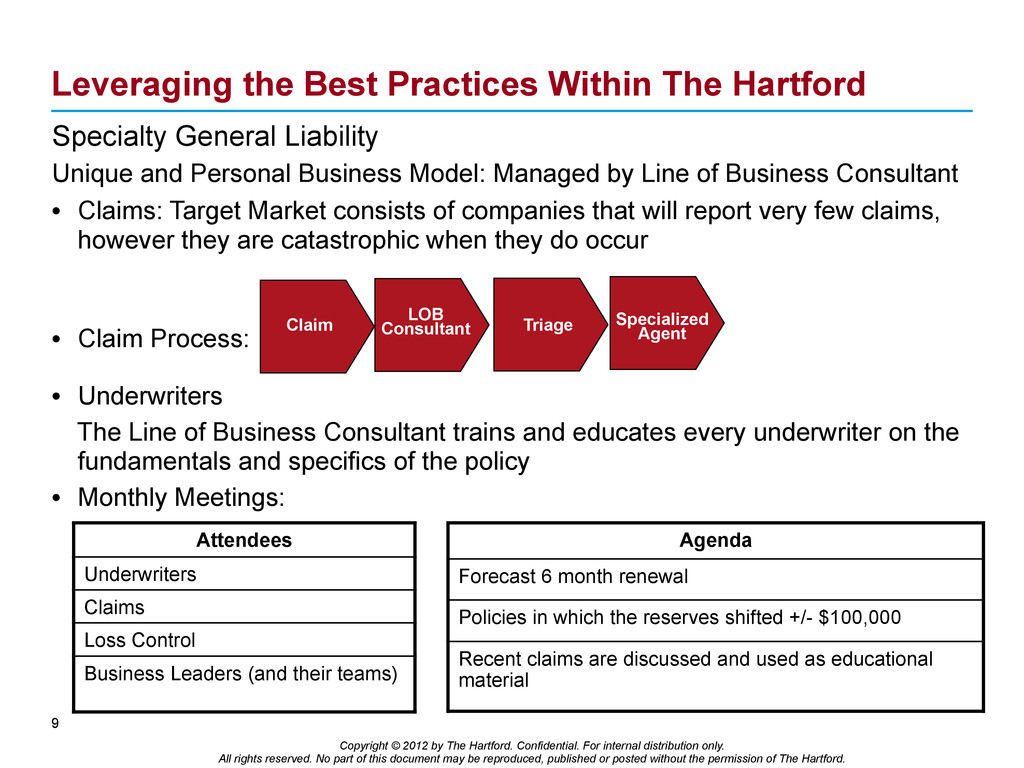

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Specialty General Liability Unique and Personal Business Model: Managed by Line of Business Consultant • Claims: Target Market consists of companies that will report very few claims, however they are catastrophic when they do occur • Claim Process: 9 Leveraging the Best Practices Within The Hartford LOB Consultant Specialized Agent Triage Claim Attendees Underwriters Claims Loss Control Business Leaders (and their teams) • Underwriters The Line of Business Consultant trains and educates every underwriter on the fundamentals and specifics of the policy • Monthly Meetings: Agenda Forecast 6 month renewal Policies in which the reserves shifted +/- $100,000 Recent claims are discussed and used as educational material

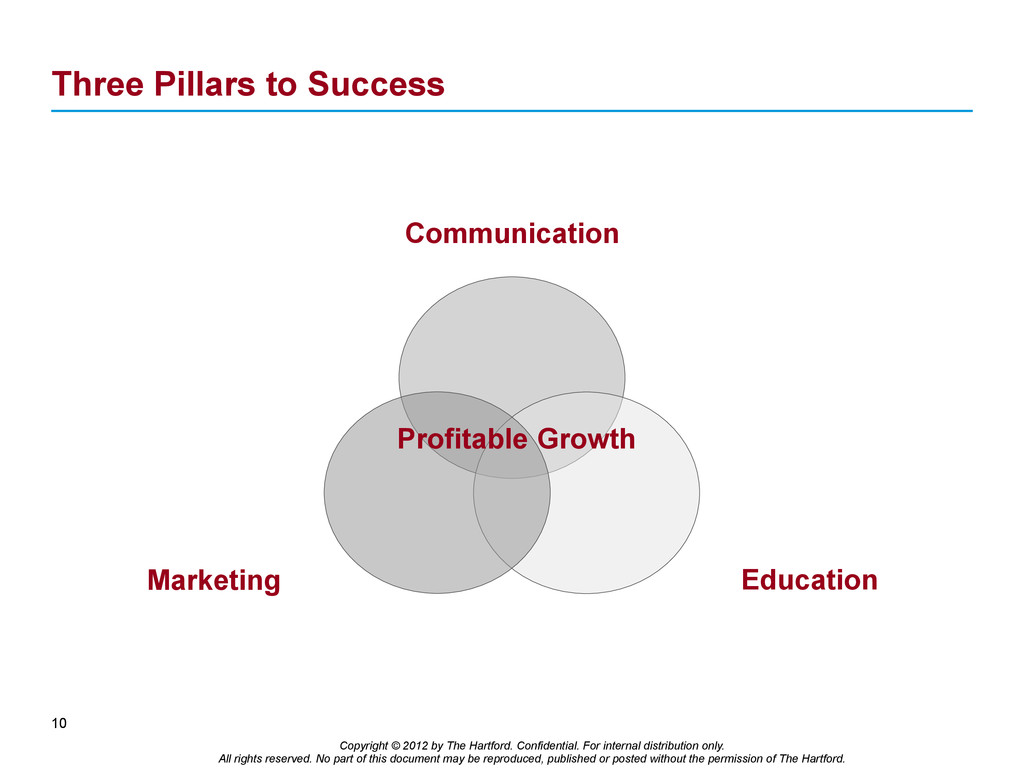

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 10 Three Pillars to Success Communication Education Marketing Profitable Growth

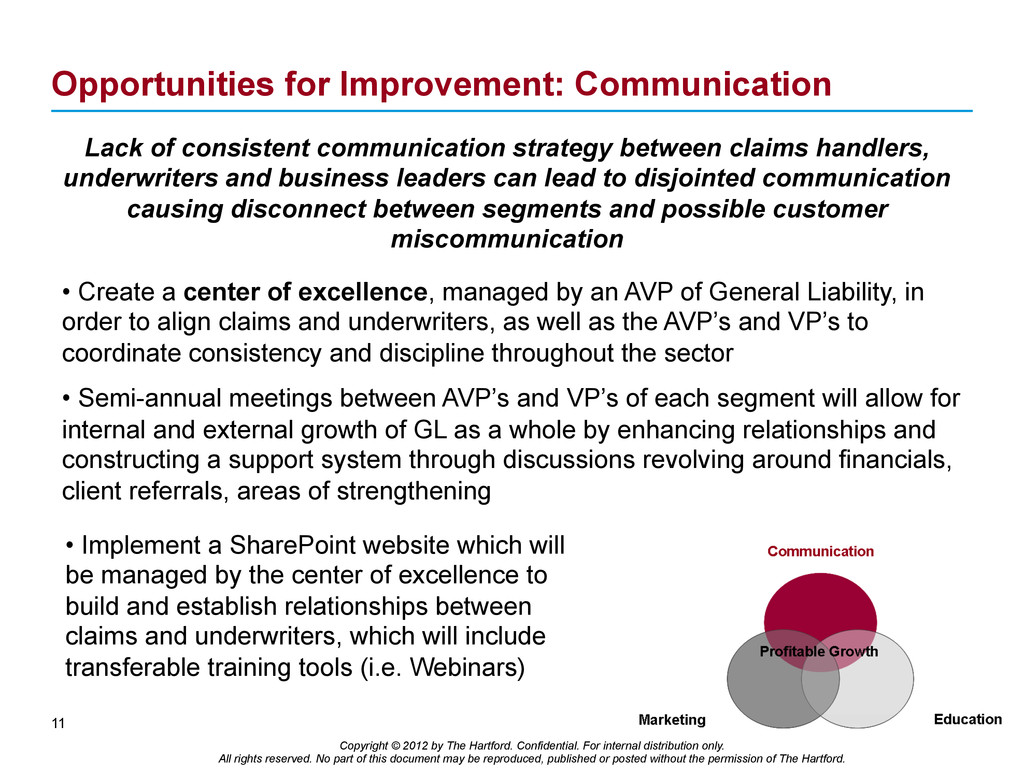

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 11 Opportunities for Improvement: Communication Lack of consistent communication strategy between claims handlers, underwriters and business leaders can lead to disjointed communication causing disconnect between segments and possible customer miscommunication • Create a center of excellence, managed by an AVP of General Liability, in order to align claims and underwriters, as well as the AVP’s and VP’s to coordinate consistency and discipline throughout the sector • Semi-annual meetings between AVP’s and VP’s of each segment will allow for internal and external growth of GL as a whole by enhancing relationships and constructing a support system through discussions revolving around financials, client referrals, areas of strengthening • Implement a SharePoint website which will be managed by the center of excellence to build and establish relationships between claims and underwriters, which will include transferable training tools (i.e. Webinars)

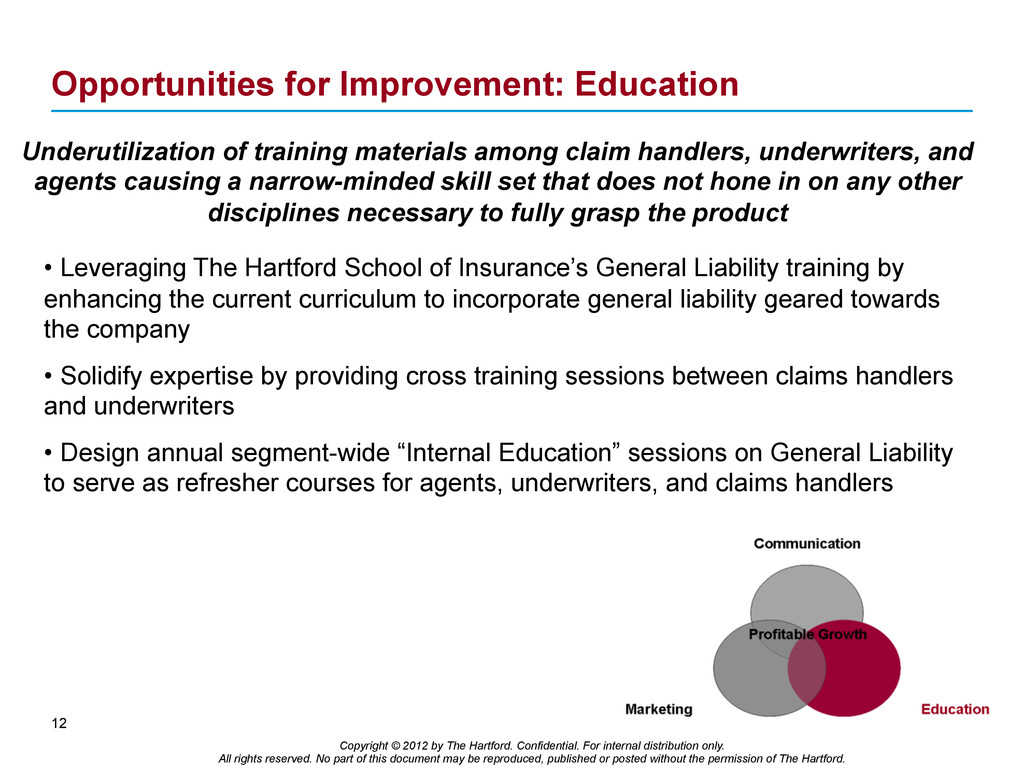

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 12 Opportunities for Improvement: Education • Leveraging The Hartford School of Insurance’s General Liability training by enhancing the current curriculum to incorporate general liability geared towards the company • Solidify expertise by providing cross training sessions between claims handlers and underwriters • Design annual segment-wide “Internal Education” sessions on General Liability to serve as refresher courses for agents, underwriters, and claims handlers Underutilization of training materials among claim handlers, underwriters, and agents causing a narrow-minded skill set that does not hone in on any other disciplines necessary to fully grasp the product

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 13 Opportunities for Improvement: Marketing • Highlight the existing universal segment strengths and accentuate new emphasis on communication in order to create an easier approach for marketing to target agents and offer incentives to enhance sales • Shift focus into social media in order to increase The Hartford’s General Liability exposure • Establish an agent immersion program to have participants have the opportunity to learn about their position and the company more in depth Limited opportunities to leverage motivation and increase confidence among agents to sell General Liability leading to an focus on other product offerings

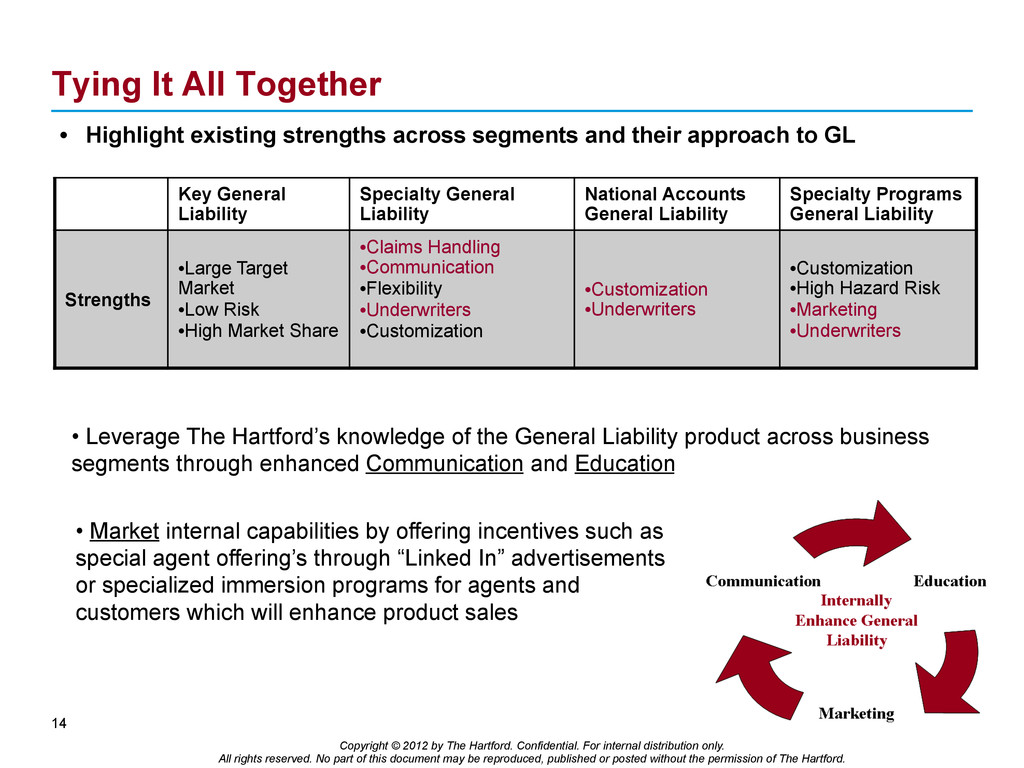

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 14 Tying It All Together • Highlight existing strengths across segments and their approach to GL Key General Liability Specialty General Liability National Accounts General Liability Specialty Programs General Liability Strengths • Large Target Market • Low Risk • High Market Share • Claims Handling • Communication • Flexibility • Underwriters • Customization • Customization • Underwriters • Customization • High Hazard Risk • Marketing • Underwriters • Leverage The Hartford’s knowledge of the General Liability product across business segments through enhanced Communication and Education • Market internal capabilities by offering incentives such as special agent offering’s through “Linked In” advertisements or specialized immersion programs for agents and customers which will enhance product sales

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 15 The Hartford's “Go Forward Strategy” “Broadening property and liability capabilities to complement existing strength in workers’ compensation” “We want to build on our core competencies in insurance underwriting, claims management and distribution” “The company will leverage its strong relationships with clients and distribution partners, product breadth, and expertise in underwriting and claims management to improve returns and grow profitability” *Quotes taken from The Hartford’s website and March 2012 Conference Call Presentation

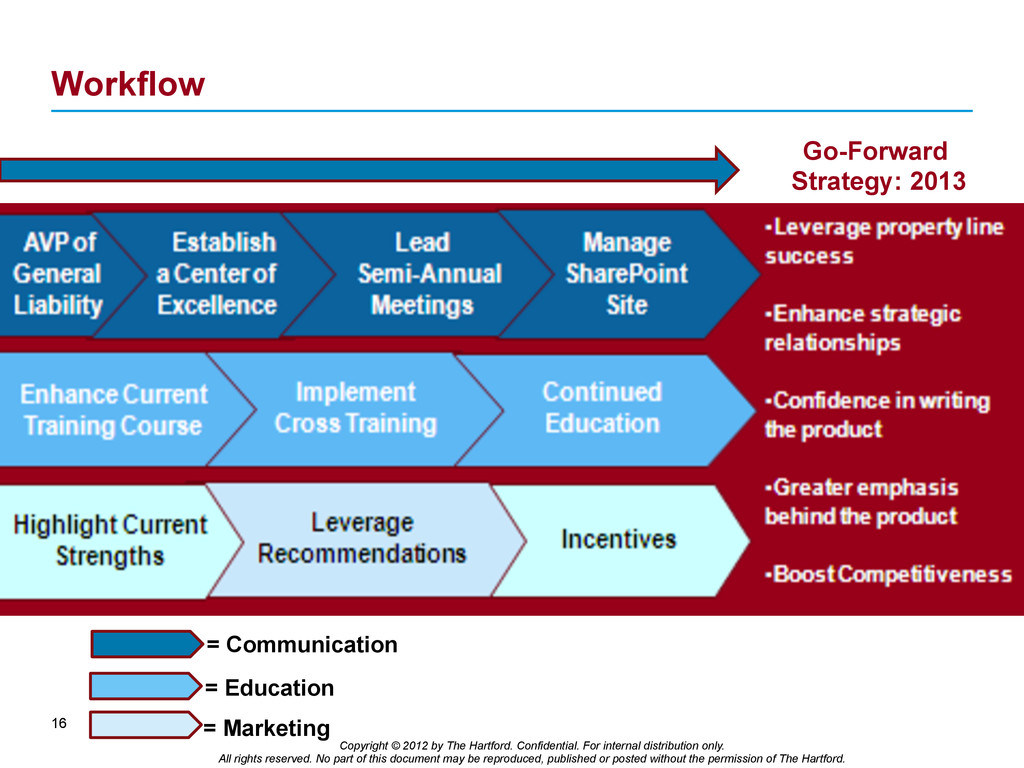

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Workflow 16 Go-Forward Strategy: 2013 = Communication = Education = Marketing

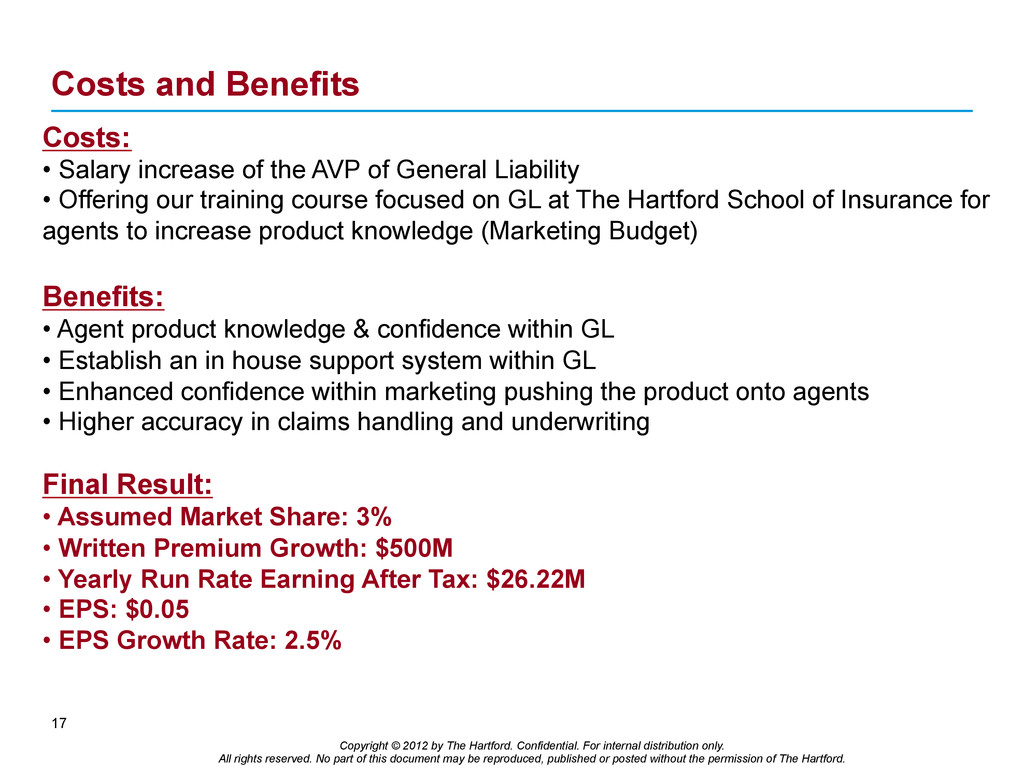

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 17 Costs and Benefits Costs: • Salary increase of the AVP of General Liability • Offering our training course focused on GL at The Hartford School of Insurance for agents to increase product knowledge (Marketing Budget) Benefits: • Agent product knowledge & confidence within GL • Establish an in house support system within GL • Enhanced confidence within marketing pushing the product onto agents • Higher accuracy in claims handling and underwriting Final Result: • Assumed Market Share: 3% • Written Premium Growth: $500M • Yearly Run Rate Earning After Tax: $26.22M • EPS: $0.05 • EPS Growth Rate: 2.5%

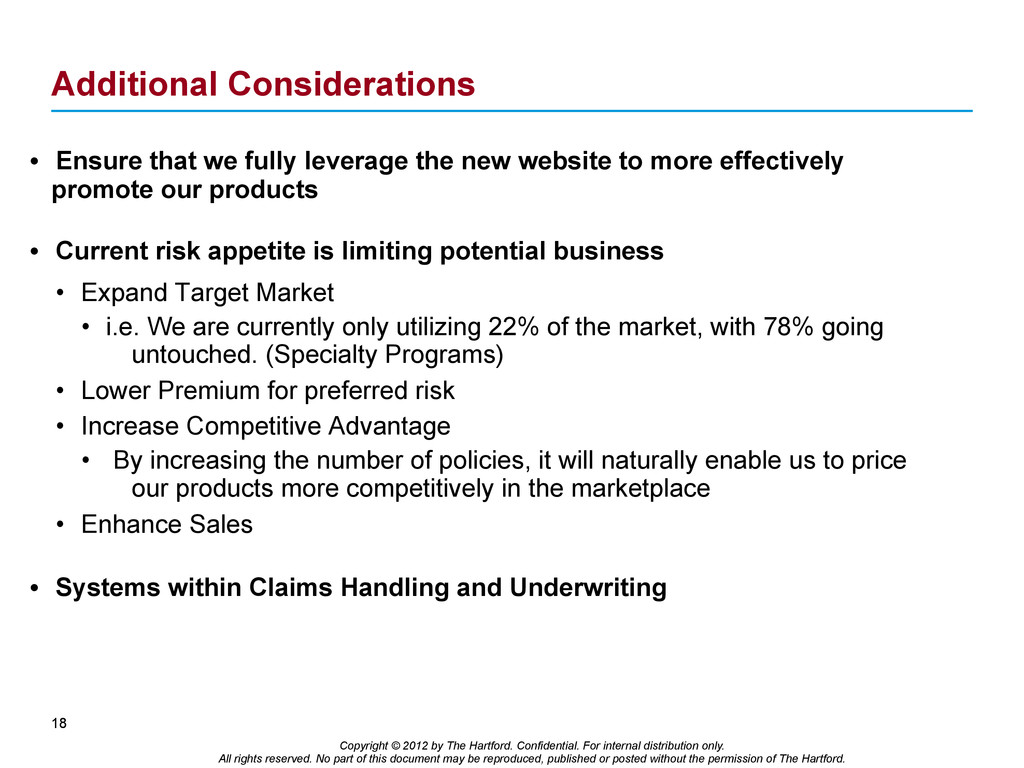

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 18 Additional Considerations • Ensure that we fully leverage the new website to more effectively promote our products • Current risk appetite is limiting potential business • Expand Target Market • i.e. We are currently only utilizing 22% of the market, with 78% going untouched. (Specialty Programs) • Lower Premium for preferred risk • Increase Competitive Advantage • By increasing the number of policies, it will naturally enable us to price our products more competitively in the marketplace • Enhance Sales • Systems within Claims Handling and Underwriting 18

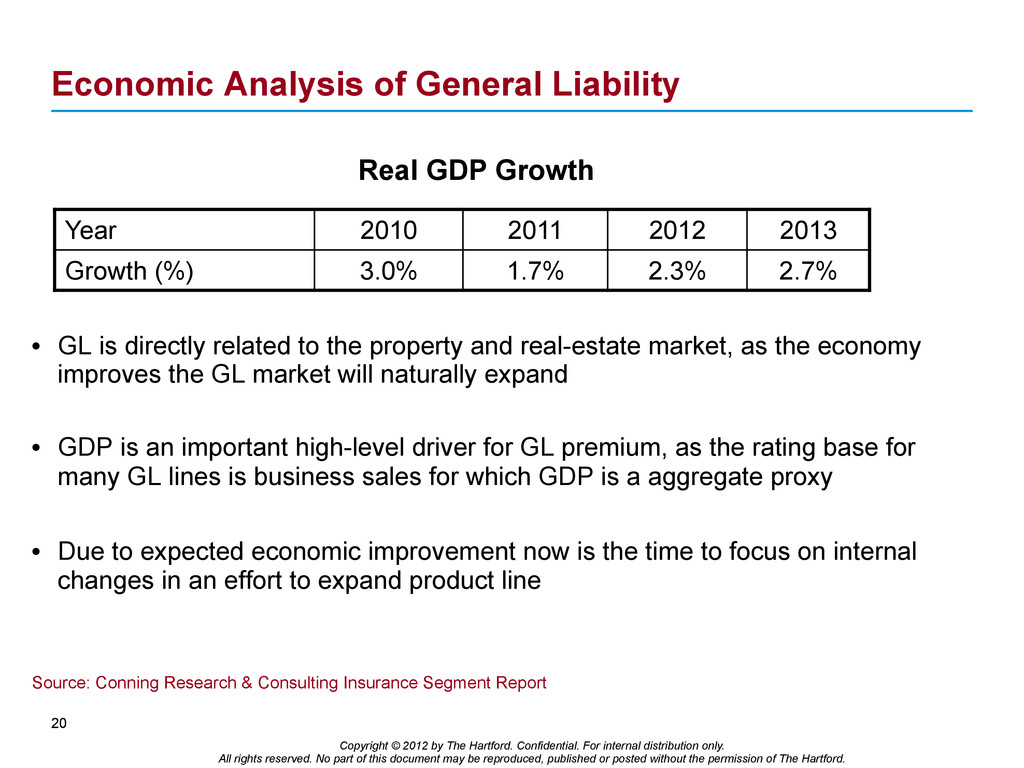

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 20 Economic Analysis of General Liability • GL is directly related to the property and real-estate market, as the economy improves the GL market will naturally expand • GDP is an important high-level driver for GL premium, as the rating base for many GL lines is business sales for which GDP is a aggregate proxy • Due to expected economic improvement now is the time to focus on internal changes in an effort to expand product line Source: Conning Research & Consulting Insurance Segment Report Year 2010 2011 2012 2013 Growth (%) 3.0% 1.7% 2.3% 2.7% Real GDP Growth

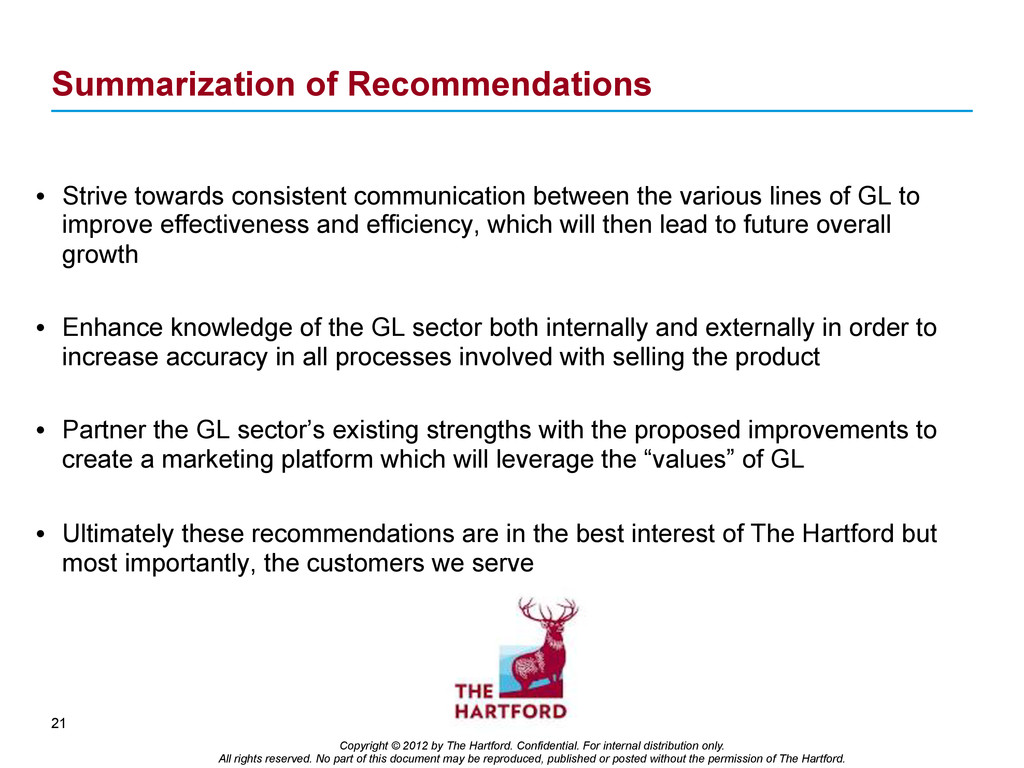

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 21 Summarization of Recommendations • Strive towards consistent communication between the various lines of GL to improve effectiveness and efficiency, which will then lead to future overall growth • Enhance knowledge of the GL sector both internally and externally in order to increase accuracy in all processes involved with selling the product • Partner the GL sector’s existing strengths with the proposed improvements to create a marketing platform which will leverage the “values” of GL • Ultimately these recommendations are in the best interest of The Hartford but most importantly, the customers we serve

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 22 Acknowledgements • Deb Bibbins, VP Cap and Spec Programs • Richard Bulat, Mgr Strategic Marketing • Marissa Crean, FLDP Director • Kevin Finn, VP National Accounts • Laurie Flanagan, AD Marketing • Rick Griffin, Director UW Spec Commercial • Walker Hawkins, FLDP • Martin John, AVP Fin Analysis Reporting • Brian Kearney, VP Underwriting • Brendon Kelly, Dir Fin Analysis Reporting • Michele Lemery, AVP Field Claims • Nicole Marek, Director Marketing • Joe Mathieu, AVP Prod & UW Key Accts • Rosemary Meskill, Paralegal Claim • Matt Moore, Cons Fin Analysis • Greg Porydzy, AVP Underwriting RMD • Jen Raulukaitis, FLDP • Charlene Ridgeway, VP Field Claims • Marianne Stefanov, Mgr Strategic Marketing • Scott Stevens, VP Program Cap & Spec • Rowena Styron, Director UW Practices • John Voglesong, AD Financial Analysis • Bob Walsh, Cons LOB Claim • Keith Wechsler, Product Manager

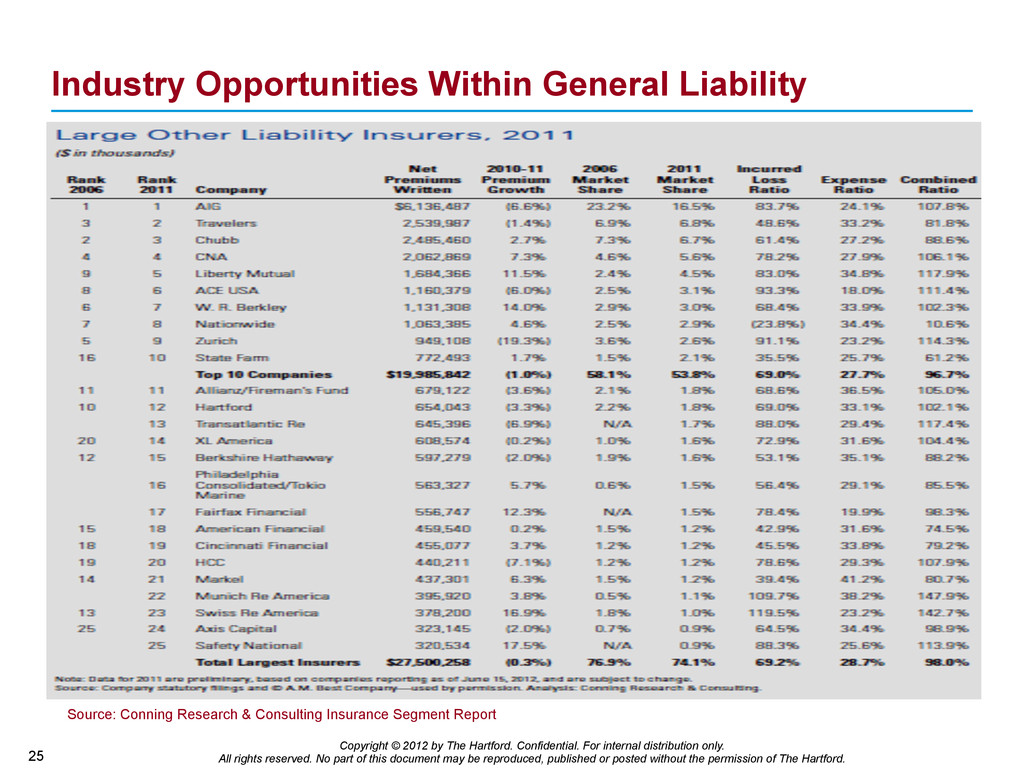

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Industry Opportunities Within General Liability 25 Source: Conning Research & Consulting Insurance Segment Report

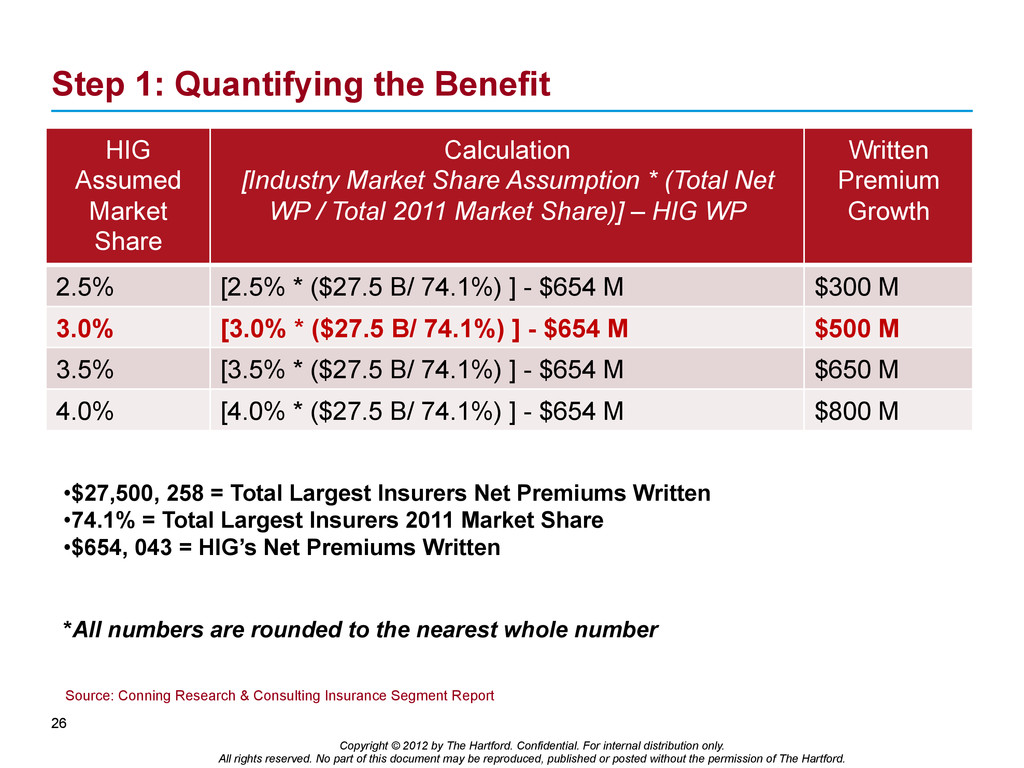

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Step 1: Quantifying the Benefit HIG Assumed Market Share Calculation [Industry Market Share Assumption * (Total Net WP / Total 2011 Market Share)] – HIG WP Written Premium Growth 2.5% [2.5% * ($27.5 B/ 74.1%) ] - $654 M $300 M 3.0% [3.0% * ($27.5 B/ 74.1%) ] - $654 M $500 M 3.5% [3.5% * ($27.5 B/ 74.1%) ] - $654 M $650 M 4.0% [4.0% * ($27.5 B/ 74.1%) ] - $654 M $800 M 26 • $27,500, 258 = Total Largest Insurers Net Premiums Written • 74.1% = Total Largest Insurers 2011 Market Share • $654, 043 = HIG’s Net Premiums Written *All numbers are rounded to the nearest whole number Source: Conning Research & Consulting Insurance Segment Report

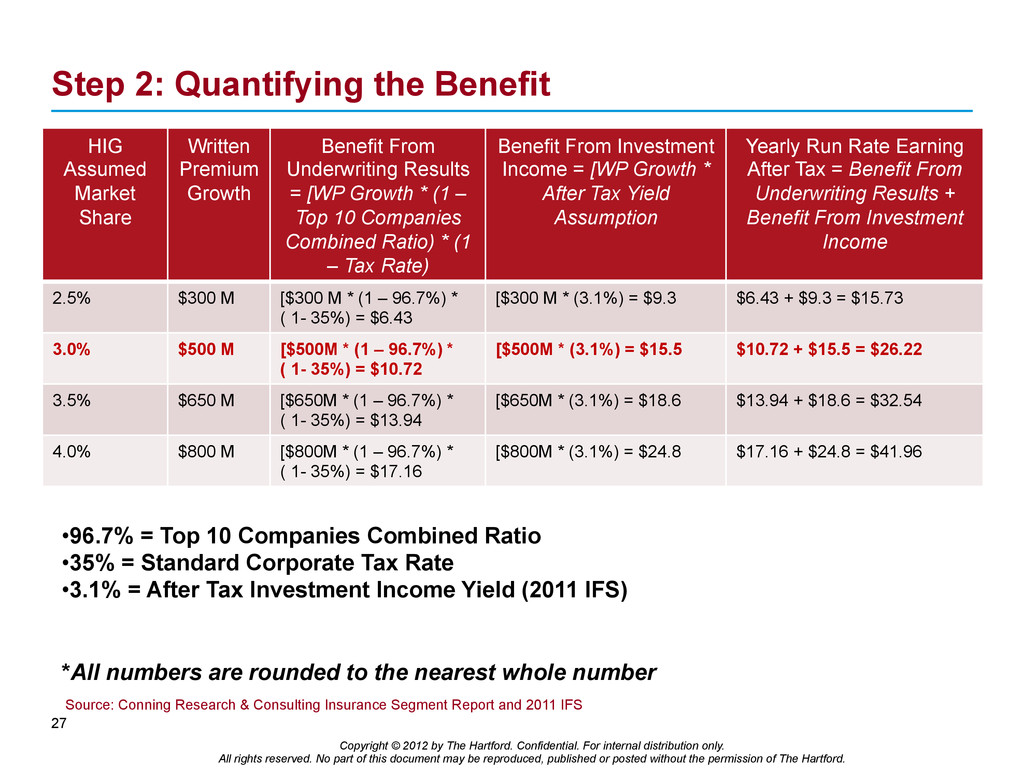

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Step 3: Quantifying the Benefit HIG Assumed Market Share Yearly Run Rate Earning After Tax = Benefit From Underwriting Results + Benefit From Investment Income EPS = Yearly Run Rate Earning After Tax / Number of Shares Outstanding EPS Growth Rate = EPS / 2011 EPS 2.5% $6.43 + $9.3 = $15.73 $15.73 / 478 M = $0.03 $0.03 / $1.96 = 1.5% 3.0% $10.72 + $15.5 = $26.22 $26.22 / 478 M = $0.05 $0.05 / $1.96 = 2.5% 3.5% $13.94 + $18.6 = $32.54 $32.54 / 478 M = $0.07 $0.07 / $1.96 = 3.6% 4.0% $17.16 + $24.8 = $41.96 $41.96 / 478 M = $0.09 $0.09 / $1.96 = 4.6% 28 • 478 M = Number of Shares Outstanding • $1.96 = 2011 EPS *All numbers are rounded to the nearest whole number Source: 2011 IFS

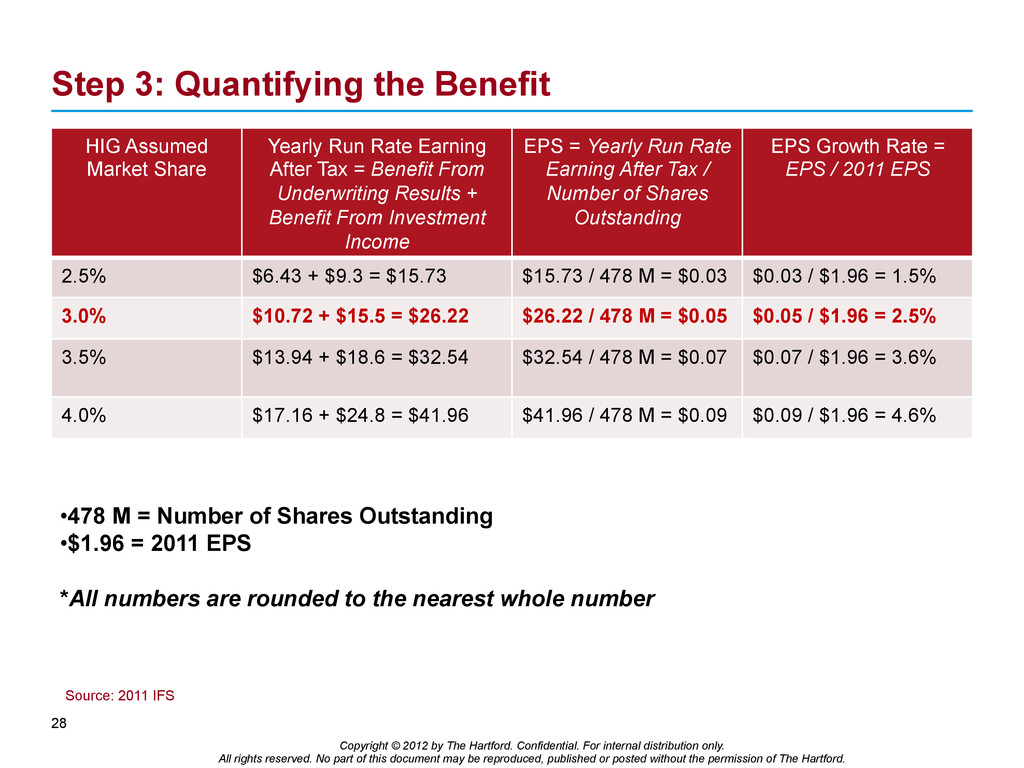

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. Written Premium by Segment Forecasted 2012 2013 Growth Assumptions Key GL 250 M 252 M Spec. GL 133 M 132 M National Accts. 31 M 32 M SP GL 70 M 86 M Total 483 M 502 M The Hartford expects the GL book to grow 3.9% from 2012 to 2013 Source: All financials pulled directly from TM1

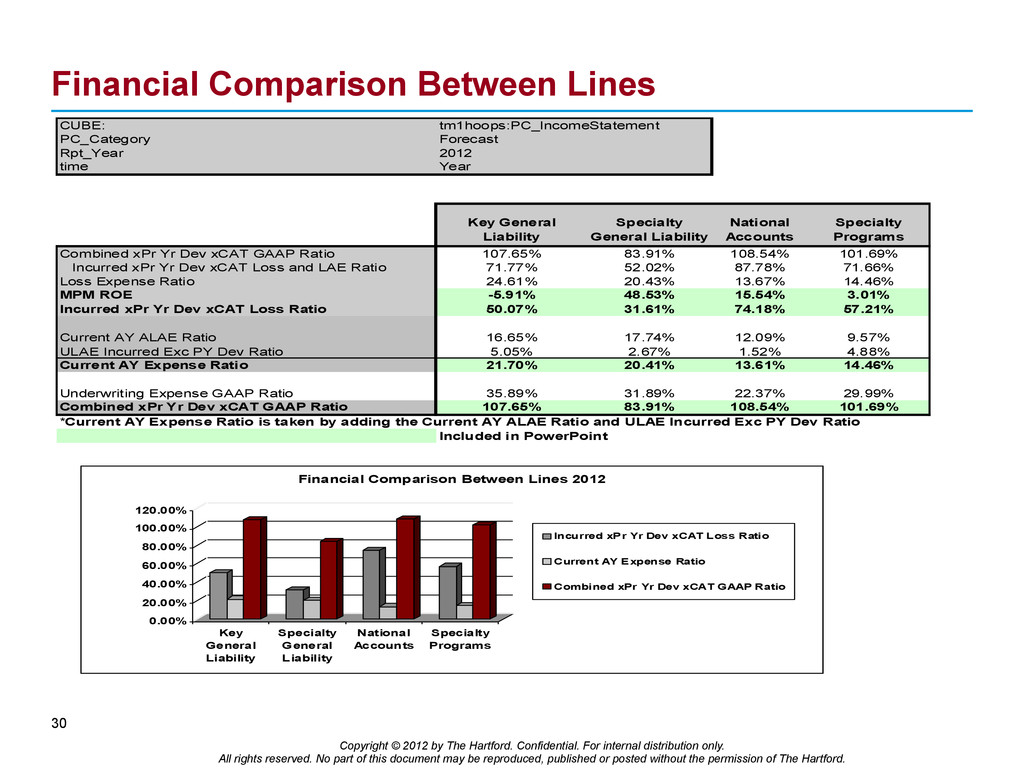

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 30 Financial Comparison Between Lines CUBE: tm1hoops:PC_IncomeStatement PC_Category Forecast Rpt_Year 2012 time Year Key General Liability Specialty General Liability National Accounts Specialty Programs Combined xPr Yr Dev xCAT GAAP Ratio 107.65% 83.91% 108.54% 101.69% Incurred xPr Yr Dev xCAT Loss and LAE Ratio 71.77% 52.02% 87.78% 71.66% Loss Expense Ratio 24.61% 20.43% 13.67% 14.46% MPM ROE -5.91% 48.53% 15.54% 3.01% Incurred xPr Yr Dev xCAT Loss Ratio 50.07% 31.61% 74.18% 57.21% Current AY ALAE Ratio 16.65% 17.74% 12.09% 9.57% ULAE Incurred Exc PY Dev Ratio 5.05% 2.67% 1.52% 4.88% Current AY Expense Ratio 21.70% 20.41% 13.61% 14.46% Underwriting Expense GAAP Ratio 35.89% 31.89% 22.37% 29.99% Combined xPr Yr Dev xCAT GAAP Ratio 107.65% 83.91% 108.54% 101.69% *Current AY Expense Ratio is taken by adding the Current AY ALAE Ratio and ULAE Incurred Exc PY Dev Ratio Included in PowerPoint 0.00% 20.00% 40.00% 60.00% 80.00% 100.00% 120.00% Key General Liability Specialty General Liability National Accounts Specialty Programs Financial Comparison Between Lines 2012 Incurred xPr Yr Dev xCAT Loss Ratio Current AY Expense Ratio Combined xPr Yr Dev xCAT GAAP Ratio

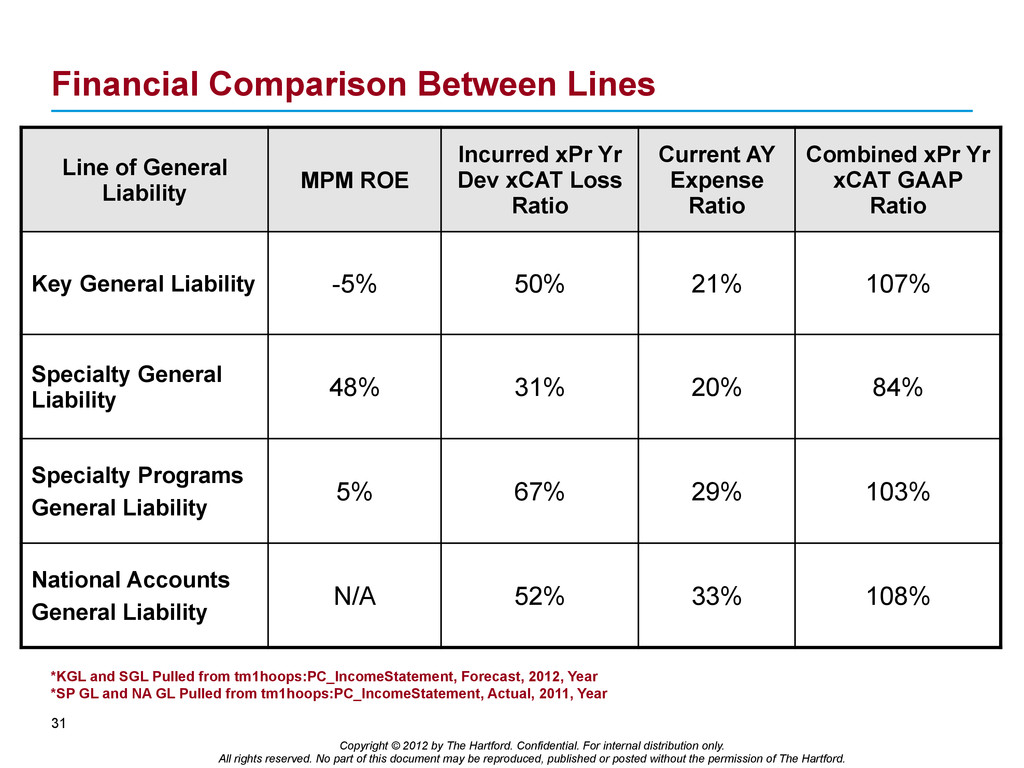

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 31 Financial Comparison Between Lines Line of General Liability MPM ROE Incurred xPr Yr Dev xCAT Loss Ratio Current AY Expense Ratio Combined xPr Yr xCAT GAAP Ratio Key General Liability -5% 50% 21% 107% Specialty General Liability 48% 31% 20% 84% Specialty Programs General Liability 5% 67% 29% 103% National Accounts General Liability N/A 52% 33% 108% *KGL and SGL Pulled from tm1hoops:PC_IncomeStatement, Forecast, 2012, Year *SP GL and NA GL Pulled from tm1hoops:PC_IncomeStatement, Actual, 2011, Year

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. SWOT Analysis 32 Specialty Programs Key GL Specialty GL National Accounts Strengths - Underwriters (dedicated, experiences, controlled) - Profitability - Marketing (brochures) - Program Customization - Flexibility - Centralized, which makes things more focused and efficient - 80% of GL accounts in MM - Low risk - Large target market, which means security for this line of business - Underwriters (specialized, experienced) - Loss Control - Claims handling - Communication (monthly meetings), which is a huge benefit to everyone - Strong Profit Margins - Program customization - Flexibility - ROE of 48% - Program Customization - Flexibility - Claims handling - Underwriters (Very experienced, because of the magnitude/importance of the accounts) -Total Revenue is 275M - Roughly 350 accounts Weaknesses - Underwriting guidelines - High hazard risk - Claim handling - No national presence - Loss Control - Referrals - Marketing - Reaction time - Agent awareness - Generalized - Marketing (focused on industry, not specific) - Underwriters (not specialized) - Claims handling - Communication - Pricing guidelines - Industry focused - High hazard risk - Claims handling - Reaction time - Marketing is difficult - GL in terms of their whole package - Communication - Pricing - Agent awareness - Marketing - Claims handling (overall message, claims cost) - Only about 160 accounts included GL Opportunities - Growing economy - Competition - Claims - Technology (quote online, social media) - Economic Recovery - Technology (social media) - Interactions between claims/underwriters -More user friendly website and information - Economic Recovery - Technology (social media) - Expanding SGL - Internet is a primary means of sparking interest in customers - Expanding GL (hired specialist) - Lower to mid hazard - Increase appetite and risk level - Account size Threats - Competition, willing to take on more risky accounts - The low risk - Claims department - Economy - Generalized - Competition - Pricing guidelines - Hard to differentiate - Niche market - Economy (interest rates) - Soft vs. Hard Market conditions - Competition - Target market

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 33 AVP Underwriter: Job Description • Experienced professional within insurance field, specifically focused in GL. • Responsible for: – Establishes a cohesive team environment where underwriters and claims handlers can collaborate and best support their customers – Responsible for the profitability of the GL product offerings across The Hartford – Hosts quarterly checkpoints between agents, underwriters and claim handlers to ensure communication and information sharing is present and effective – Responsible for overseeing and supporting cross functional training for underwriters, claim handlers, and agents on GL and best practices, at least annually – Provides and maintains additional training and resources via Share Point

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 34 VP & AVP Semi-Annual Meeting Agenda • Financial reporting on each segment • Client referrals • Target Market discussion • Best practices within segments Incorporate these practices within other segments if feasible • Discuss areas in need of improvement Brainstorm solutions to these problems • Product enhancements • Competitive analysis

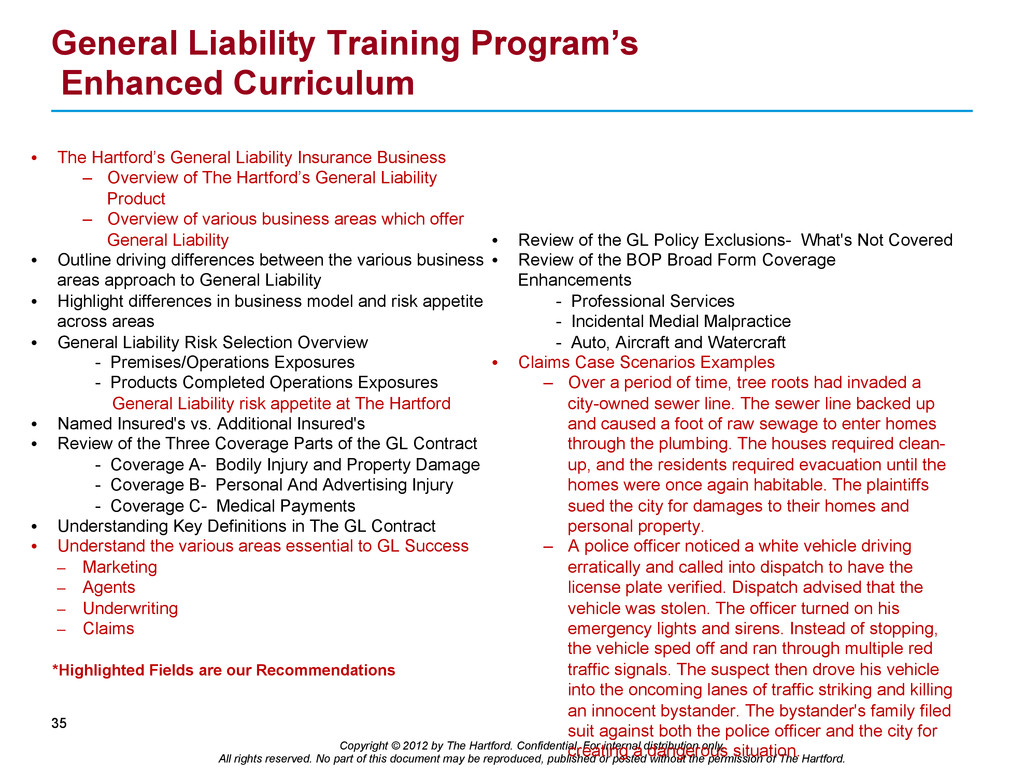

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 35 General Liability Training Program’s Enhanced Curriculum • The Hartford’s General Liability Insurance Business – Overview of The Hartford’s General Liability Product – Overview of various business areas which offer General Liability • Outline driving differences between the various business areas approach to General Liability • Highlight differences in business model and risk appetite across areas • General Liability Risk Selection Overview - Premises/Operations Exposures - Products Completed Operations Exposures General Liability risk appetite at The Hartford • Named Insured's vs. Additional Insured's • Review of the Three Coverage Parts of the GL Contract - Coverage A- Bodily Injury and Property Damage - Coverage B- Personal And Advertising Injury - Coverage C- Medical Payments • Understanding Key Definitions in The GL Contract • Understand the various areas essential to GL Success – Marketing – Agents – Underwriting – Claims • Review of the GL Policy Exclusions- What's Not Covered • Review of the BOP Broad Form Coverage Enhancements - Professional Services - Incidental Medial Malpractice - Auto, Aircraft and Watercraft • Claims Case Scenarios Examples – Over a period of time, tree roots had invaded a city-owned sewer line. The sewer line backed up and caused a foot of raw sewage to enter homes through the plumbing. The houses required clean- up, and the residents required evacuation until the homes were once again habitable. The plaintiffs sued the city for damages to their homes and personal property. – A police officer noticed a white vehicle driving erratically and called into dispatch to have the license plate verified. Dispatch advised that the vehicle was stolen. The officer turned on his emergency lights and sirens. Instead of stopping, the vehicle sped off and ran through multiple red traffic signals. The suspect then drove his vehicle into the oncoming lanes of traffic striking and killing an innocent bystander. The bystander's family filed suit against both the police officer and the city for creating a dangerous situation. 35 *Highlighted Fields are our Recommendations

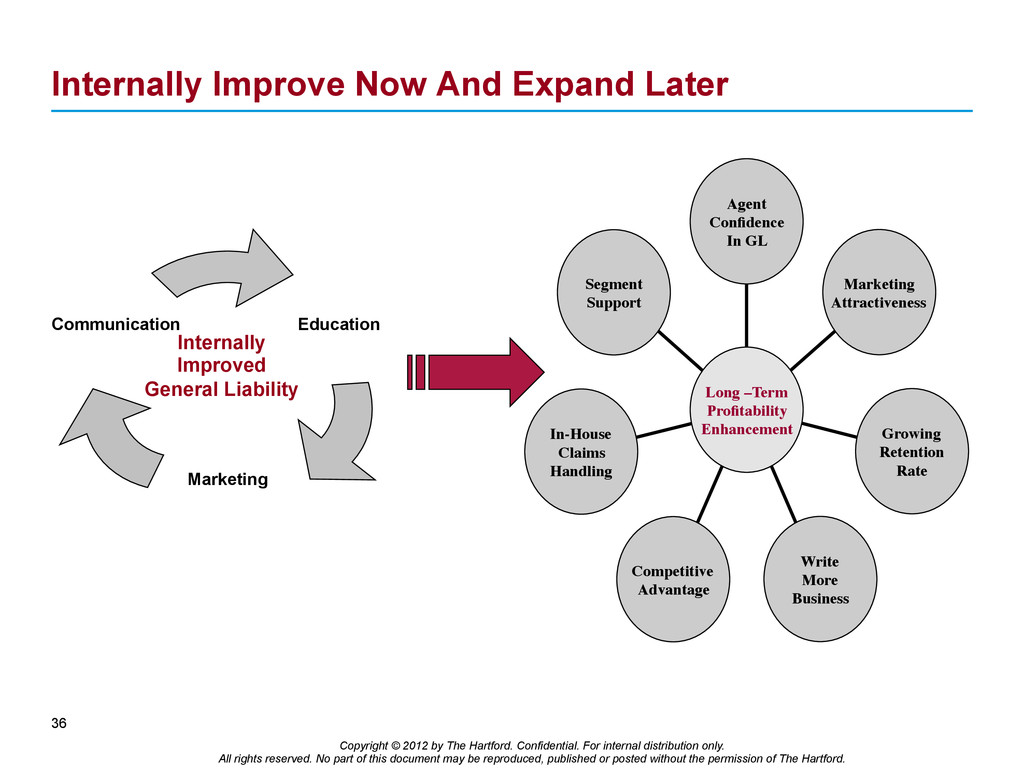

only. All rights reserved. No part of this document may be reproduced, published or posted without the permission of The Hartford. 36 Internally Improve Now And Expand Later Internally Improved General Liability Marketing Education Communication Segment Support In-House Claims Handling Competitive Advantage Write More Business Growing Retention Rate Marketing Attractiveness Agent Confidence In GL Long –Term Profitability Enhancement

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}