“Nearly half of 2026 [is] already on the books… alongside [an] unprecedented start to 2027 with record booking volumes during 3Q.” Carnival; Q3 Results – September 2025 Saga 2025-2026 Interim Results Statement – September 2025 “The trading of the Group for the period is ahead of expectations, with a strong performance in Travel… we have strong forward bookings for the second half of the year in both Ocean and River Cruises, and in Holidays we anticipate a further improvement in profitability driven by higher passenger numbers.”

sector On current trading for ‘Markets + Airline’ - “The UK shows positive momentum [for summer] with bookings up +1% whilst in Germany, bookings are at -5% reflecting our strategic focus on protecting margins. UK bookings are broadly in line with Winter 2024/25.” On the Beach Pre-Close Trading Update – September 2025 “It remains clear that customers are still prioritising their holidays with our Winter 25 bookings up 12% and we are confident that Summer 26 will continue to build, notwithstanding the later booking patterns.” Club Med H1 2025 Results – September 2025 “Club Med achieved a new record revenue in the first half of 2025, driven by strong activity throughout the period in a Company Business Volume of €1,175 million, up 4% year-on-year at constant exchange rates with positive growth in all regions.”

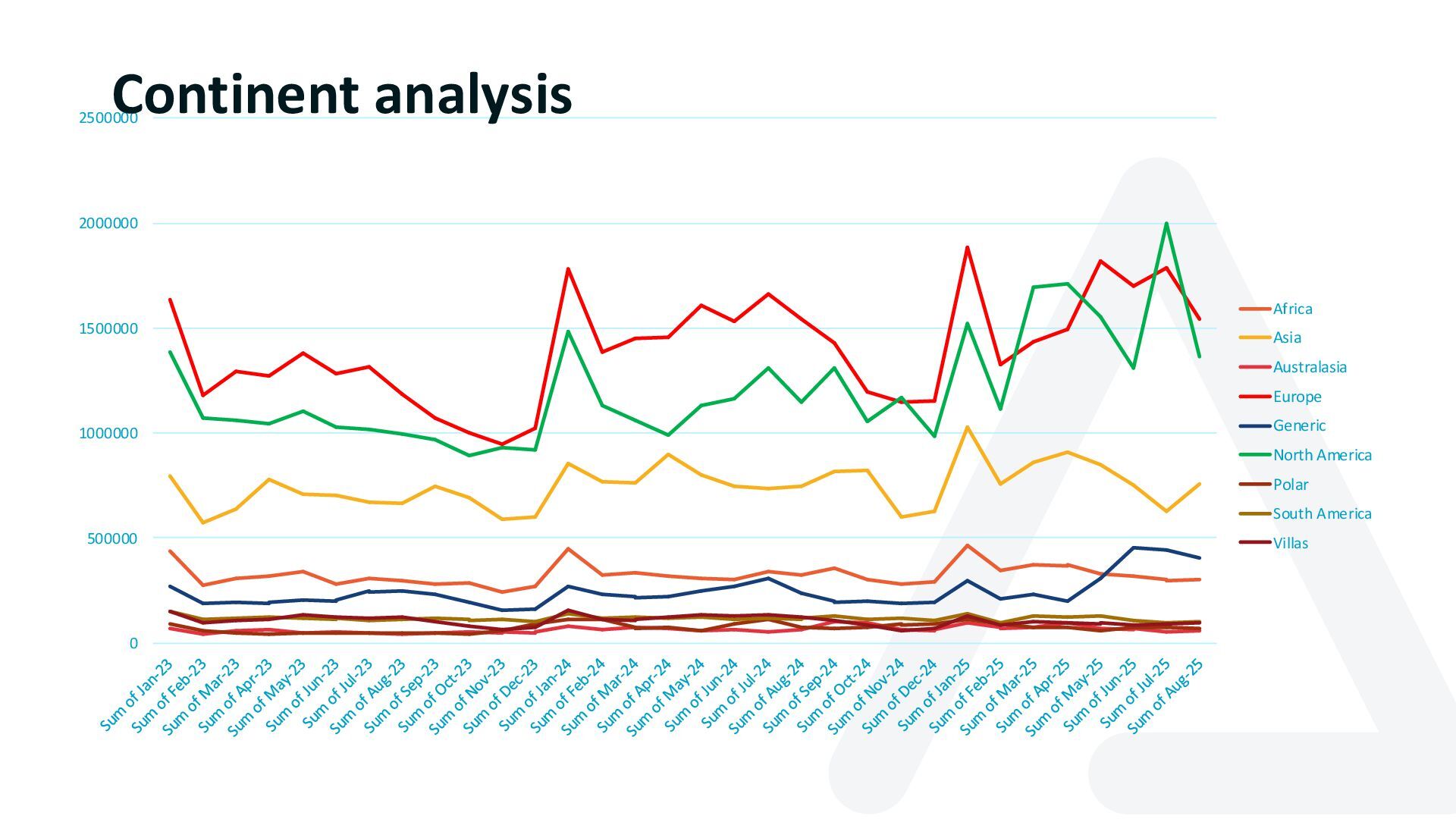

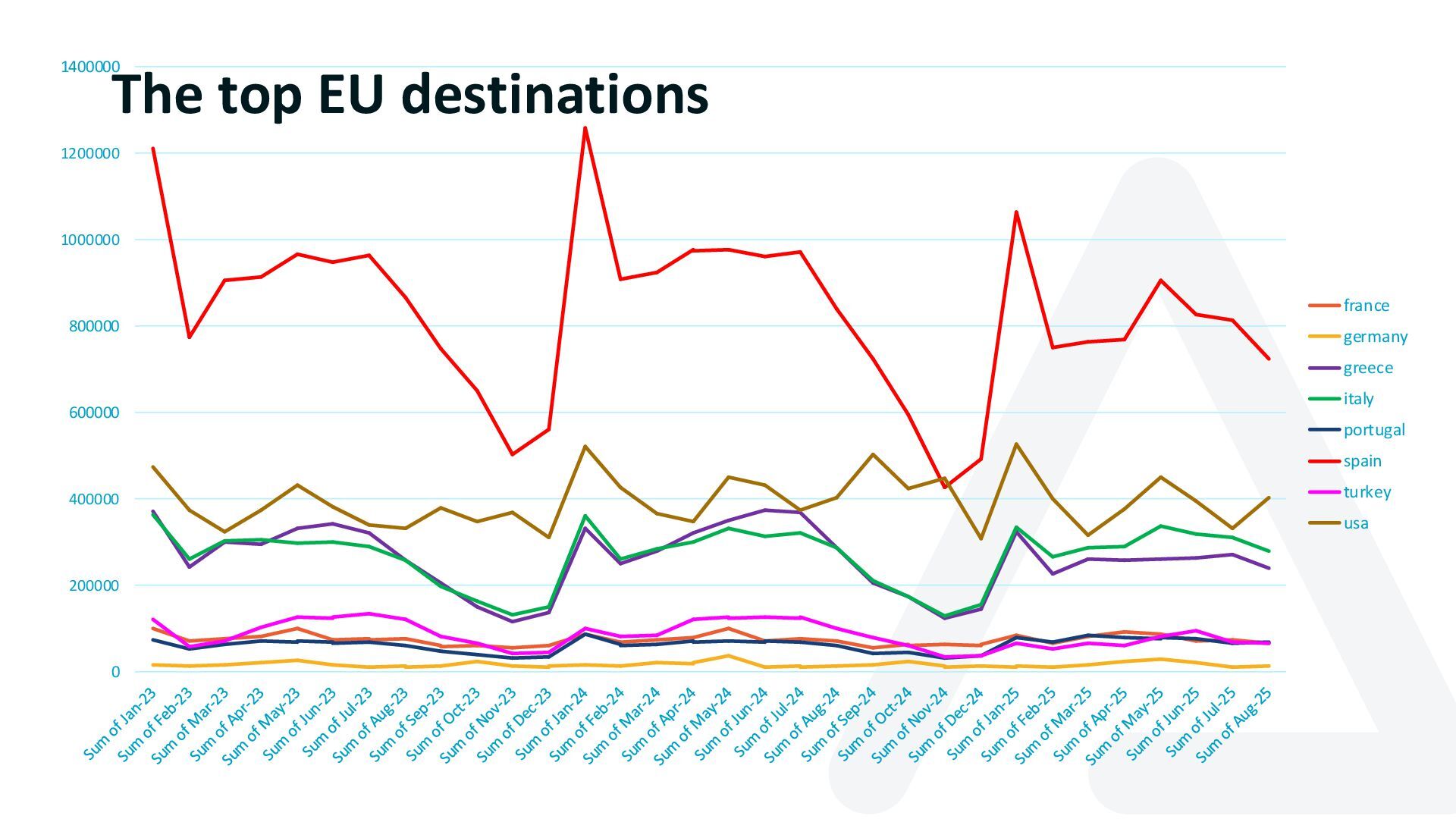

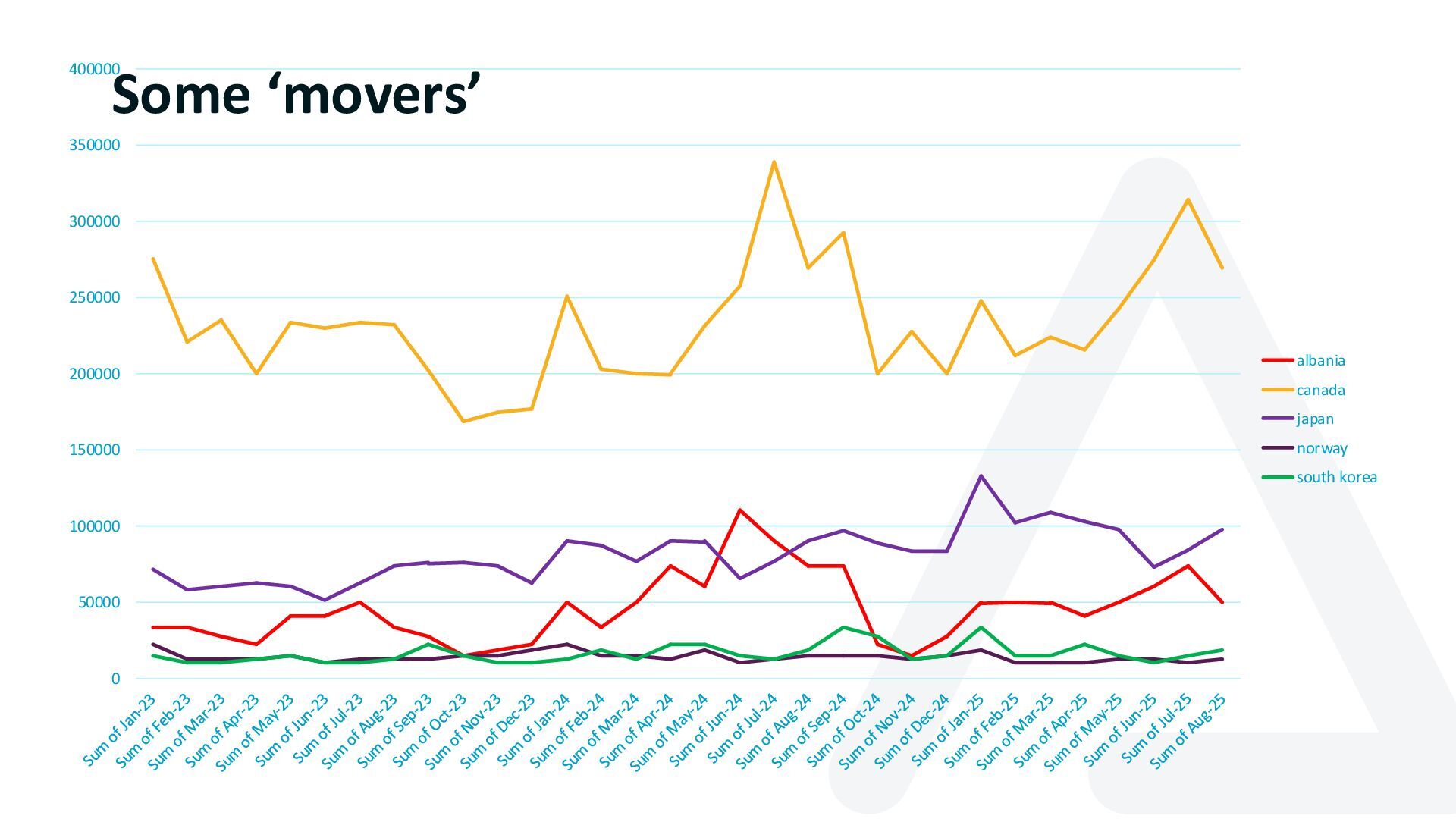

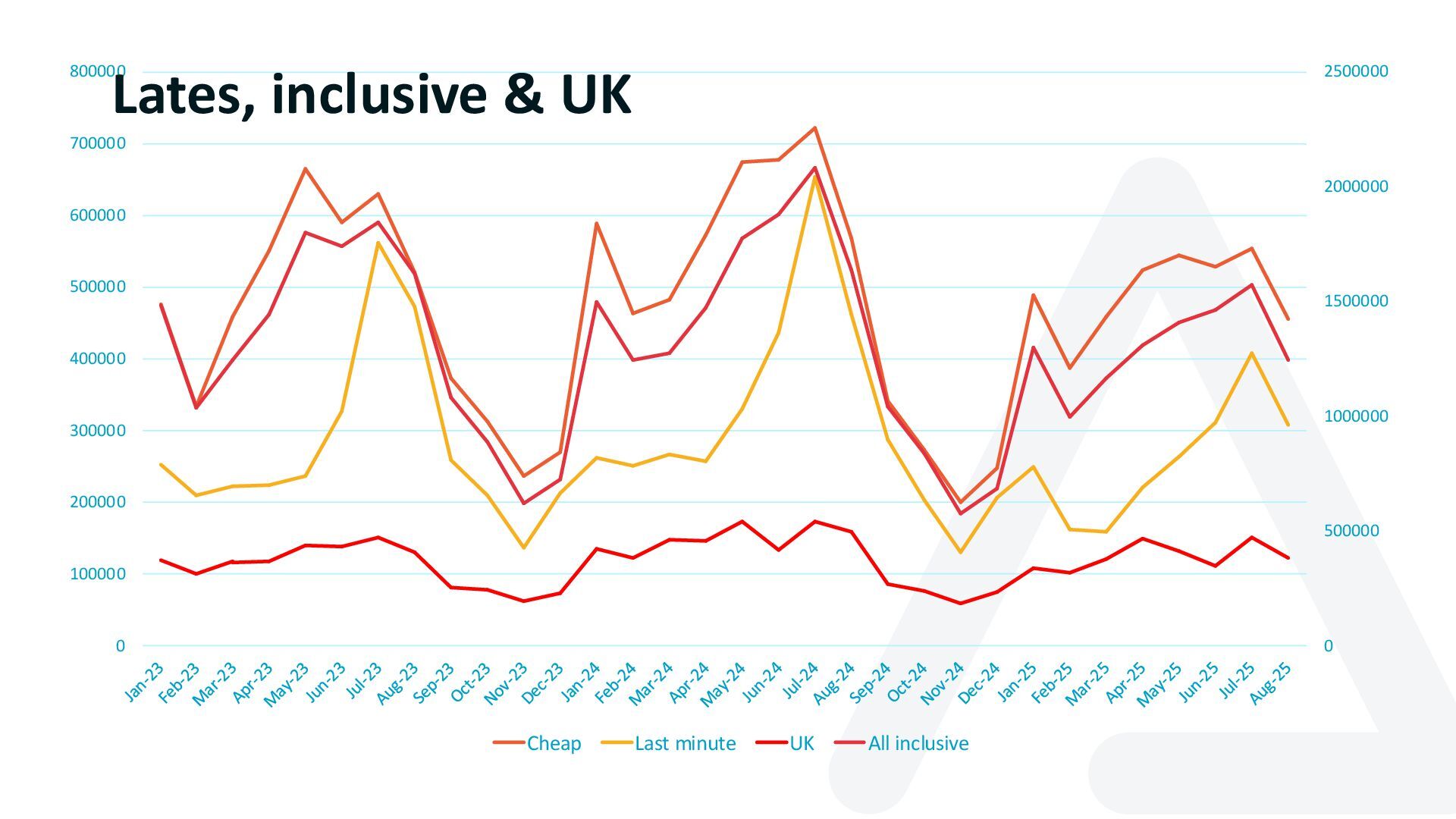

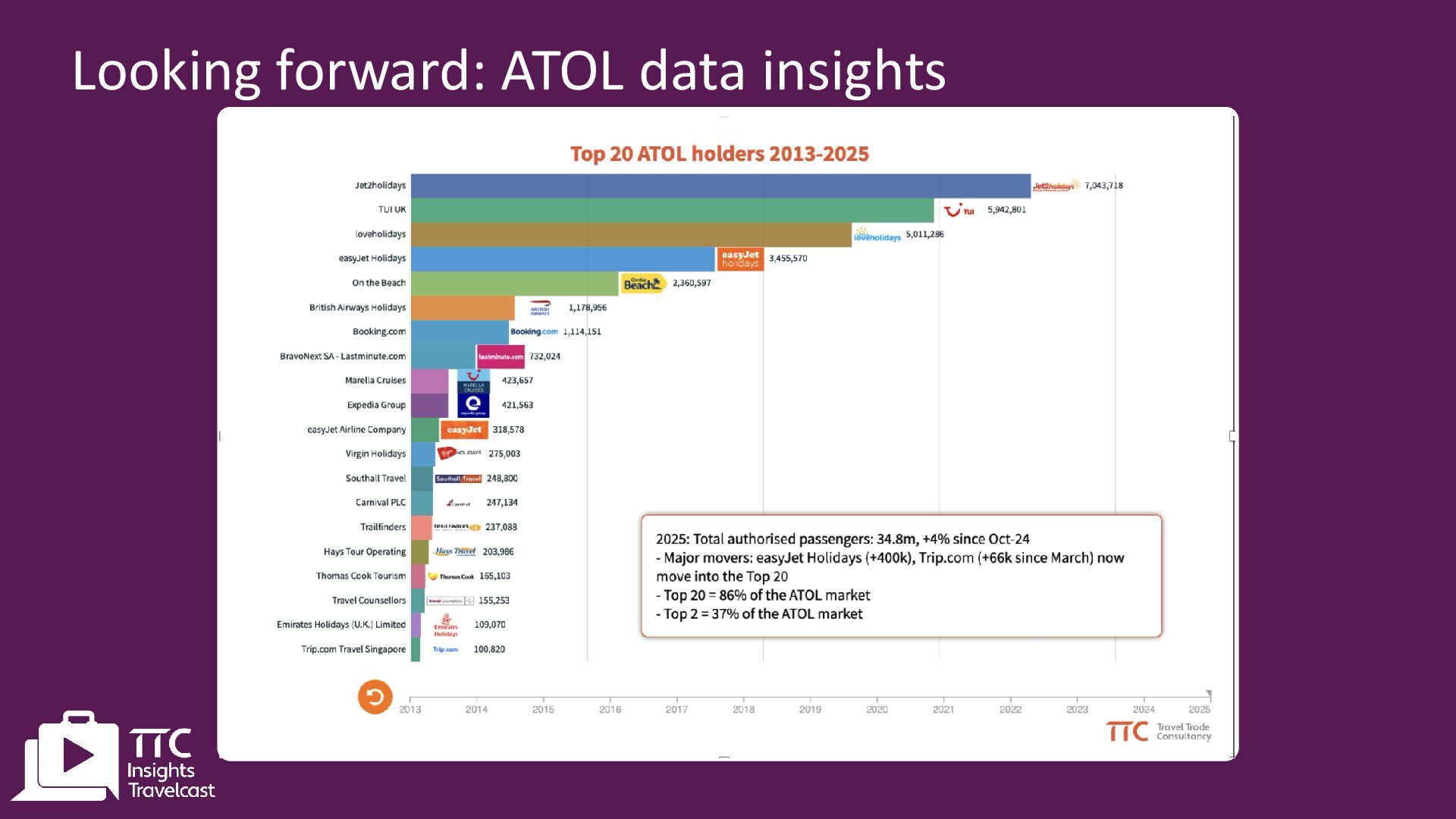

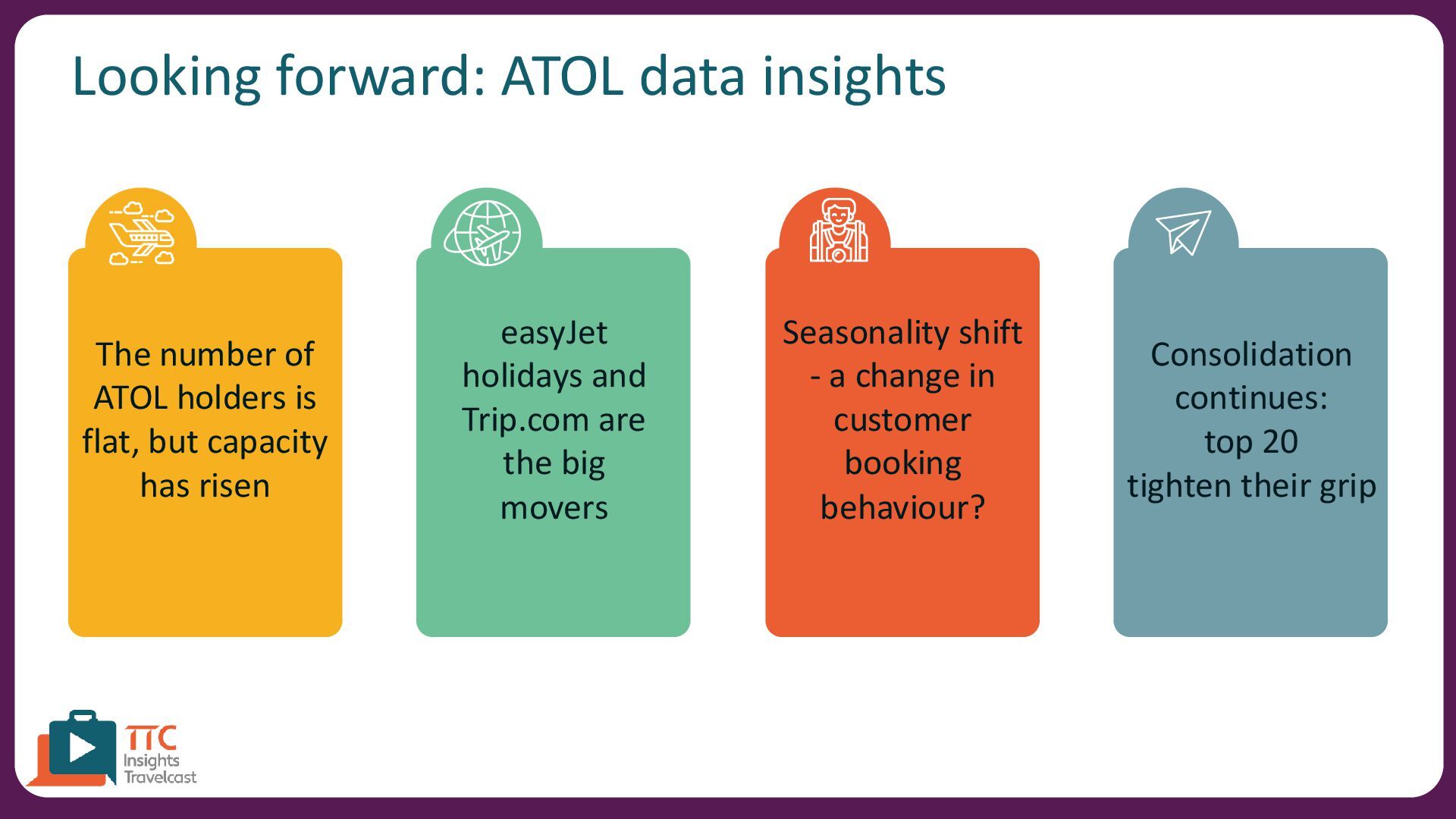

is flat, but capacity has risen easyJet holidays and Trip.com are the big movers Seasonality shift - a change in customer booking behaviour? Consolidation continues: top 20 tighten their grip

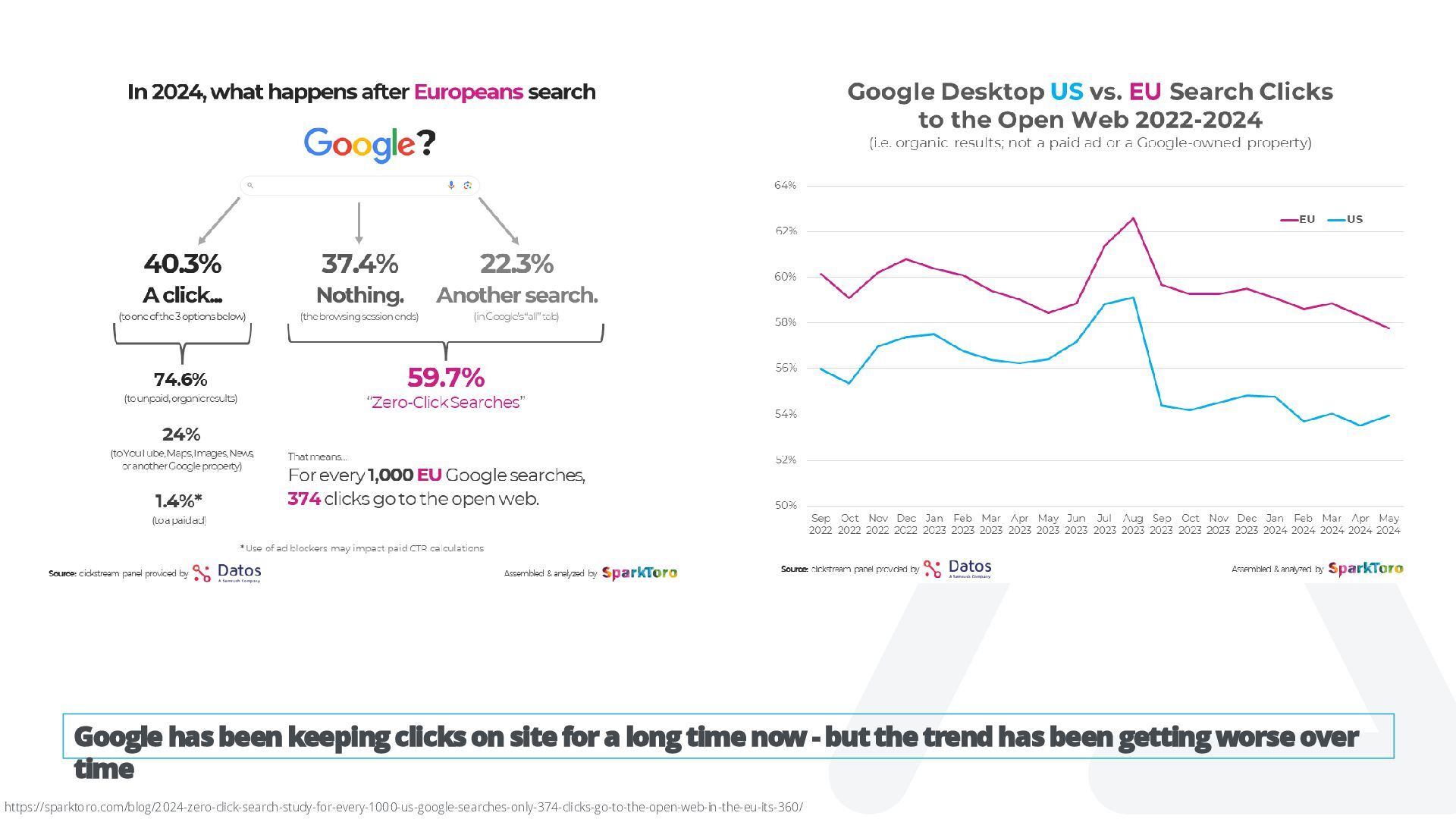

time now - but the trend has been getting worse over time https://sparktoro.com/blog/2024-zero-click-search-study-for-every-1000-us-google-searches-only-374-clicks-go-to-the-open-web-in-the-eu-its-360/

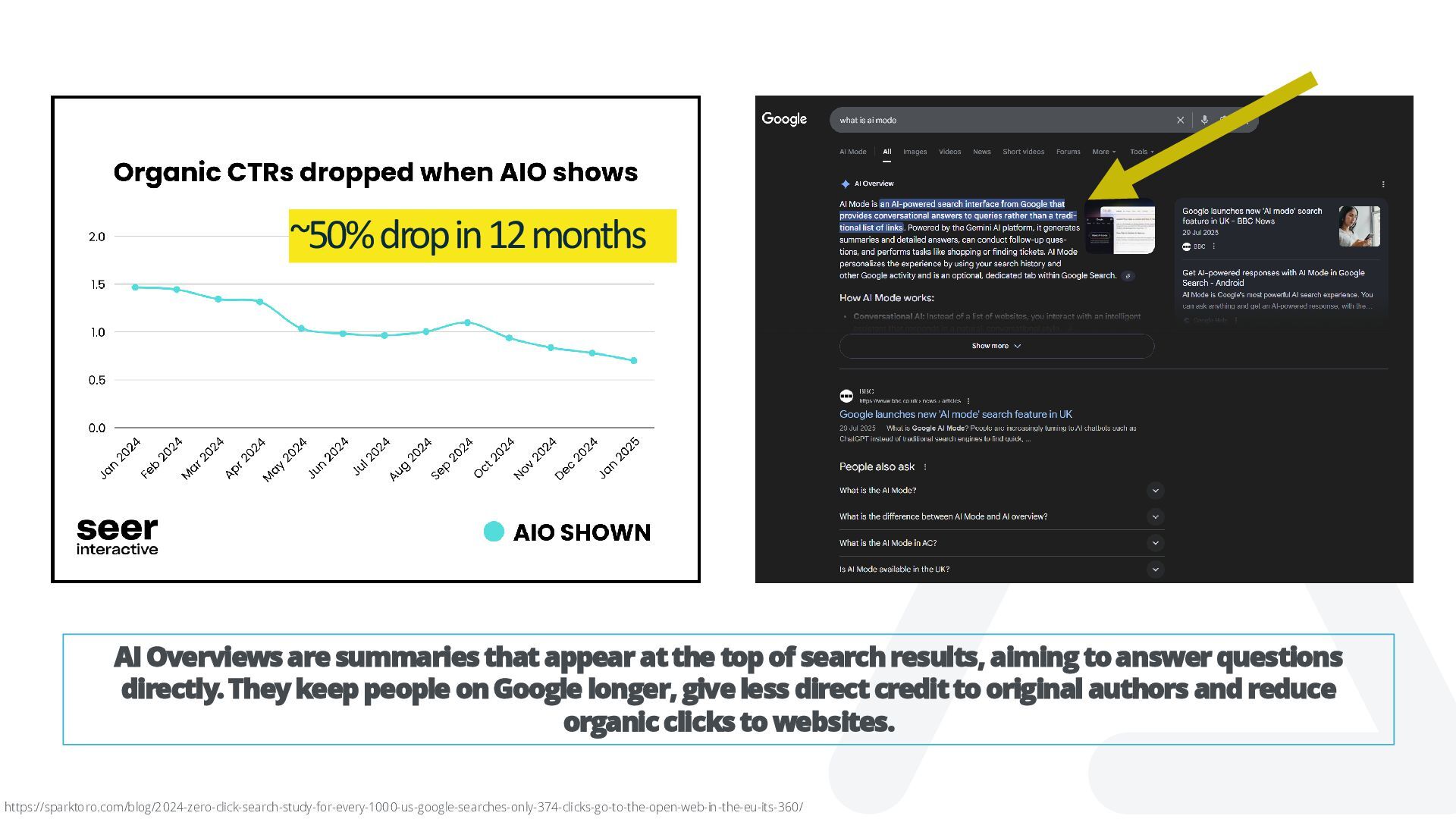

appear at the top of search results, aiming to answer questions directly. They keep people on Google longer, give less direct credit to original authors and reduce organic clicks to websites. https://sparktoro.com/blog/2024-zero-click-search-study-for-every-1000-us-google-searches-only-374-clicks-go-to-the-open-web-in-the-eu-its-360/

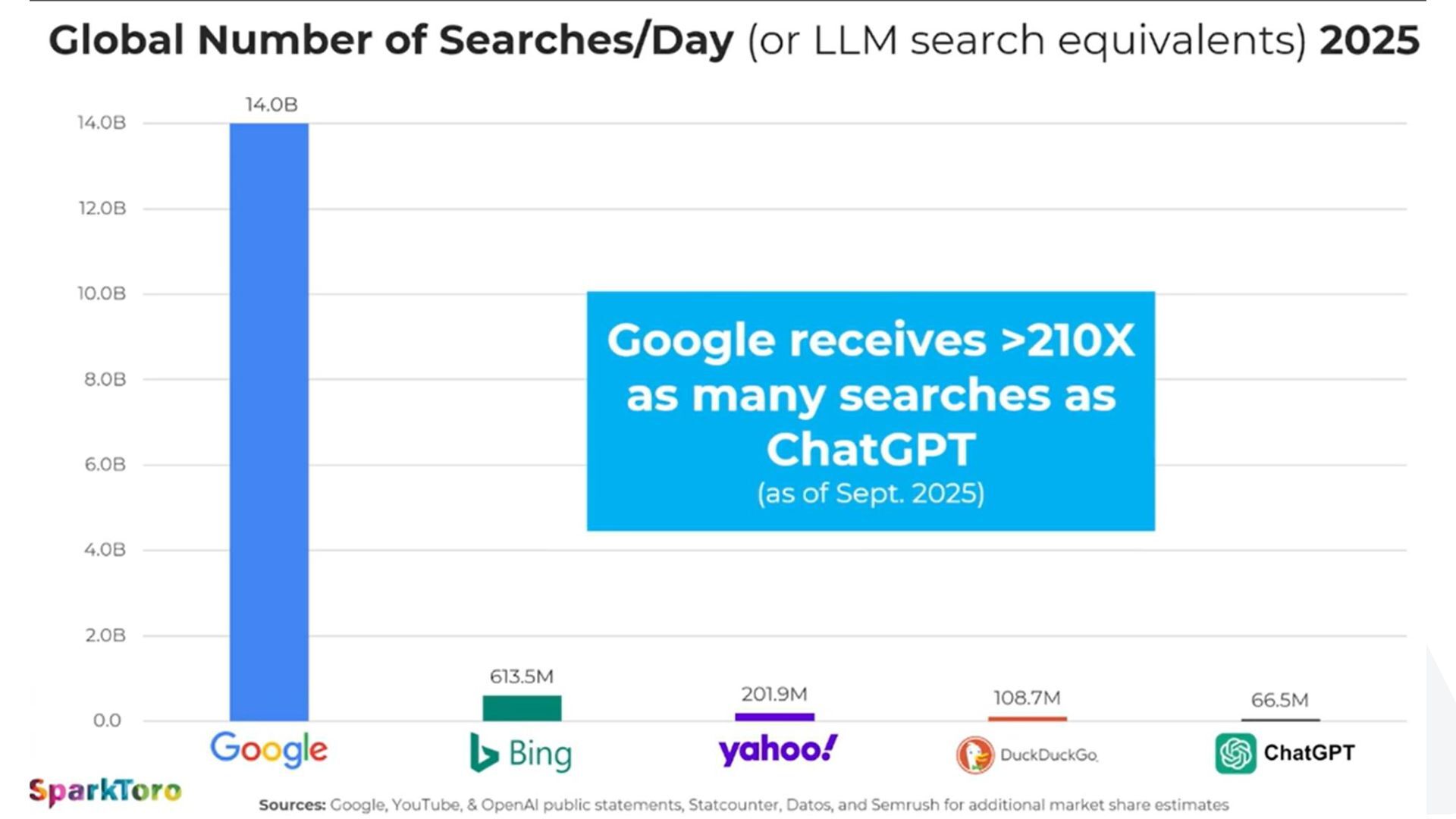

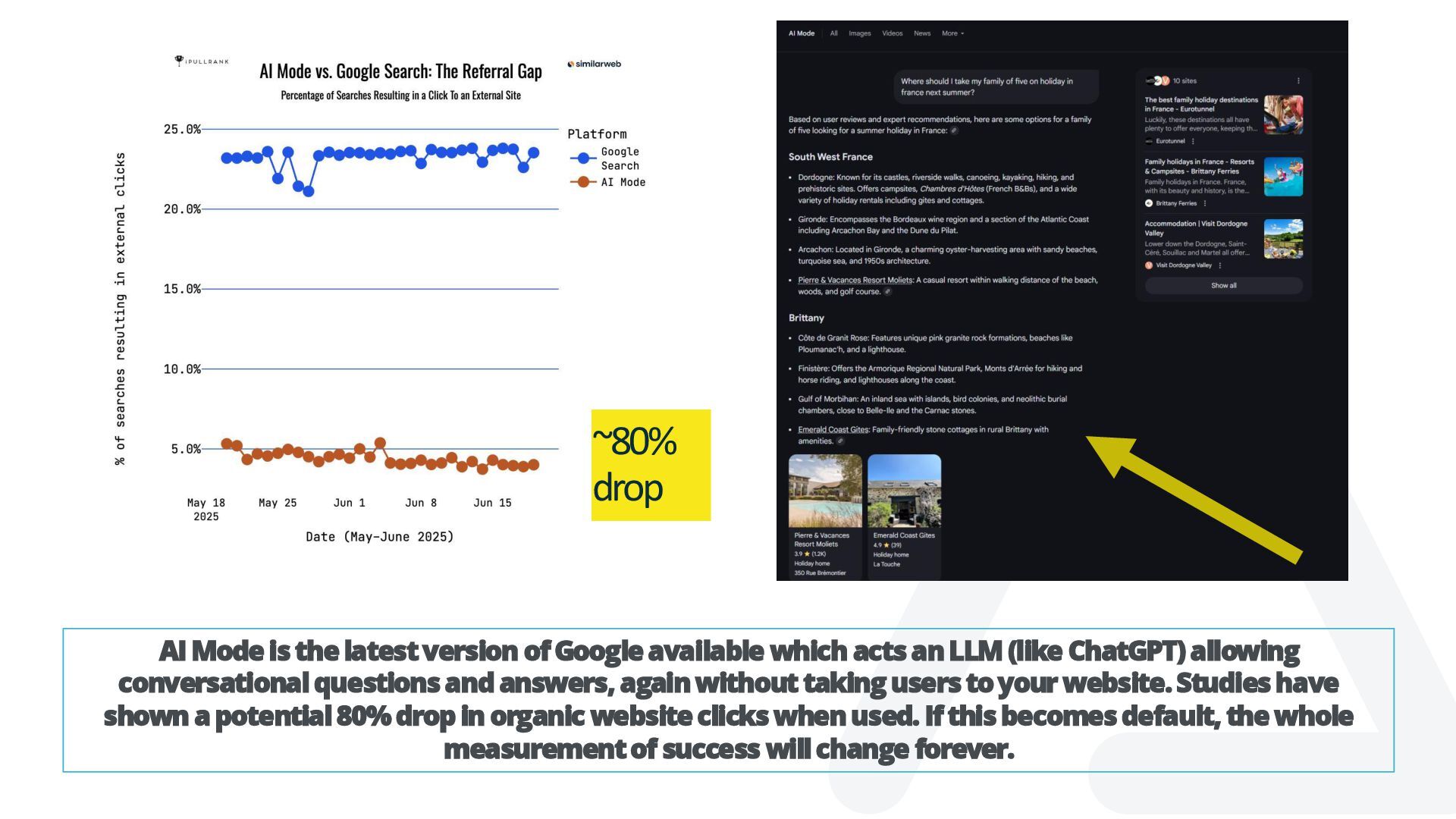

acts an LLM (like ChatGPT) allowing conversational questions and answers, again without taking users to your website. Studies have shown a potential 80% drop in organic website clicks when used. If this becomes default, the whole measurement of success will change forever. ~80% drop

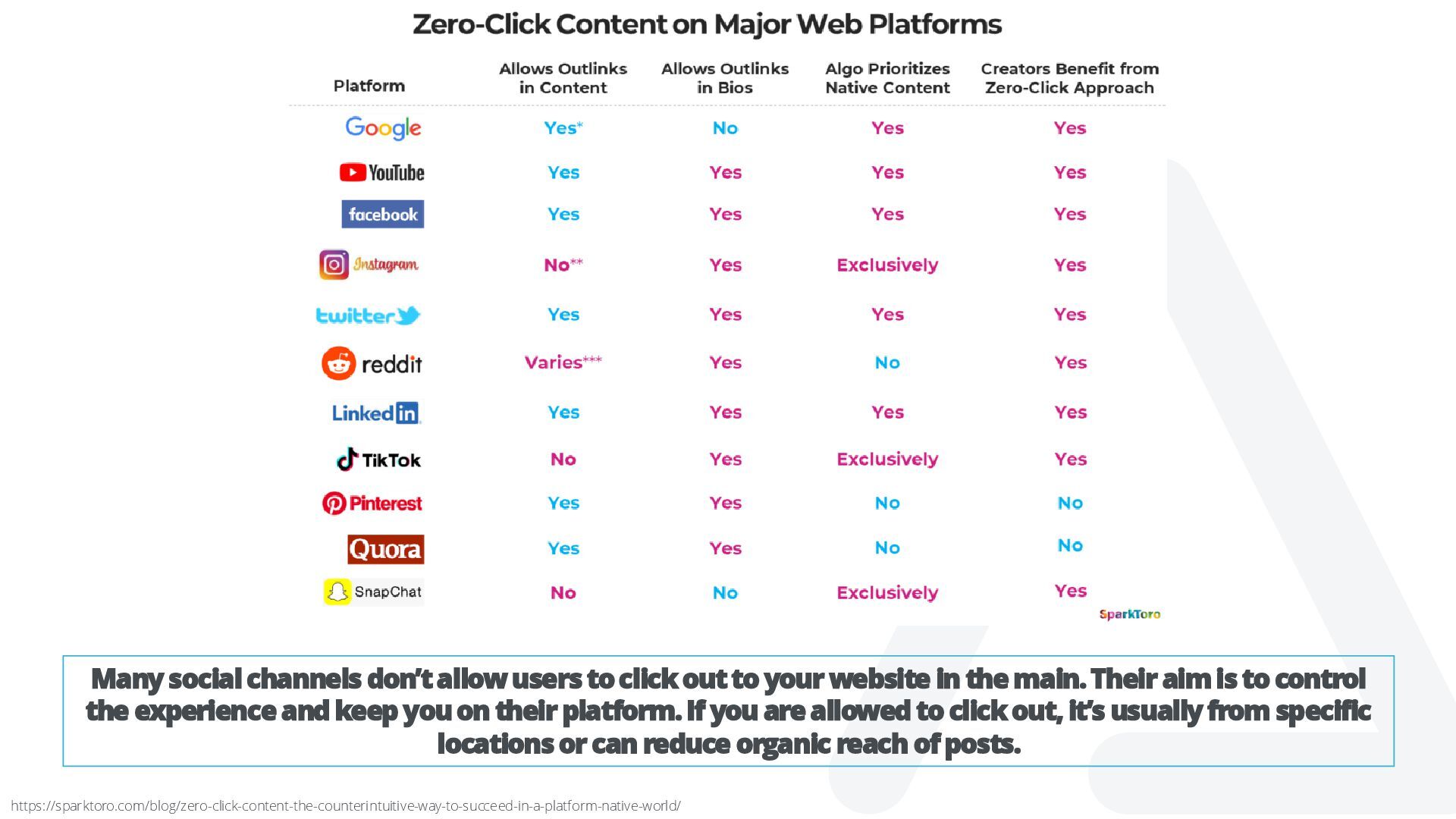

your website in the main. Their aim is to control the experience and keep you on their platform. If you are allowed to click out, it’s usually from specific locations or can reduce organic reach of posts. https://sparktoro.com/blog/zero-click-content-the-counterintuitive-way-to-succeed-in-a-platform-native-world/

In 2026 your website traffic WILL drop. There is no way of getting this back. You need to adapt your measurement and reporting approach going forward. Brand mentions, visibility on social and traditional rank tracking all need to form part of your measurement metrics.

{kind=link}

![Today’s presenters Martin Alcock Director, TTC [email protected] Simon Brodie Director,](https://files.speakerdeck.com/presentations/51b6fa416b7346a29bc3986864708acb/slide_1.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Today’s presenters Martin Alcock Director, TTC [email protected] Simon Brodie Director,](https://files.speakerdeck.com/presentations/51b6fa416b7346a29bc3986864708acb/slide_38.jpg){kind=link}

{kind=link}