Presented at:

Bank of Italy, Rome, June 21, 2016

European Banking Federation, Bruxelles, July 7, 2016

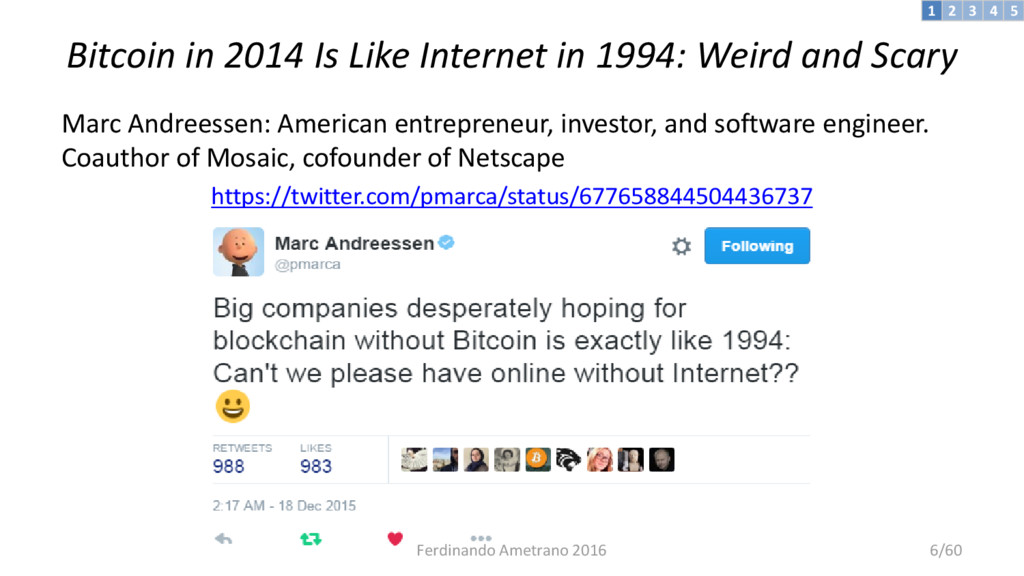

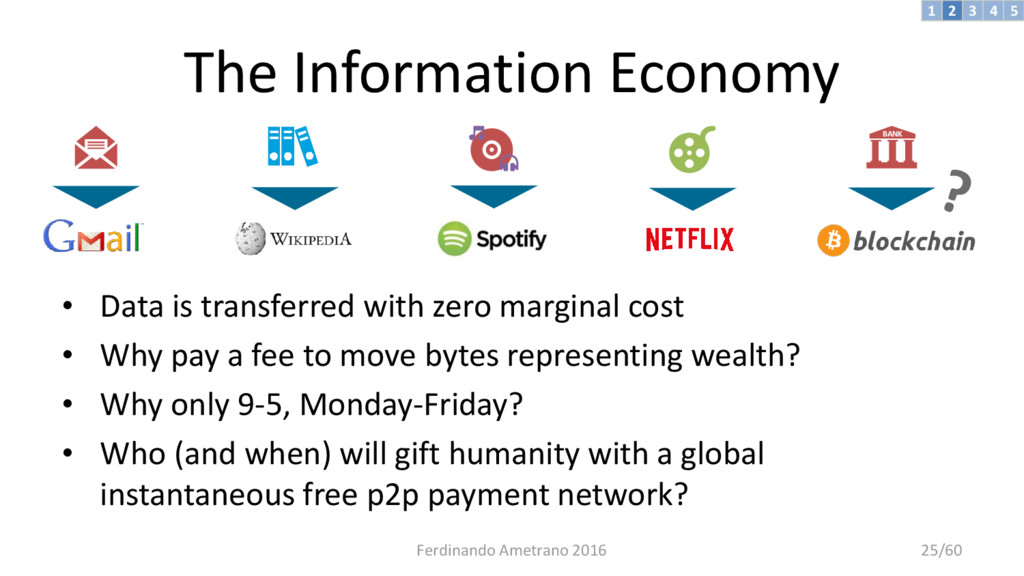

Understanding of blockchain technology lags well behind the hype. Notably, the need of a native digital asset such as bitcoin is neglected, the brilliance of distributed consensus is obfuscated, and fuzzy distributed ledgers are advocated instead.

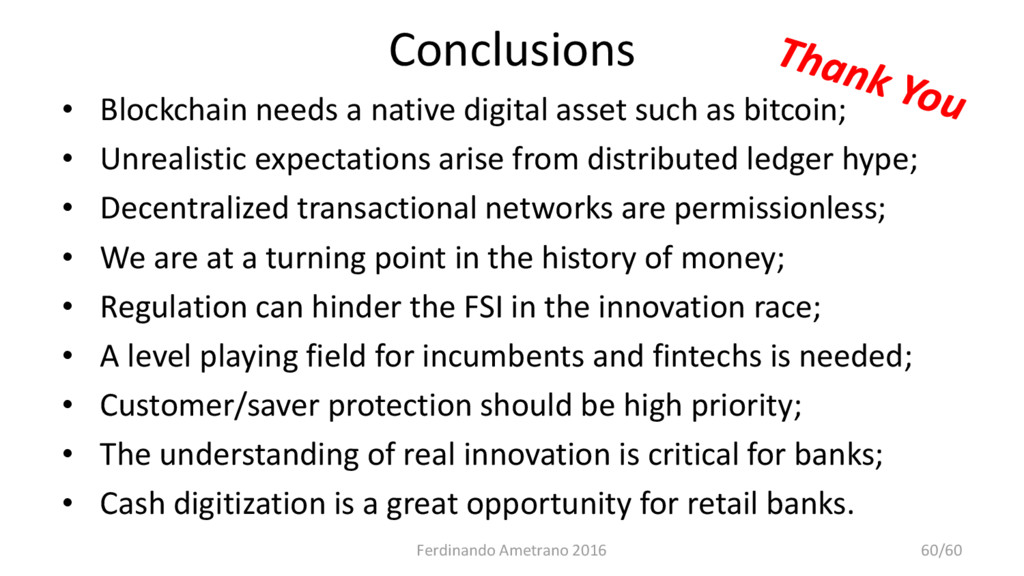

In this presentation the following conclusions are offered:

* Blockchain needs a native digital asset such as bitcoin;

* Unrealistic expectations arise from distributed ledger hype;

* Decentralized transactional networks are permissionless;

* We are at a turning point in the history of money;

* Regulation can hinder the Financial Service Industry in the innovation race;

* A level playing field for incumbents and fintechs is needed;

* Customer/saver protection should be high priority;

* The understanding of real innovation is critical for banks;

* Cash digitization is a great opportunity for retail banks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}