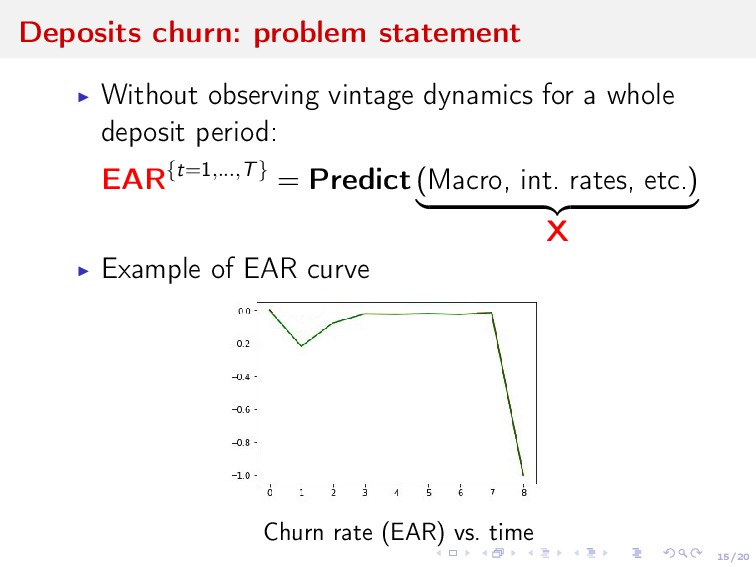

risks ⇒ long-term forecasting Net Revenue from Acquiring Deposits Churn Vintage economic units grouped by some categorical characteristics and united by time interval

risks ⇒ long-term forecasting Net Revenue from Acquiring Deposits Churn Vintage economic units grouped by some categorical characteristics and united by time interval Forecast the value of the vintage, or the sum w.r.t. some vintages

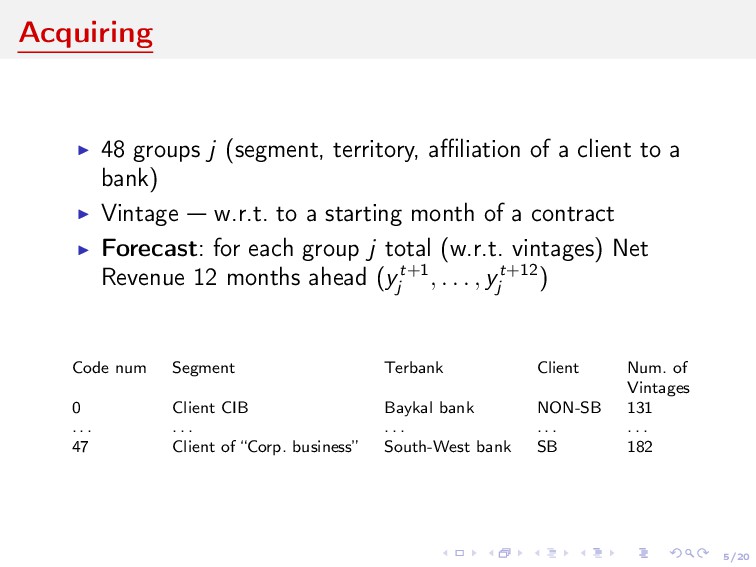

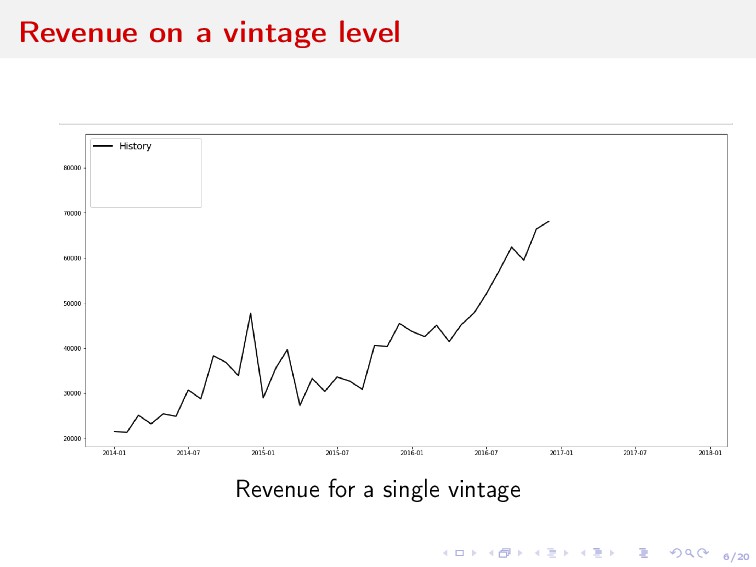

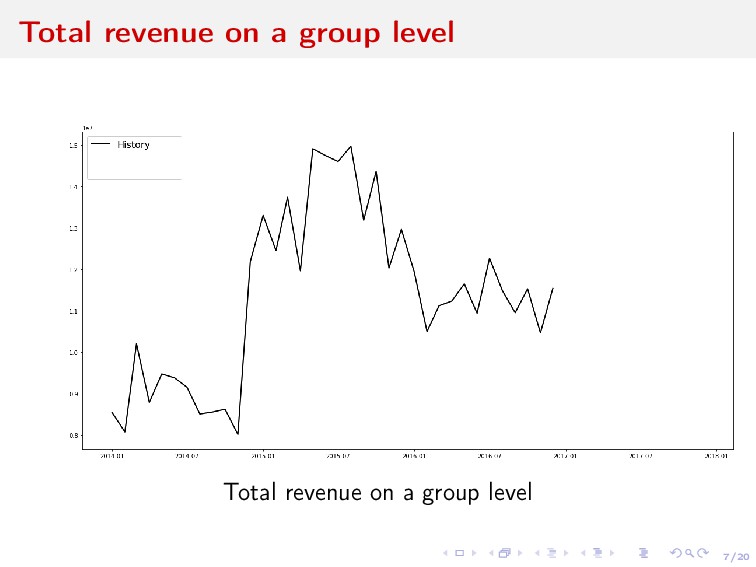

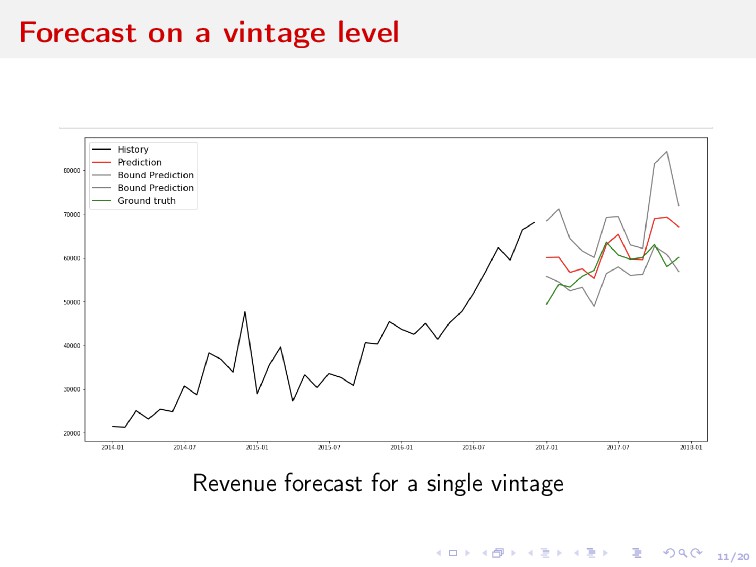

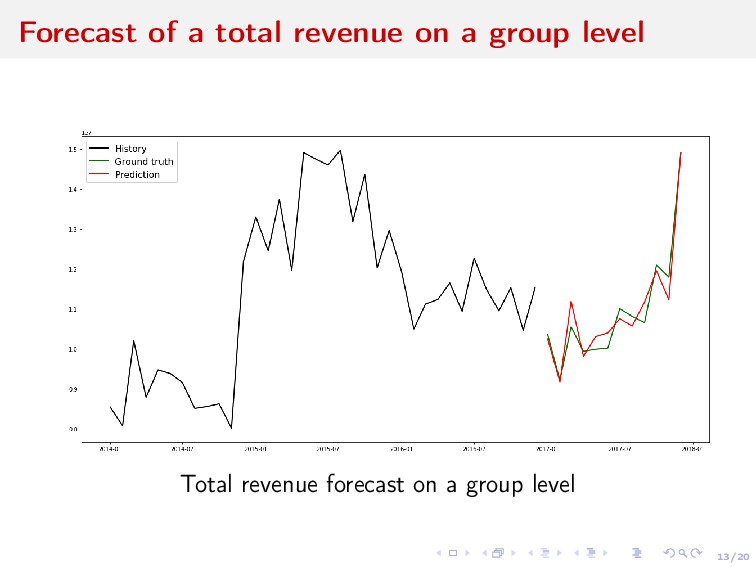

client to a bank) Vintage w.r.t. to a starting month of a contract Forecast: for each group j total (w.r.t. vintages) Net Revenue 12 months ahead (yt+1 j , . . . , yt+12 j ) Code num Segment Terbank Client Num. of Vintages 0 Client CIB Baykal bank NON-SB 131 . . . . . . . . . . . . . . . 47 Client of “Corp. business” South-West bank SB 182

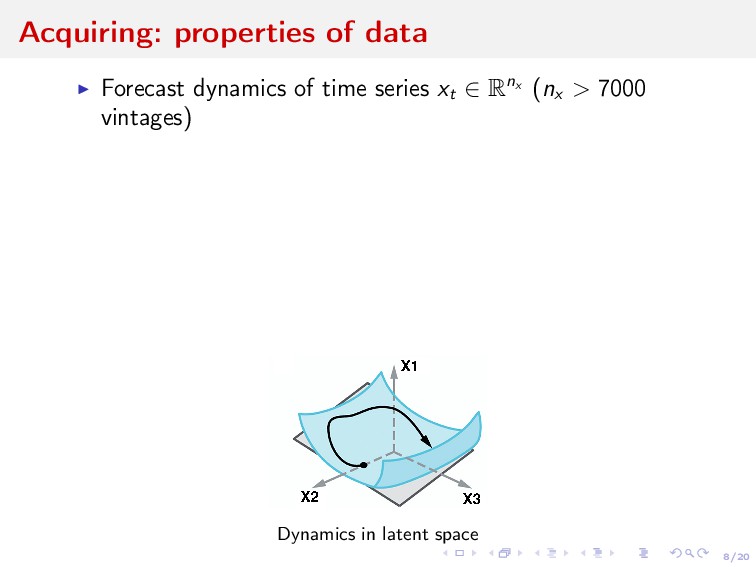

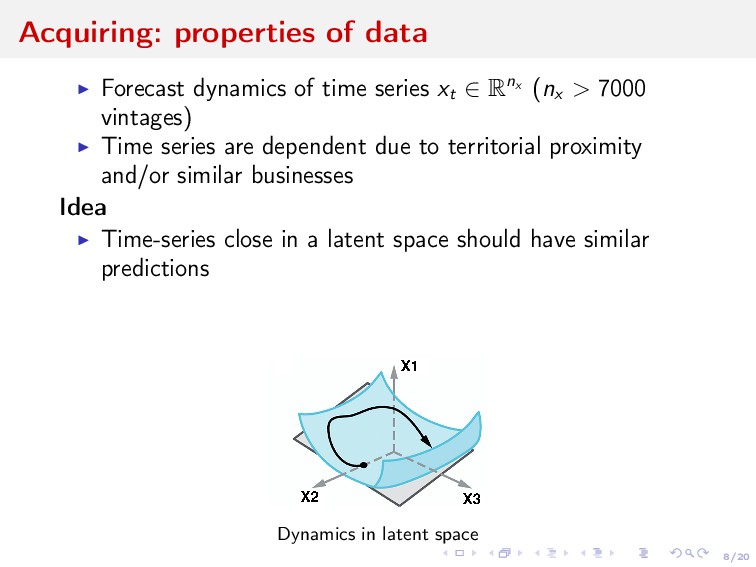

xt ∈ Rnx (nx > 7000 vintages) Time series are dependent due to territorial proximity and/or similar businesses Idea Time-series close in a latent space should have similar predictions Dynamics in latent space

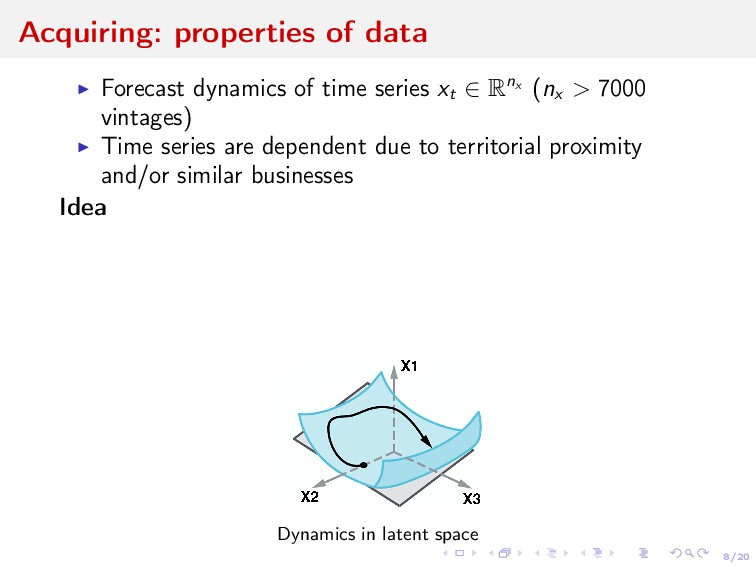

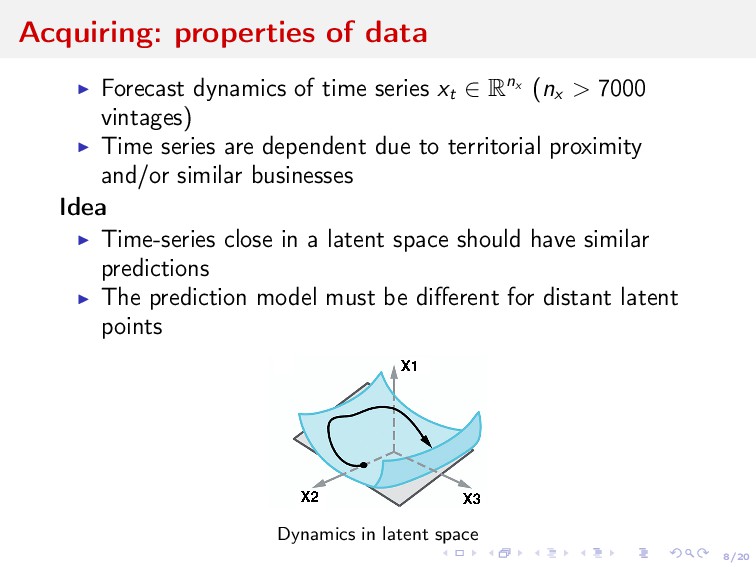

xt ∈ Rnx (nx > 7000 vintages) Time series are dependent due to territorial proximity and/or similar businesses Idea Time-series close in a latent space should have similar predictions The prediction model must be different for distant latent points Dynamics in latent space

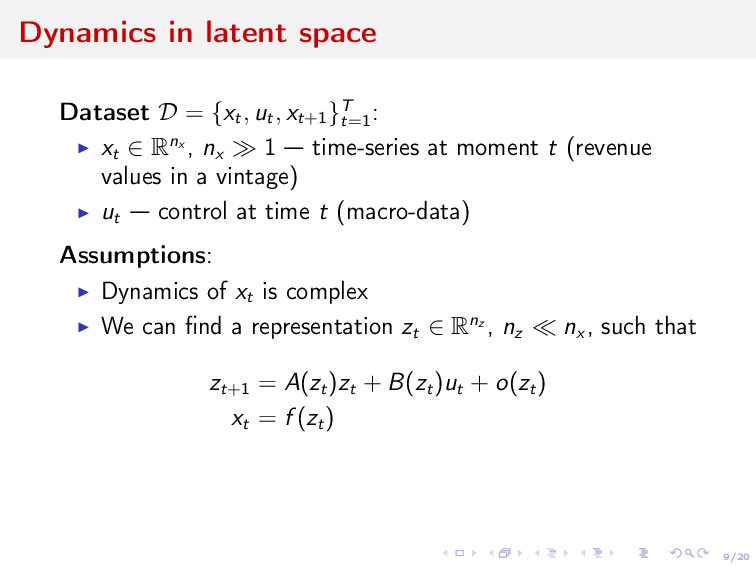

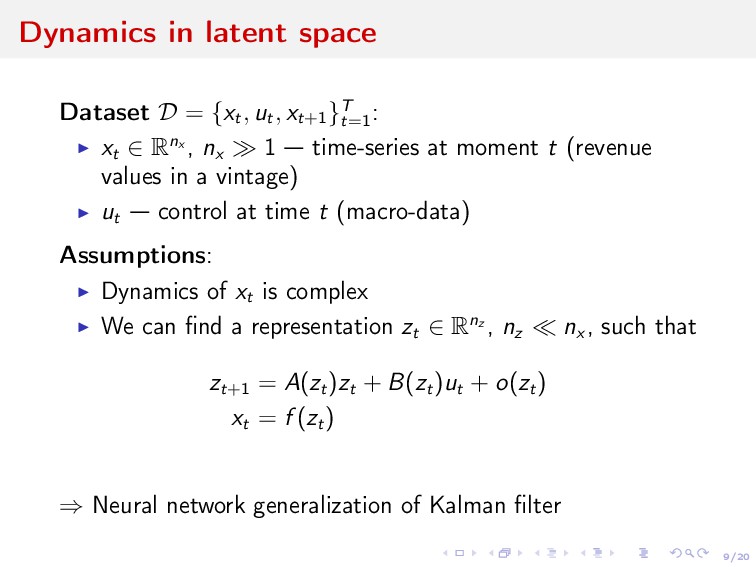

ut , xt+1 }T t=1 : xt ∈ Rnx , nx 1 time-series at moment t (revenue values in a vintage) ut control at time t (macro-data) Assumptions: Dynamics of xt is complex

ut , xt+1 }T t=1 : xt ∈ Rnx , nx 1 time-series at moment t (revenue values in a vintage) ut control at time t (macro-data) Assumptions: Dynamics of xt is complex We can find a representation zt ∈ Rnz , nz nx , such that

ut , xt+1 }T t=1 : xt ∈ Rnx , nx 1 time-series at moment t (revenue values in a vintage) ut control at time t (macro-data) Assumptions: Dynamics of xt is complex We can find a representation zt ∈ Rnz , nz nx , such that zt+1 = A(zt )zt + B(zt )ut + o(zt ) xt = f (zt )

ut , xt+1 }T t=1 : xt ∈ Rnx , nx 1 time-series at moment t (revenue values in a vintage) ut control at time t (macro-data) Assumptions: Dynamics of xt is complex We can find a representation zt ∈ Rnz , nz nx , such that zt+1 = A(zt )zt + B(zt )ut + o(zt ) xt = f (zt ) ⇒ Neural network generalization of Kalman filter

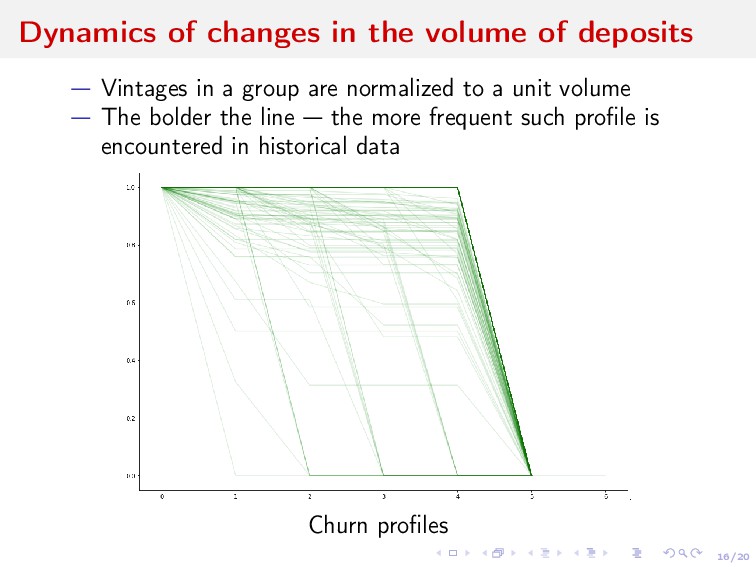

a level of vintages Vintage deposits with the same characteristics (vintage code): Date of opening of a Deposit Deposit currency, term of Deposit Segment of a deposit, sales channel, volume, etc. Has a deposit been prolonged?

a level of vintages Vintage deposits with the same characteristics (vintage code): Date of opening of a Deposit Deposit currency, term of Deposit Segment of a deposit, sales channel, volume, etc. Has a deposit been prolonged? Forecast monthly change in a vintage volume (churn rate) EARt = V t adj − V t−1 adj V t−1 adj ∈ [−1; 0], t ∈ {1, . . . , T}

a level of vintages Vintage deposits with the same characteristics (vintage code): Date of opening of a Deposit Deposit currency, term of Deposit Segment of a deposit, sales channel, volume, etc. Has a deposit been prolonged? Forecast monthly change in a vintage volume (churn rate) EARt = V t adj − V t−1 adj V t−1 adj ∈ [−1; 0], t ∈ {1, . . . , T} In total 103932 vintages, and we have only 48 time-series points

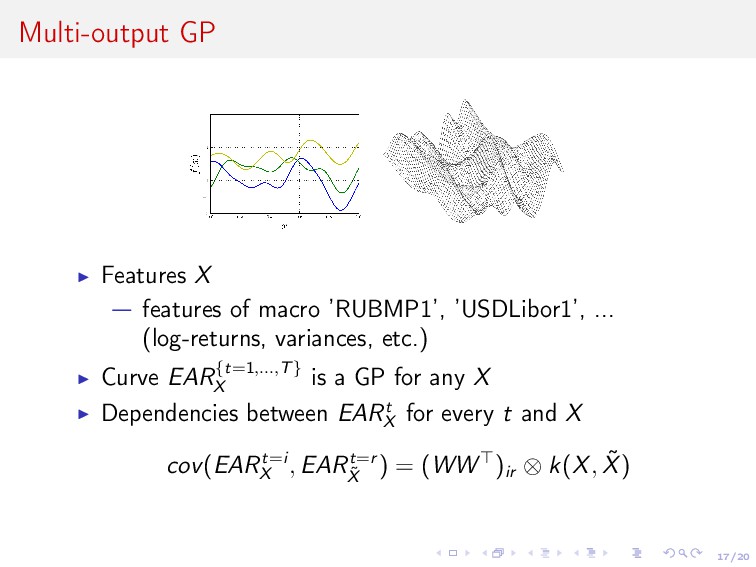

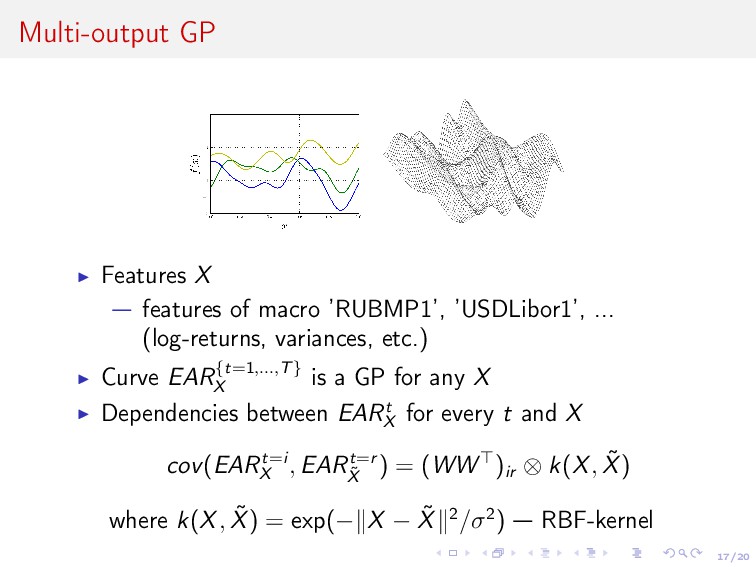

... (log-returns, variances, etc.) Curve EAR{t=1,...,T} X is a GP for any X Dependencies between EARt X for every t and X cov(EARt=i X , EARt=r ˜ X ) = (WW )ir ⊗ k(X, ˜ X)

... (log-returns, variances, etc.) Curve EAR{t=1,...,T} X is a GP for any X Dependencies between EARt X for every t and X cov(EARt=i X , EARt=r ˜ X ) = (WW )ir ⊗ k(X, ˜ X) where k(X, ˜ X) = exp(− X − ˜ X 2/σ2) RBF-kernel

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}