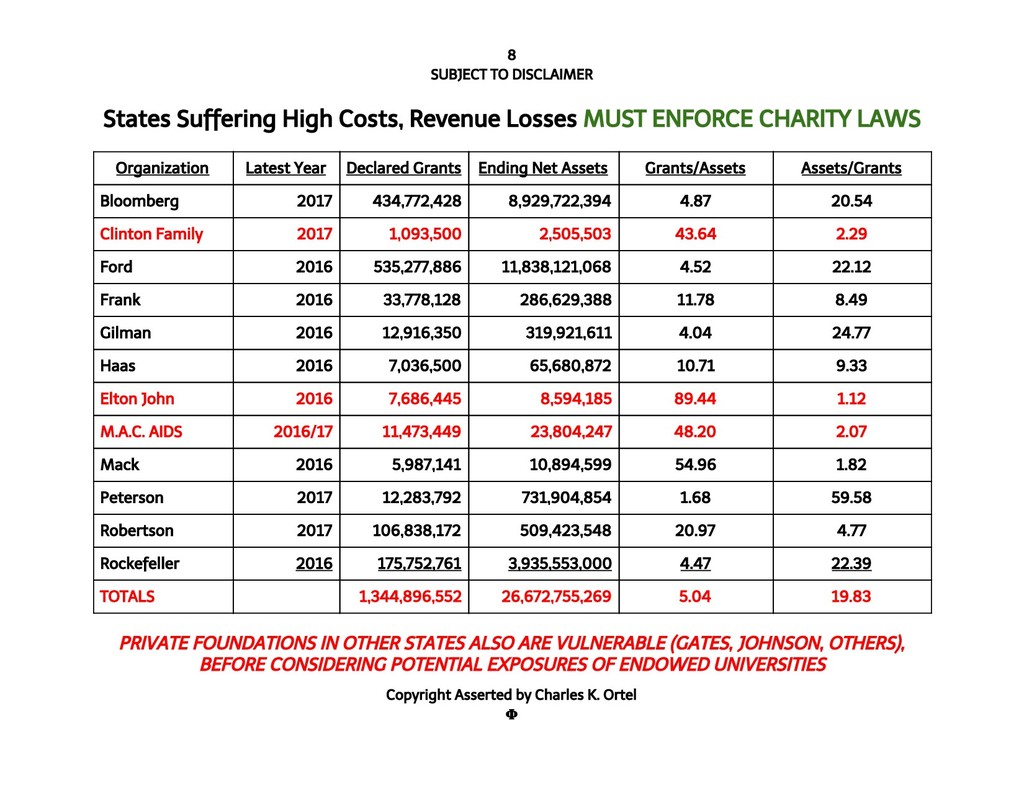

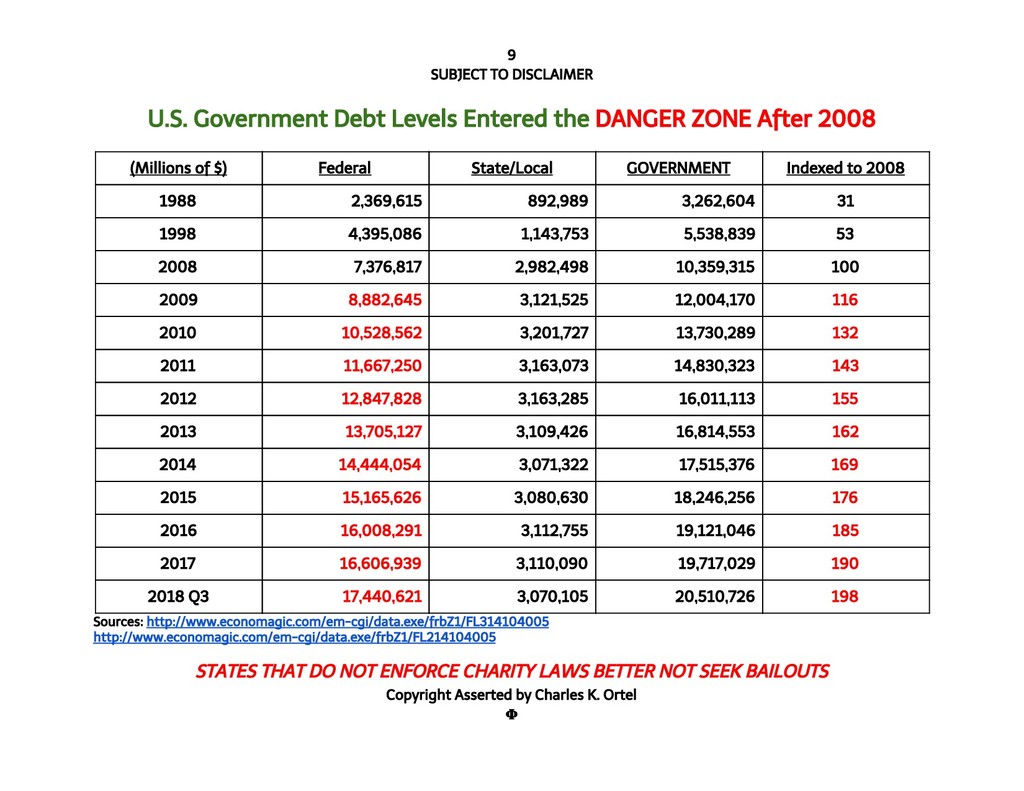

DANGER ZONE After 2008 (Millions of $) Federal State/Local GOVERNMENT Indexed to 2008 1988 2,369,615 892,989 3,262,604 31 1998 4,395,086 1,143,753 5,538,839 53 2008 7,376,817 2,982,498 10,359,315 100 2009 8,882,645 3,121,525 12,004,170 116 2010 10,528,562 3,201,727 13,730,289 132 2011 11,667,250 3,163,073 14,830,323 143 2012 12,847,828 3,163,285 16,011,113 155 2013 13,705,127 3,109,426 16,814,553 162 2014 14,444,054 3,071,322 17,515,376 169 2015 15,165,626 3,080,630 18,246,256 176 2016 16,008,291 3,112,755 19,121,046 185 2017 16,606,939 3,110,090 19,717,029 190 2018 Q3 17,440,621 3,070,105 20,510,726 198 Sources: http://www.economagic.com/em-cgi/data.exe/frbZ1/FL314104005 http://www.economagic.com/em-cgi/data.exe/frbZ1/FL214104005 STATES THAT DO NOT ENFORCE CHARITY LAWS BETTER NOT SEEK BAILOUTS Copyright Asserted by Charles K. Ortel

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}