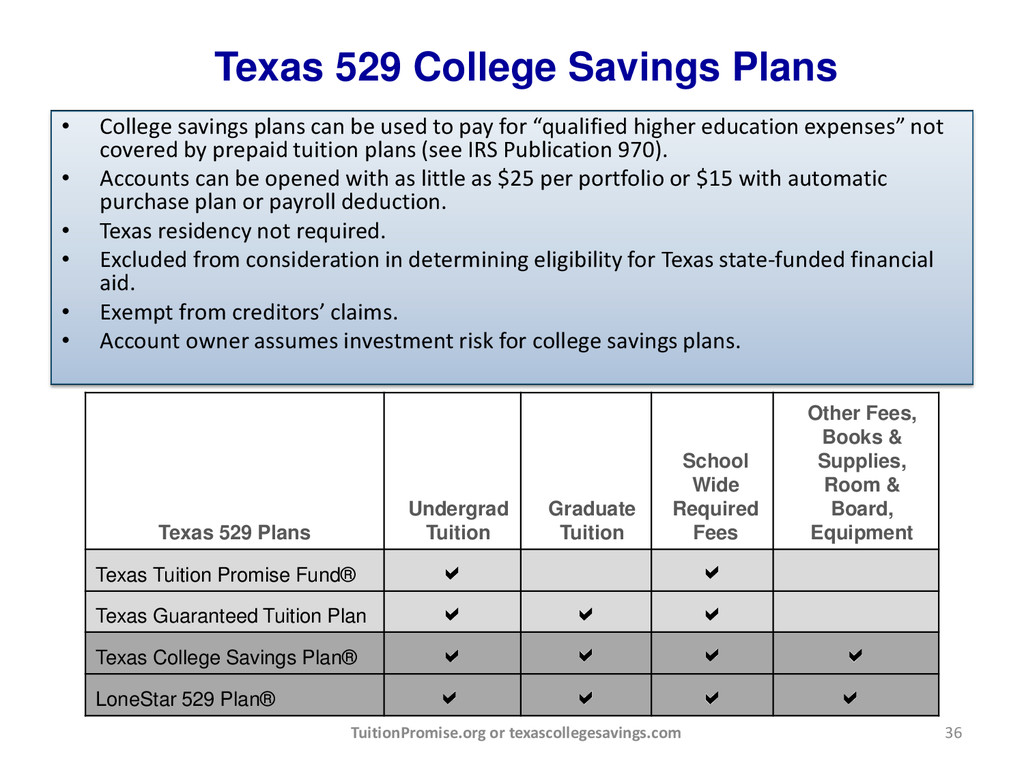

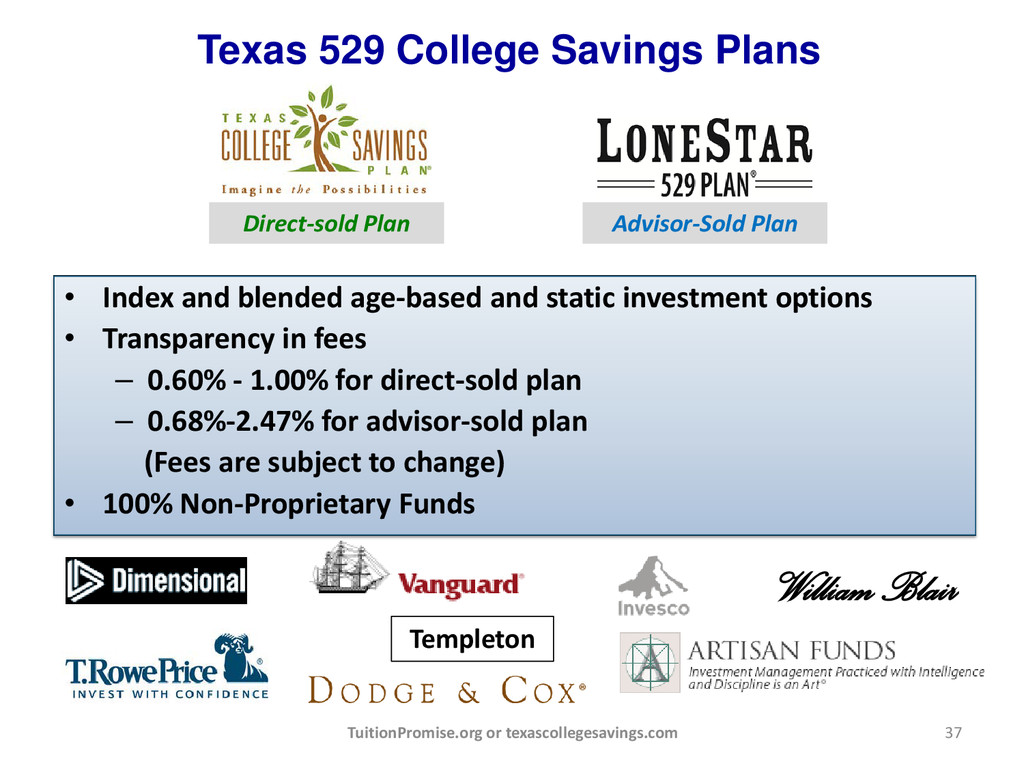

and maintained by the Texas Prepaid Higher Education Tuition Board and distributed by Northern Lights Distributors, LLC, Member FINRA, SIPC. NorthStar Financial Services Group, LLC, the parent company of Northern Lights Distributors, LLC, is the Plan manager and administrator of the Plan. Some states offer favorable tax treatment to their residents only if they invest in the state’s own 529 plan. Purchasers who are non-residents of Texas should consider whether their home state offers its residents a 529 plan with alternative tax advantages and should consult their tax advisor. Contracts in the Plan are not deposits or other obligations of any depository institution. Neither a contract nor any return paid with a refund is insured or guaranteed by the FDIC, the state of Texas, the Texas Prepaid Higher Education Tuition Board, any other state or federal governmental agency or NorthStar or its affiliates. The contracts have not been registered with the U.S. Securities and Exchange Commission or with any state. Purchasers should carefully consider the risks, administrative fees, service and other charges and expenses associated with the contracts, including Plan termination and decreased transfer or refund value. The Plan Description and Agreement contain this and other information about the Plan and may be obtained by visiting www.TuitionPromise.org or by calling 1.800.445.GRAD (4723), Option #5. Purchasers should read these documents carefully before participating. The Texas College Savings Plan® and the LoneStar 529 Plan® As stated in the Texas College Savings Plan’s current Plan Description and Savings Trust Agreement, total fees for the portfolios range from 0.60% to 1.00%. As stated in the LoneStar 529 Plan’s current Plan Description and Savings Trust Agreement, total Plan fees for the portfolios range from 0.68% to 2.47% with a maximum sales charge of 5.75%. Fees are subject to change. The Texas College Savings Plan and the LoneStar 529 Plan are each established and maintained by the Texas Prepaid Higher Education Tuition Board and distributed by Northern Lights Distributors, LLC, Member FINRA, SIPC. NorthStar Financial Services Group, LLC, the parent company of Northern Lights Distributors, LLC, is the Plan manager and administrator of the Plans. Some states offer favorable tax treatment to their residents only if they invest in the state’s own plan. Purchasers who are non-residents of Texas should consider whether their home state offers its residents a 529 plan with alternative tax advantages and should consult their tax advisor. Interests in each Plan are not deposits or other obligations of any depository institution. Before investing in either of the Plans, investors should carefully consider the investment objectives, risks, administrative fees, service and other charges and expenses associated with municipal fund securities. The Plan Descriptions and Savings Trust Agreements contain this and other information about the Plans and may be obtained by visiting www.texascollegesavings.com or calling 1.800.445.GRAD (4723), Option #3, and www.lonestar529.com or calling 1.800.445.GRAD (4723), Option #4. Investors should read these documents carefully before investing. 57 5035-NLD-01/14/2015

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}