We are surrounded by card payments as a part of buying groceries or paying our monthly bills. As much as we hope these payment methods are safe, their inherent complexity as a result of decades of backwards compatibility leads to insecurity instead.

Dominican Republic for 13 years • Lived in California for 5 years. • I dig • Payments technologies (obviously) • Security UX • Public transportation • Embedded devices

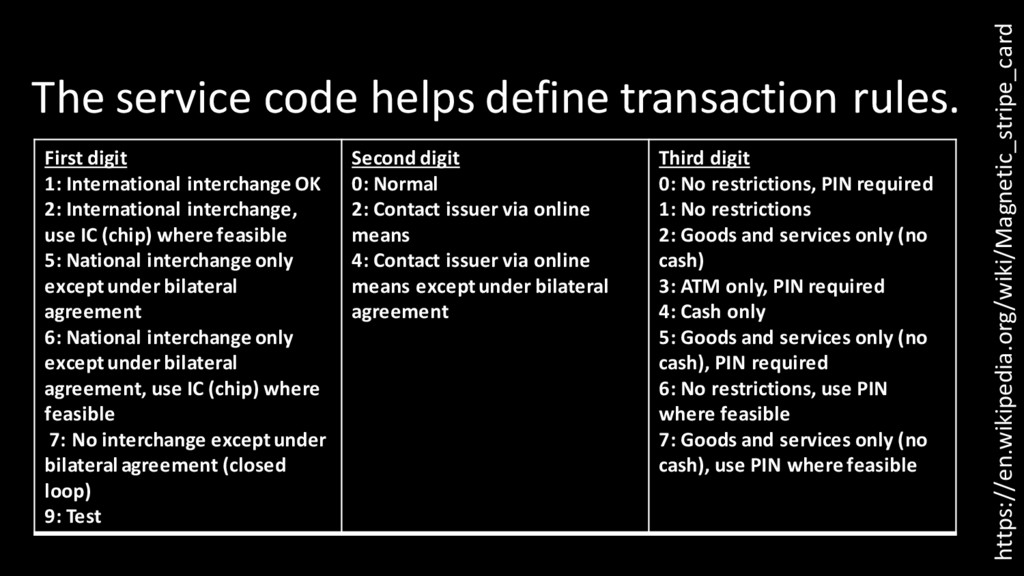

International interchange OK 2: International interchange, use IC (chip) where feasible 5: National interchange only except under bilateral agreement 6: National interchange only except under bilateral agreement, use IC (chip) where feasible 7: No interchange except under bilateral agreement (closed loop) 9: Test Second digit 0: Normal 2: Contact issuer via online means 4: Contact issuer via online means except under bilateral agreement Third digit 0: No restrictions, PIN required 1: No restrictions 2: Goods and services only (no cash) 3: ATM only, PIN required 4: Cash only 5: Goods and services only (no cash), PIN required 6: No restrictions, use PIN where feasible 7: Goods and services only (no cash), use PIN where feasible https://en.wikipedia.org/wiki/Magnetic_stripe_card

to allow debit cards to be run in stores over the credit network or the debit network. * Supporting this is legally required as a result of the Durbin Amendment

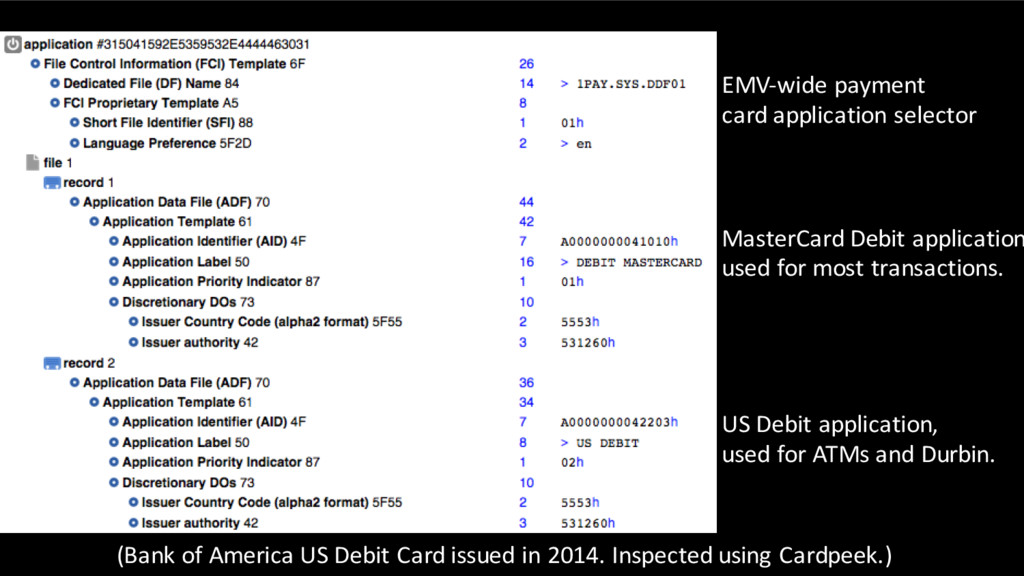

using Cardpeek.) EMV-wide payment card application selector MasterCard Debit application used for most transactions. US Debit application, used for ATMs and Durbin.

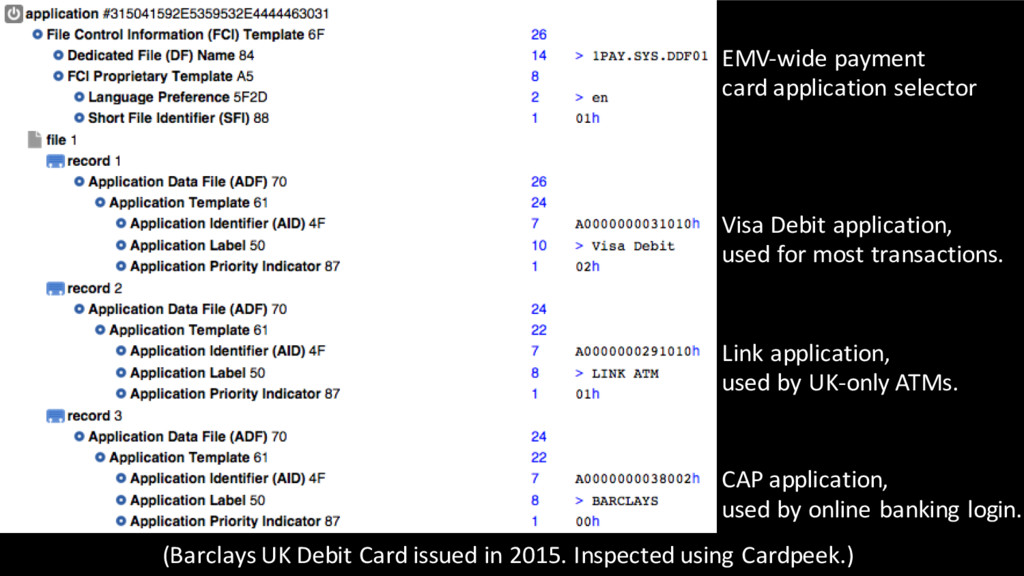

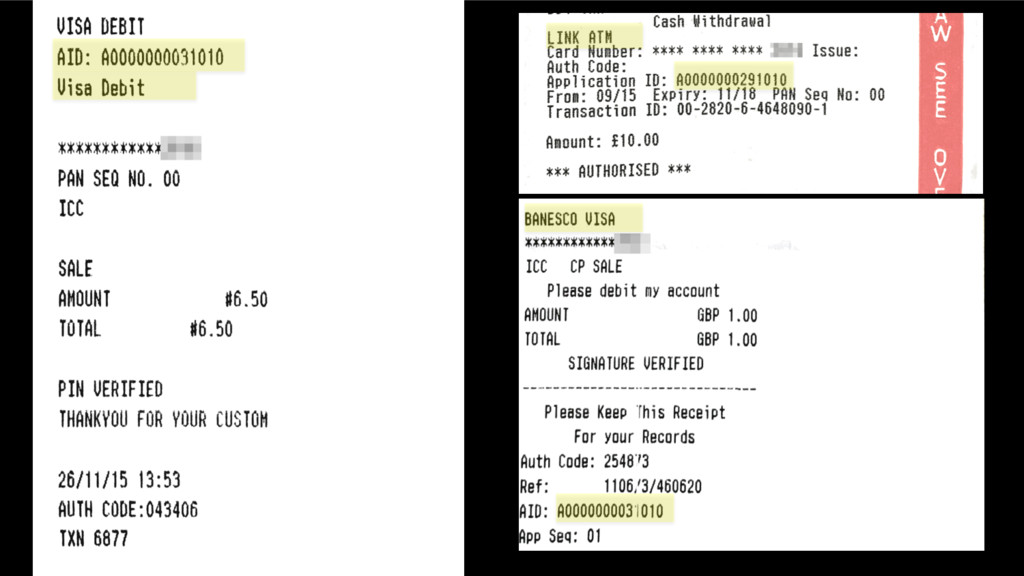

EMV-wide payment card application selector Visa Debit application, used for most transactions. Link application, used by UK-only ATMs. CAP application, used by online banking login.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Thanks! @henriwatson [email protected] https://henriwatson.com/talks/cashonly](https://files.speakerdeck.com/presentations/9a2b3dc86cc044ca94b43ad14d9d3d7c/slide_82.jpg){kind=link}