The Global Veterinary Drugs Market is projected to grow significantly from US$ 53.1 billion in 2024 to approximately US$ 121.2 billion by 2034. This expansion reflects a compound annual growth rate (CAGR) of 8.6% during the forecast period from 2025 to 2034. The growth can be attributed to the rising awareness of animal health, increasing pet ownership, and the growing burden of diseases among both companion and production animals. These factors are contributing to the increased demand for high-quality veterinary pharmaceuticals and biologics.

Veterinary drugs are crucial for treating infectious diseases, parasitic conditions, and chronic illnesses in animals. They also support preventive healthcare and promote overall animal welfare. The growing pet population, especially in urban areas, is fueling market demand. Pet owners are increasingly seeking advanced healthcare for their animals, including preventive treatments and specialty medications. This shift in consumer behavior is creating lucrative opportunities for drug manufacturers and veterinary service providers around the world.

Advancements in drug delivery methods and formulations are shaping the market. The development of vaccines, antibiotics, antiparasitic agents, and pain management drugs is gaining traction. These innovations not only improve treatment outcomes but also contribute to livestock productivity. In agriculture, veterinary drugs help maintain reproductive health and control infections, thus improving meat, milk, and egg yields in commercial farming.

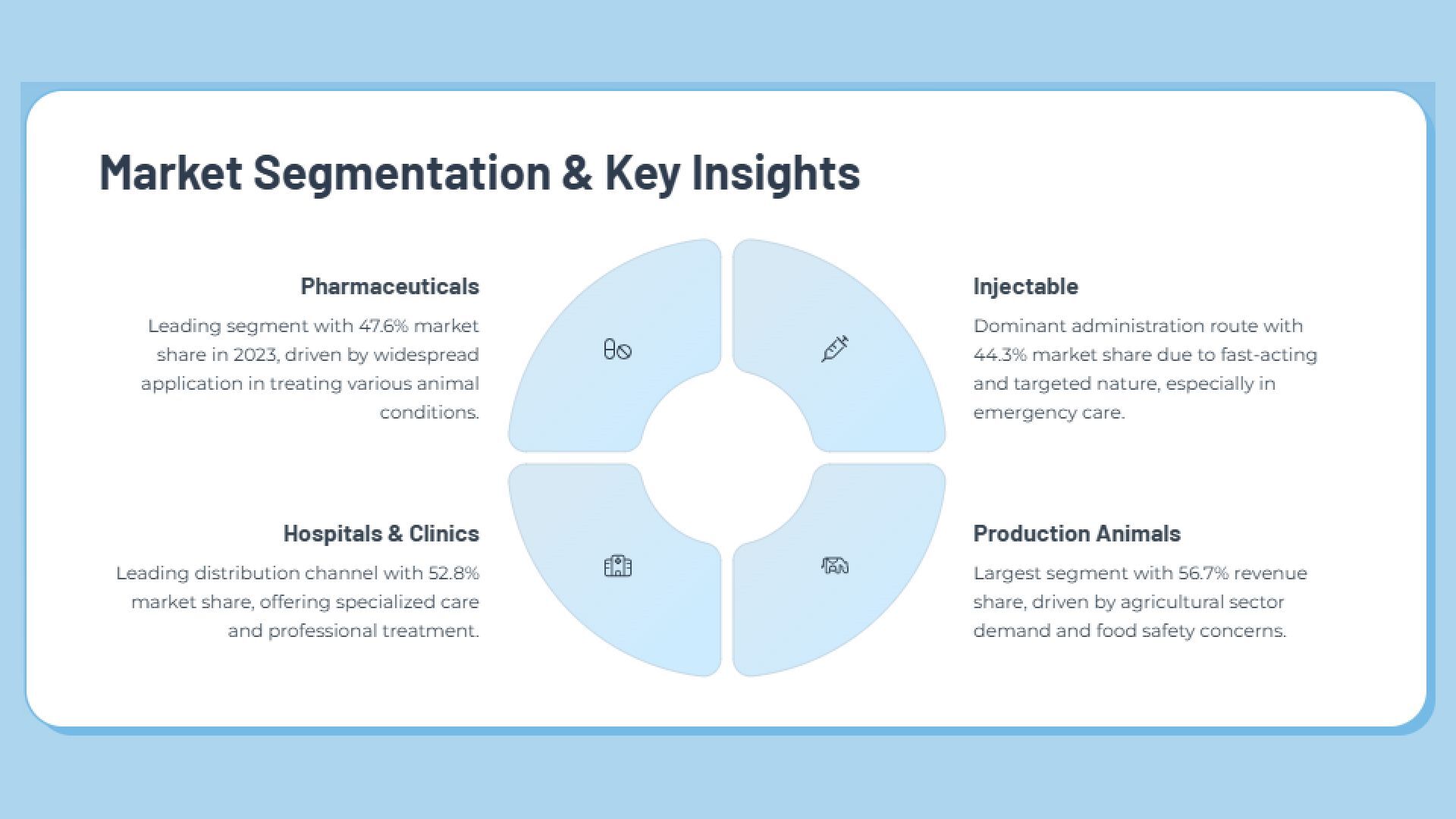

The market is segmented by product type into pharmaceuticals, biologics, and medicated feed additives. Among these, pharmaceuticals dominated the market in 2023, accounting for 47.6% of the total revenue share. These include anti-inflammatories, antimicrobials, and hormonal drugs. Their widespread use in both companion and production animals ensures continued dominance in the product landscape, supported by regulatory approvals and advancements in drug safety and efficacy.

In terms of route of administration, the market includes oral, injectable, topical, and others. Injectable drugs held the largest market share of 44.3% in 2023. This is due to their fast action and high bioavailability. Injectables are widely used for vaccinations, pain relief, and treating severe infections in livestock and pets. The increasing availability of single-dose, long-acting injectables is further contributing to their market growth.

The market is divided into companion animals and production animals. Production animals accounted for the largest revenue share of 56.7% in 2023. The dominance of this segment is driven by the economic importance of livestock health in food production. From a distribution perspective, veterinary hospitals and clinics were the leading channels in 2023, capturing 52.8% market share. North America dominated the regional market with a 41.1% share, supported by strong healthcare infrastructure and advanced veterinary care systems.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}