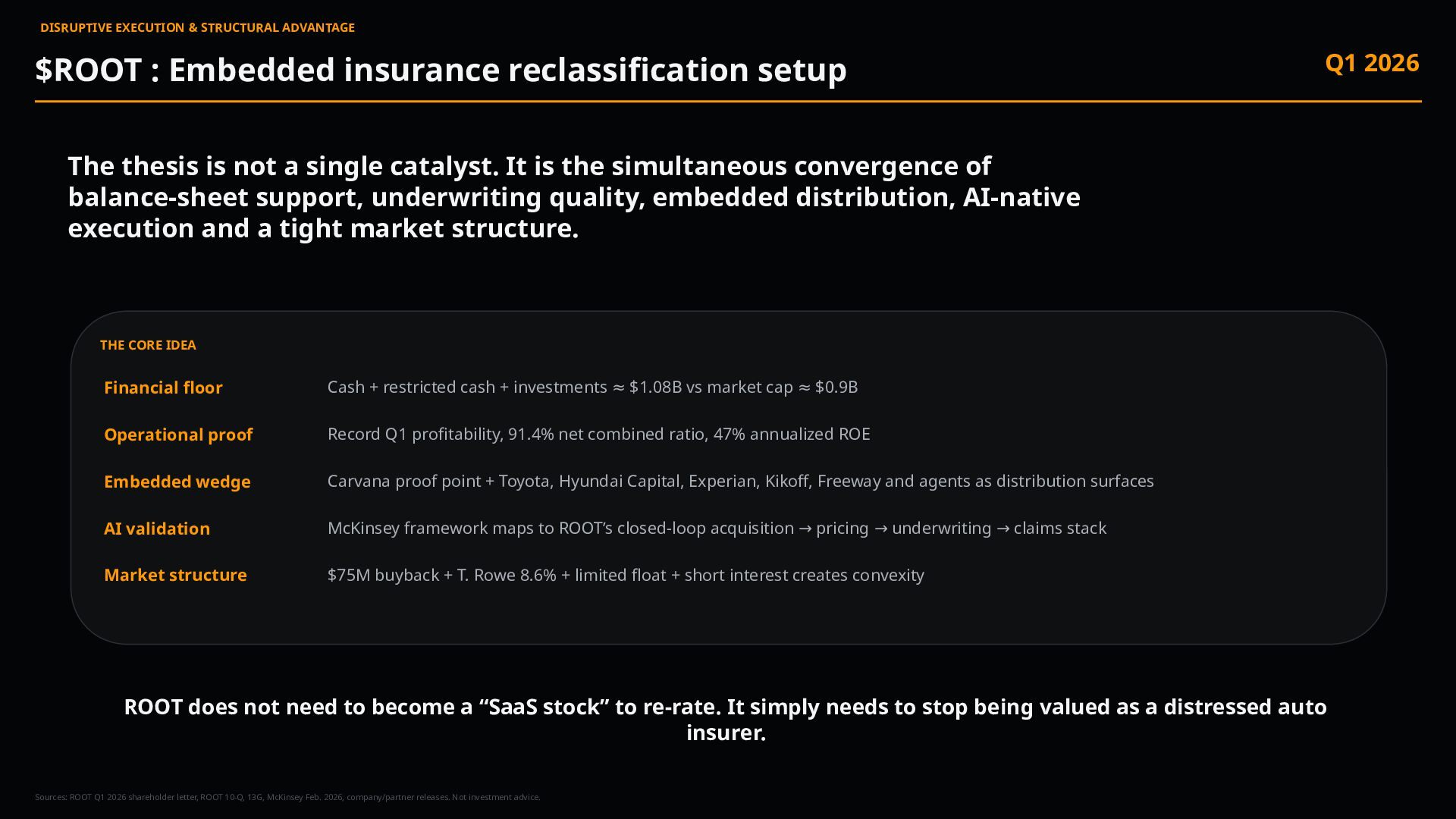

setup Q1 2026 The thesis is not a single catalyst. It is the simultaneous convergence of balance-sheet support, underwriting quality, embedded distribution, AI-native execution and a tight market structure. THE CORE IDEA Financial floor Cash + restricted cash + investments $1.08B vs market cap $0.9B ≈ ≈ Operational proof Record Q1 profitability, 91.4% net combined ratio, 47% annualized ROE Embedded wedge Carvana proof point + Toyota, Hyundai Capital, Experian, Kikoff, Freeway and agents as distribution surfaces AI validation McKinsey framework maps to ROOT’s closed-loop acquisition pricing underwriting claims stack → → → Market structure $75M buyback + T. Rowe 8.6% + limited float + short interest creates convexity ROOT does not need to become a “SaaS stock” to re-rate. It simply needs to stop being valued as a distressed auto insurer. Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice.

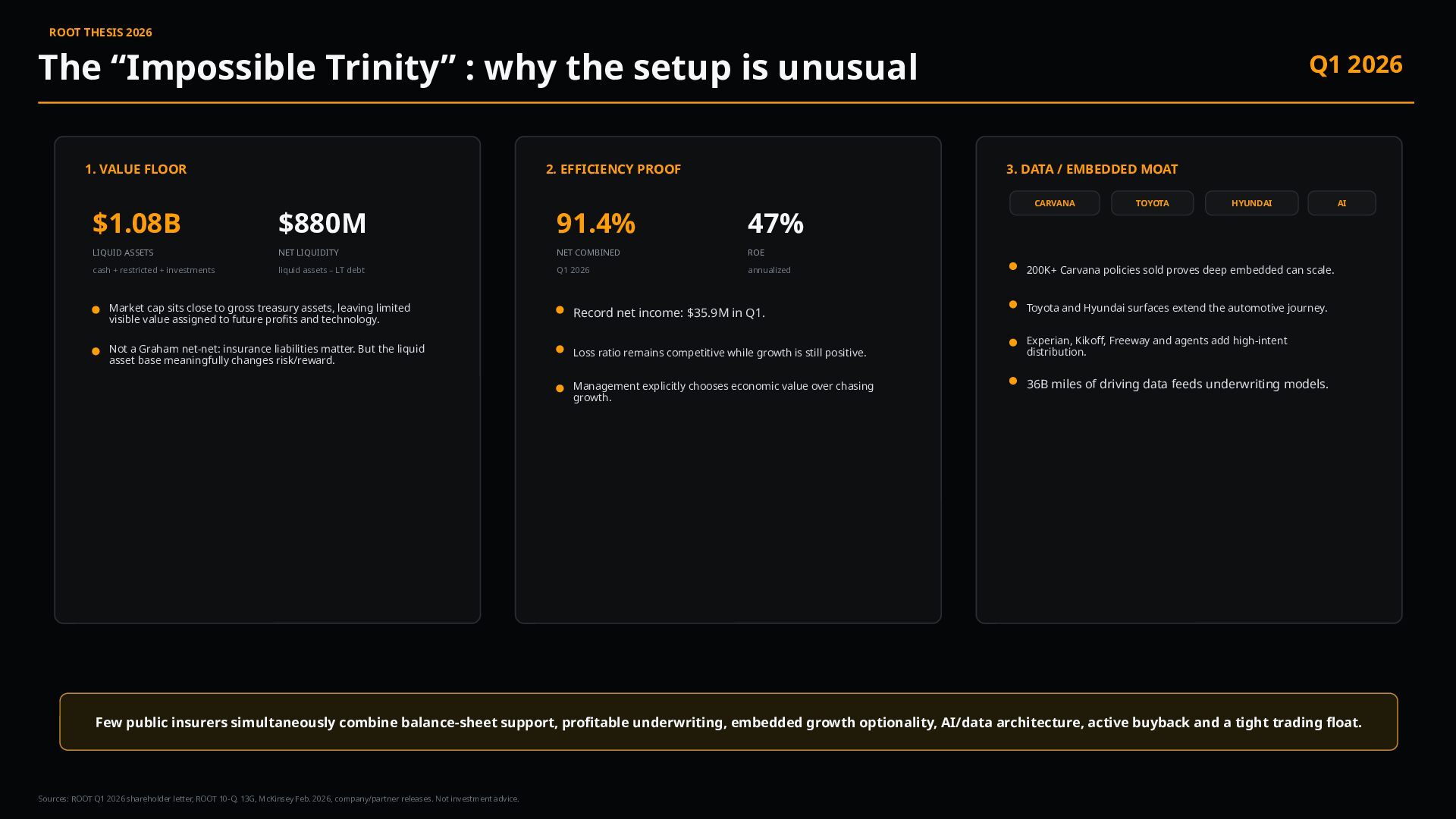

is unusual Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. 1. VALUE FLOOR 2. EFFICIENCY PROOF 3. DATA / EMBEDDED MOAT $1.08B LIQUID ASSETS cash + restricted + investments $880M NET LIQUIDITY liquid assets – LT debt Market cap sits close to gross treasury assets, leaving limited visible value assigned to future profits and technology. Not a Graham net-net: insurance liabilities matter. But the liquid asset base meaningfully changes risk/reward. 91.4% NET COMBINED Q1 2026 47% ROE annualized Record net income: $35.9M in Q1. Loss ratio remains competitive while growth is still positive. Management explicitly chooses economic value over chasing growth. CARVANA TOYOTA HYUNDAI AI 200K+ Carvana policies sold proves deep embedded can scale. Toyota and Hyundai surfaces extend the automotive journey. Experian, Kikoff, Freeway and agents add high-intent distribution. 36B miles of driving data feeds underwriting models. Few public insurers simultaneously combine balance-sheet support, profitable underwriting, embedded growth optionality, AI/data architecture, active buyback and a tight trading float.

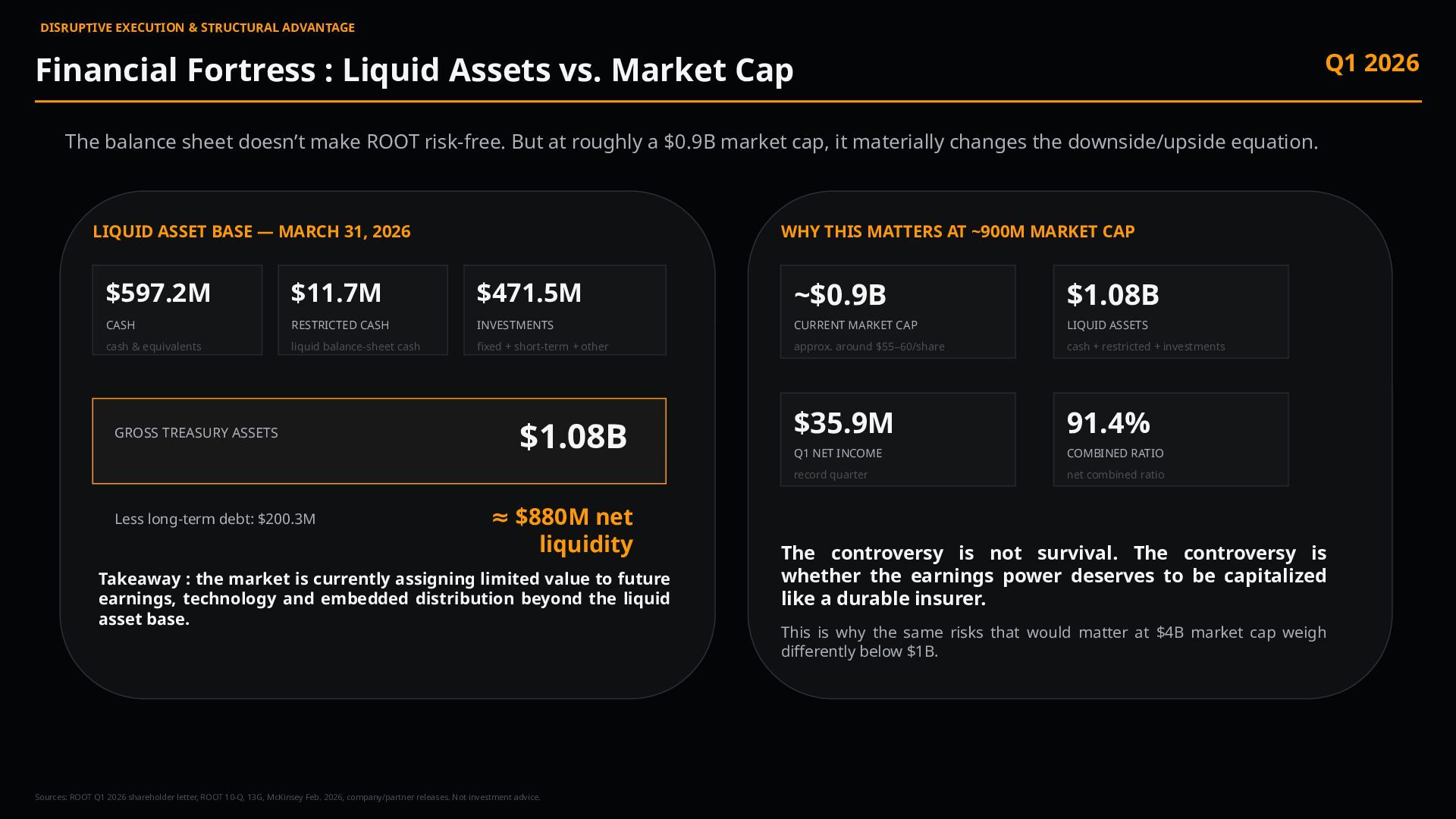

vs. Market Cap Q1 2026 The balance sheet doesn’t make ROOT risk-free. But at roughly a $0.9B market cap, it materially changes the downside/upside equation. LIQUID ASSET BASE — MARCH 31, 2026 $597.2M CASH cash & equivalents $11.7M RESTRICTED CASH liquid balance-sheet cash $471.5M INVESTMENTS fixed + short-term + other GROSS TREASURY ASSETS $1.08B Less long-term debt: $200.3M $880M net ≈ liquidity Takeaway : the market is currently assigning limited value to future earnings, technology and embedded distribution beyond the liquid asset base. WHY THIS MATTERS AT ~900M MARKET CAP ~$0.9B CURRENT MARKET CAP approx. around $55–60/share $1.08B LIQUID ASSETS cash + restricted + investments $35.9M Q1 NET INCOME record quarter 91.4% COMBINED RATIO net combined ratio The controversy is not survival. The controversy is whether the earnings power deserves to be capitalized like a durable insurer. This is why the same risks that would matter at $4B market cap weigh differently below $1B. Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice.

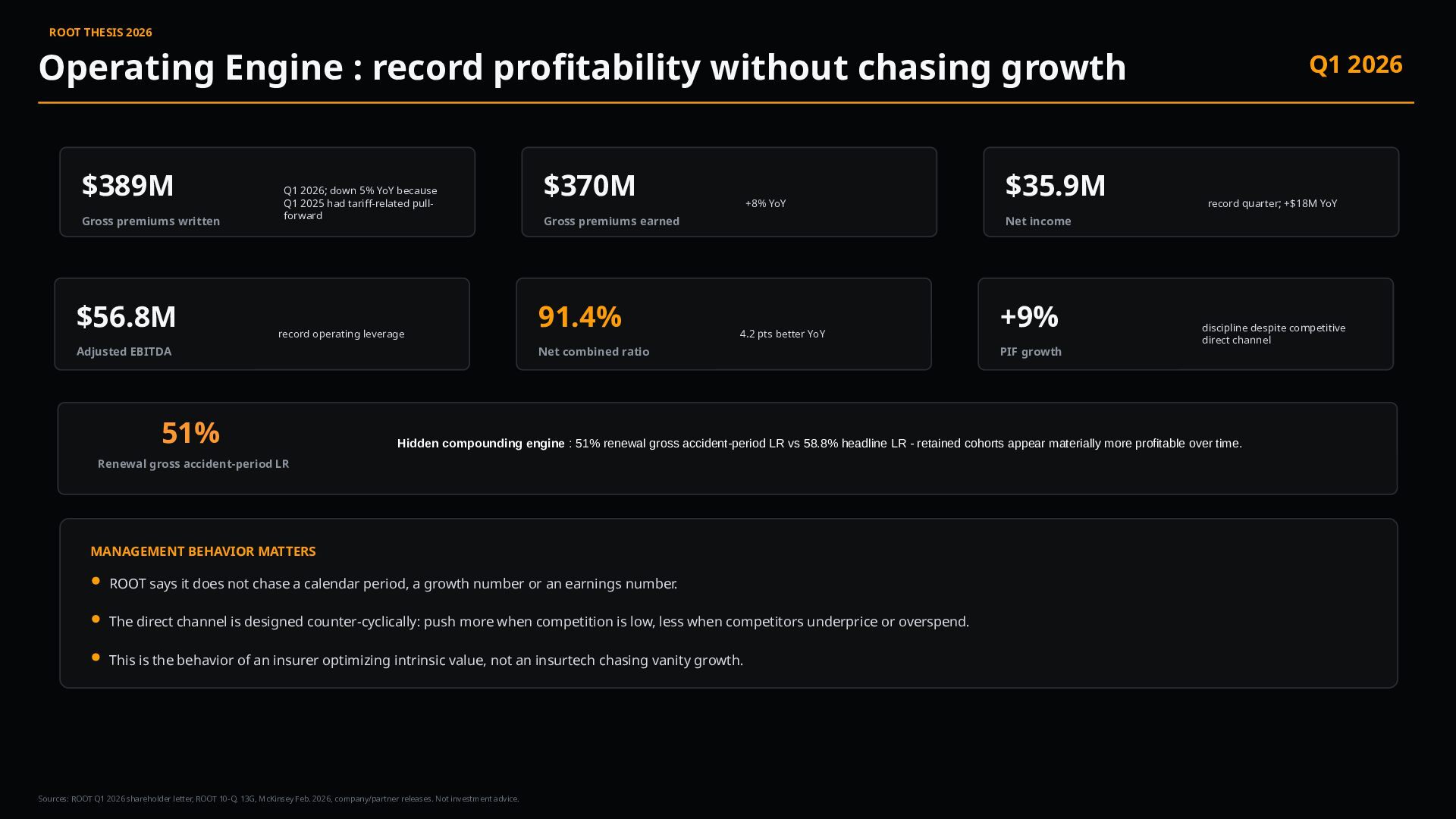

growth Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. $389M Gross premiums written Q1 2026; down 5% YoY because Q1 2025 had tariff-related pull- forward $370M Gross premiums earned +8% YoY $35.9M Net income record quarter; +$18M YoY $56.8M Adjusted EBITDA record operating leverage 91.4% Net combined ratio 4.2 pts better YoY +9% PIF growth discipline despite competitive direct channel MANAGEMENT BEHAVIOR MATTERS ROOT says it does not chase a calendar period, a growth number or an earnings number. The direct channel is designed counter-cyclically: push more when competition is low, less when competitors underprice or overspend. This is the behavior of an insurer optimizing intrinsic value, not an insurtech chasing vanity growth. 51% Hidden compounding engine : 51% renewal gross accident-period LR vs 58.8% headline LR - retained cohorts appear materially more profitable over time. Renewal gross accident-period LR

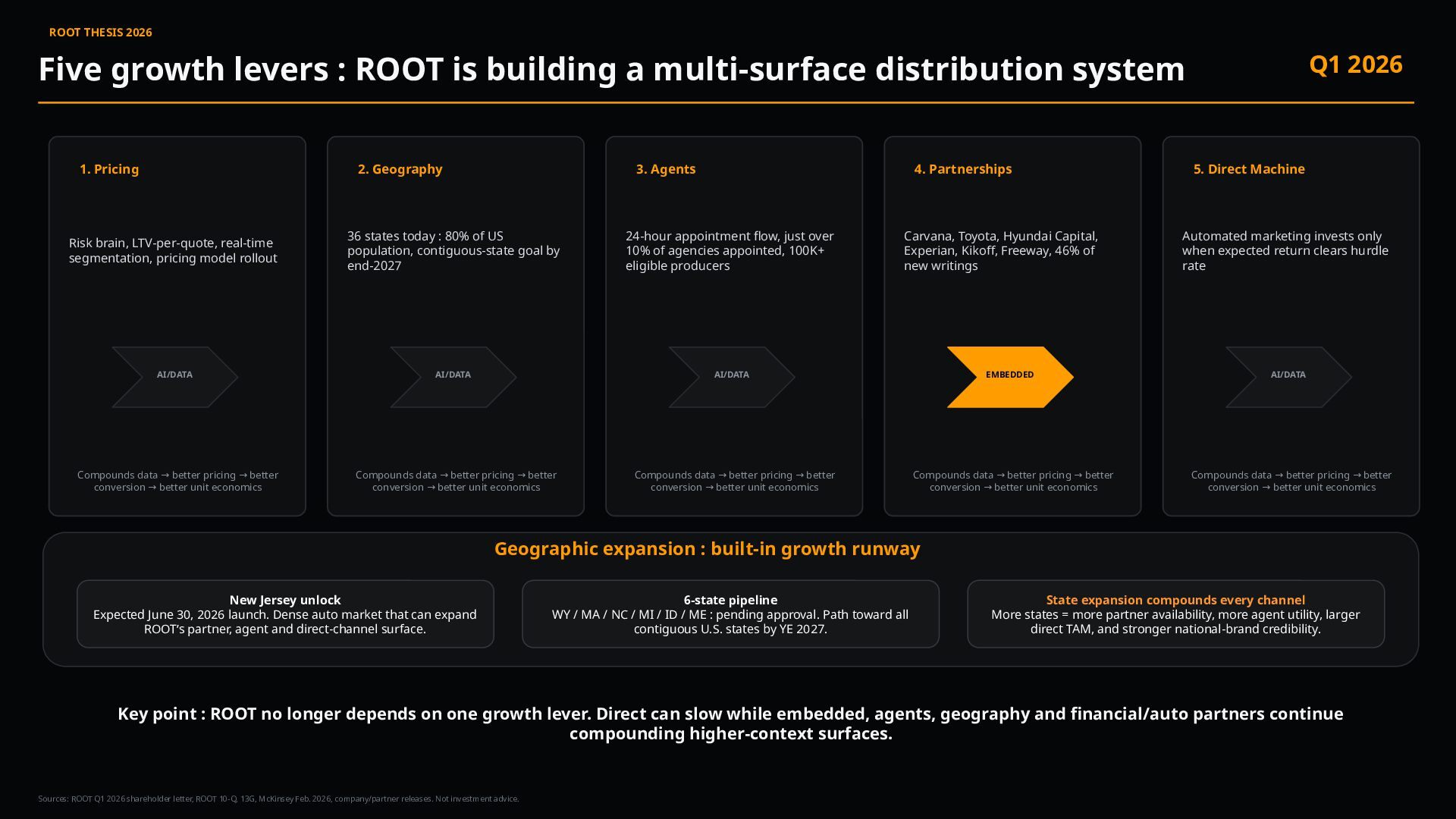

a multi-surface distribution system Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. 1. Pricing Risk brain, LTV-per-quote, real-time segmentation, pricing model rollout AI/DATA Compounds data better pricing better → → conversion better unit economics → 2. Geography 36 states today : 80% of US population, contiguous-state goal by end-2027 AI/DATA Compounds data better pricing better → → conversion better unit economics → 3. Agents 24-hour appointment flow, just over 10% of agencies appointed, 100K+ eligible producers AI/DATA Compounds data better pricing better → → conversion better unit economics → 4. Partnerships Carvana, Toyota, Hyundai Capital, Experian, Kikoff, Freeway, 46% of new writings EMBEDDED Compounds data better pricing better → → conversion better unit economics → 5. Direct Machine Automated marketing invests only when expected return clears hurdle rate AI/DATA Compounds data better pricing better → → conversion better unit economics → Key point : ROOT no longer depends on one growth lever. Direct can slow while embedded, agents, geography and financial/auto partners continue compounding higher-context surfaces. Geographic expansion : built-in growth runway New Jersey unlock Expected June 30, 2026 launch. Dense auto market that can expand ROOT’s partner, agent and direct-channel surface. 6-state pipeline WY / MA / NC / MI / ID / ME : pending approval. Path toward all contiguous U.S. states by YE 2027. State expansion compounds every channel More states = more partner availability, more agent utility, larger direct TAM, and stronger national-brand credibility.

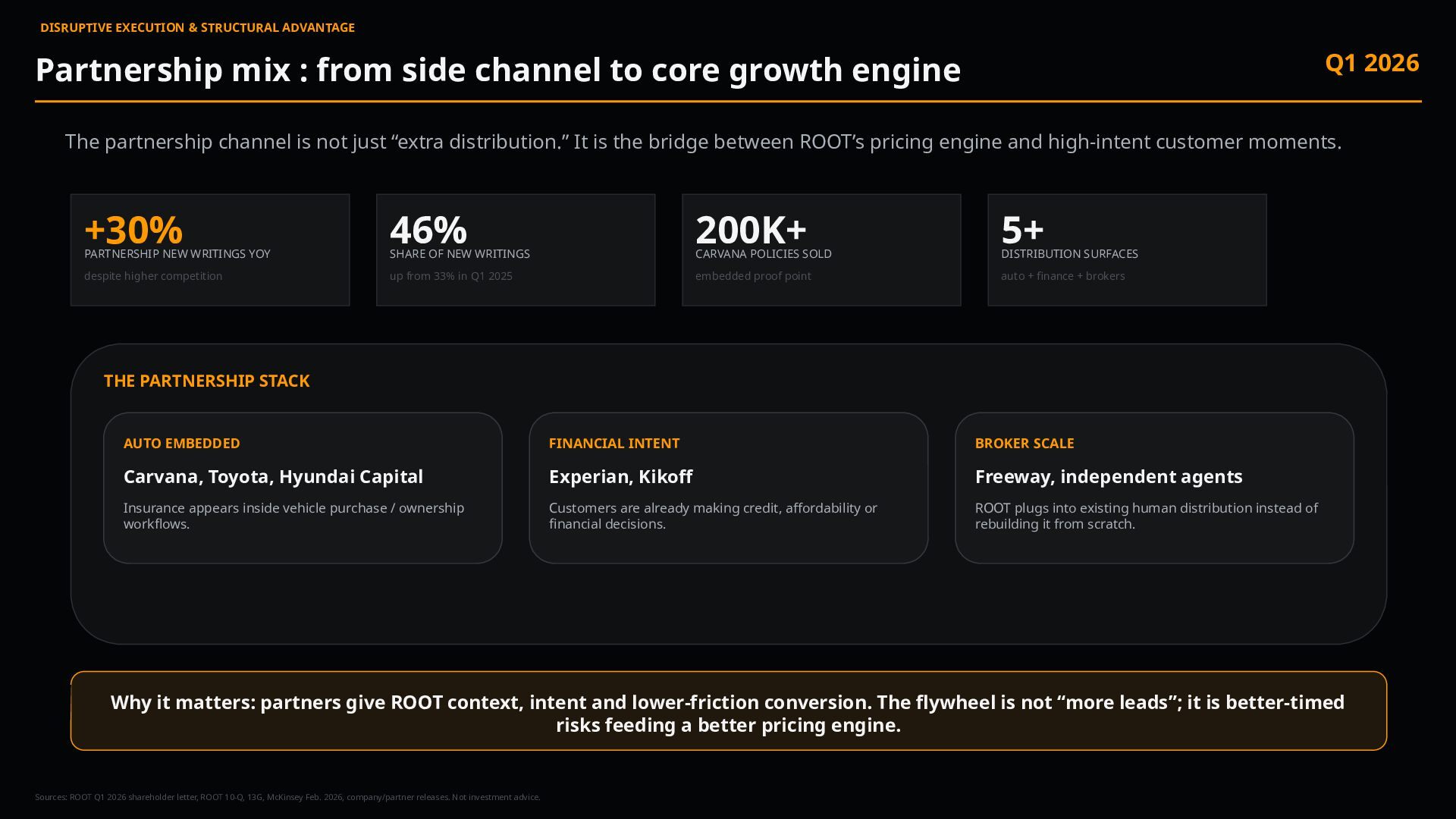

channel to core growth engine Q1 2026 The partnership channel is not just “extra distribution.” It is the bridge between ROOT’s pricing engine and high-intent customer moments. +30% PARTNERSHIP NEW WRITINGS YOY despite higher competition 46% SHARE OF NEW WRITINGS up from 33% in Q1 2025 200K+ CARVANA POLICIES SOLD embedded proof point 5+ DISTRIBUTION SURFACES auto + finance + brokers THE PARTNERSHIP STACK AUTO EMBEDDED Carvana, Toyota, Hyundai Capital Insurance appears inside vehicle purchase / ownership workflows. FINANCIAL INTENT Experian, Kikoff Customers are already making credit, affordability or financial decisions. BROKER SCALE Freeway, independent agents ROOT plugs into existing human distribution instead of rebuilding it from scratch. Why it matters: partners give ROOT context, intent and lower-friction conversion. The flywheel is not “more leads”; it is better-timed risks feeding a better pricing engine. Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice.

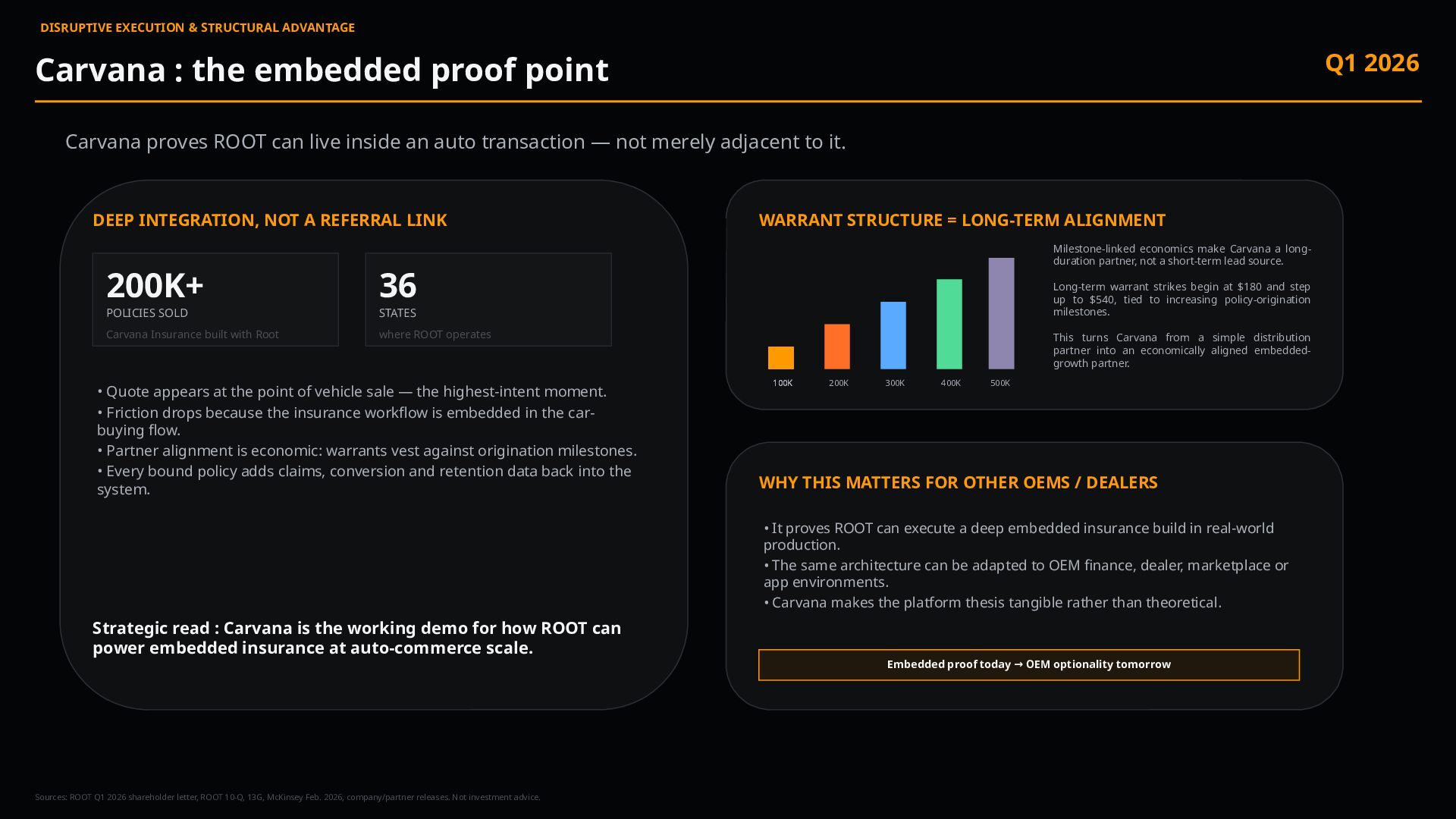

point Q1 2026 Carvana proves ROOT can live inside an auto transaction — not merely adjacent to it. DEEP INTEGRATION, NOT A REFERRAL LINK 200K+ POLICIES SOLD Carvana Insurance built with Root 36 STATES where ROOT operates • Quote appears at the point of vehicle sale — the highest-intent moment. • Friction drops because the insurance workflow is embedded in the car- buying flow. • Partner alignment is economic: warrants vest against origination milestones. • Every bound policy adds claims, conversion and retention data back into the system. Strategic read : Carvana is the working demo for how ROOT can power embedded insurance at auto-commerce scale. WARRANT STRUCTURE = LONG-TERM ALIGNMENT 100K 200K 300K 400K Milestone-linked economics make Carvana a long- duration partner, not a short-term lead source. Long-term warrant strikes begin at $180 and step up to $540, tied to increasing policy-origination milestones. This turns Carvana from a simple distribution partner into an economically aligned embedded- growth partner. WHY THIS MATTERS FOR OTHER OEMS / DEALERS • It proves ROOT can execute a deep embedded insurance build in real-world production. • The same architecture can be adapted to OEM finance, dealer, marketplace or app environments. • Carvana makes the platform thesis tangible rather than theoretical. Embedded proof today OEM optionality tomorrow → Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. 100K 100K 500K

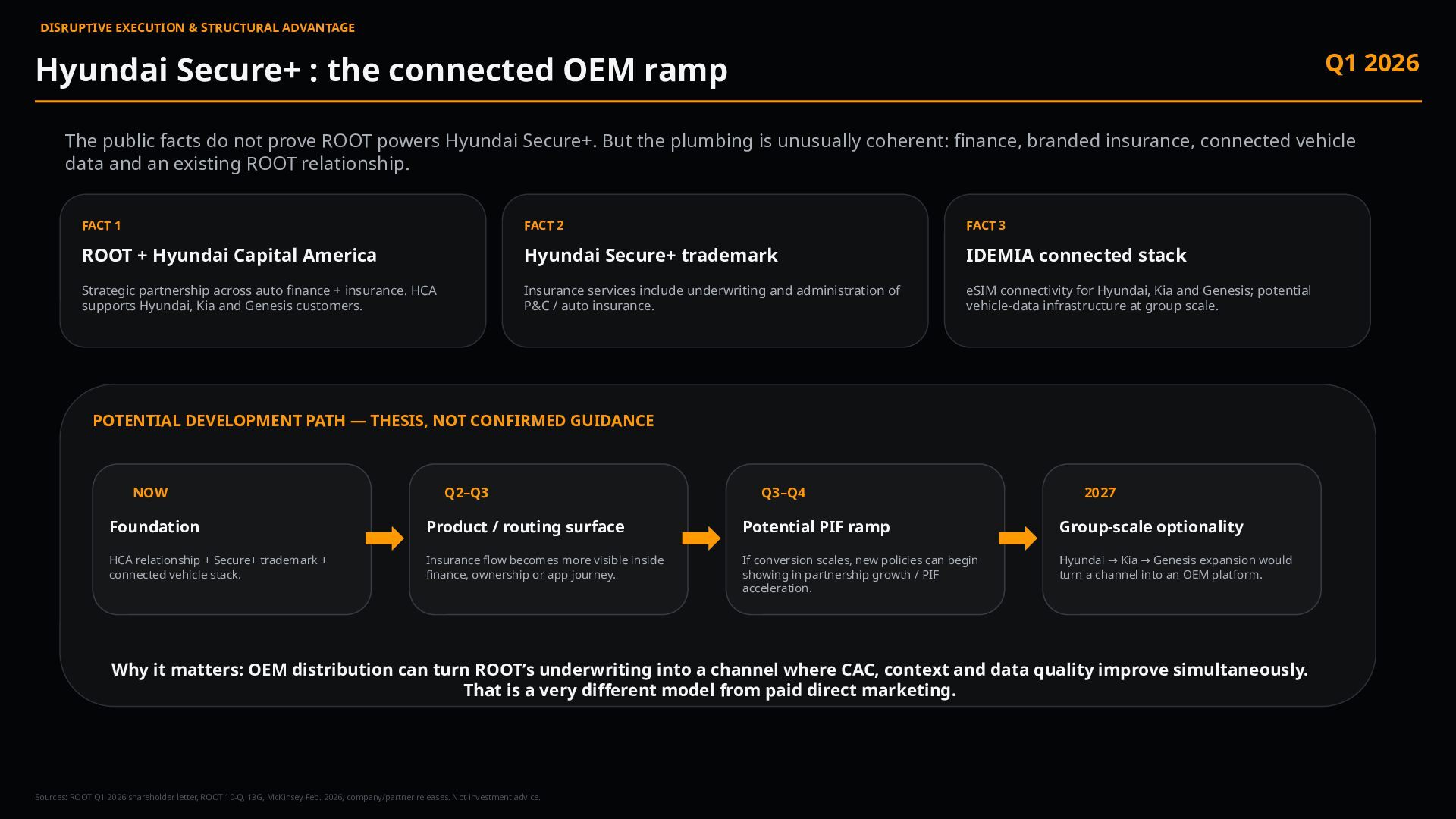

OEM ramp Q1 2026 The public facts do not prove ROOT powers Hyundai Secure+. But the plumbing is unusually coherent: finance, branded insurance, connected vehicle data and an existing ROOT relationship. FACT 1 ROOT + Hyundai Capital America Strategic partnership across auto finance + insurance. HCA supports Hyundai, Kia and Genesis customers. FACT 2 Hyundai Secure+ trademark Insurance services include underwriting and administration of P&C / auto insurance. FACT 3 IDEMIA connected stack eSIM connectivity for Hyundai, Kia and Genesis; potential vehicle-data infrastructure at group scale. POTENTIAL DEVELOPMENT PATH — THESIS, NOT CONFIRMED GUIDANCE NOW Foundation HCA relationship + Secure+ trademark + connected vehicle stack. Q2–Q3 Product / routing surface Insurance flow becomes more visible inside finance, ownership or app journey. Q3–Q4 Potential PIF ramp If conversion scales, new policies can begin showing in partnership growth / PIF acceleration. 2027 Group-scale optionality Hyundai Kia Genesis expansion would → → turn a channel into an OEM platform. Why it matters: OEM distribution can turn ROOT’s underwriting into a channel where CAC, context and data quality improve simultaneously. That is a very different model from paid direct marketing. Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice.

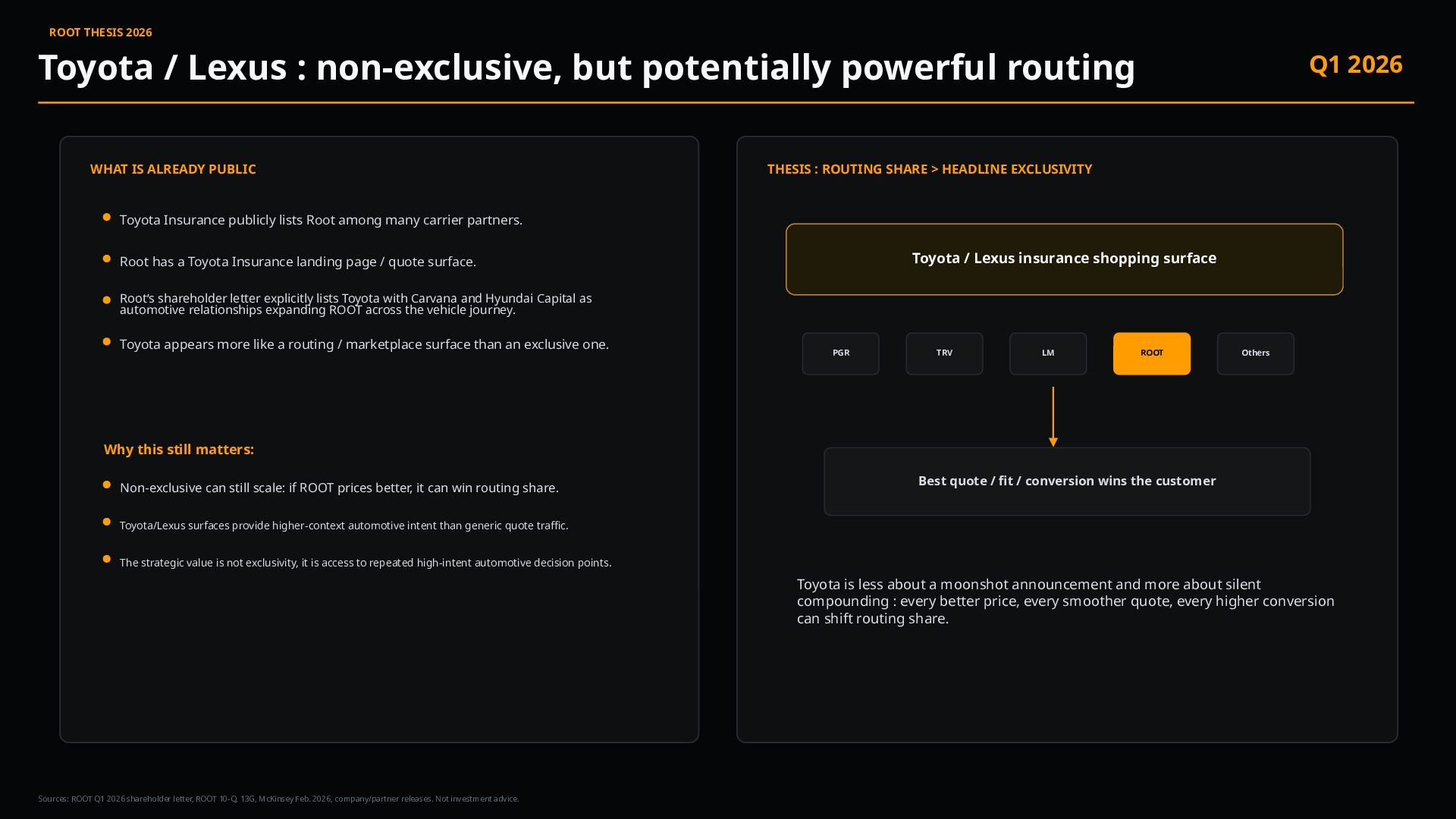

powerful routing Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. WHAT IS ALREADY PUBLIC Toyota Insurance publicly lists Root among many carrier partners. Root has a Toyota Insurance landing page / quote surface. Root’s shareholder letter explicitly lists Toyota with Carvana and Hyundai Capital as automotive relationships expanding ROOT across the vehicle journey. Toyota appears more like a routing / marketplace surface than an exclusive one. Why this still matters: Non-exclusive can still scale: if ROOT prices better, it can win routing share. Toyota/Lexus surfaces provide higher-context automotive intent than generic quote traffic. The strategic value is not exclusivity, it is access to repeated high-intent automotive decision points. THESIS : ROUTING SHARE > HEADLINE EXCLUSIVITY Toyota / Lexus insurance shopping surface PGR TRV LM ROOT Others Best quote / fit / conversion wins the customer Toyota is less about a moonshot announcement and more about silent compounding : every better price, every smoother quote, every higher conversion can shift routing share.

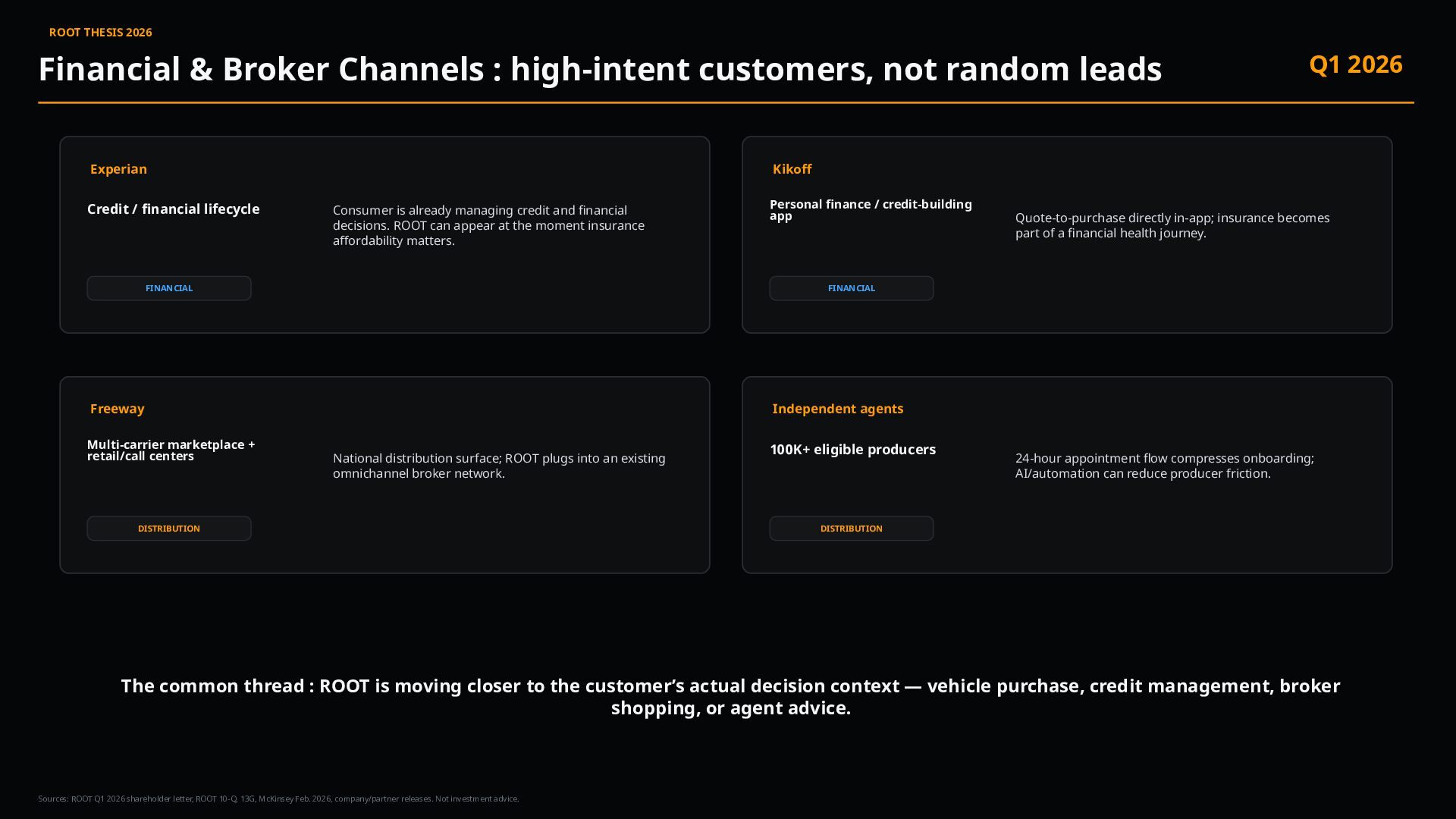

not random leads Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. Experian Credit / financial lifecycle Consumer is already managing credit and financial decisions. ROOT can appear at the moment insurance affordability matters. FINANCIAL Kikoff Personal finance / credit-building app Quote-to-purchase directly in-app; insurance becomes part of a financial health journey. FINANCIAL Freeway Multi-carrier marketplace + retail/call centers National distribution surface; ROOT plugs into an existing omnichannel broker network. DISTRIBUTION Independent agents 100K+ eligible producers 24-hour appointment flow compresses onboarding; AI/automation can reduce producer friction. DISTRIBUTION The common thread : ROOT is moving closer to the customer’s actual decision context — vehicle purchase, credit management, broker shopping, or agent advice.

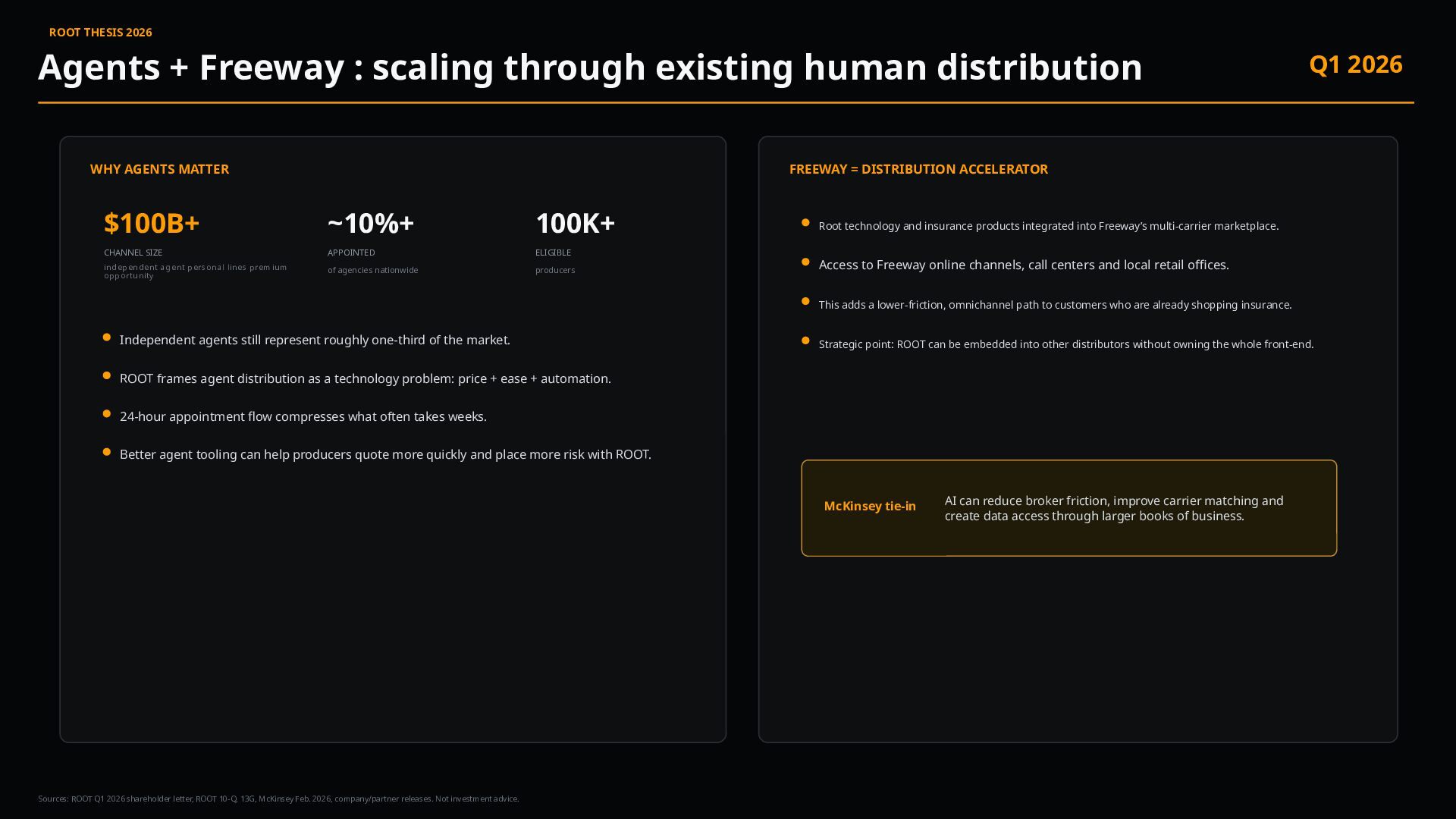

human distribution Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. WHY AGENTS MATTER $100B+ CHANNEL SIZE independent agent personal lines prem ium opportunity ~10%+ APPOINTED of agencies nationwide 100K+ ELIGIBLE producers Independent agents still represent roughly one-third of the market. ROOT frames agent distribution as a technology problem: price + ease + automation. 24-hour appointment flow compresses what often takes weeks. Better agent tooling can help producers quote more quickly and place more risk with ROOT. FREEWAY = DISTRIBUTION ACCELERATOR Root technology and insurance products integrated into Freeway’s multi-carrier marketplace. Access to Freeway online channels, call centers and local retail offices. This adds a lower-friction, omnichannel path to customers who are already shopping insurance. Strategic point: ROOT can be embedded into other distributors without owning the whole front-end. McKinsey tie-in AI can reduce broker friction, improve carrier matching and create data access through larger books of business.

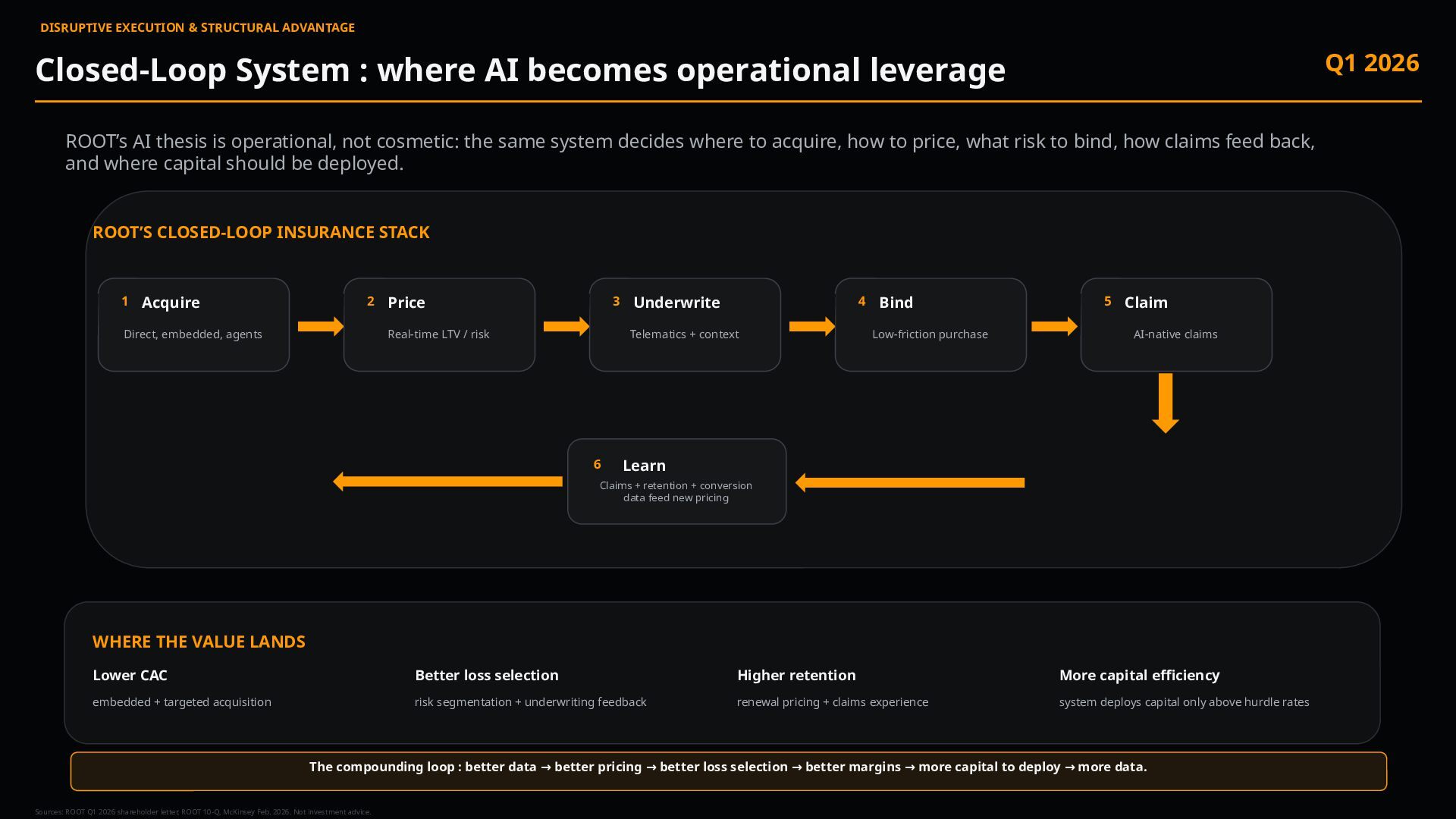

becomes operational leverage Q1 2026 ROOT’s AI thesis is operational, not cosmetic: the same system decides where to acquire, how to price, what risk to bind, how claims feed back, and where capital should be deployed. ROOT’S CLOSED-LOOP INSURANCE STACK 1 Acquire Direct, embedded, agents 2 Price Real-time LTV / risk 3 Underwrite Telematics + context 4 Bind Low-friction purchase 5 Claim AI-native claims 6 Learn Claims + retention + conversion data feed new pricing WHERE THE VALUE LANDS Lower CAC embedded + targeted acquisition Better loss selection risk segmentation + underwriting feedback Higher retention renewal pricing + claims experience More capital efficiency system deploys capital only above hurdle rates The compounding loop : better data better pricing better loss selection better margins more capital to deploy more data. → → → → → Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, McKinsey Feb. 2026. Not investment advice.

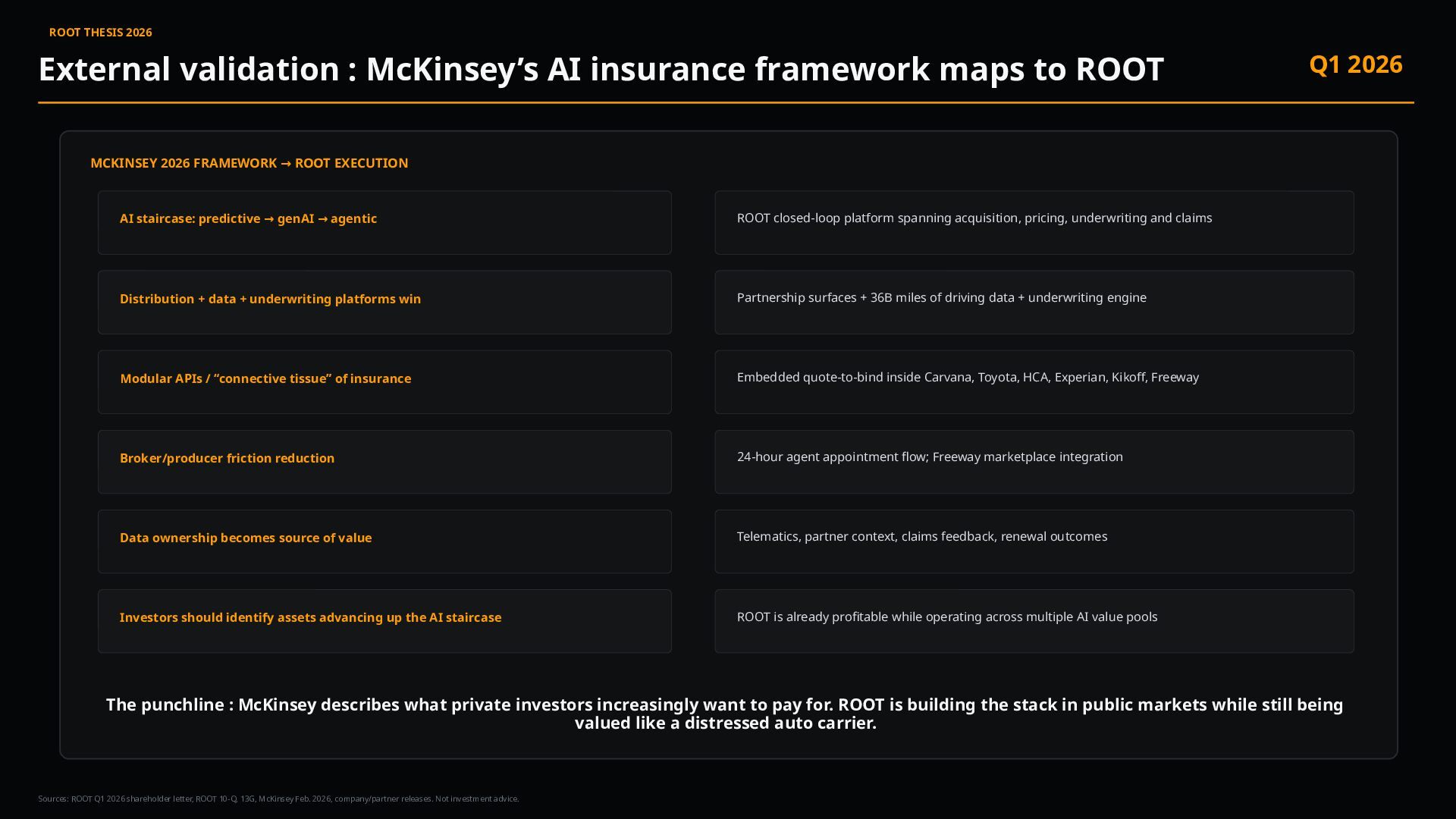

maps to ROOT Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. MCKINSEY 2026 FRAMEWORK ROOT EXECUTION → AI staircase: predictive genAI agentic → → ROOT closed-loop platform spanning acquisition, pricing, underwriting and claims Distribution + data + underwriting platforms win Partnership surfaces + 36B miles of driving data + underwriting engine Modular APIs / “connective tissue” of insurance Embedded quote-to-bind inside Carvana, Toyota, HCA, Experian, Kikoff, Freeway Broker/producer friction reduction 24-hour agent appointment flow; Freeway marketplace integration Data ownership becomes source of value Telematics, partner context, claims feedback, renewal outcomes Investors should identify assets advancing up the AI staircase ROOT is already profitable while operating across multiple AI value pools The punchline : McKinsey describes what private investors increasingly want to pay for. ROOT is building the stack in public markets while still being valued like a distressed auto carrier.

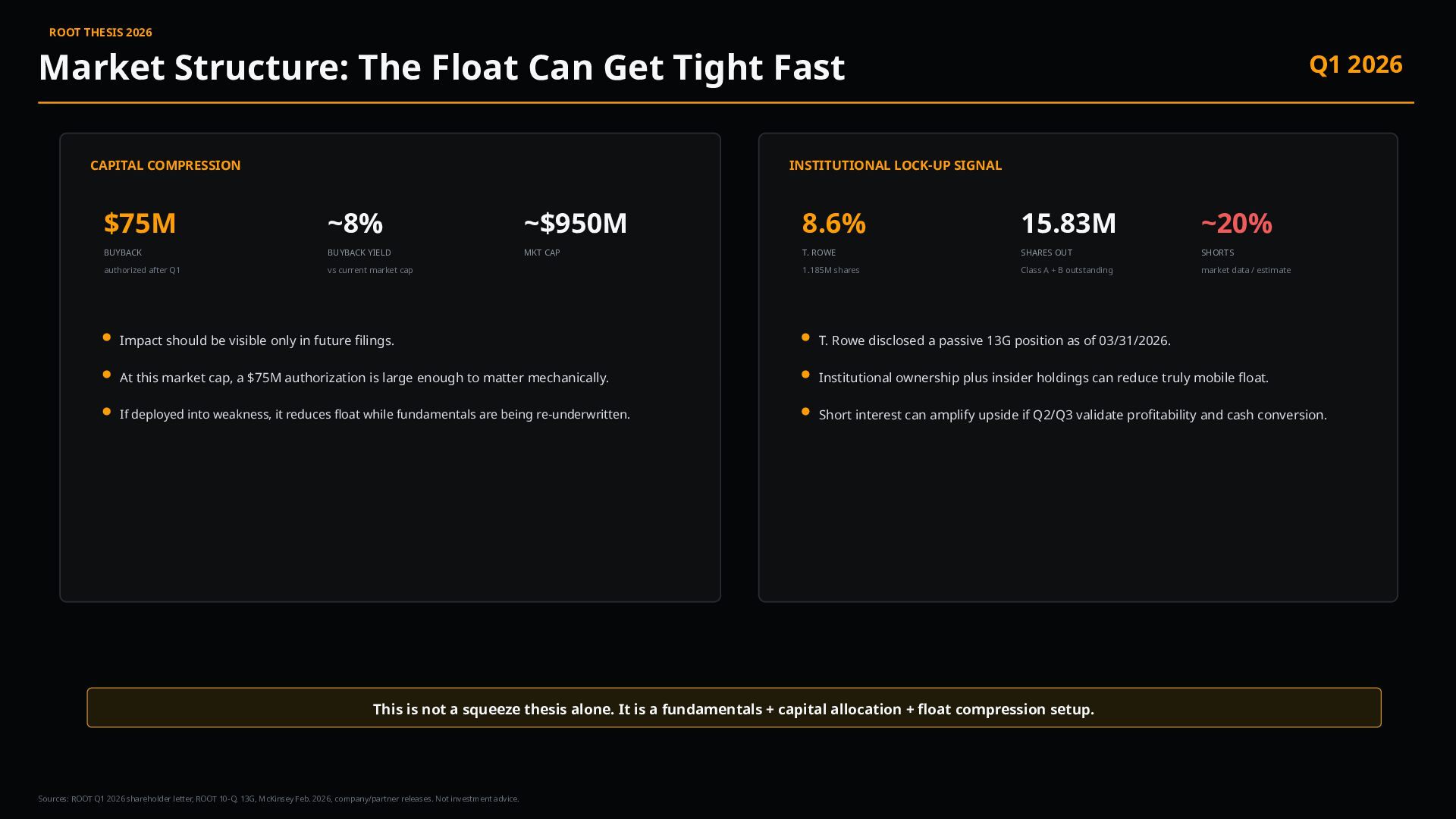

Fast Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. CAPITAL COMPRESSION $75M BUYBACK authorized after Q1 ~8% BUYBACK YIELD vs current market cap ~$950M MKT CAP Impact should be visible only in future filings. At this market cap, a $75M authorization is large enough to matter mechanically. If deployed into weakness, it reduces float while fundamentals are being re-underwritten. INSTITUTIONAL LOCK-UP SIGNAL 8.6% T. ROWE 1.185M shares 15.83M SHARES OUT Class A + B outstanding ~20% SHORTS market data / estimate T. Rowe disclosed a passive 13G position as of 03/31/2026. Institutional ownership plus insider holdings can reduce truly mobile float. Short interest can amplify upside if Q2/Q3 validate profitability and cash conversion. This is not a squeeze thesis alone. It is a fundamentals + capital allocation + float compression setup.

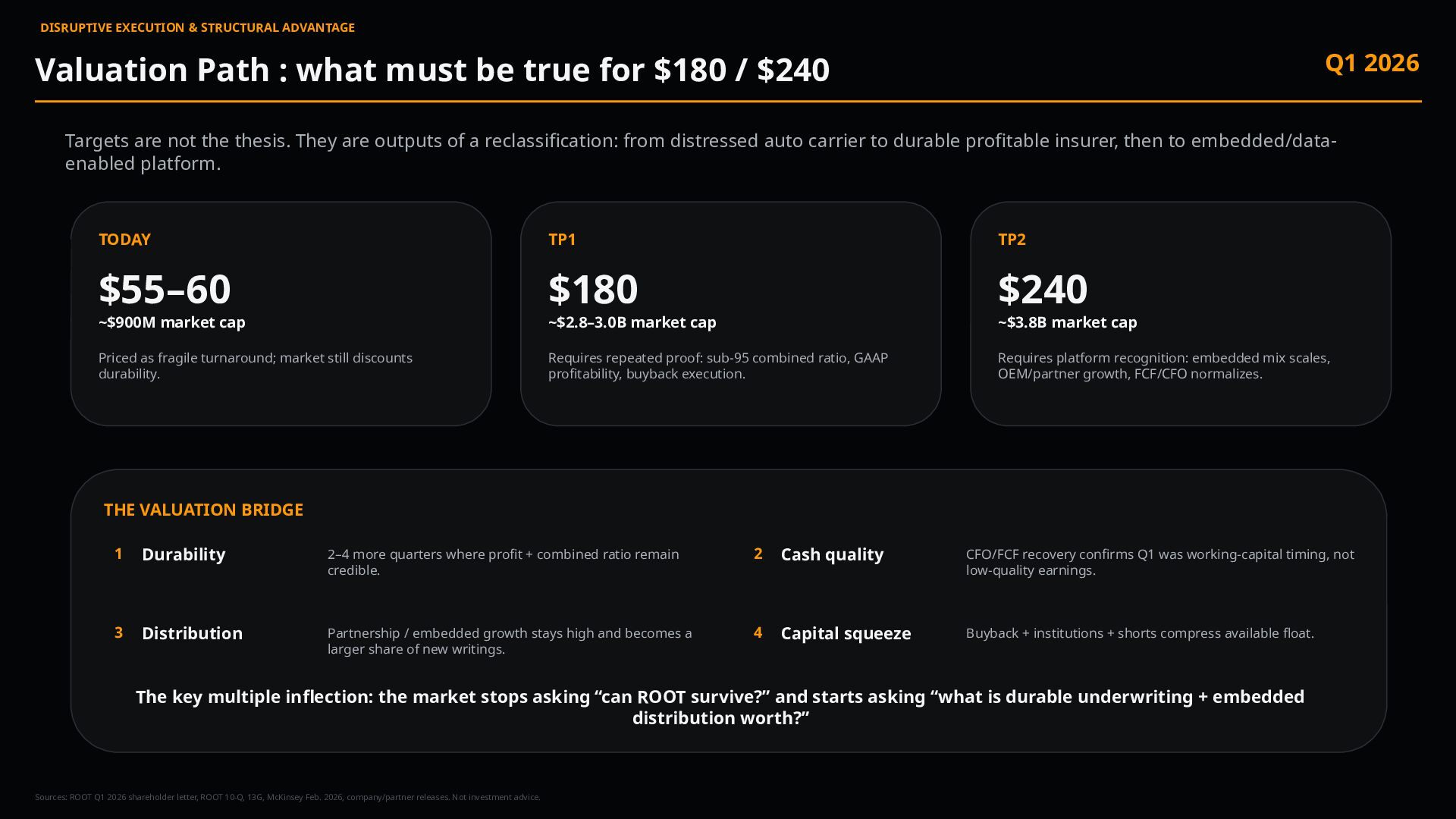

be true for $180 / $240 Q1 2026 Targets are not the thesis. They are outputs of a reclassification: from distressed auto carrier to durable profitable insurer, then to embedded/data- enabled platform. TODAY $55–60 ~$900M market cap Priced as fragile turnaround; market still discounts durability. TP1 $180 ~$2.8–3.0B market cap Requires repeated proof: sub-95 combined ratio, GAAP profitability, buyback execution. TP2 $240 ~$3.8B market cap Requires platform recognition: embedded mix scales, OEM/partner growth, FCF/CFO normalizes. THE VALUATION BRIDGE 1 Durability 2–4 more quarters where profit + combined ratio remain credible. 2 Cash quality CFO/FCF recovery confirms Q1 was working-capital timing, not low-quality earnings. 3 Distribution Partnership / embedded growth stays high and becomes a larger share of new writings. 4 Capital squeeze Buyback + institutions + shorts compress available float. The key multiple inflection: the market stops asking “can ROOT survive?” and starts asking “what is durable underwriting + embedded distribution worth?” Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice.

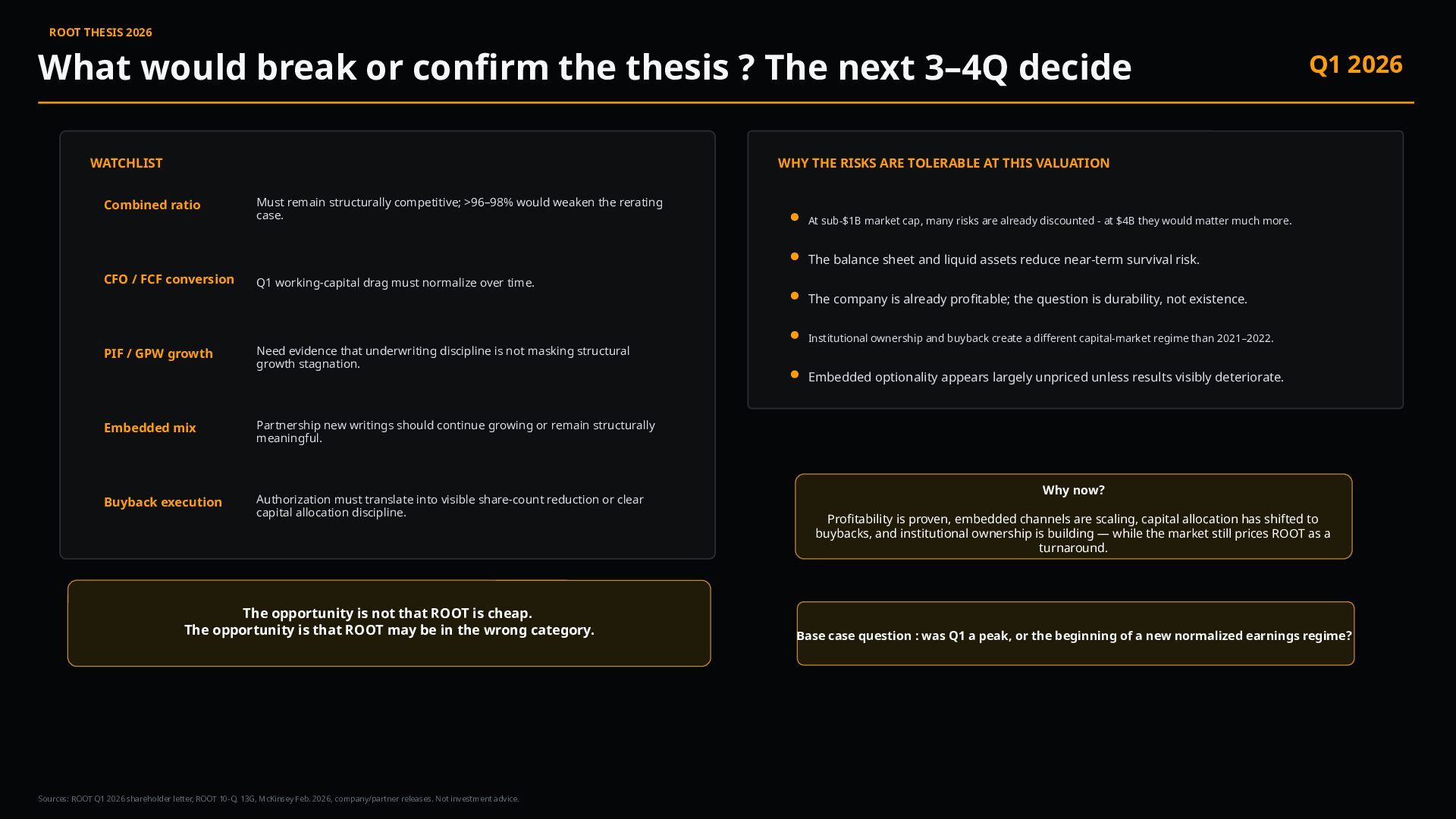

? The next 3–4Q decide Q1 2026 Sources: ROOT Q1 2026 shareholder letter, ROOT 10-Q, 13G, McKinsey Feb. 2026, company/partner releases. Not investment advice. WATCHLIST Combined ratio Must remain structurally competitive; >96–98% would weaken the rerating case. CFO / FCF conversion Q1 working-capital drag must normalize over time. PIF / GPW growth Need evidence that underwriting discipline is not masking structural growth stagnation. Embedded mix Partnership new writings should continue growing or remain structurally meaningful. Buyback execution Authorization must translate into visible share-count reduction or clear capital allocation discipline. WHY THE RISKS ARE TOLERABLE AT THIS VALUATION At sub-$1B market cap, many risks are already discounted - at $4B they would matter much more. The balance sheet and liquid assets reduce near-term survival risk. The company is already profitable; the question is durability, not existence. Institutional ownership and buyback create a different capital-market regime than 2021–2022. Embedded optionality appears largely unpriced unless results visibly deteriorate. Base case question : was Q1 a peak, or the beginning of a new normalized earnings regime? The opportunity is not that ROOT is cheap. The opportunity is that ROOT may be in the wrong category. Why now? Profitability is proven, embedded channels are scaling, capital allocation has shifted to buybacks, and institutional ownership is building — while the market still prices ROOT as a turnaround.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}