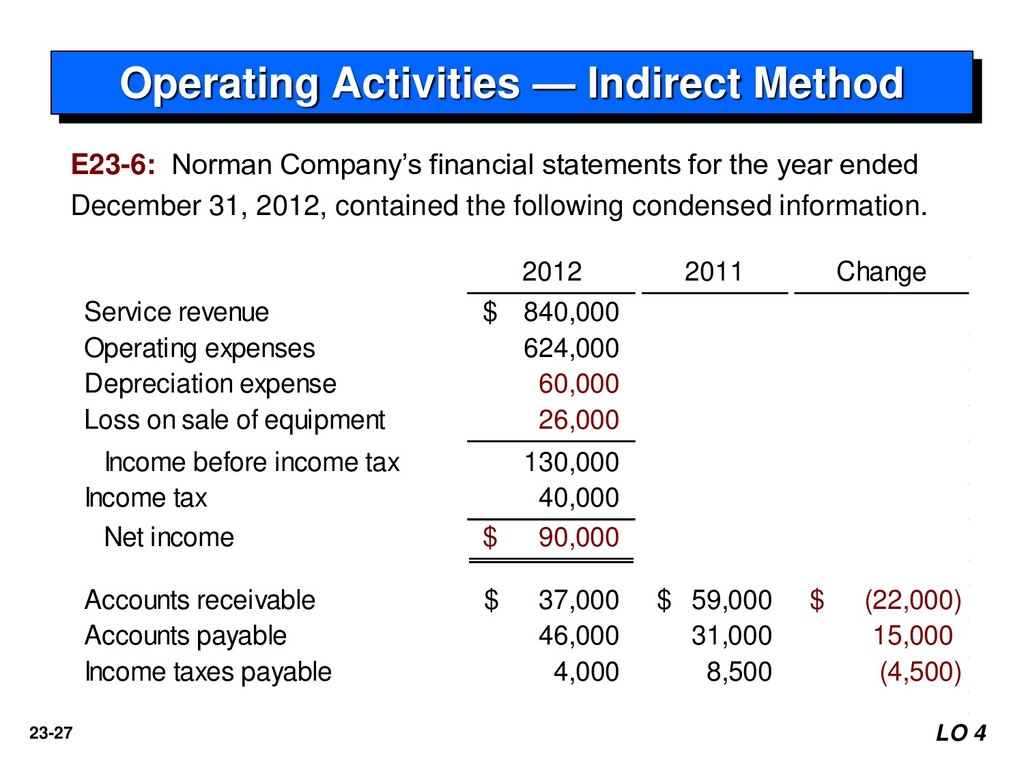

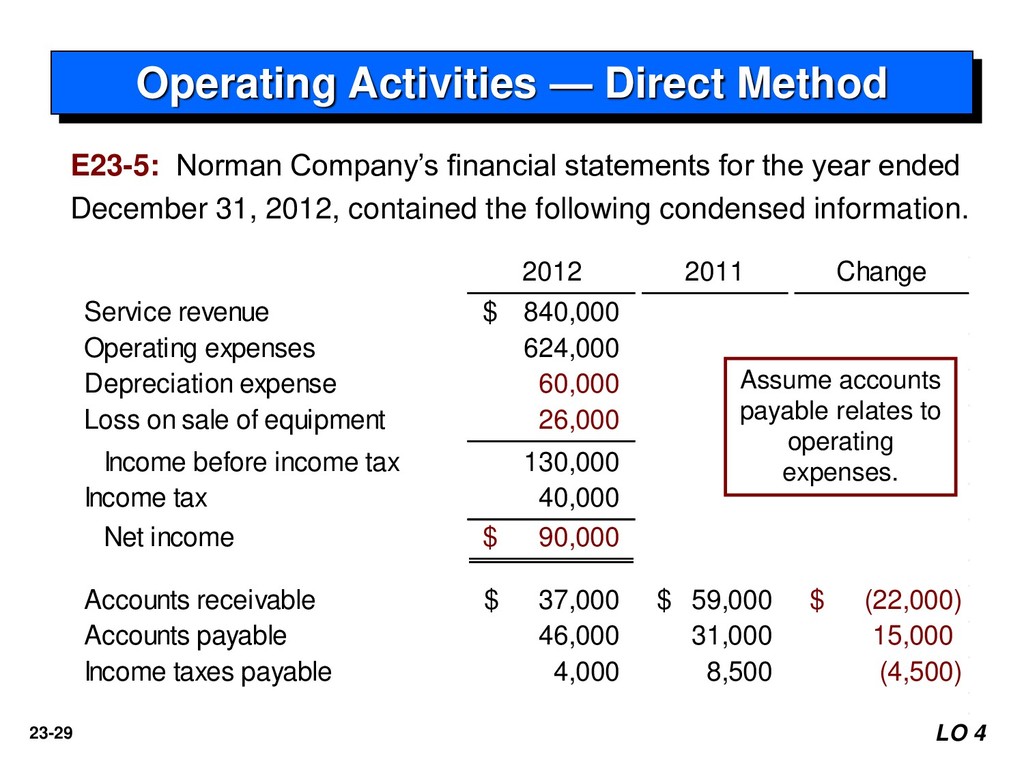

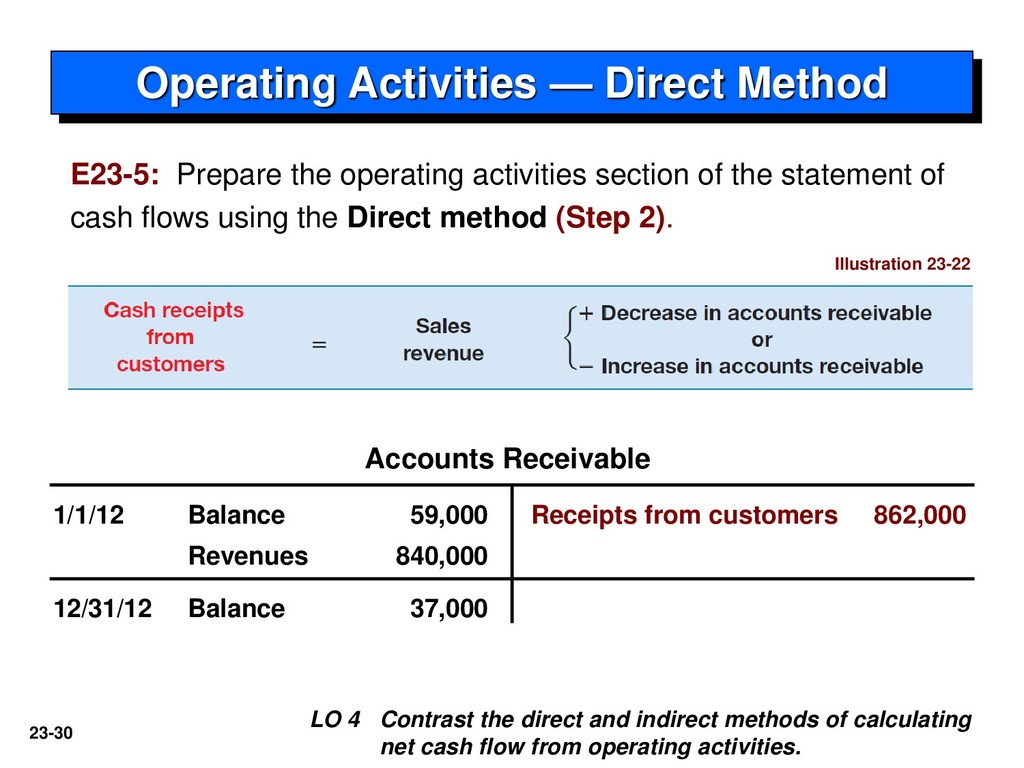

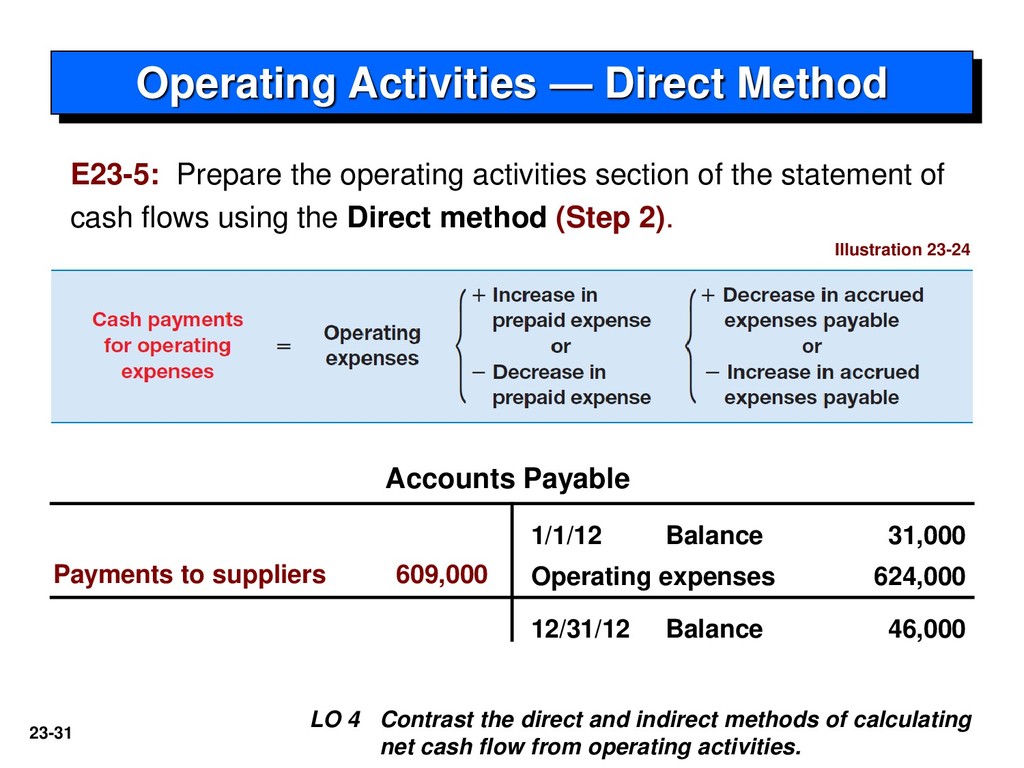

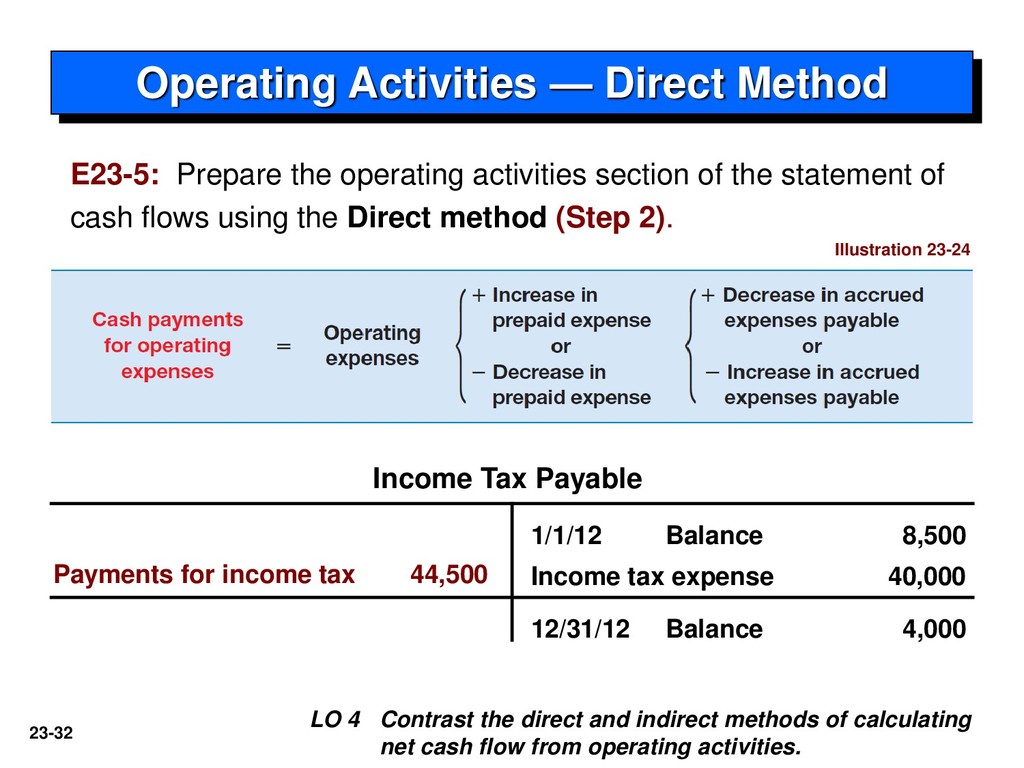

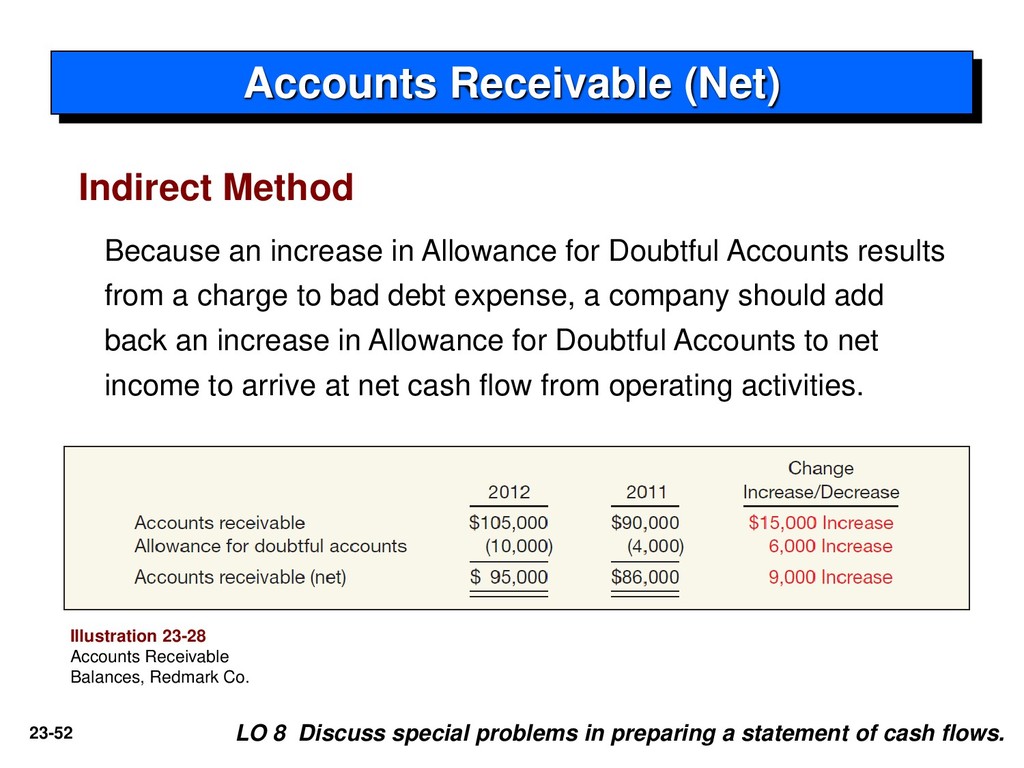

December 31, 2012, contained the following condensed information. Operating Activities — Indirect Method 2012 2011 Change Service revenue 840,000 $ Operating expenses 624,000 Depreciation expense 60,000 Loss on sale of equipment 26,000 Income before income tax 130,000 Income tax 40,000 Net income 90,000 $ Accounts receivable 37,000 $ 59,000 $ (22,000) $ Accounts payable 46,000 31,000 15,000 Income taxes payable 4,000 8,500 (4,500) LO 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}