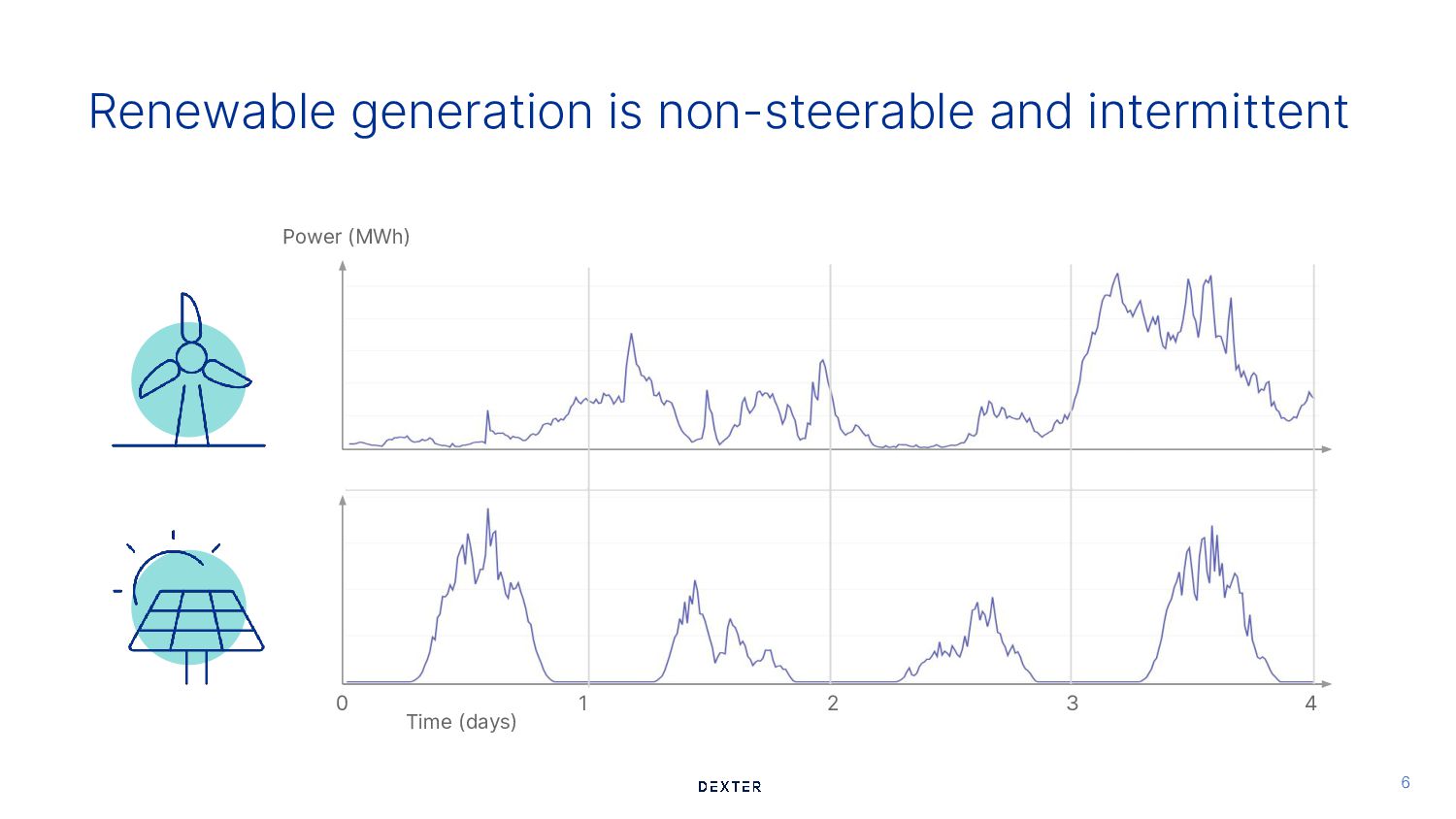

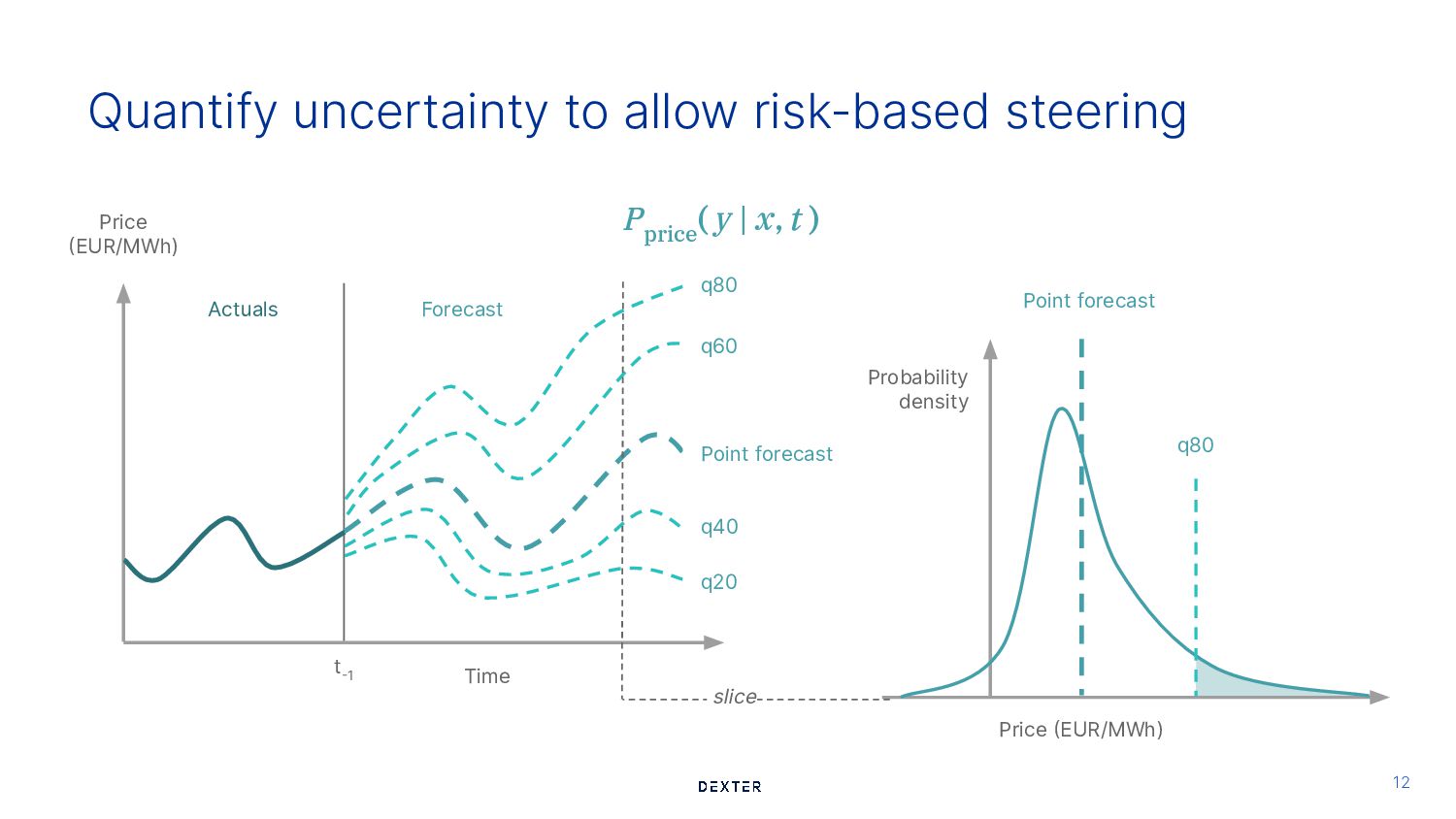

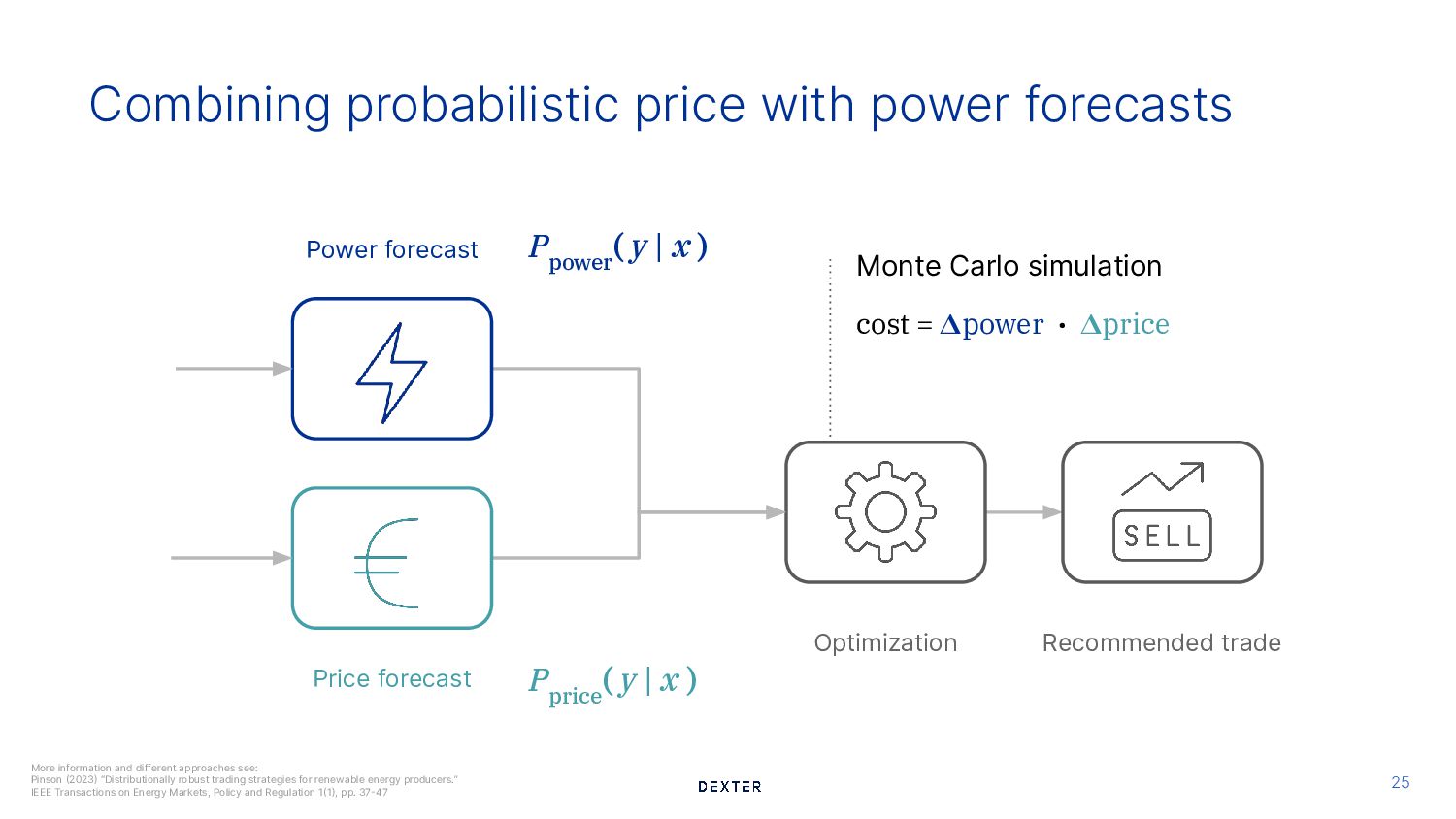

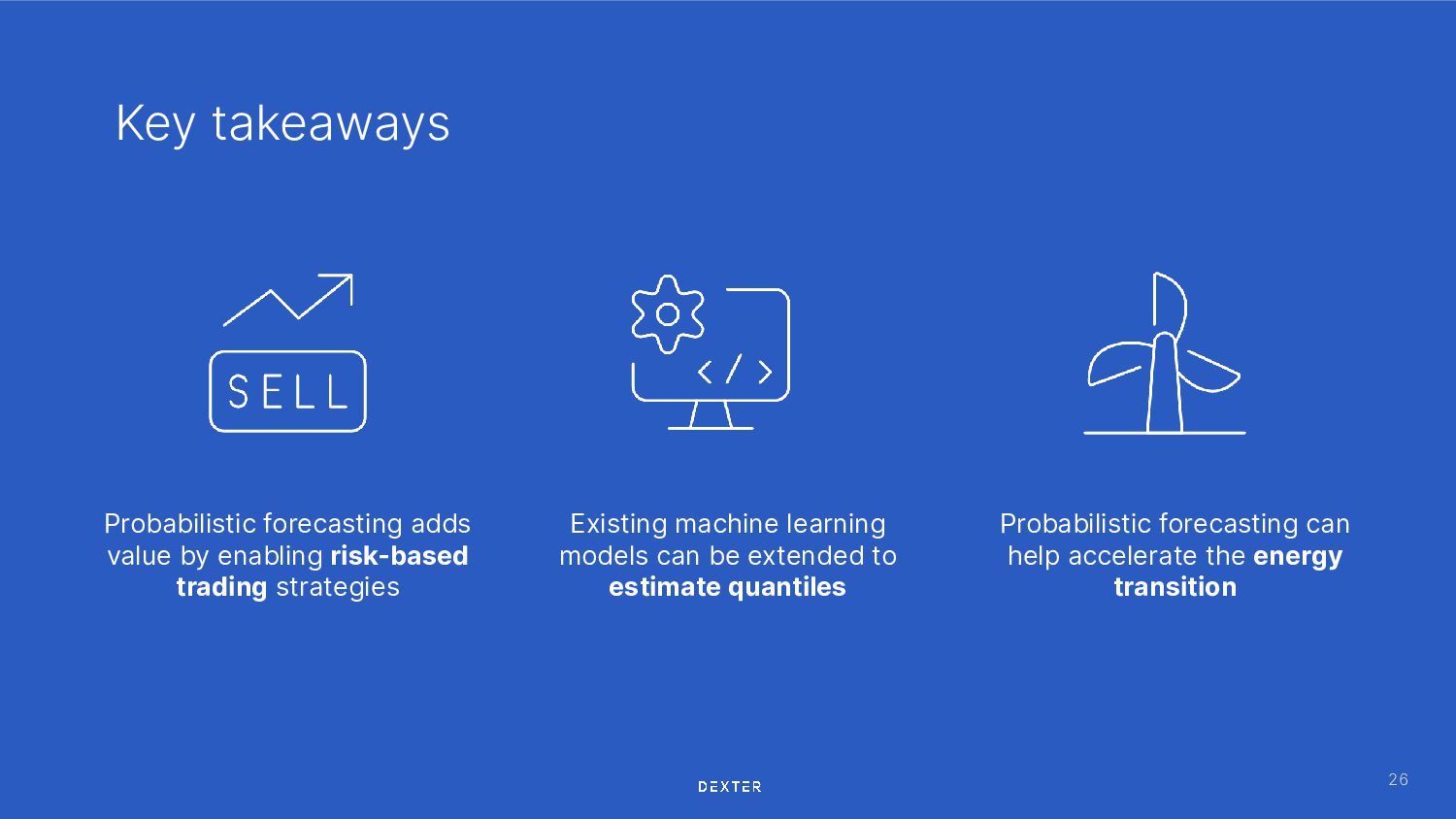

How can probabilistic forecasting accelerate the renewable energy transition? The rapid growth of non-steerable and intermittent wind and solar power requires accurate forecasts and the ability to plan under uncertainty. In this talk, we will make a case for using probabilistic forecasts over deterministic forecasts. We will cover methods for generating and evaluating probabilistic forecasts, and discuss how probabilistic price and wind power forecasts can be combined to derive optimal short-term power trading strategies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}