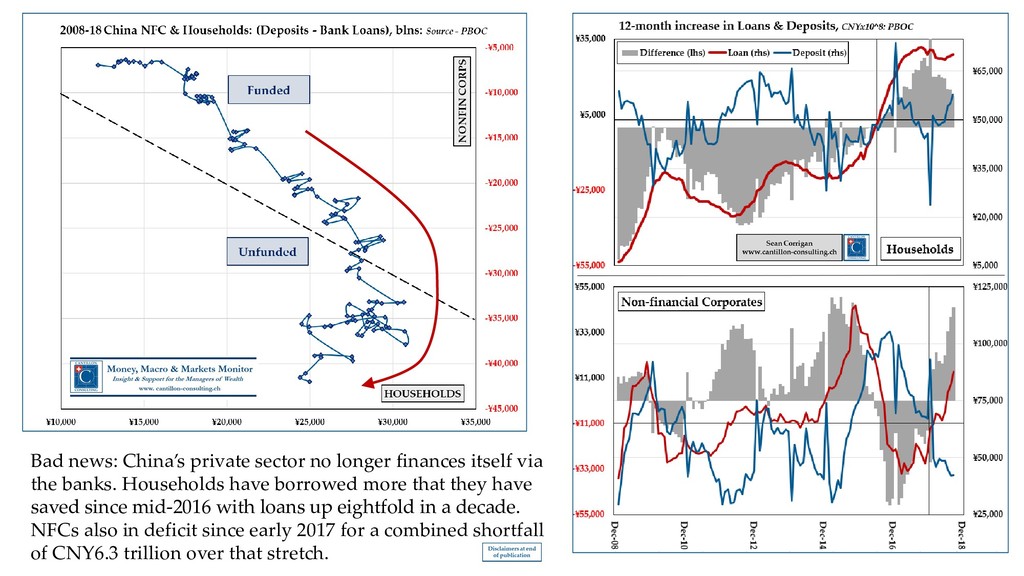

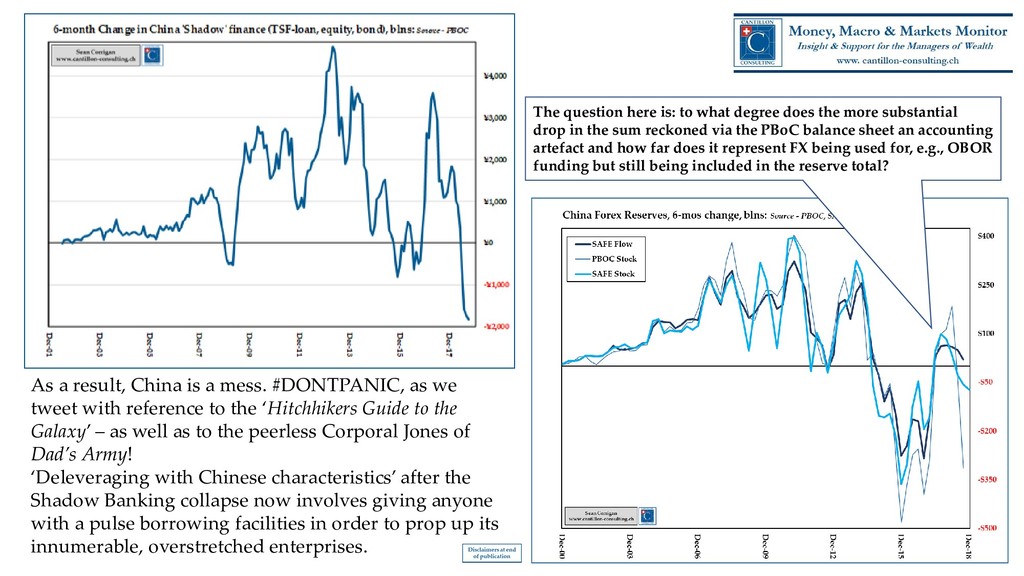

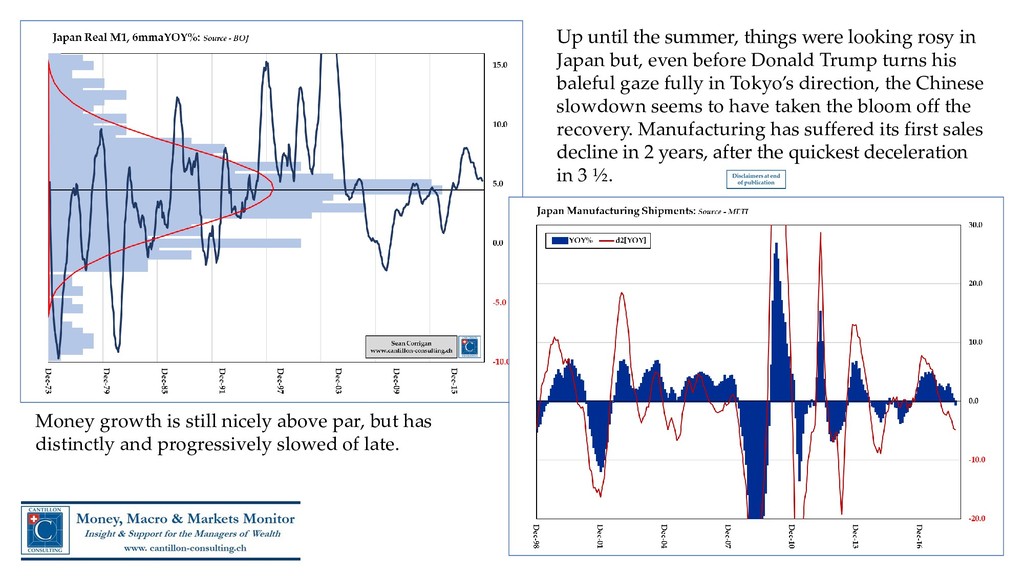

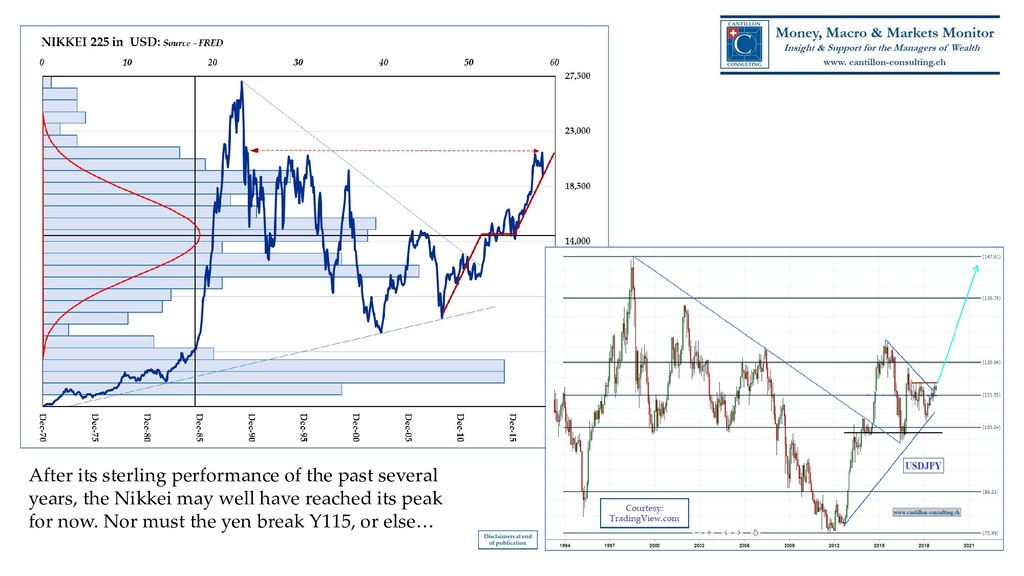

No surprises this time from the Fed - since no surprises either in the broad run of still largely solid data - something which will maintain the pressure on the bond market. China, meanwhile, is finding it harder than ever to keep the plates spinning as the long years of over-borrowing take their much-delayed toll. Europe, too, has hit something of an air pocket - a development which might just give the ECB the excuse we strongly suspect its chiefs are seeking to keep the pedal to the metal. It's a shame that we think the throttle cable has been broken. Finally, in a Japan which has been one of our favoured markets for some good while now, there are the first signs that the cycle may have turned; a reversal which, if confirmed, would coincide with some nice technical signals in the equity market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}