there were over 2.7 million registered companies in the UK* Business Protection gap defined as £1.1 trillion** Corporate debt gap just under £300bn Shareholder protection gap £400bn Key person protection gap £400bn** 39% of business owners said their businesses would fold within 18 months of the death or critical illness of a key person** Sources * http://www.companieshouse.gov.uk/about/businessRegisterStat.shtml ** http://www.legalandgeneralcomms.co.uk/businessprotection/the-business-protection-gap.html

critical illness or dying before his/her 65th birthday 1 in 3 Source:http://zdownload.zurich.co.uk/document/pdf/zurich/campaigns/card2.pdf Loss of Keyperson….

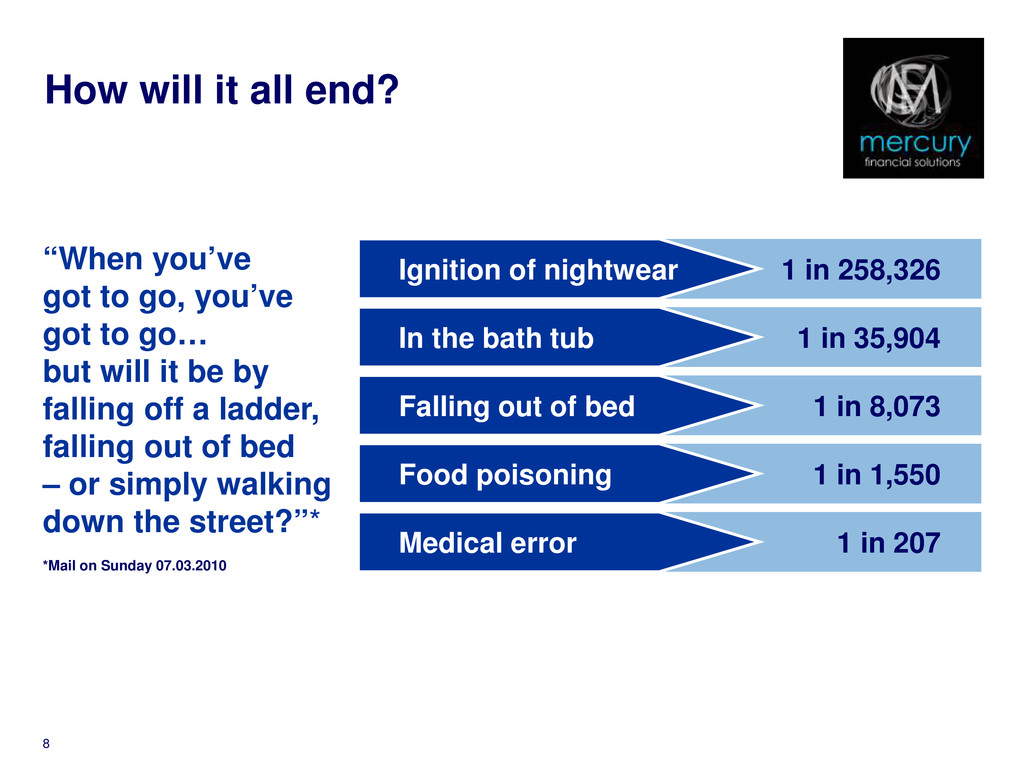

go, you’ve got to go… but will it be by falling off a ladder, falling out of bed – or simply walking down the street?”* *Mail on Sunday 07.03.2010 1 in 258,326 Ignition of nightwear 1 in 35,904 In the bath tub 1 in 8,073 Falling out of bed 1 in 1,550 Food poisoning 1 in 207 Medical error

Enables business to recruit and train a replacement • Support cash flow • Maintain value of business/shareholding 10 Risk and cash flow • Provides time and space to re-organise • Decreases unwanted attention from creditors

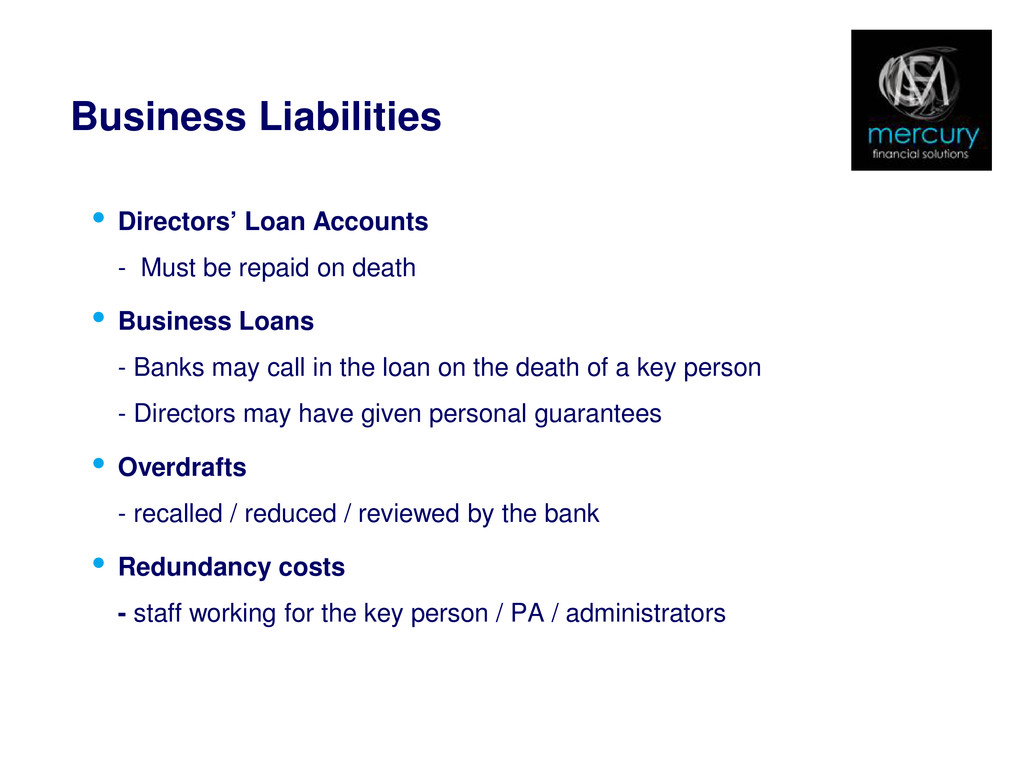

on death • Business Loans - Banks may call in the loan on the death of a key person - Directors may have given personal guarantees • Overdrafts - recalled / reduced / reviewed by the bank • Redundancy costs - staff working for the key person / PA / administrators

C Spouse A Owner B Owner C Owner B Ch ren ild A dies or even Problems for owner A’s beneficiaries: • Own a share of a company they may know nothing about • Loss of owner A’s income • No buyer for shares • If buyer found, at what price? • In addition to emotional issues with the loss. Problems for owners B and C • New shareholder(s) could cause unwanted interference • Loss of control • Cannot afford to buy shares from beneficiaries

a small, successful company, and is a high earner. • Over the years he has built up a substantial pension fund. • He wants death in service benefit through the company and is worried about the benefits forming part of his lifetime allowance.

pays for it and places it under a Relevant Life Policy Trust Life cover paid out on Ali’s death and paid to his family • Must be an employee, including directors. • The business can be a limited company, a partnership, a charity or a sole trader. • Cannot be used for sole traders or equity partners who are taxed under schedule D to provide cover for themselves. • 'Salaried' partners who are taxed as schedule E can be covered.

a month for his life assurance. Cost to Ali as a Director paying personally Monthly premium = £200.00 Pre-tax Income to fund £200 at Income Tax rate of 40%* and National Insurance at 2%* = £344.83 Cost with employers National Insurance Contributions at 13.8% on this salary = £392.41 Gross Salary and National Insurance are allowable deductions against Corporation Tax at 20%* Total monthly cost to Ali and LBD Ltd Company = £313.93

plan Monthly premium = £200.00 No employee Income Tax or National Insurance No employer National Insurance Relevant life policy is an allowable deduction against corporation tax at 20%* Total Cost to LBD Ltd Company = £160.00 Cost to Ali and LBD Ltd company paying personally = £313.93 Cost to LBD Ltd Company paying through RLPT = £160.00 Saving = £ 153.93 or 49%

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}