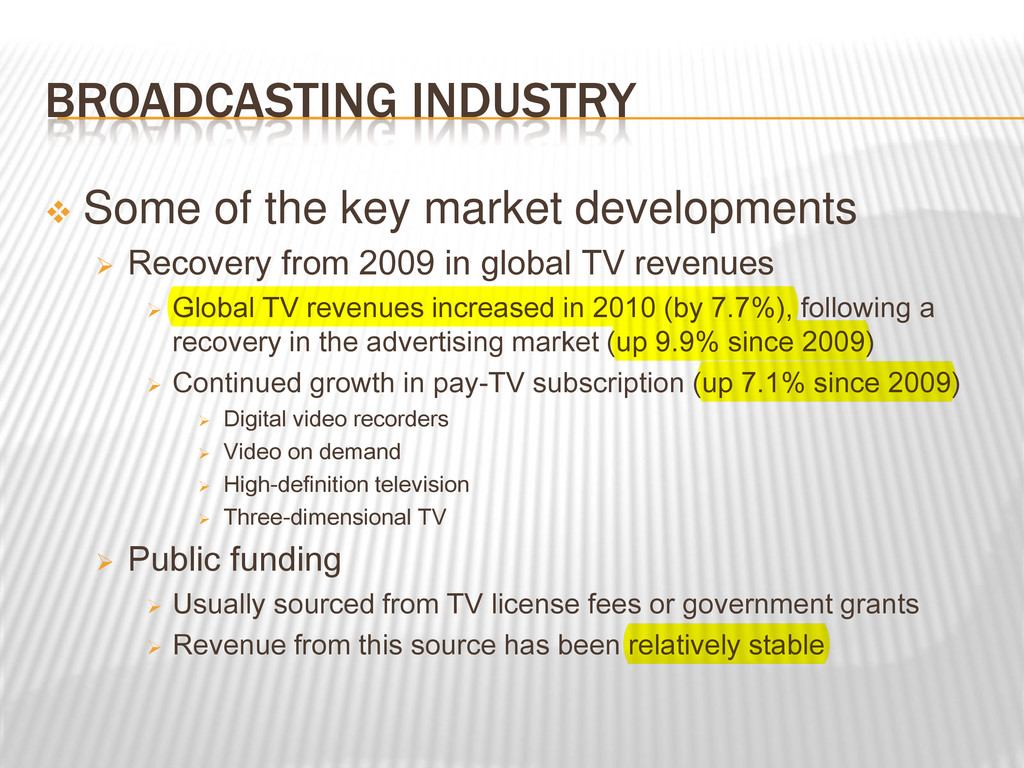

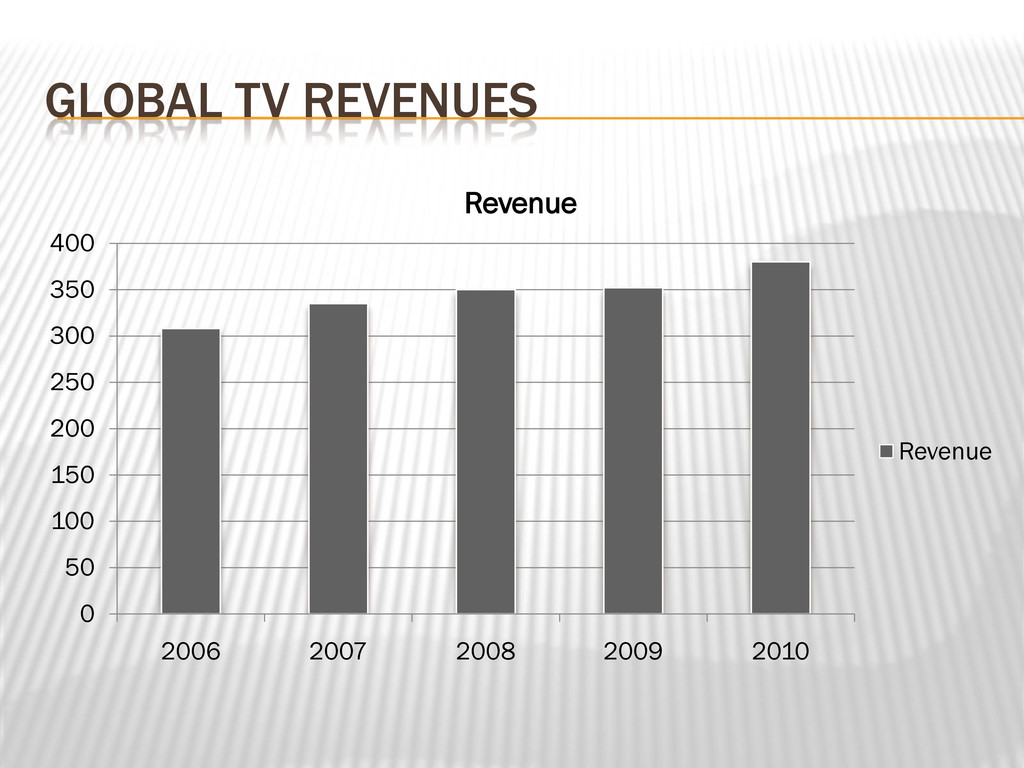

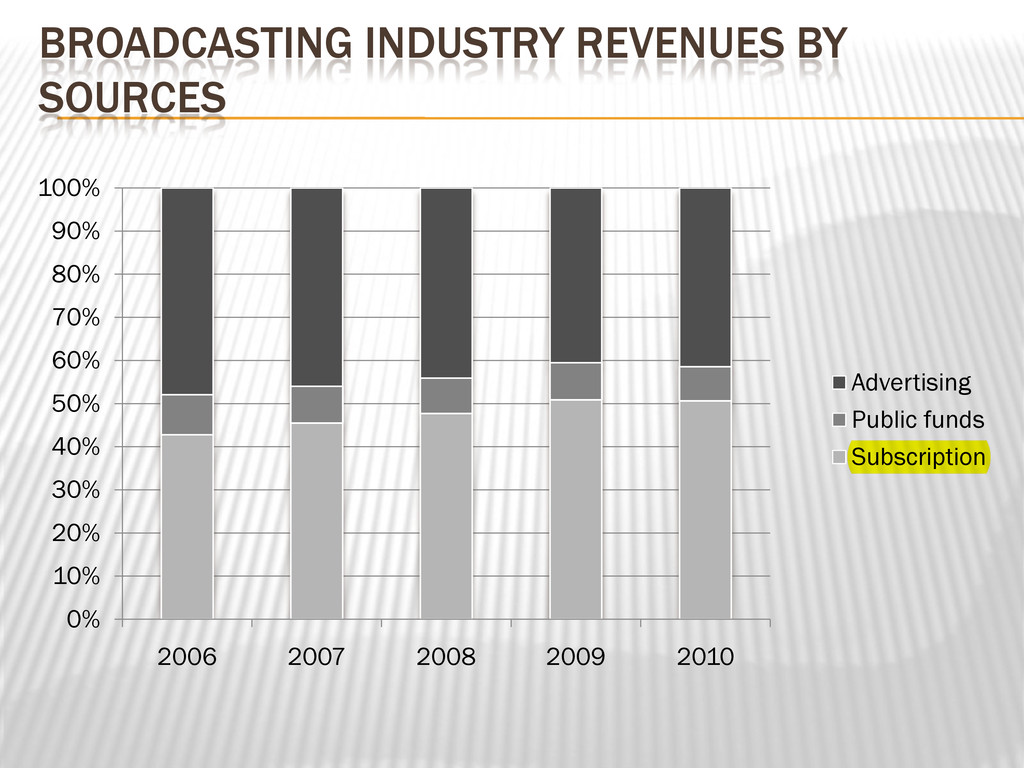

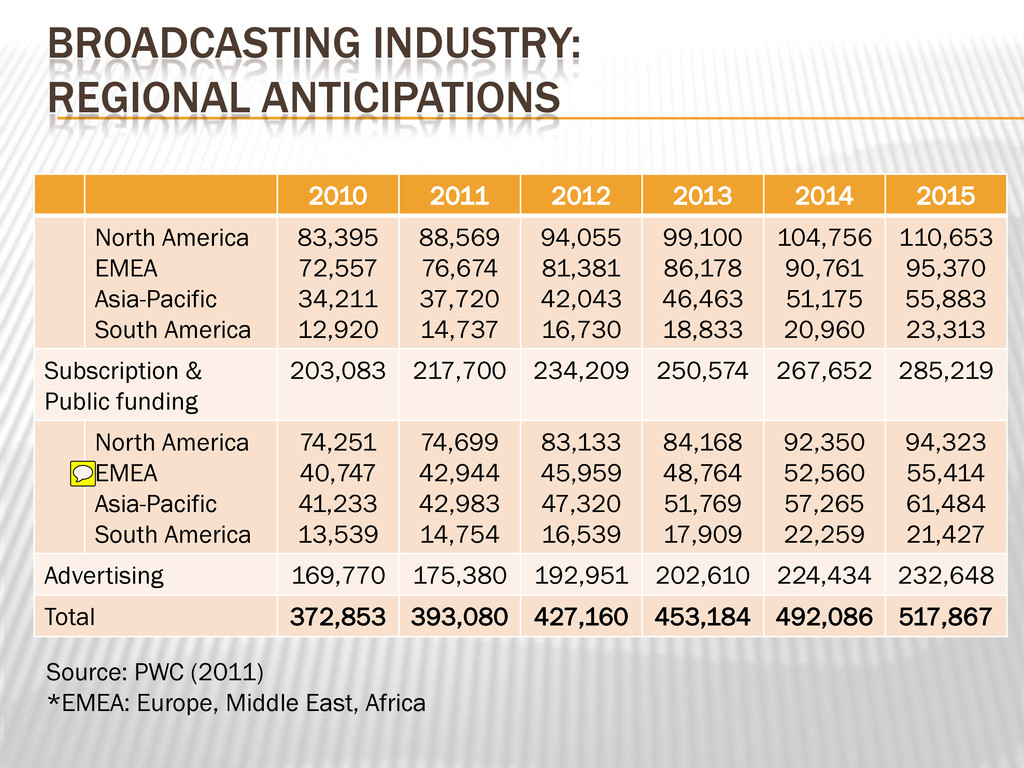

North America EMEA Asia-Pacific South America 83,395 72,557 34,211 12,920 88,569 76,674 37,720 14,737 94,055 81,381 42,043 16,730 99,100 86,178 46,463 18,833 104,756 90,761 51,175 20,960 110,653 95,370 55,883 23,313 Subscription & Public funding 203,083 217,700 234,209 250,574 267,652 285,219 North America EMEA Asia-Pacific South America 74,251 40,747 41,233 13,539 74,699 42,944 42,983 14,754 83,133 45,959 47,320 16,539 84,168 48,764 51,769 17,909 92,350 52,560 57,265 22,259 94,323 55,414 61,484 21,427 Advertising 169,770 175,380 192,951 202,610 224,434 232,648 Total 372,853 393,080 427,160 453,184 492,086 517,867 Source: PWC (2011) *EMEA: Europe, Middle East, Africa

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}