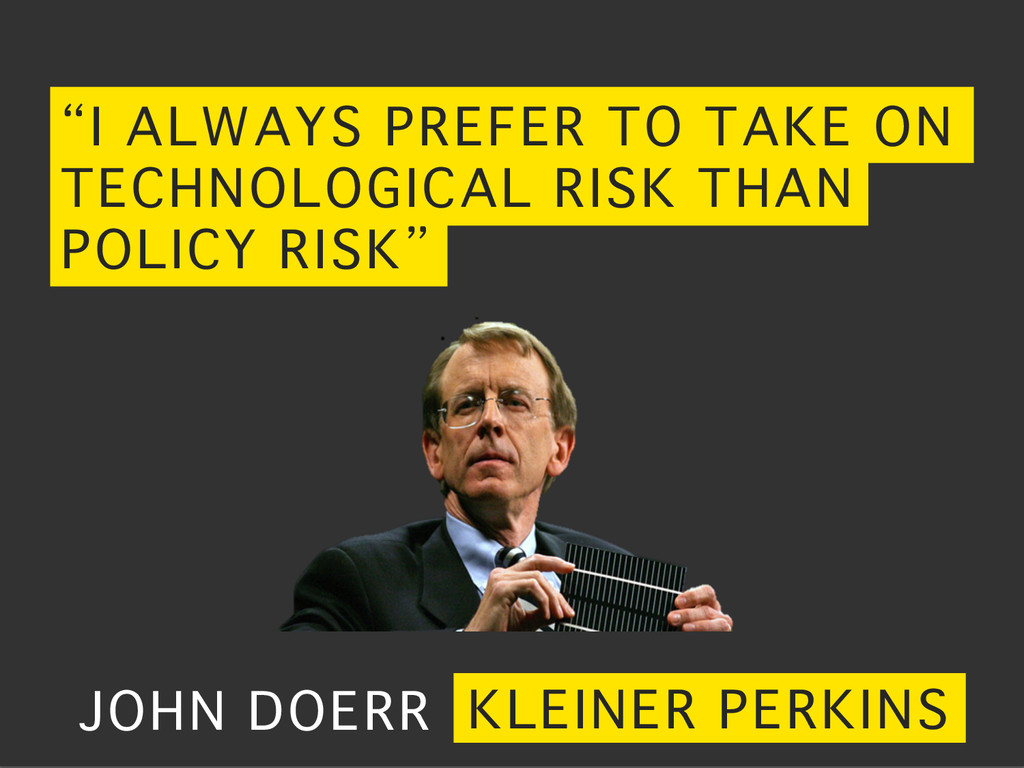

PREMISE� First, while entrepreneurs and VCs are great at dealing with technological, market, and operational risks, they are poorly equipped to to assess and mitigate regulatory and legal risks. There are a lot of interesting reasons why this is the case, but that’s beyond our scope here. �

PREMISE� This is important, because we’ve passed an inflection point. The last generation of great startups – the Facebooks, Googles, and Amazons – disrupted among the least regulated facets of the American economy: how we communicate with each other, and how we buy stuff.�

PREMISE� This is important, because we’ve passed an inflection point. The last generation of great startups – the Facebooks, Googles, and Amazons – disrupted among the least regulated facets of the American economy: how we communicate with each other, and how we buy stuff.�

PREMISE� This is important, because we’ve passed an inflection point. The last generation of great startups – the Facebooks, Googles, and Amazons – disrupted among the least regulated facets of the American economy: how we communicate with each other, and how we buy stuff.�

PREMISE� This is important, because we’ve passed an inflection point. The last generation of great startups – the Facebooks, Googles, and Amazons – disrupted among the least regulated facets of the American economy: how we communicate with each other, and how we buy stuff.�

PREMISE� The next generation of disruptive startups – the Airbnbs and Ubers, the personalized genomics companies, the bitcoin-based financial services companies – are going to come in industries that are highly regulated.�

PREMISE� The next generation of disruptive startups – the Airbnbs and Ubers, the personalized genomics companies, the bitcoin-based financial services companies – are going to come in industries that are highly regulated.�

PREMISE� The next generation of disruptive startups – the Airbnbs and Ubers, the personalized genomics companies, the bitcoin-based financial services companies – are going to come in industries that are highly regulated.�

PREMISE� Putting 1. and 2. together, it becomes clear that VCs and entrepreneurs need better tools to deal with regulatory and legal risks. Those tools are the focus of the rest of this talk.�

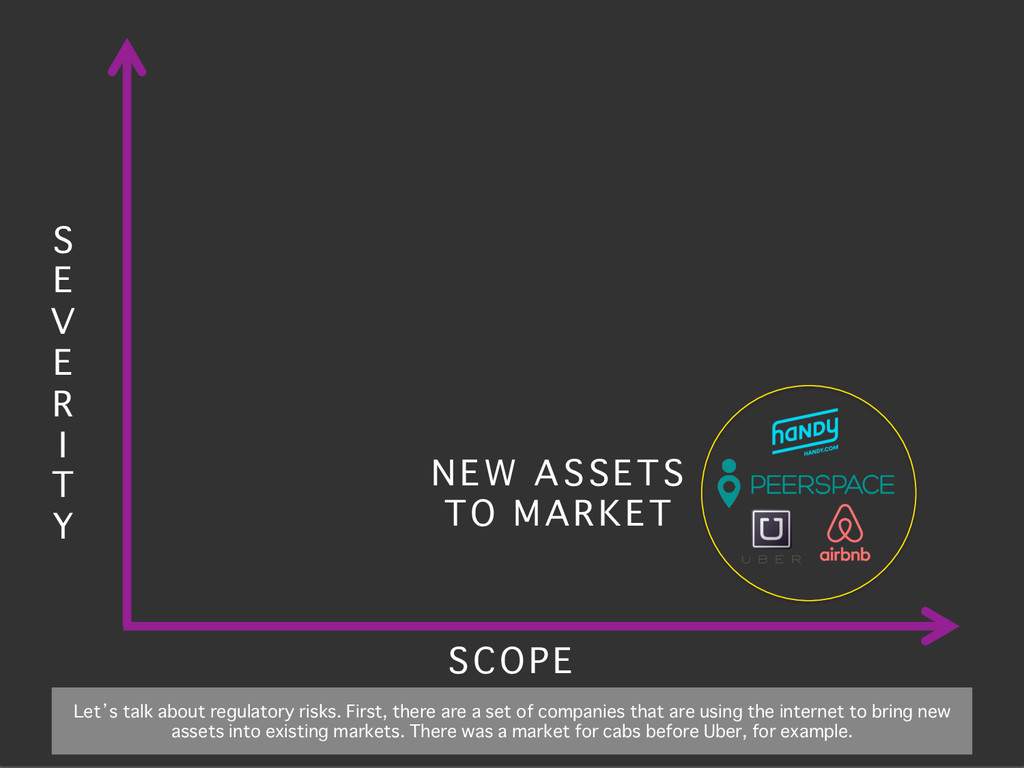

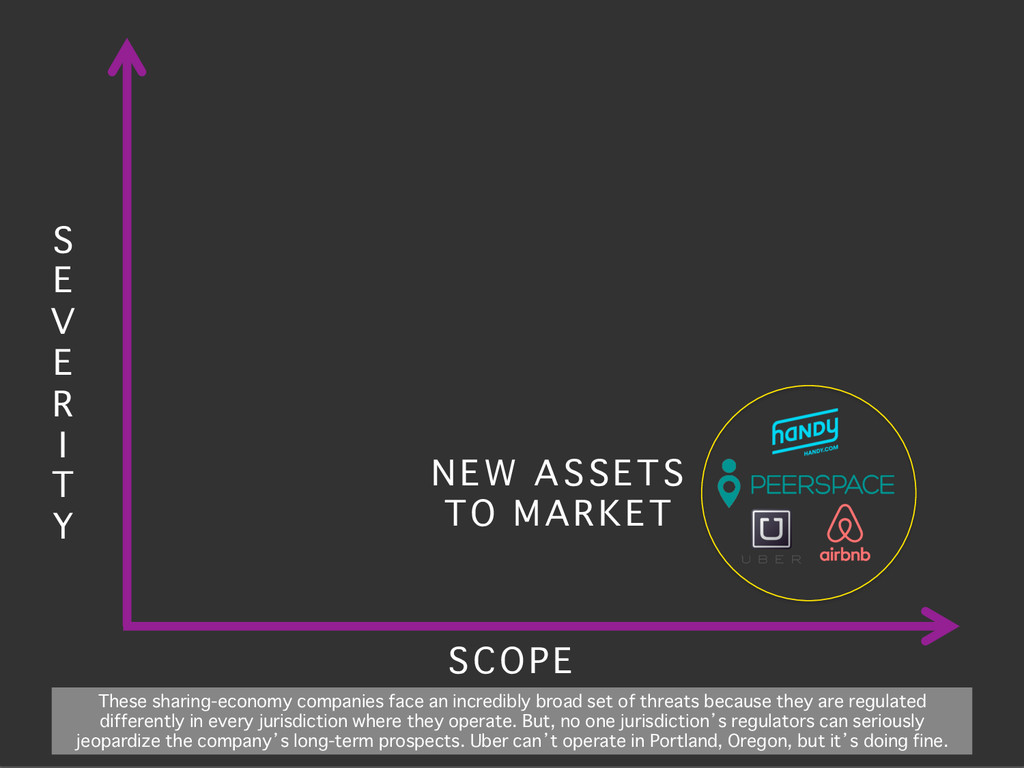

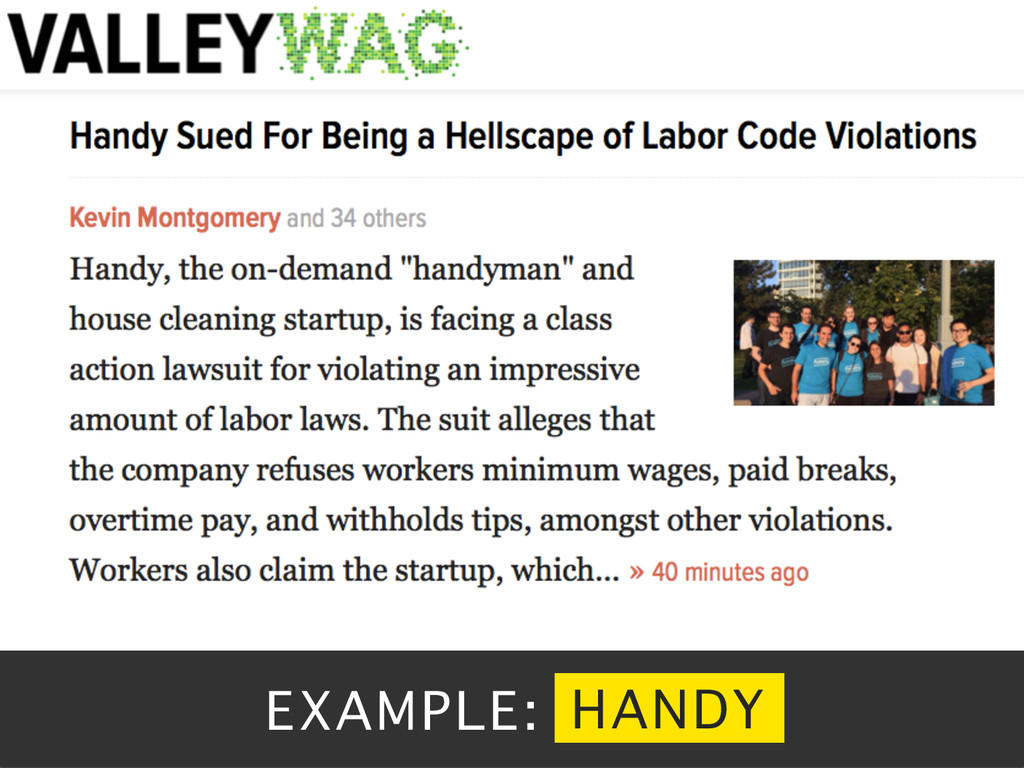

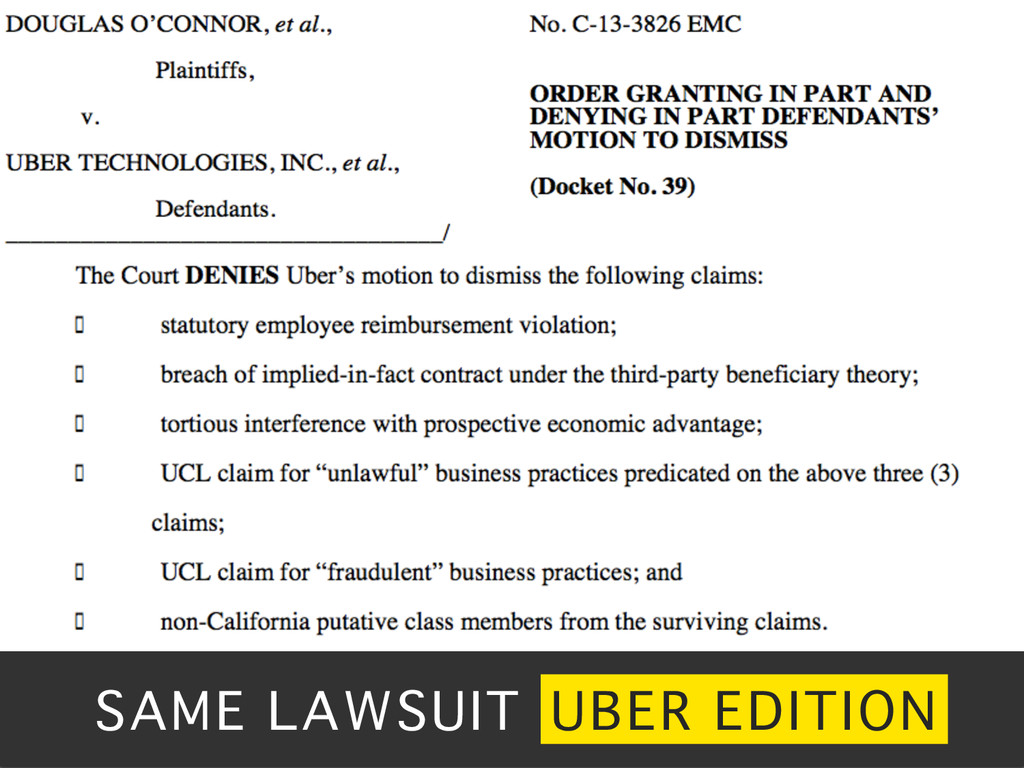

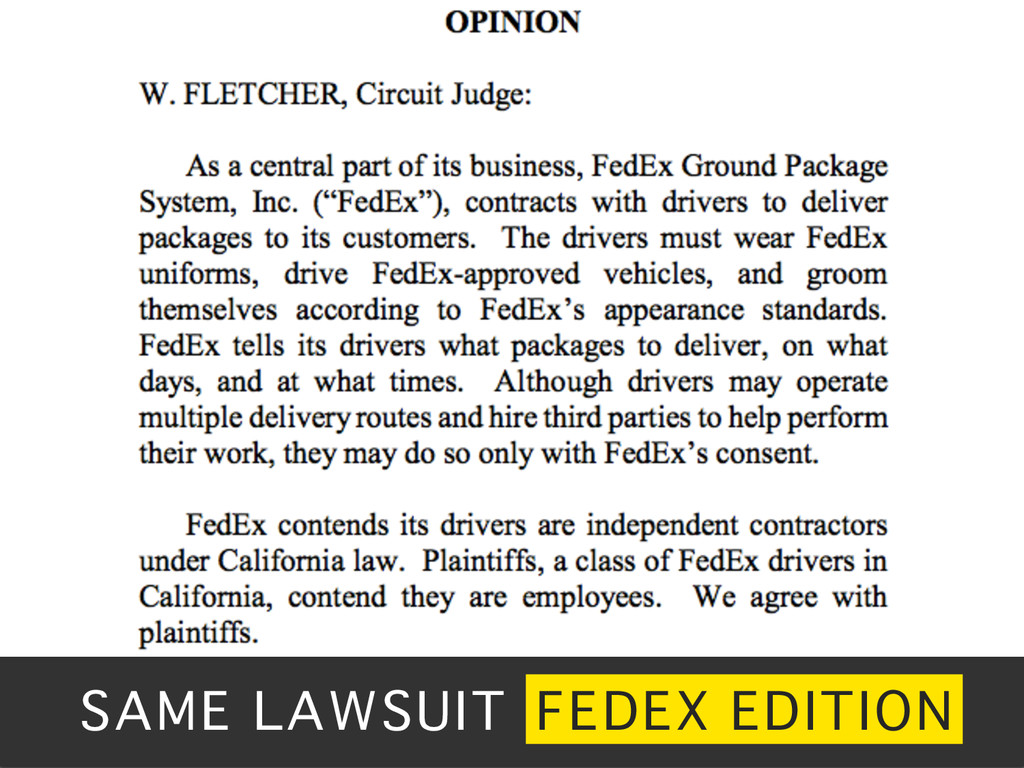

a set of companies that are using the internet to bring new assets into existing markets. There was a market for cabs before Uber, for example. � SCOPE� S E V E R I T Y� NEW ASSETS � TO MARKET�

of threats because they are regulated differently in every jurisdiction where they operate. But, no one jurisdiction’s regulators can seriously jeopardize the company’s long-term prospects. Uber can’t operate in Portland, Oregon, but it’s doing fine. � SCOPE� S E V E R I T Y� NEW ASSETS � TO MARKET�

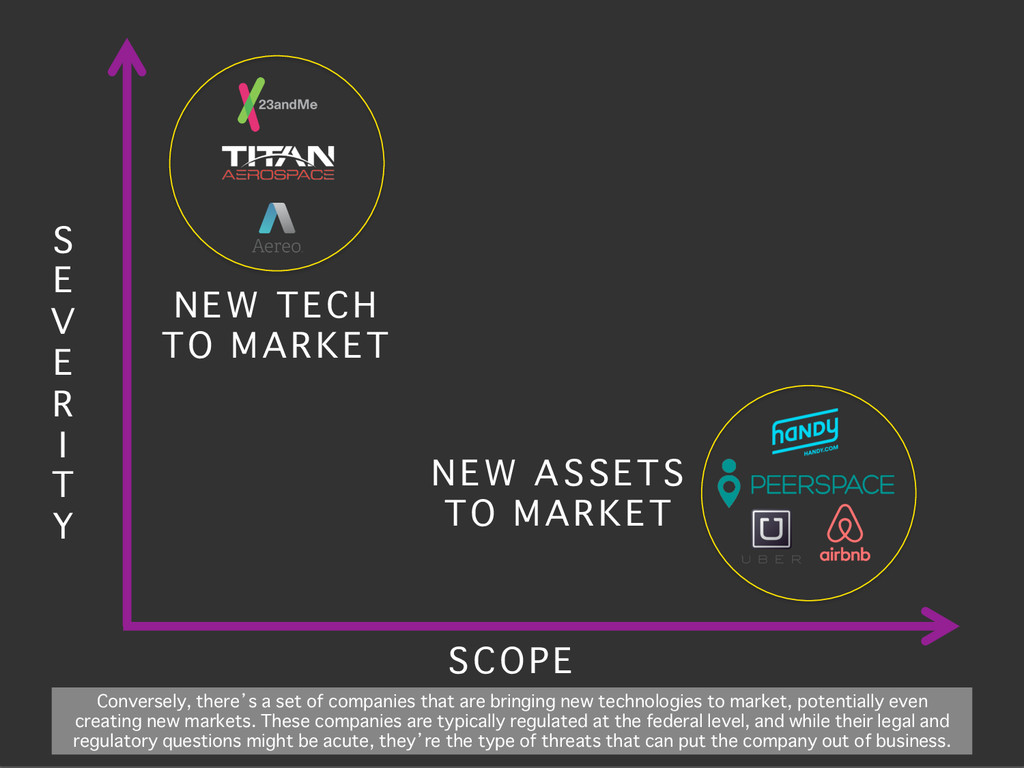

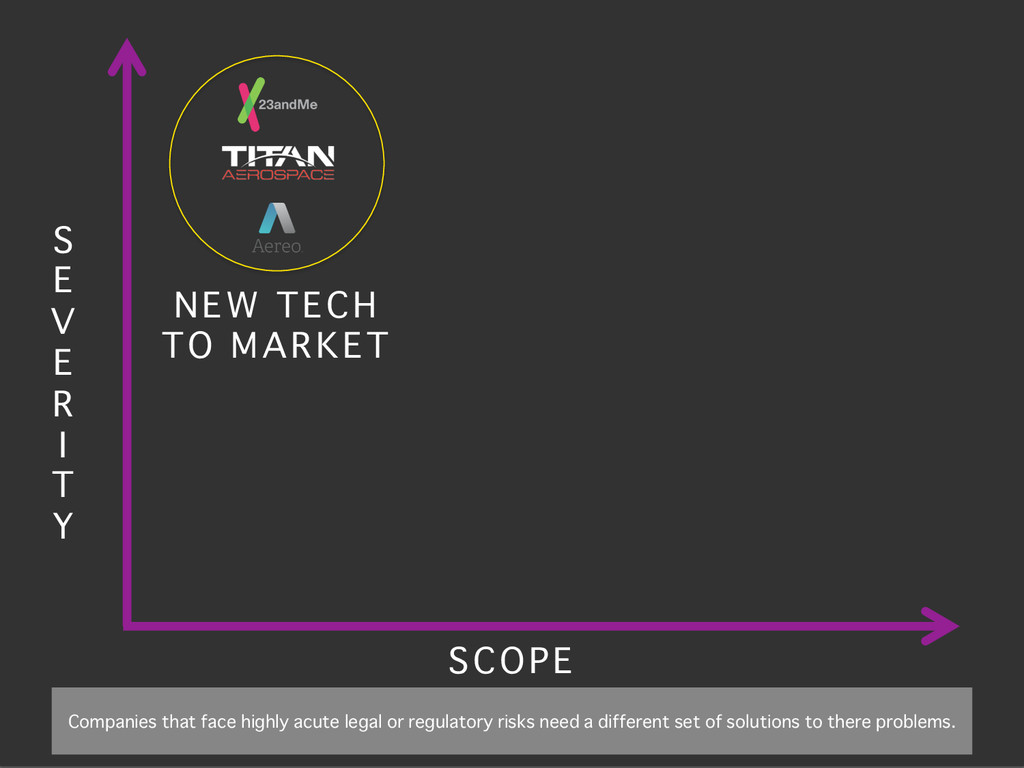

bringing new technologies to market, potentially even creating new markets. These companies are typically regulated at the federal level, and while their legal and regulatory questions might be acute, they’re the type of threats that can put the company out of business. � SCOPE� S E V E R I T Y� NEW ASSETS � TO MARKET� NEW TECH� TO MARKET�

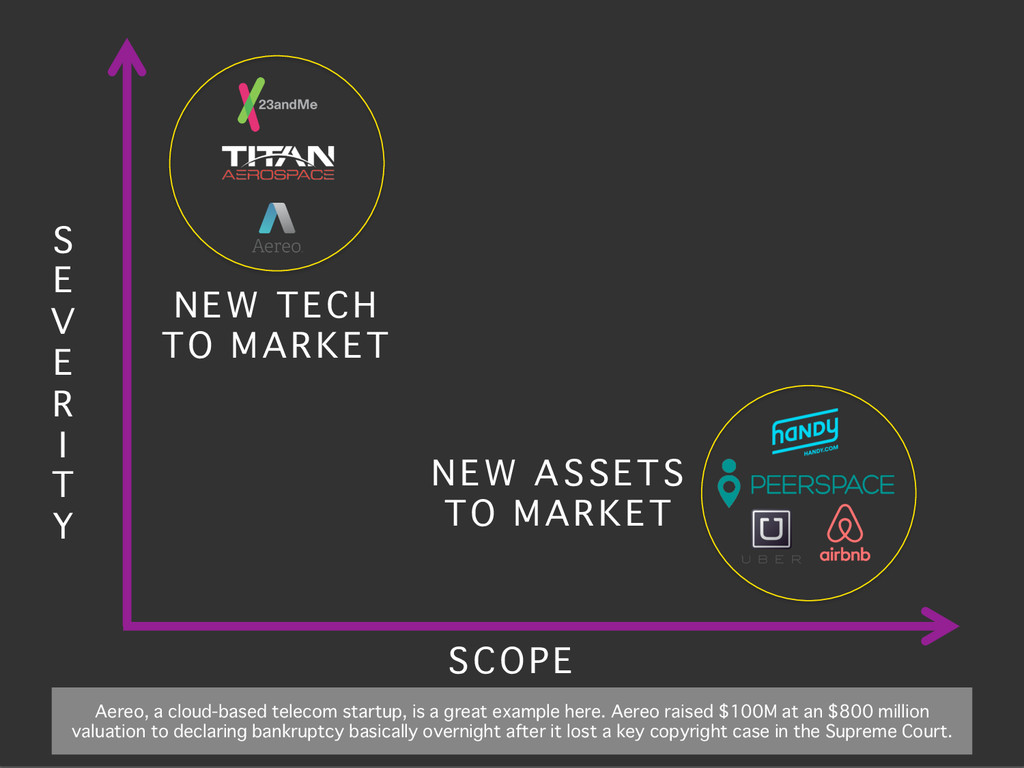

example here. Aereo raised $100M at an $800 million valuation to declaring bankruptcy basically overnight after it lost a key copyright case in the Supreme Court.� SCOPE� S E V E R I T Y� NEW ASSETS � TO MARKET� NEW TECH� TO MARKET�

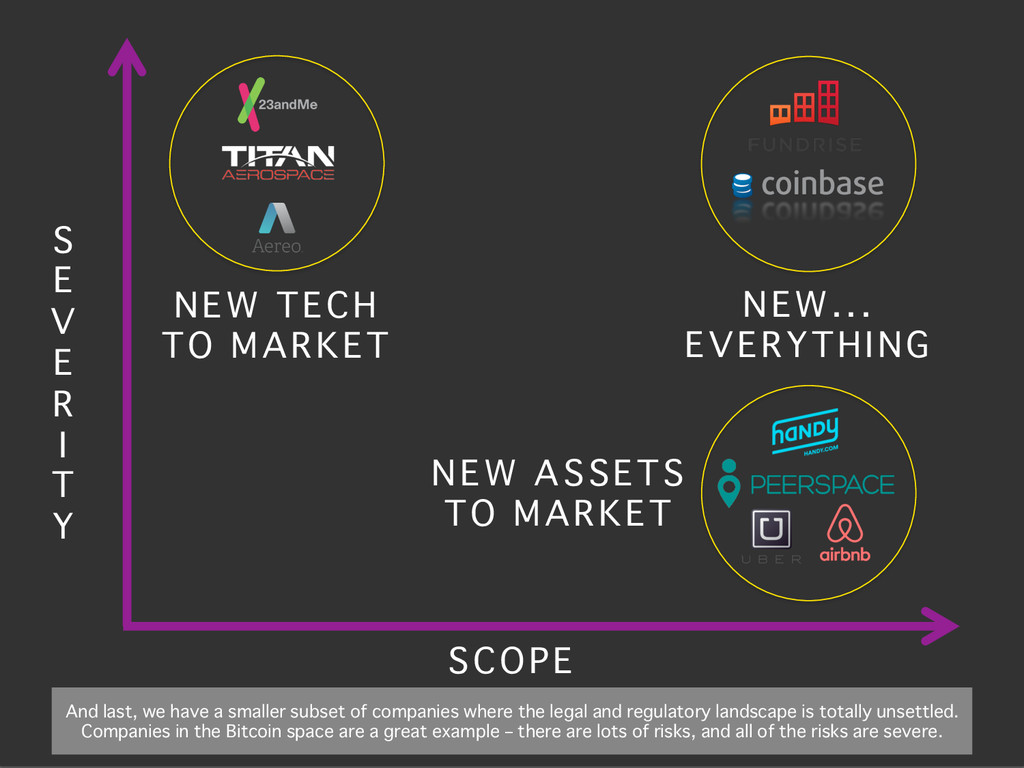

companies where the legal and regulatory landscape is totally unsettled. Companies in the Bitcoin space are a great example – there are lots of risks, and all of the risks are severe. � SCOPE� S E V E R I T Y� NEW ASSETS � TO MARKET� NEW TECH� TO MARKET� NEW...� EVERYTHING�

we’re in DC, and lobbying is boring, so I’m not going to say much except to point out that Uber has done a great job generating grassroots support in local political matters.�

Law is doing – developing a legal platform for “1099 economy” companies to manage relationships with independent contractors, in order to reduce the risk of violating local and federal labor laws. InSITE alum Vinay Jain is Shake Law’s chief legal officer, btw.�

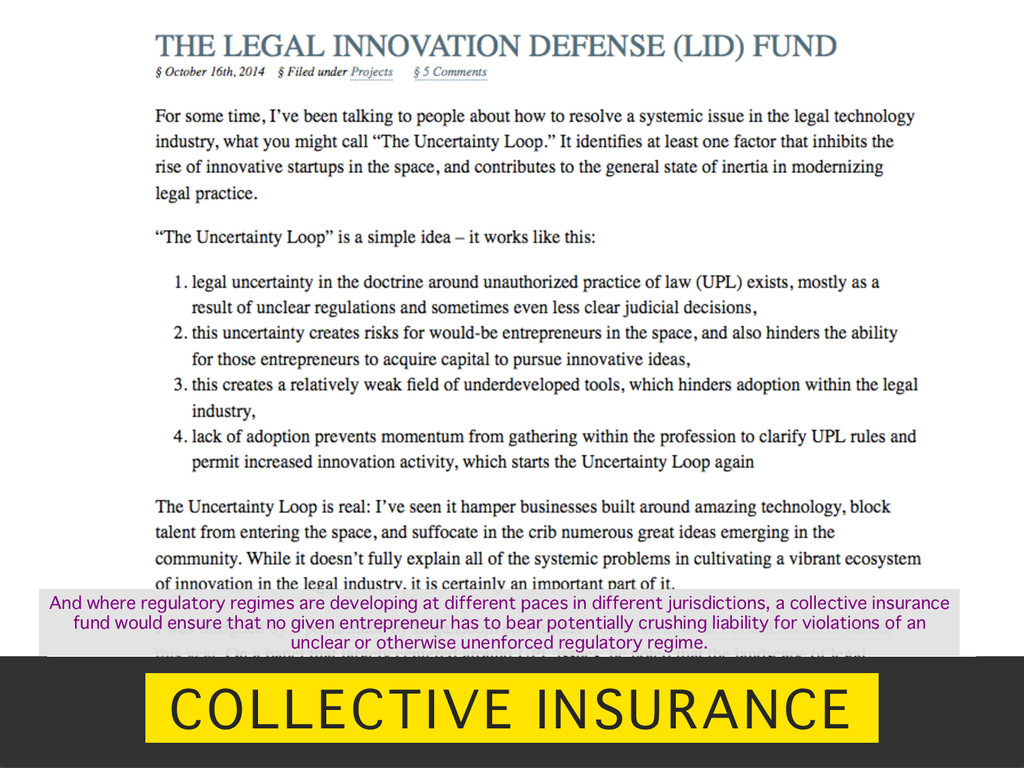

at different paces in different jurisdictions, a collective insurance fund would ensure that no given entrepreneur has to bear potentially crushing liability for violations of an unclear or otherwise unenforced regulatory regime.�

here involves the financial markets. You can think about venture capital as a way of using finance to spread the technological, market, and operational risks that startups face. �

to finance legal risks; a number of litigation finance firms have launched recently. VCs could use these products as a hedging strategy when investing in a startup like Aereo (which was inevitably going to get sued by the major cable companies...).�

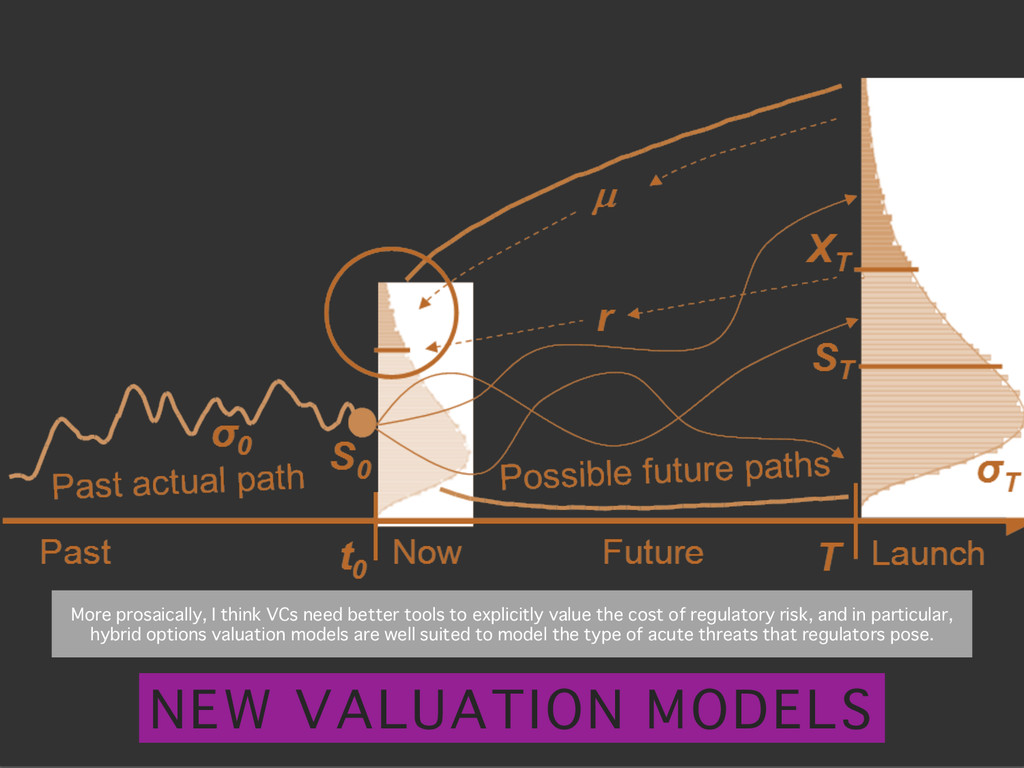

need better tools to explicitly value the cost of regulatory risk, and in particular, hybrid options valuation models are well suited to model the type of acute threats that regulators pose. �

in order to explicitly model the costs of legal or regulatory risk, you need to have a sense of what the likely outcomes are. There are a couple cool startups that are taking a big-data approach to legislation and regulation.�

predictive tools to generate insights into whether certain legislation is likely to pass, and it’s working on a regulatory forecasting engine as well.�

landscape is totally unsettled, time is essential – the democratic and regulatory processes just need to play out. � SCOPE� S E V E R I T Y� NEW...� EVERYTHING�

interesting idea here came from the newest FCC commissioner, Jessica Rosenworcel, who borrowed a software programming term. Commissioner Rosenworcel’s proposal suggests that federal regulatory agencies carve out areas where the typical regulatory regimes don’t apply.�

out disruptive ideas that otherwise might be illegal, even though they’re not necessarily harmful and might yield net benefits. This would be a big step for risk-averse federal regulators, but it’s still a good idea.�

idea that “states are the laboratories of democracy” – that four states, to give one example, can legalize self-driving cars, and the other 46 states get to watch and see what happens in California, Neva. �

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[email protected]� www.joevladeck.com/insite�](https://files.speakerdeck.com/presentations/4b04f1f0780f01327d2b36d65006dff2/slide_33.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}