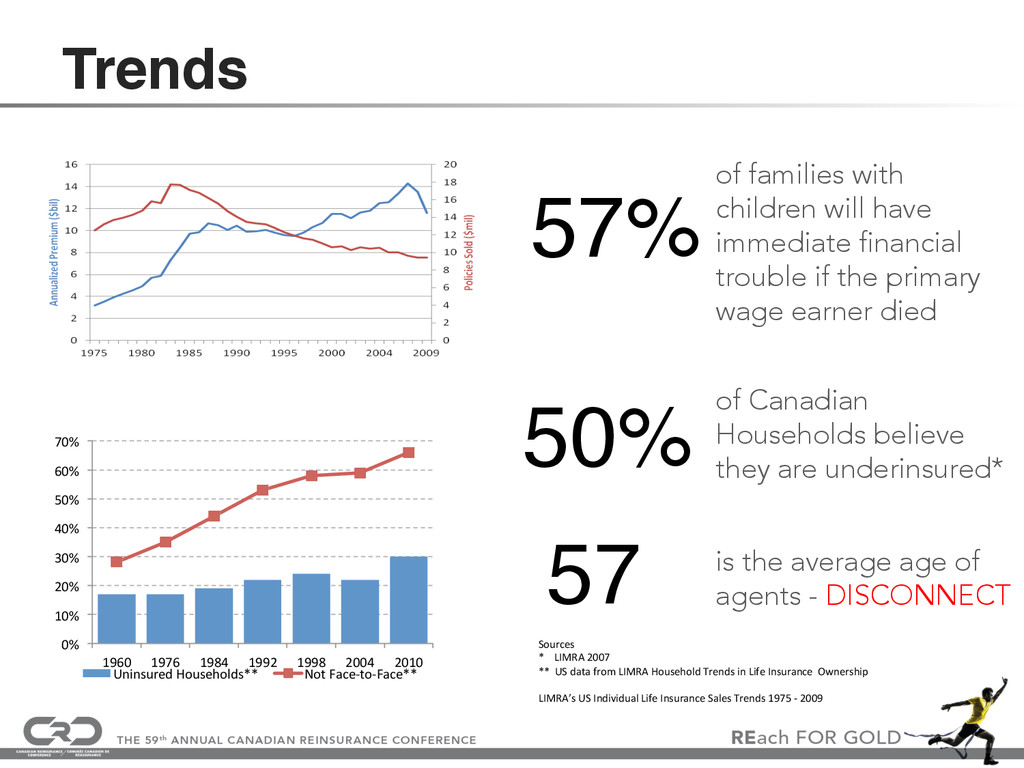

There is an estimated unmet need for $1 Trillion in additional life insurance in Canada. Small evolutionary changes in our market are unlikely to materially reduce this gap. The panel will provide real examples of innovation execution in other territories, and speculate as to their applicability in our market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}