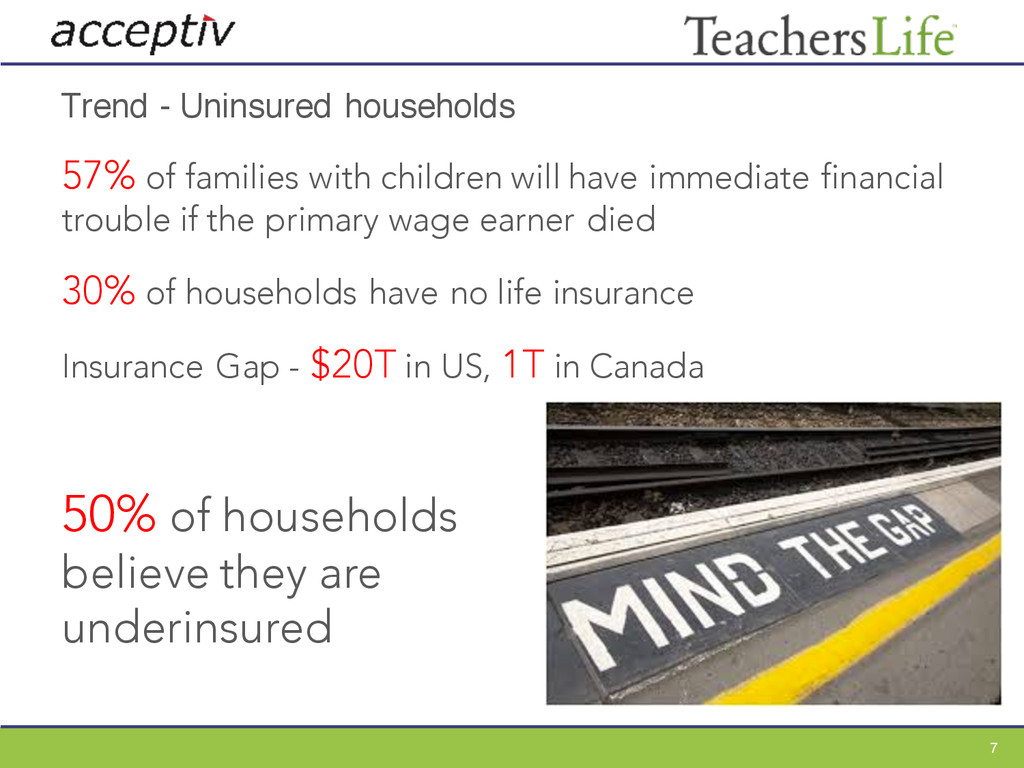

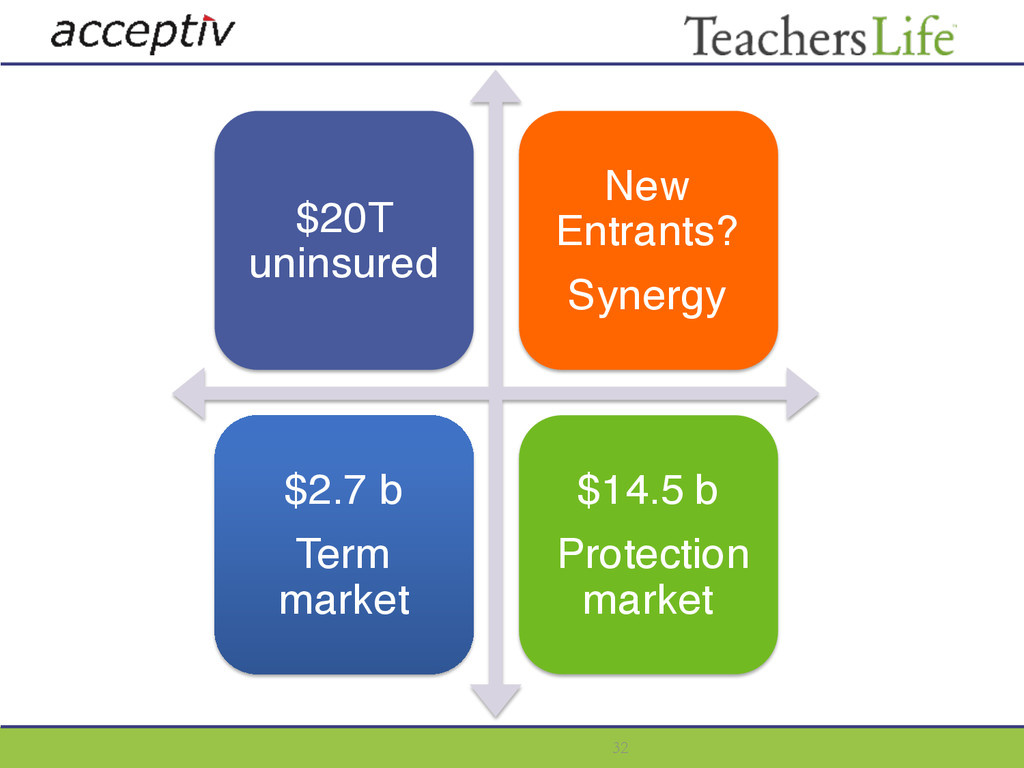

have immediate financial trouble if the primary wage earner died 30% of households have no life insurance Insurance Gap - $20T in US, 1T in Canada 50% of households believe they are underinsured 7

oversight of insurance companies Capital adequacy Policyholder protection Complex Infrastructure Systems Processes Brand Reputation LIFE INSURANCE IS SOLD NOT BOUGHT 9

not possible Fraternals have a reason to do what we do (beyond profit) But, we are still competing in the same market and (most likely) for the same customers. 10

banks Brand and Advertising can be lost, especially through intermediaries How can Teachers Life compete in this market? Responsibility to members to offer best terms possible? 13

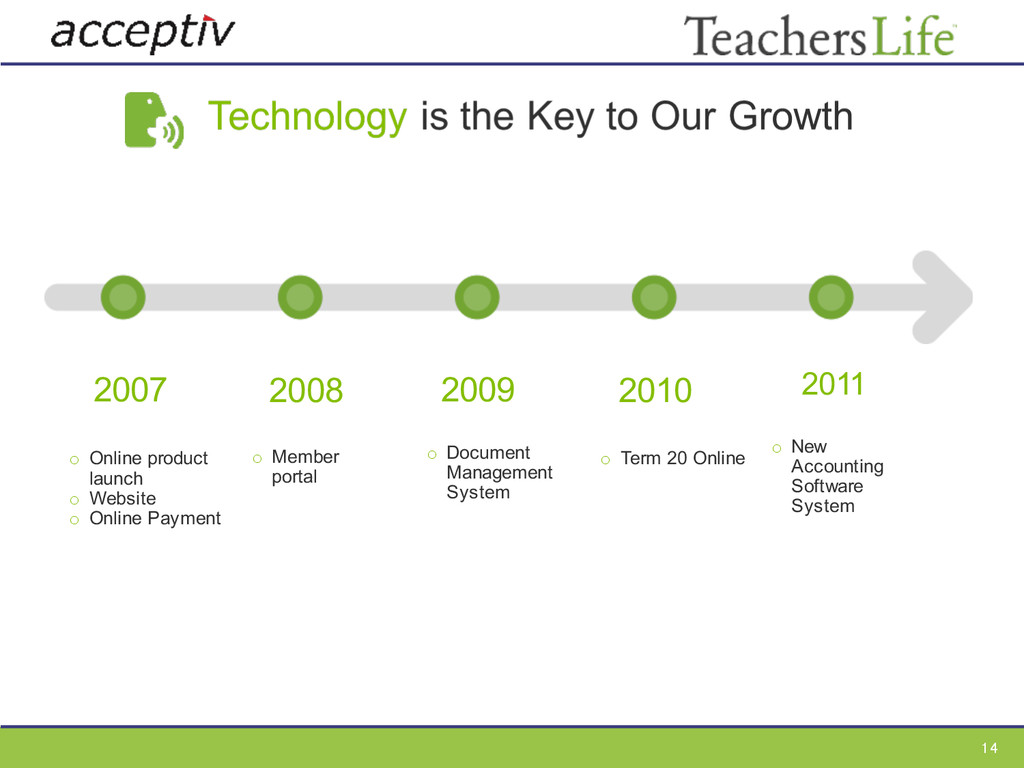

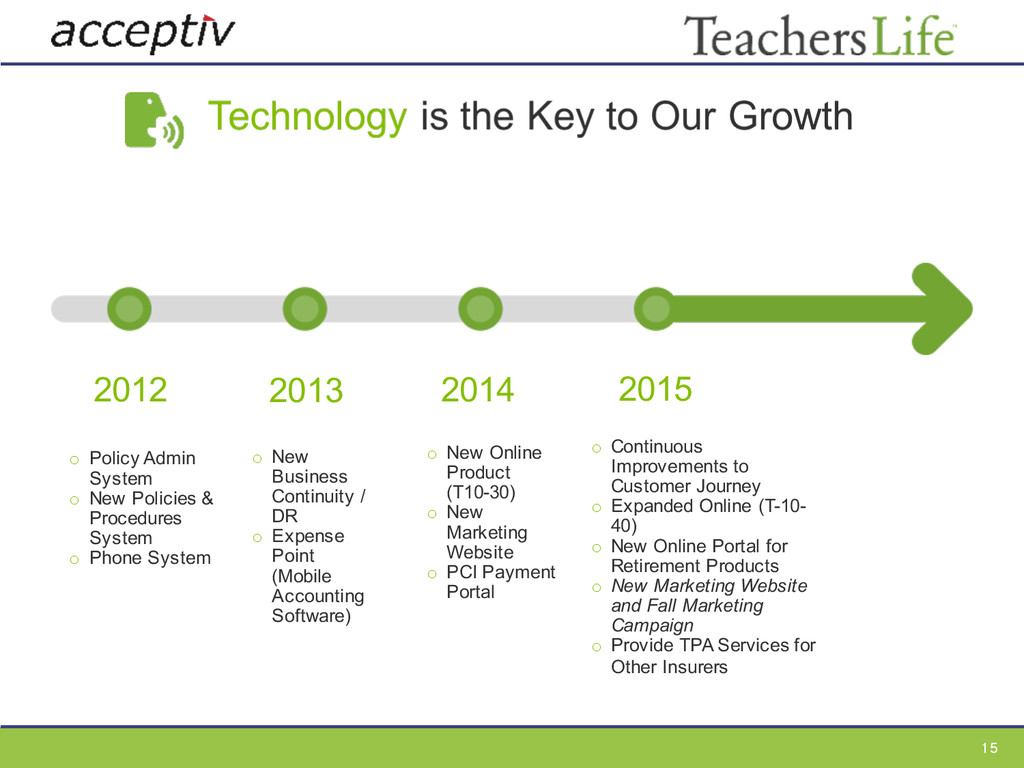

Continuity / DR o Expense Point (Mobile Accounting Software) o Policy Admin System o New Policies & Procedures System o Phone System o New Online Product (T10-30) o New Marketing Website o PCI Payment Portal o Continuous Improvements to Customer Journey o Expanded Online (T-10- 40) o New Online Portal for Retirement Products o New Marketing Website and Fall Marketing Campaign o Provide TPA Services for Other Insurers

small company. The worst thing… Our Weaknesses are our Virtues 16 Agility to respond – we had put ourselves into a position to capitalize on the new online opportunity Decision-making The ‘cost’ of technology relatively speaking is within the reach of small organizations Strong partnerships – outsourcing is key Ability to ‘punch above our weight’

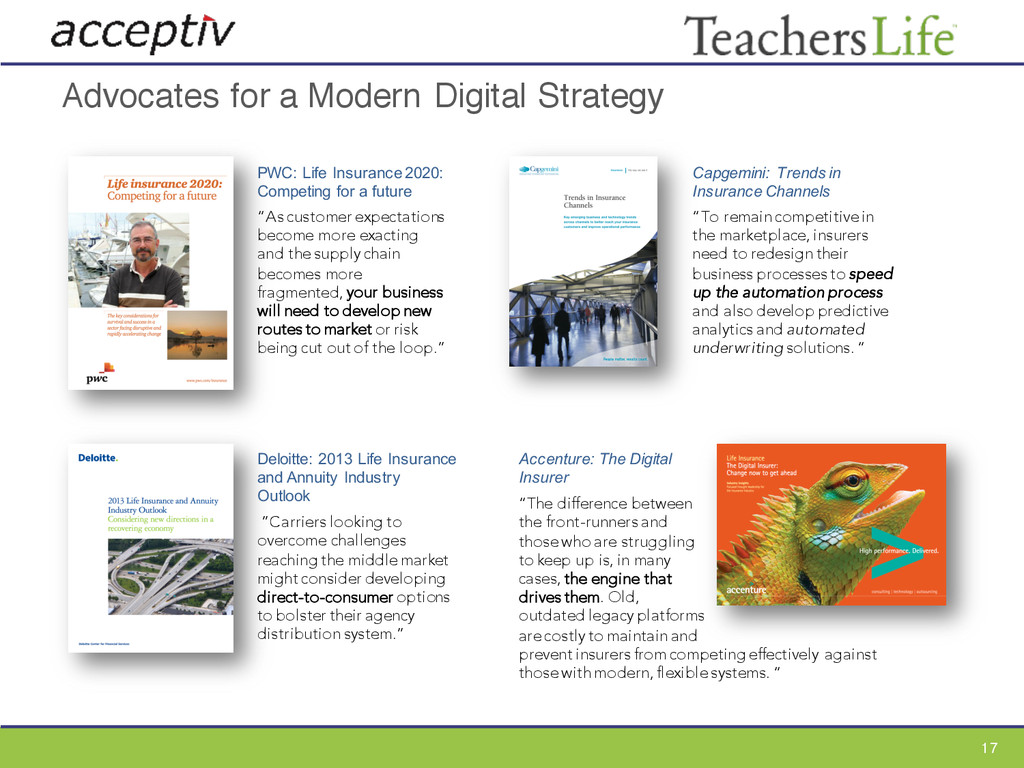

2020: Competing for a future “As customer expectations become more exacting and the supply chain becomes more fragmented, your business will need to develop new routes to market or risk being cut out of the loop.” Deloitte: 2013 Life Insurance and Annuity Industry Outlook ”Carriers looking to overcome challenges reaching the middle market might consider developing direct-to-consumer options to bolster their agency distribution system.” Accenture: The Digital Insurer “The difference between the front-runners and those who are struggling to keep up is, in many cases, the engine that drives them. Old, outdated legacy platforms are costly to maintain and prevent insurers from competing effectively against those with modern, flexible systems. “ Capgemini: Trends in Insurance Channels “To remain competitive in the marketplace, insurers need to redesign their business processes to speed up the automation process and also develop predictive analytics and automated underwriting solutions. “

– “it’s not safe” 5 years ago few people would buy groceries online 15 years ago Travel Agents would claim that you cannot book vacations online – “it needs a personal touch and experience” Digital Disruption – Other Industries 18

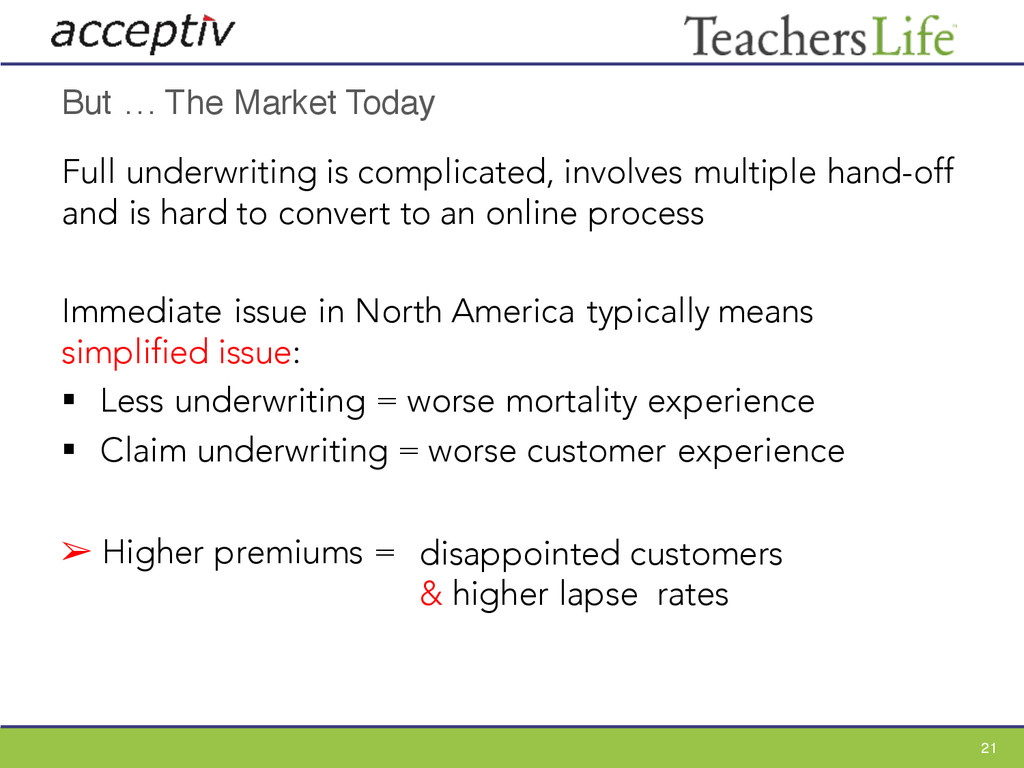

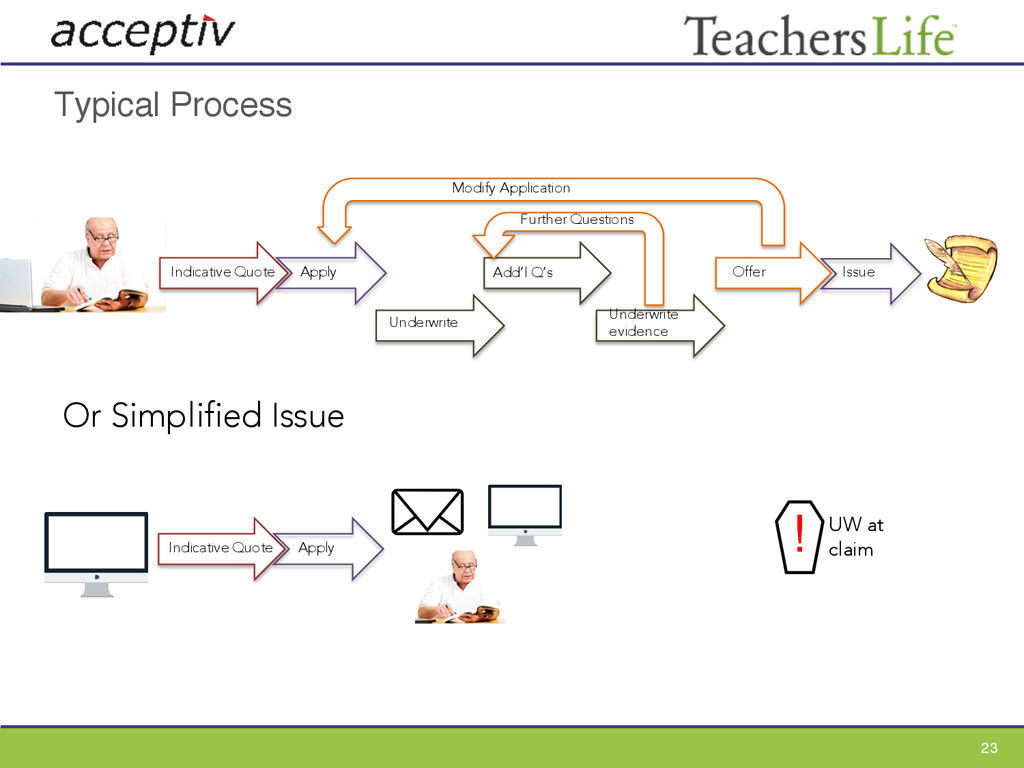

multiple hand-off and is hard to convert to an online process Immediate issue in North America typically means simplified issue: § Less underwriting = worse mortality experience § Claim underwriting = worse customer experience 21 ➢ Higher premiums = disappointed customers & higher lapse rates

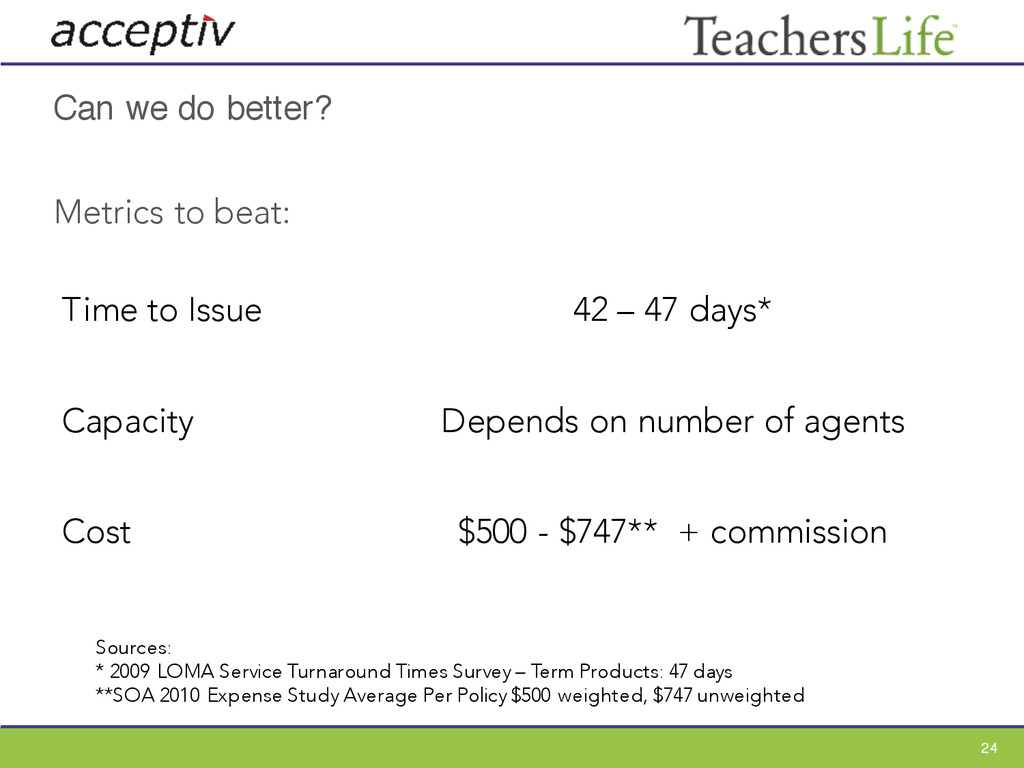

42 – 47 days* Capacity Depends on number of agents Cost $500 - $747** + commission Sources: * 2009 LOMA Service Turnaround Times Survey – Term Products: 47 days **SOA 2010 Expense Study Average Per Policy $500 weighted, $747 unweighted 24

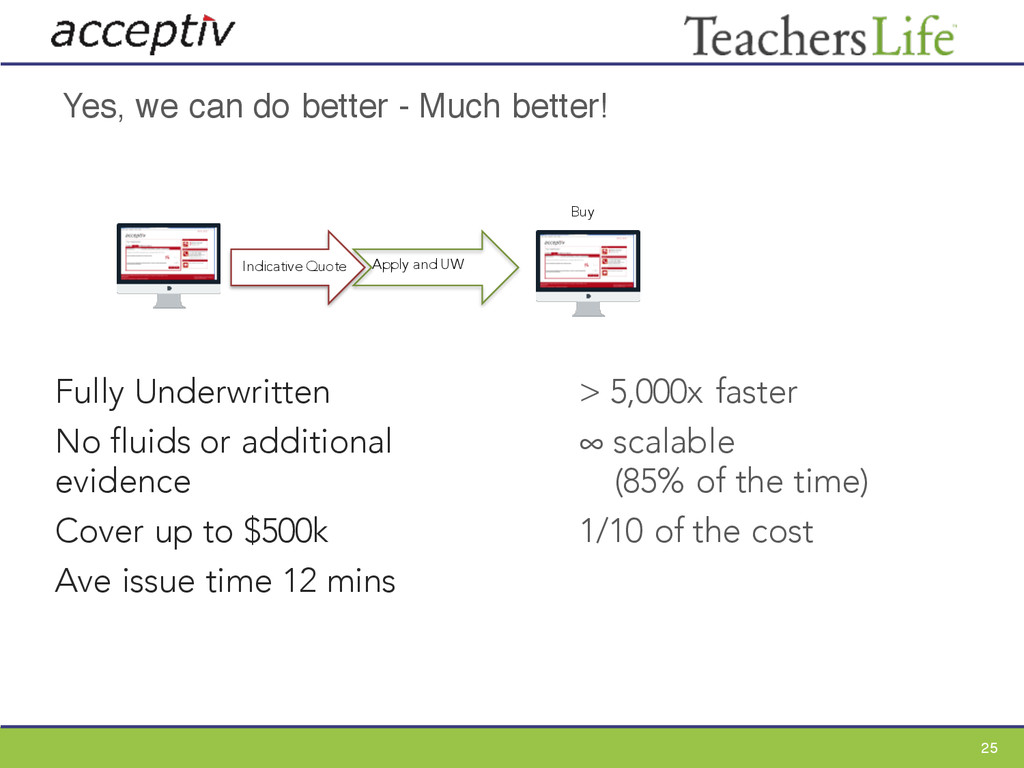

Apply and UW Buy > 5,000x faster ∞ scalable (85% of the time) 1/10 of the cost Fully Underwritten No fluids or additional evidence Cover up to $500k Ave issue time 12 mins 25

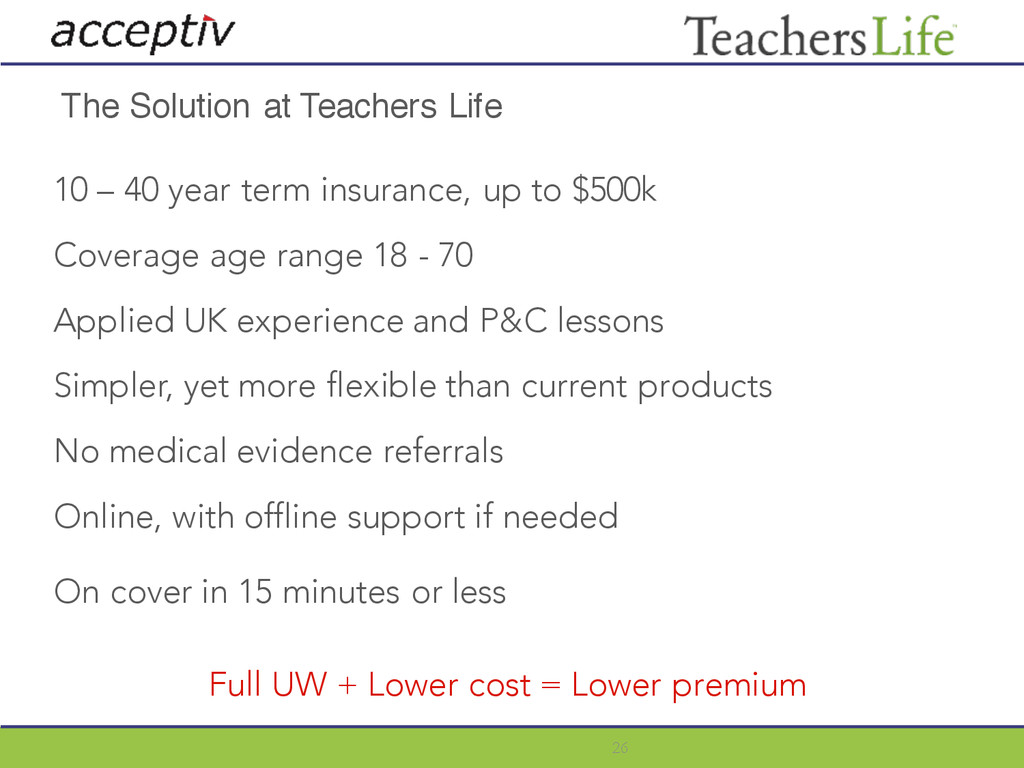

age range 18 - 70 Applied UK experience and P&C lessons Simpler, yet more flexible than current products No medical evidence referrals Online, with offline support if needed On cover in 15 minutes or less Full UW + Lower cost = Lower premium 26 The Solution at Teachers Life

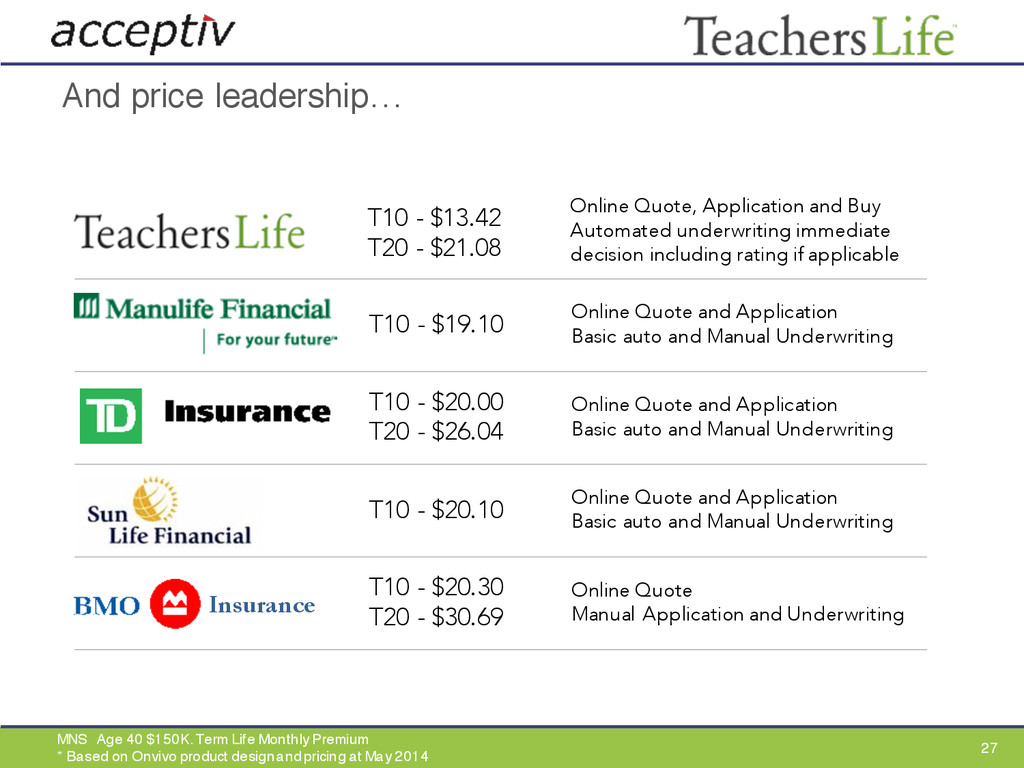

Manual Underwriting T10 - $20.00 T20 - $26.04 Online Quote and Application Basic auto and Manual Underwriting T10 - $20.10 Online Quote and Application Basic auto and Manual Underwriting T10 - $20.30 T20 - $30.69 Online Quote Manual Application and Underwriting And price leadership… MNS Age 40 $150K. Term Life Monthly Premium * Based on Onvivo product design and pricing at May 2014 27 Insurance T10 - $13.42 T20 - $21.08 Online Quote, Application and Buy Automated underwriting immediate decision including rating if applicable

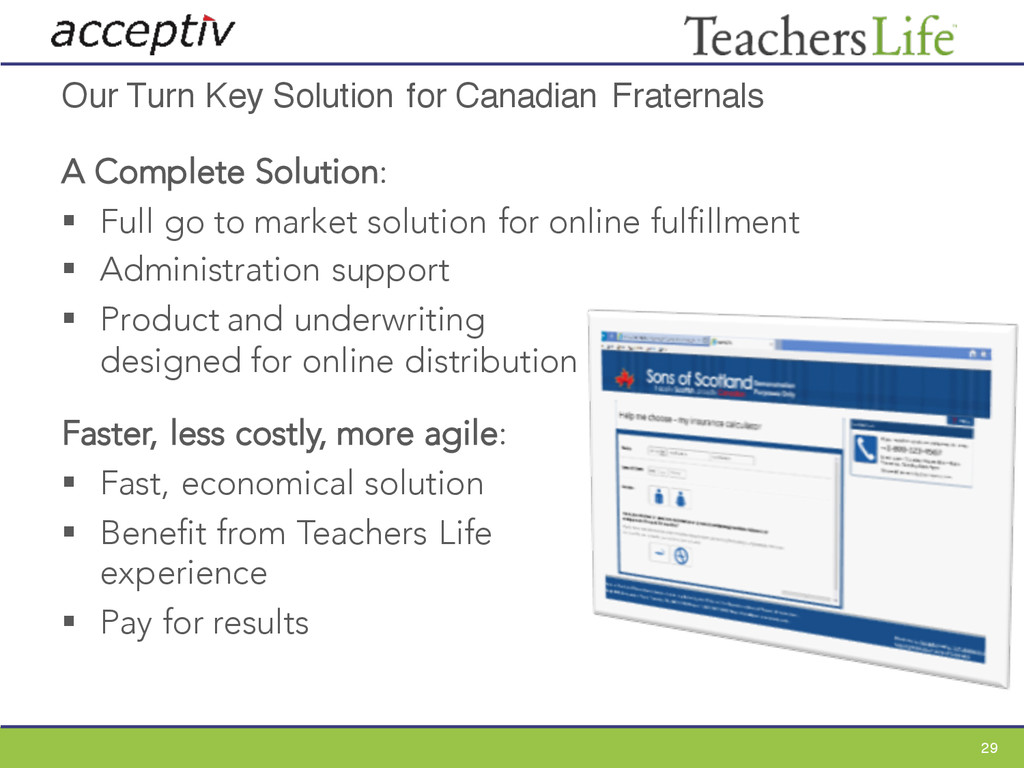

§ Full go to market solution for online fulfillment § Administration support § Product and underwriting designed for online distribution Faster, less costly, more agile: § Fast, economical solution § Benefit from Teachers Life experience § Pay for results 29

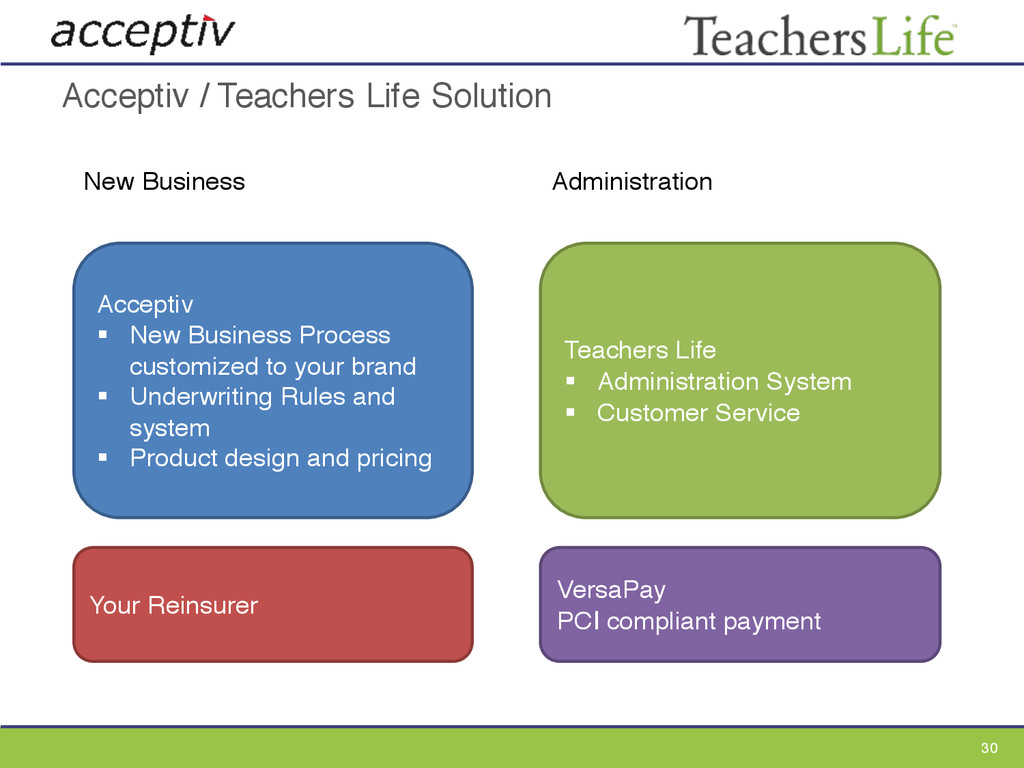

Process customized to your brand § Underwriting Rules and system § Product design and pricing Your Reinsurer Teachers Life § Administration System § Customer Service VersaPay PCI compliant payment New Business Administration

oversight of insurance companies Capital adequacy Policyholder protection Complex Infrastructure Systems Processes Brand Reputation LIFE INSURANCE IS SOLD NOT BOUGHT 33

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}