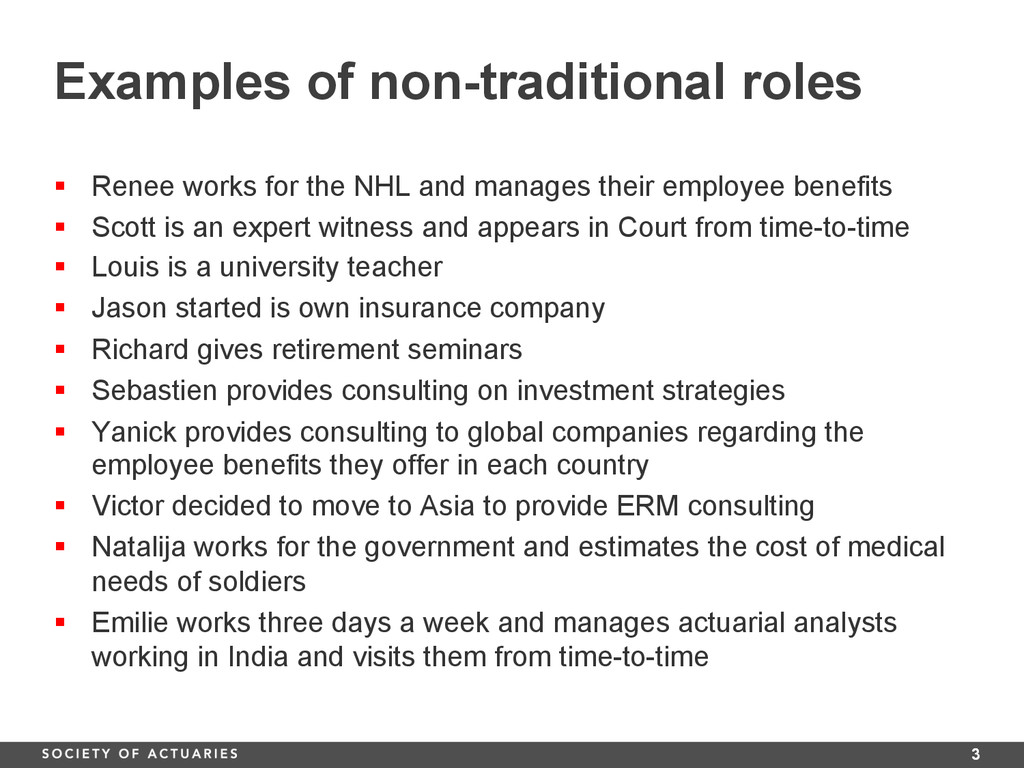

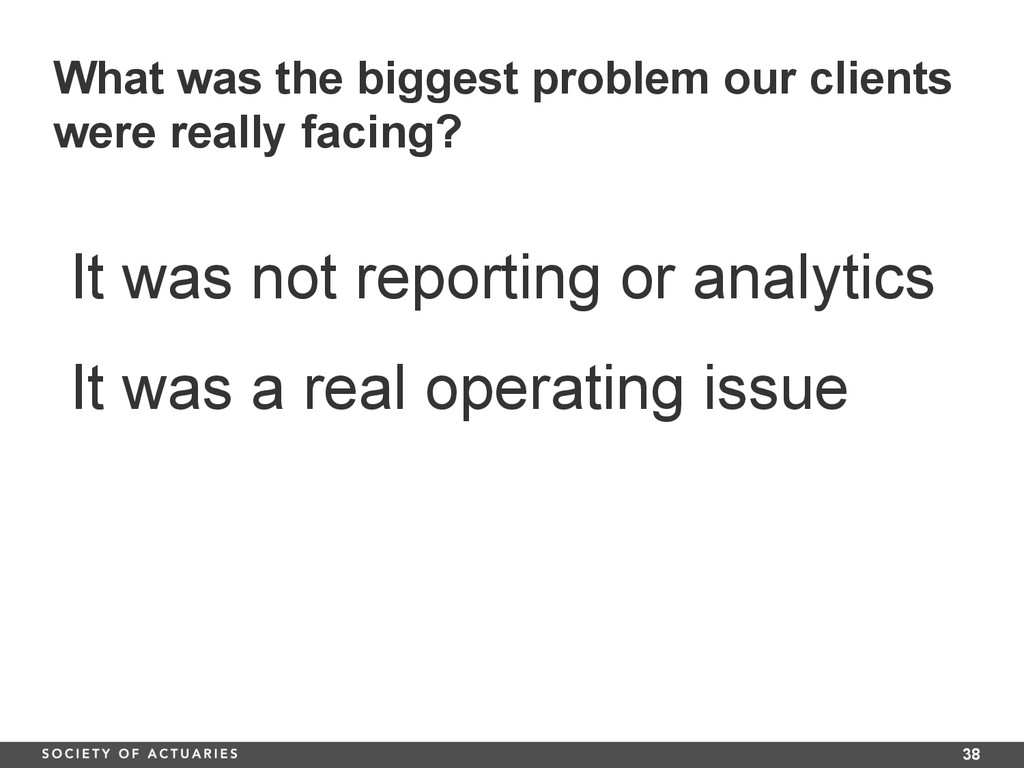

for the NHL and manages their employee benefits § Scott is an expert witness and appears in Court from time-to-time § Louis is a university teacher § Jason started is own insurance company § Richard gives retirement seminars § Sebastien provides consulting on investment strategies § Yanick provides consulting to global companies regarding the employee benefits they offer in each country § Victor decided to move to Asia to provide ERM consulting § Natalija works for the government and estimates the cost of medical needs of soldiers § Emilie works three days a week and manages actuarial analysts working in India and visits them from time-to-time

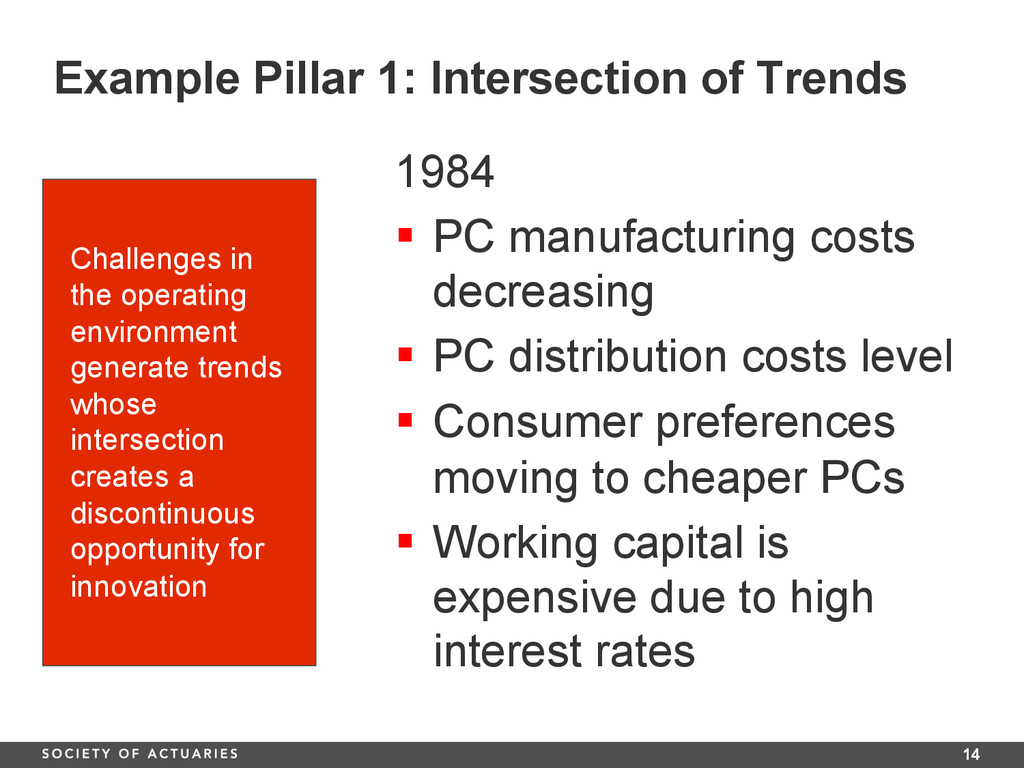

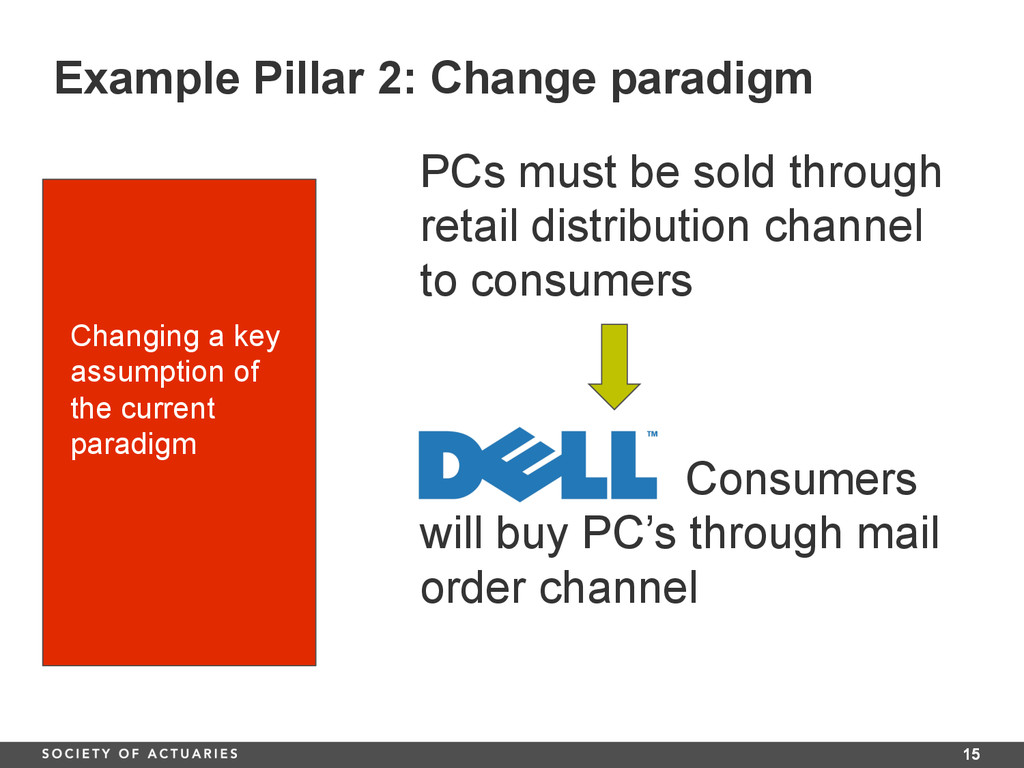

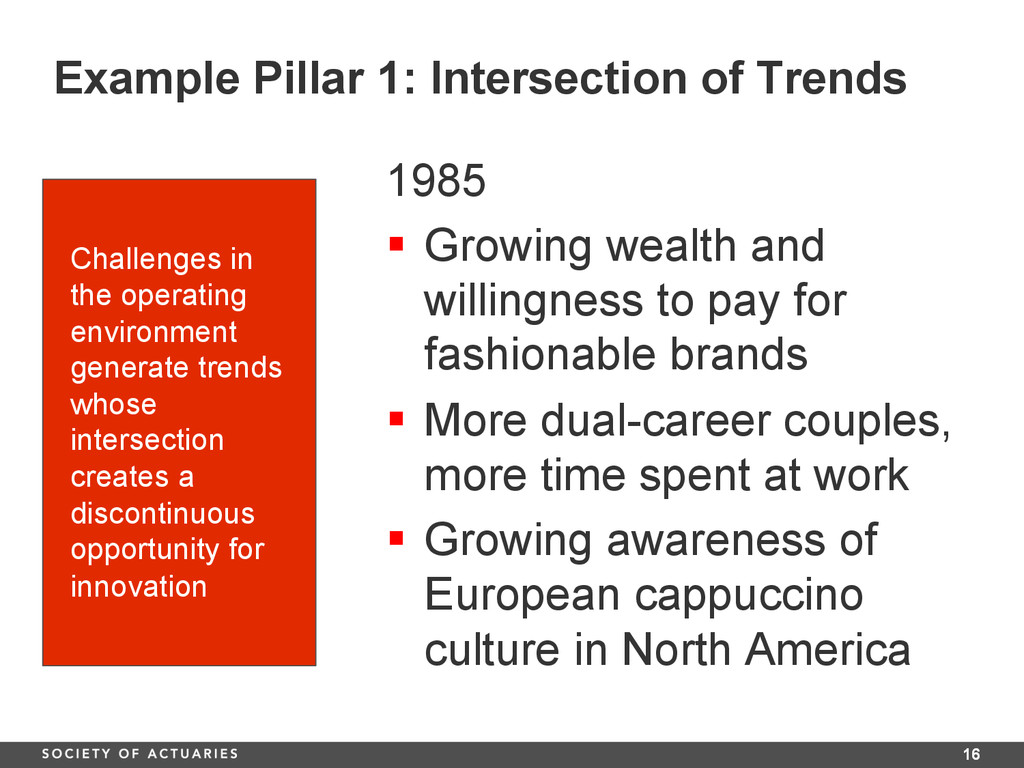

the operating environment generate trends whose intersection creates a discontinuous opportunity for innovation Changing a key assumption of the current paradigm

§ PC manufacturing costs decreasing § PC distribution costs level § Consumer preferences moving to cheaper PCs § Working capital is expensive due to high interest rates Challenges in the operating environment generate trends whose intersection creates a discontinuous opportunity for innovation

be sold through retail distribution channel to consumers Changing a key assumption of the current paradigm Consumers will buy PC’s through mail order channel

§ Growing wealth and willingness to pay for fashionable brands § More dual-career couples, more time spent at work § Growing awareness of European cappuccino culture in North America Challenges in the operating environment generate trends whose intersection creates a discontinuous opportunity for innovation

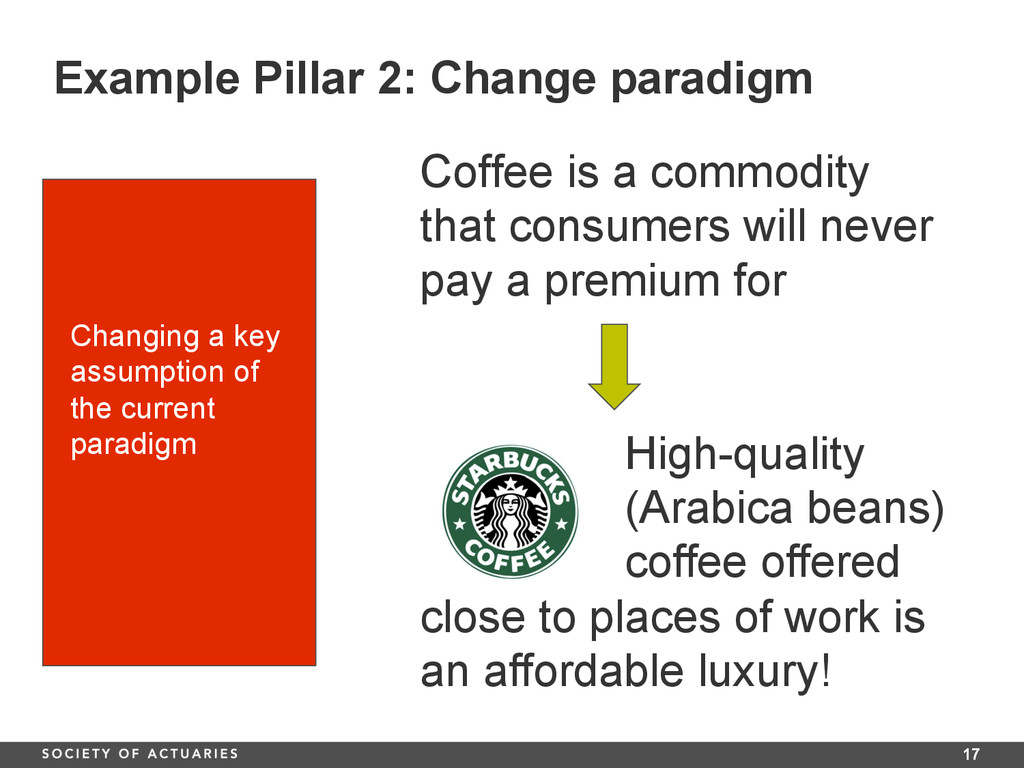

a commodity that consumers will never pay a premium for Changing a key assumption of the current paradigm High-quality (Arabica beans) coffee offered close to places of work is an affordable luxury!

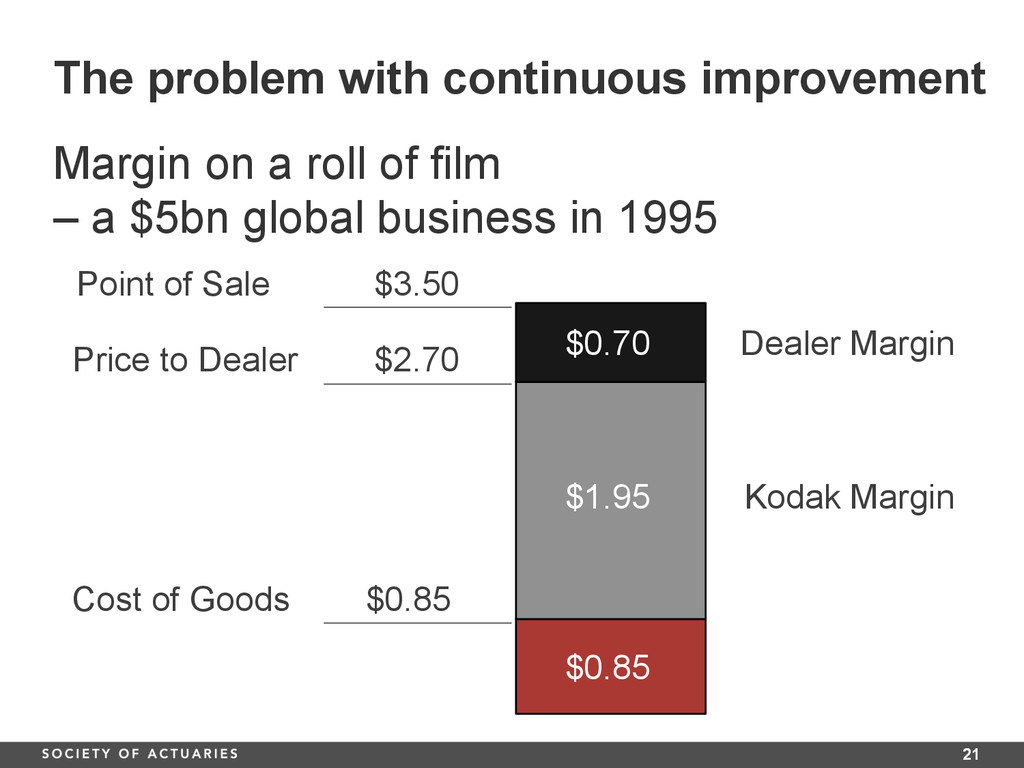

a roll of film – a $5bn global business in 1995 Cost of Goods $0.85 Point of Sale $3.50 Price to Dealer $2.70 $0.70 $1.95 $0.85 Dealer Margin Kodak Margin

in film, but down from 76% § 70% gross margin in film § Commanding share in paper in chemicals § Increasingly competitive new entrants into film business

§ Founded in 2000 based on project I had led at Foresters § Cheaper data management and reporting § Several components made this possible, but the value of the whole was greater than the individual parts

financial reporting 2. Lower cost of data storage 3. Increased use of standalone applications requiring large data feeds (valuation, ALM, experience studies) Paradigm: IT (not business areas) has to manage data

knew my customer (in fact I defined my customer to be me) 2. I knew my value proposition (for a mid sized company) 3. What would make my business obsolete? Big Data R Inclusive solution with other applications 4. BUT we didn’t do it – why not?

and capital from me § Poor equity decision – 50/50 both taking risk § Inability to make big decisions § Failure to grow and mature § When self-supporting – 100% of a slightly smaller business is better than 50% of the whole business

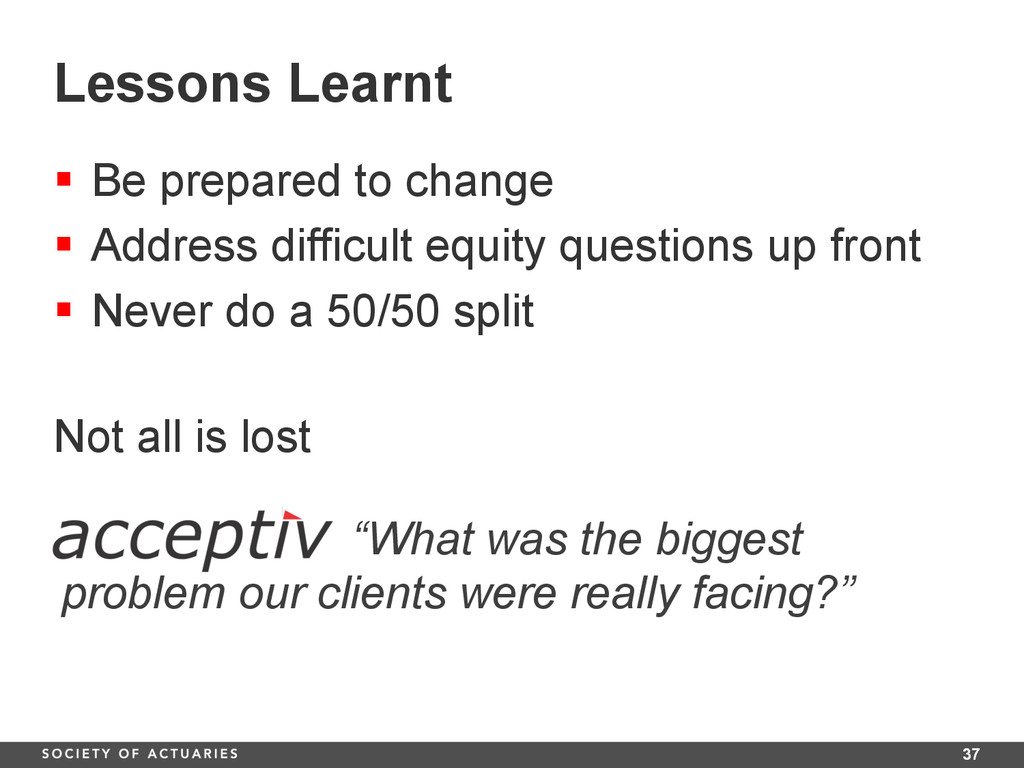

§ Address difficult equity questions up front § Never do a 50/50 split Not all is lost “What was the biggest problem our clients were really facing?”

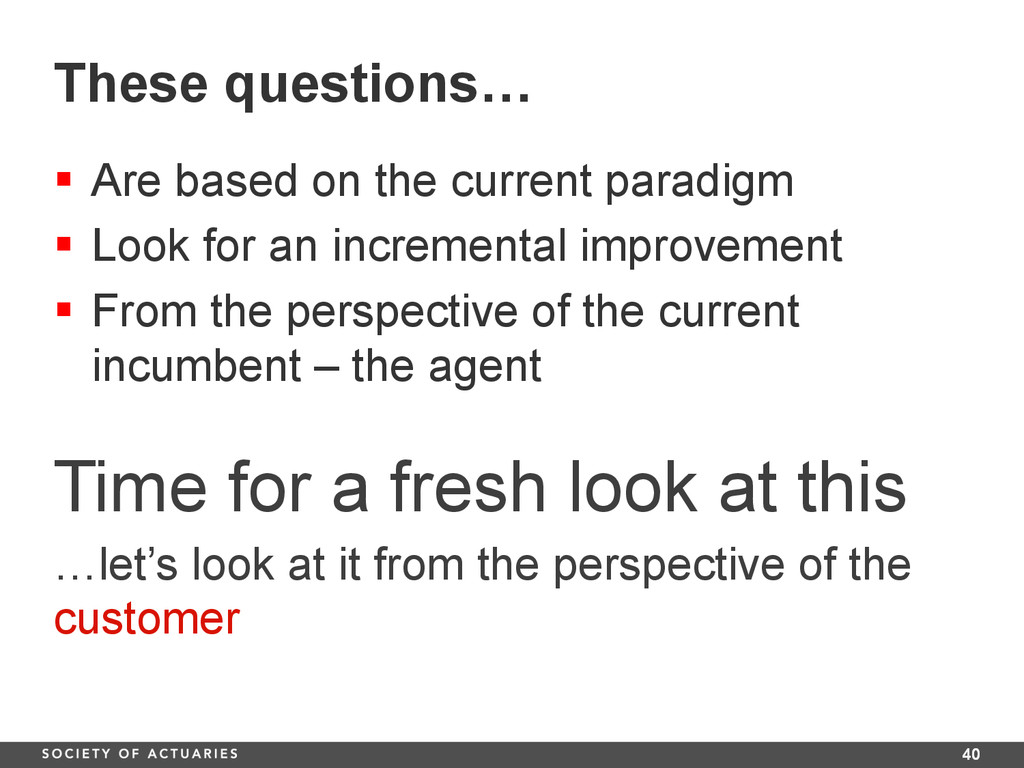

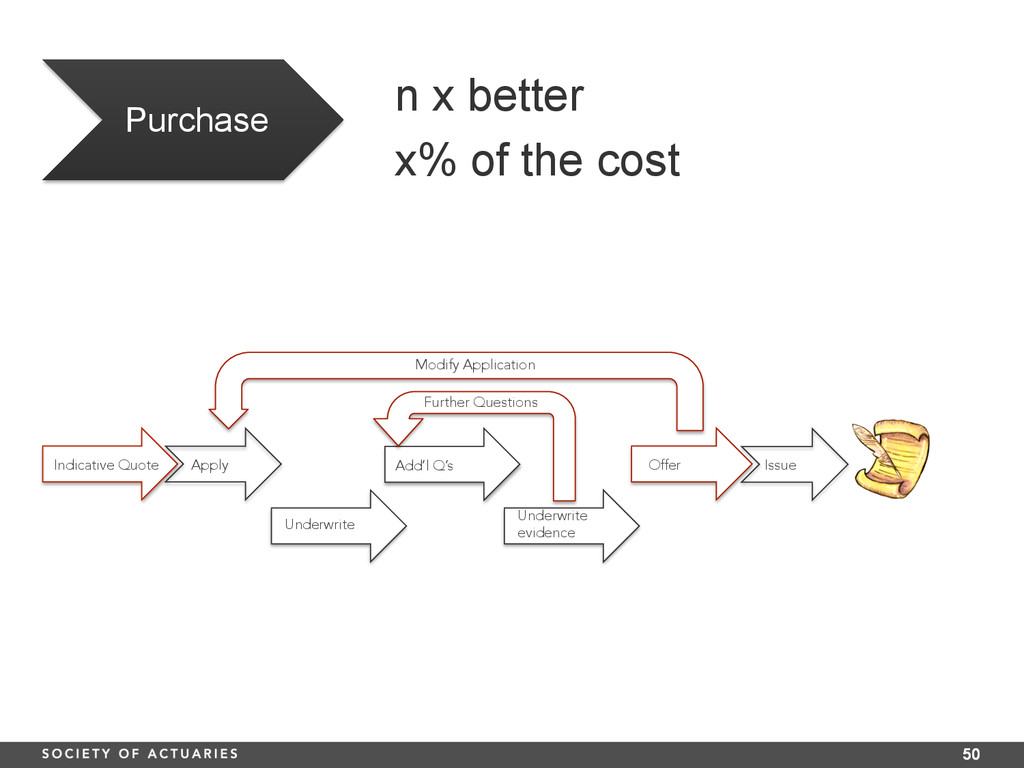

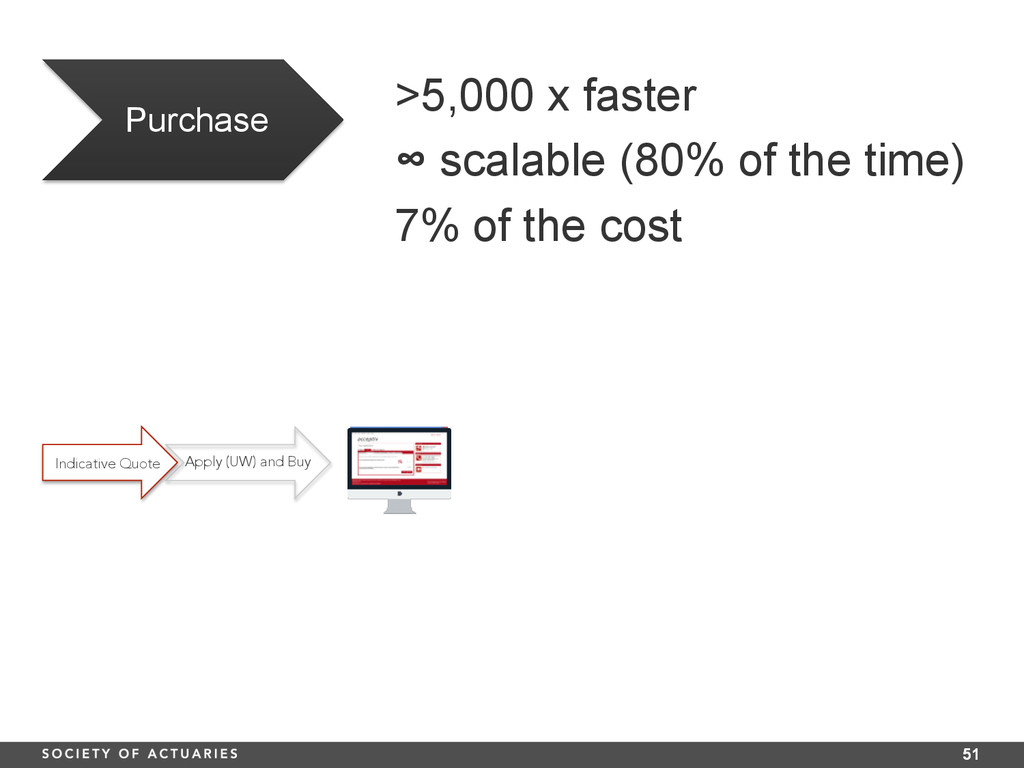

current paradigm § Look for an incremental improvement § From the perspective of the current incumbent – the agent Time for a fresh look at this …let’s look at it from the perspective of the customer

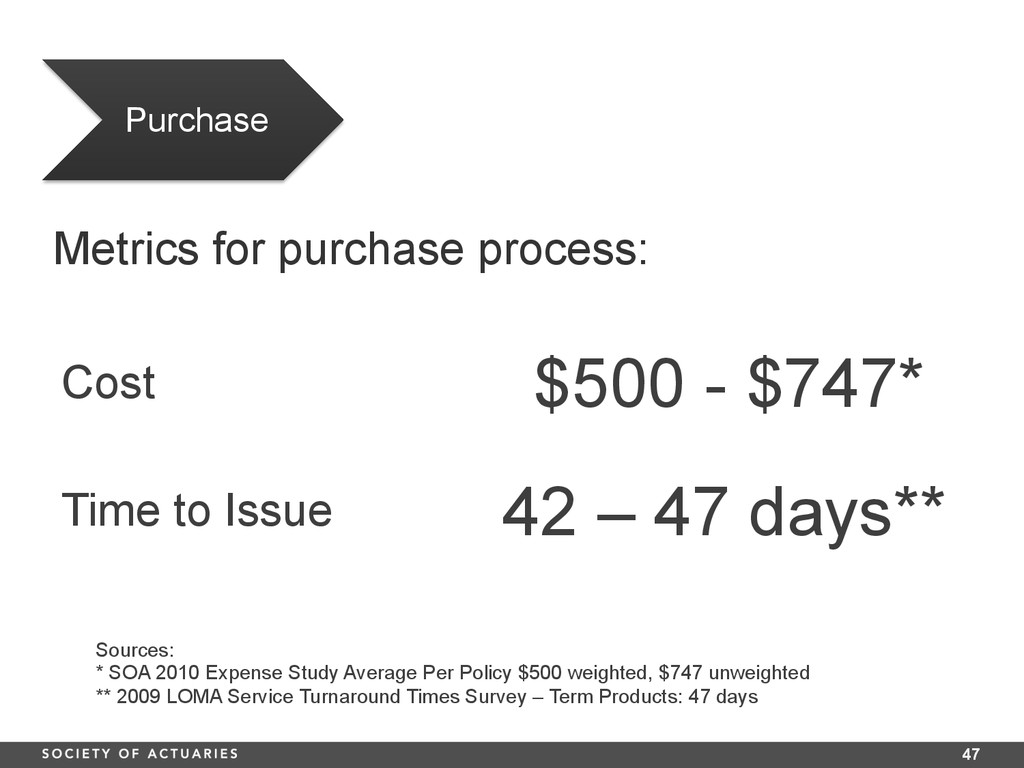

- $747* Time to Issue 42 – 47 days** Sources: * SOA 2010 Expense Study Average Per Policy $500 weighted, $747 unweighted ** 2009 LOMA Service Turnaround Times Survey – Term Products: 47 days

Increasing cost to issue business § Increase in online shopping § Aging distribution force Life insurance is sold not bought Life insurance can be bought and does not need advice Challenges in the operating environment generate trends whose intersection creates a discontinuous opportunity for innovation Changing a key assumption of the current paradigm

up to $500k § Coverage age range 18 - 70 § Applied UK experience and P&C lessons § Simpler, yet more flexible than current products § No medical evidence referrals • Online, with offline support if needed • On cover in 15 minutes or less Full UW + Lower cost = Lower premium

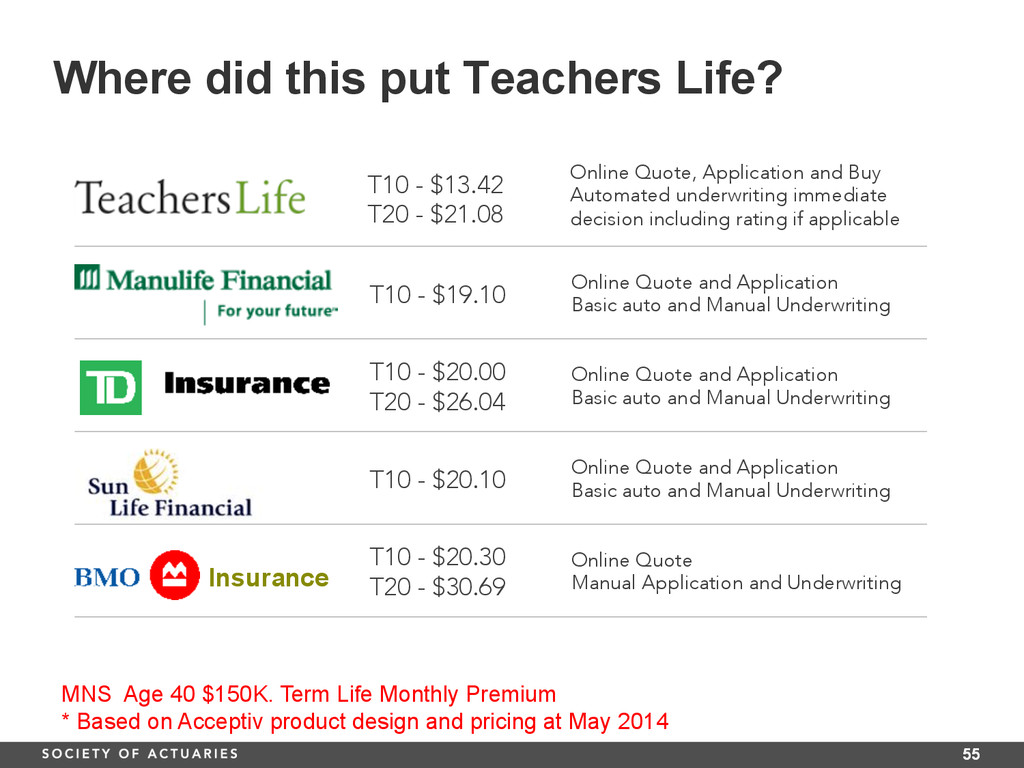

Basic auto and Manual Underwriting T10 - $20.00 T20 - $26.04 Online Quote and Application Basic auto and Manual Underwriting T10 - $20.10 Online Quote and Application Basic auto and Manual Underwriting T10 - $20.30 T20 - $30.69 Online Quote Manual Application and Underwriting Where did this put Teachers Life? MNS Age 40 $150K. Term Life Monthly Premium * Based on Acceptiv product design and pricing at May 2014 Insurance T10 - $13.42 T20 - $21.08 Online Quote, Application and Buy Automated underwriting immediate decision including rating if applicable

is a commodity § Customers want the opportunity to buy online without an advisor § Don’t need to be significantly cheaper § Online underwriting – same mortality, better lapse experience Beagle Street – new entrant launched in 2012 (not really a life insurance company)

Fellow, Canadian Membership Society of Actuaries 613 402 4118 [email protected] Kevin Pledge, FIA, FSA CEO and Founder Acceptiv Inc. 416 949 8920 [email protected] www.acceptiv.com/asna

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}