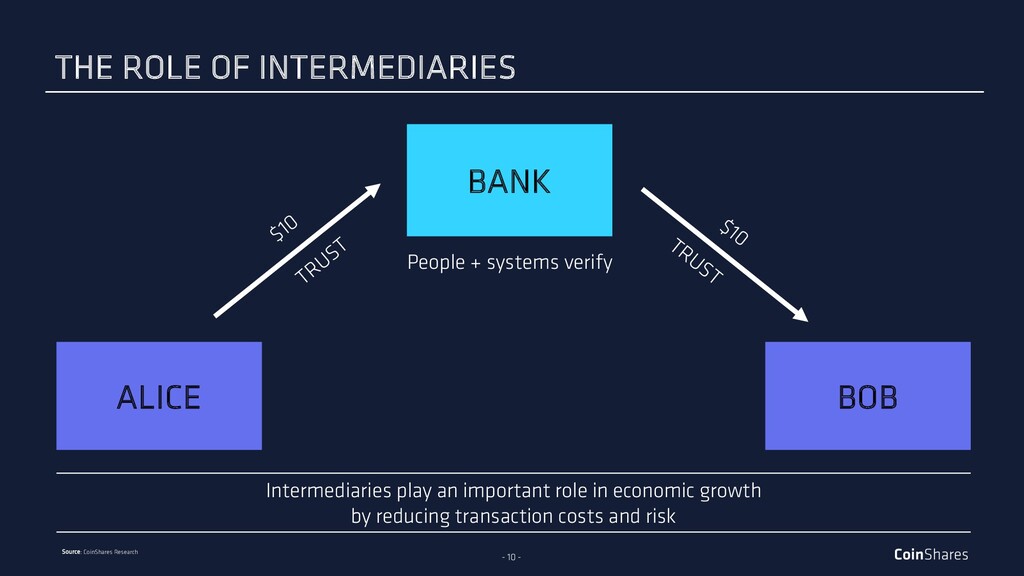

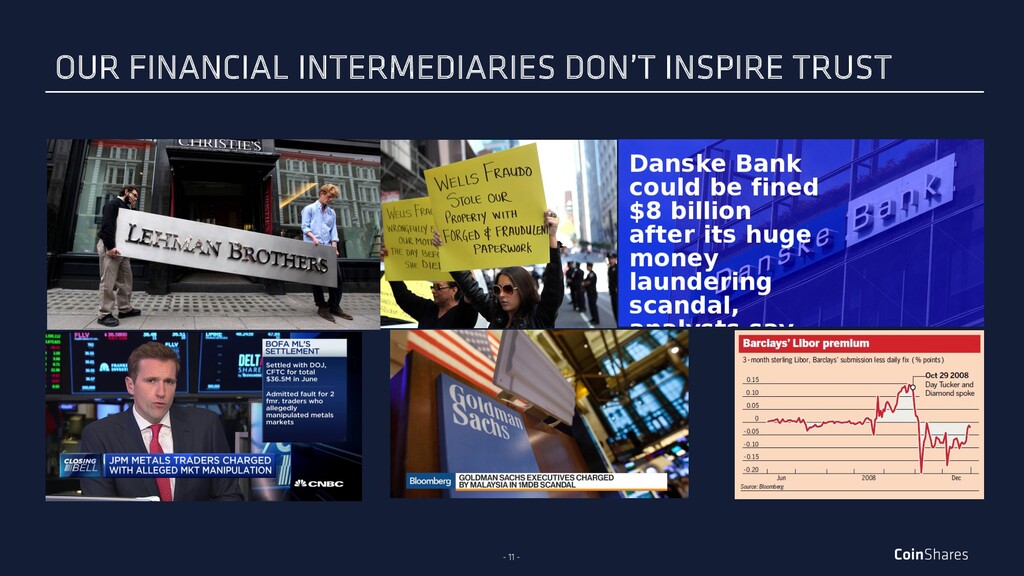

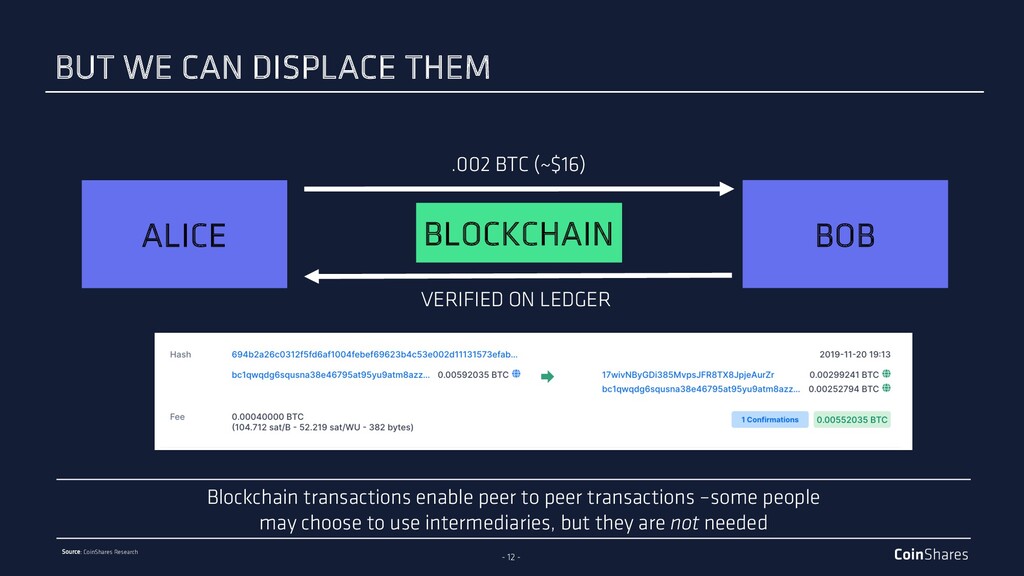

Our world is built on trust – we trust brands, products, and institutions. Over the last decade, this trust has been eroded as consumers have access to more information in real time, on the internet. Nowhere has trust been more essential than in the financial system - where we rely on a complex web of intermediaries that abstract out layers of risk and hide it behind a pretty facade. Until bitcoin was introduced, consumers had never had a functional way to operate independently from this web of intermediaries. Today, bitcoin is more complex and more difficult to use than , but for the first time - users have a viable alternative. This is a potent and powerful realization, and a force that will change the nature of trust in our world. This talk was delivered at Slush 2019 in Helsinki. More at https://www.slush.org/cryptocurrencies-are-the-future-but-not-before-they-gain-trust/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}