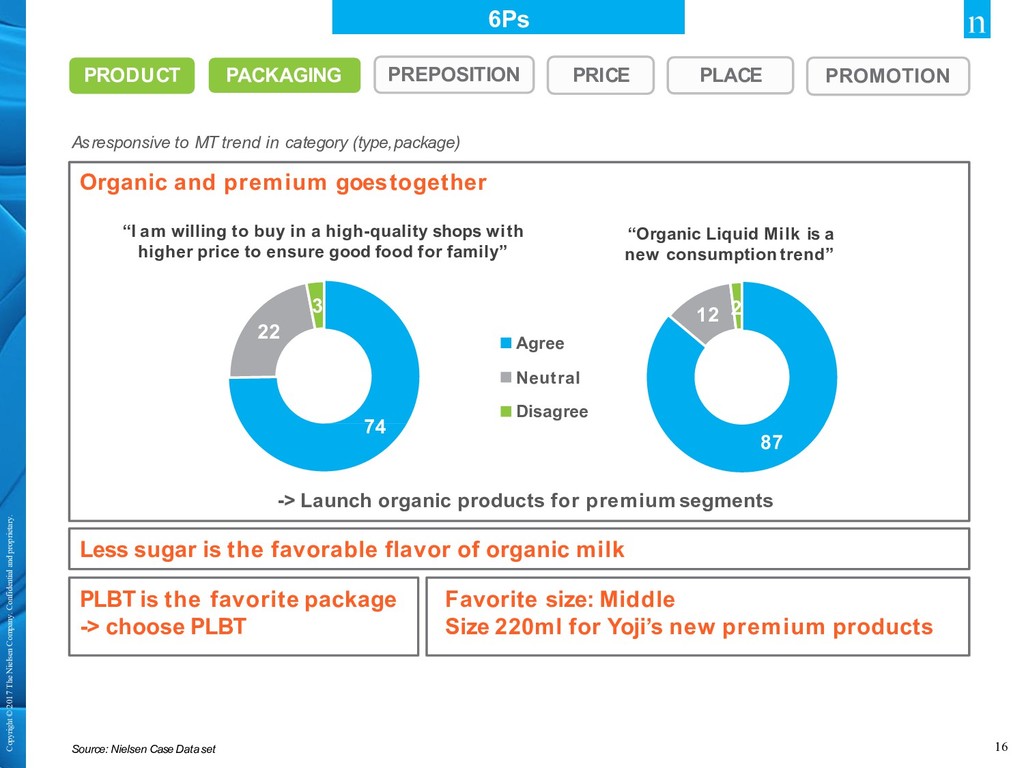

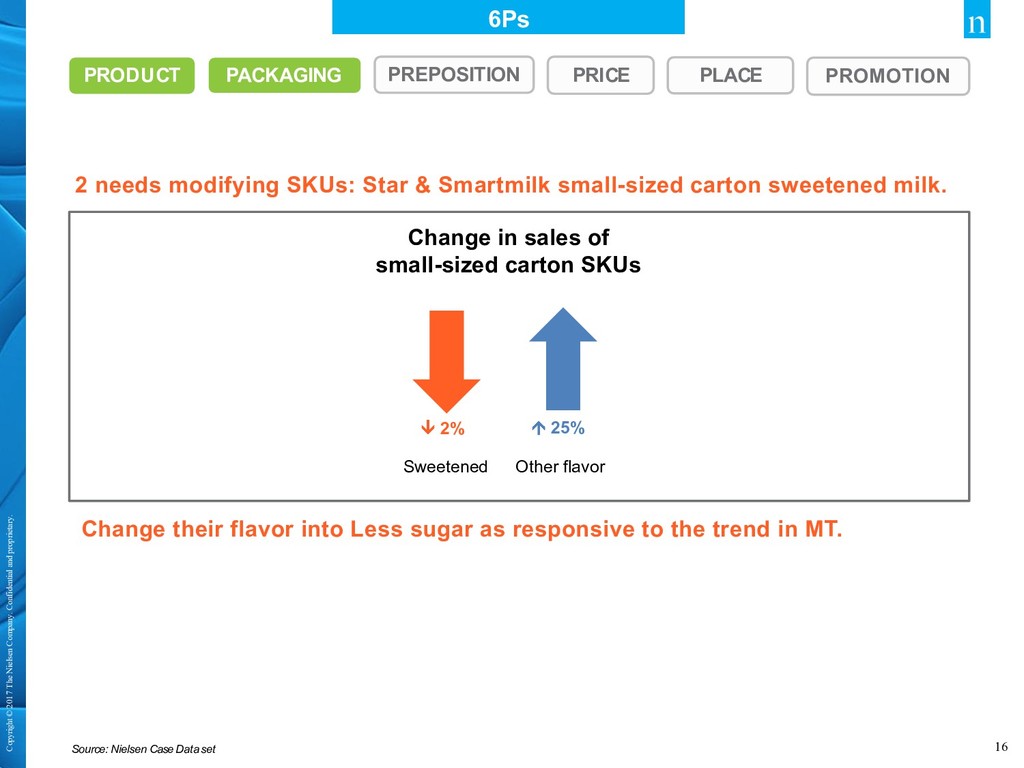

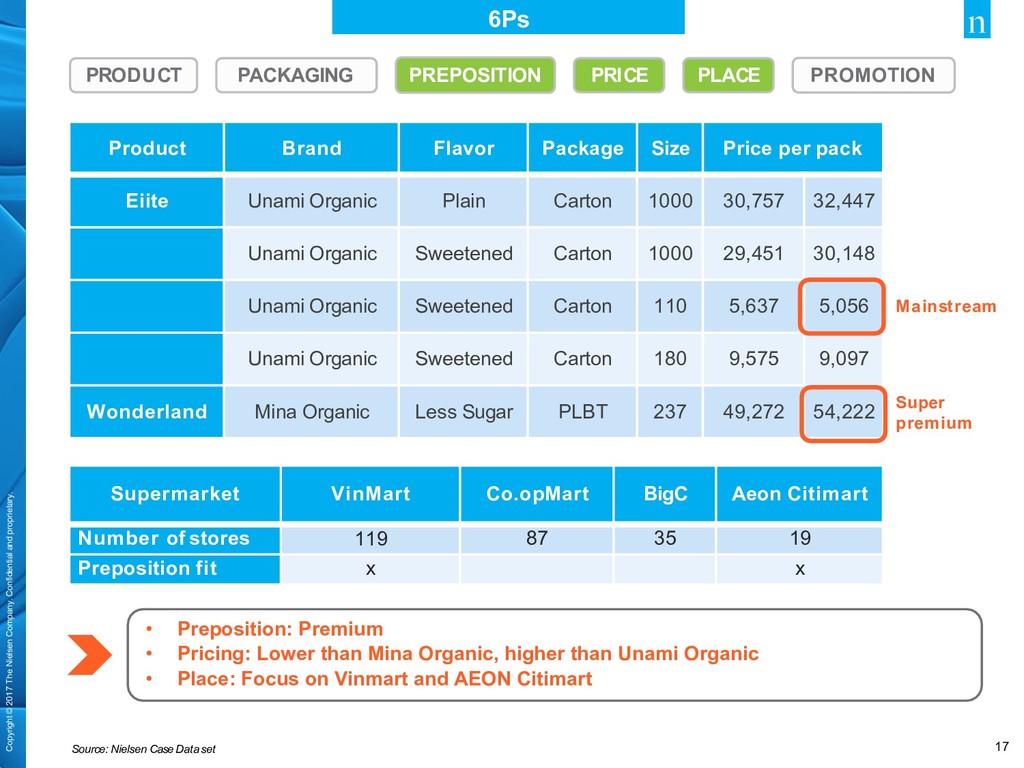

6Ps Source: Nielsen Case Dataset PREPOSITION PROMOTION PACKAGING PRODUCT PRICE PLACE Product Brand Flavor Package Size Price per pack Eiite Unami Organic Plain Carton 1000 30,757 32,447 Unami Organic Sweetened Carton 1000 29,451 30,148 Unami Organic Sweetened Carton 110 5,637 5,056 Unami Organic Sweetened Carton 180 9,575 9,097 Wonderland Mina Organic Less Sugar PLBT 237 49,272 54,222 Super premium Mainstream • Preposition: Premium • Pricing: Lower than Mina Organic, higher than Unami Organic • Place: Focus on Vinmart and AEON Citimart Supermarket VinMart Co.opMart BigC Aeon Citimart Number of stores 119 87 35 19 Preposition fit x x

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}