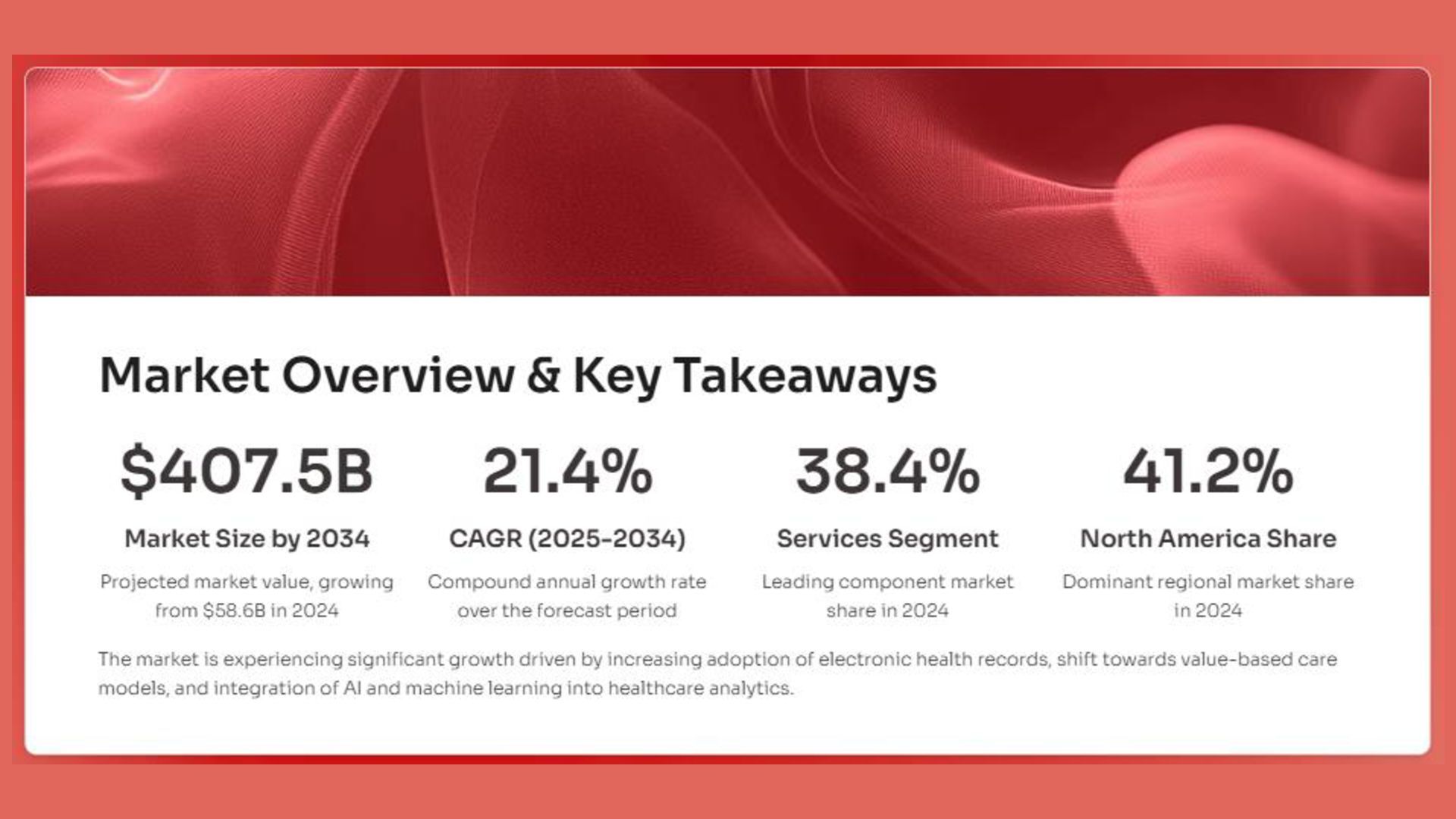

The Global Digital Health For Obesity Market is poised for robust growth. It is projected to rise from USD 58.6 billion in 2024 to USD 407.5 billion by 2034, growing at a CAGR of 21.4%. This growth reflects increasing global awareness of obesity and its associated risks. Governments and healthcare providers are investing in digital health tools to monitor, manage, and prevent obesity. Technologies such as wearable devices, health apps, and teleconsultation platforms are playing a pivotal role in enabling continuous patient engagement and lifestyle management.

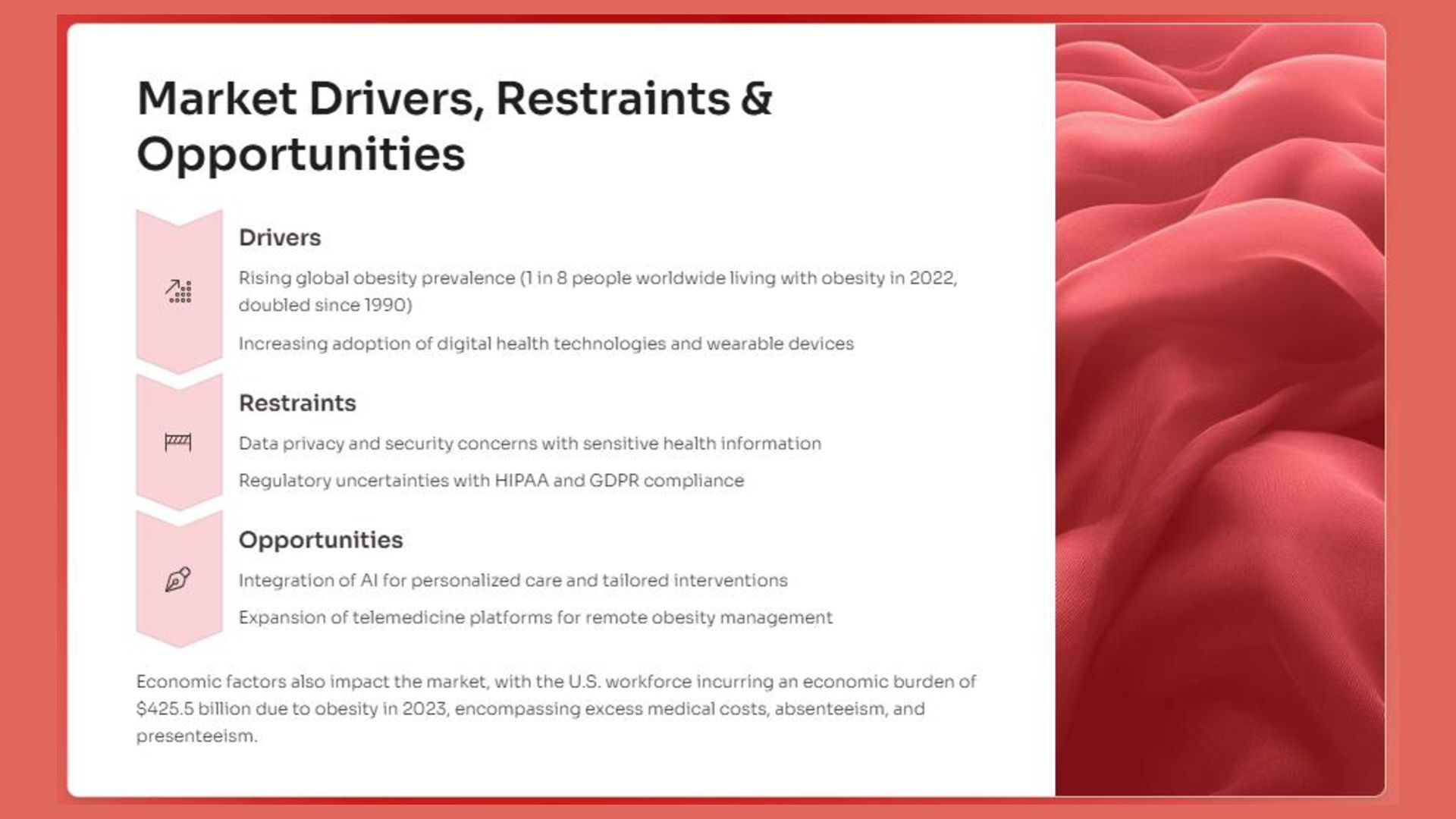

The rising use of electronic health records (EHRs) and health IT has created new pathways for data analysis. With improved access to real-time clinical data, healthcare providers are now better equipped to personalize treatment for obese patients. Government bodies like the Office of the National Coordinator for Health Information Technology (ONC) are supporting these initiatives. Their efforts to promote meaningful use of EHRs help drive better outcomes and reduce the long-term costs associated with obesity management.

Value-based care models are gaining traction across healthcare systems. These models reward outcomes rather than volume, encouraging providers to use digital tools for patient monitoring and outcome tracking. As a result, digital health solutions for obesity—especially operational analytics—are in high demand. They support early interventions, improve care delivery, and align with the broader goal of health system efficiency. This shift has opened new avenues for analytics-driven obesity care programs globally.

Artificial intelligence (AI) and machine learning technologies are transforming how obesity is treated. These tools enhance clinical decision-making, enable predictive analytics, and support the development of personalized care plans. Innovations such as AI-based dietary recommendations and activity tracking improve patient compliance and engagement. However, despite these advancements, several challenges persist. Data privacy issues, lack of interoperability, and high initial investment requirements remain significant obstacles to full-scale digital health adoption.

By segment, services accounted for 38.4% of the global market share in 2024, reflecting strong demand for digital health platforms and virtual care services. The patient segment also led with a 34.8% share, driven by rising consumer adoption of digital tools for obesity management. Regionally, North America held the largest share of 41.2% in 2024. This dominance is attributed to its advanced healthcare infrastructure, high digital literacy, and supportive reimbursement policies. The continued integration of smart technologies is expected to reinforce regional growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}