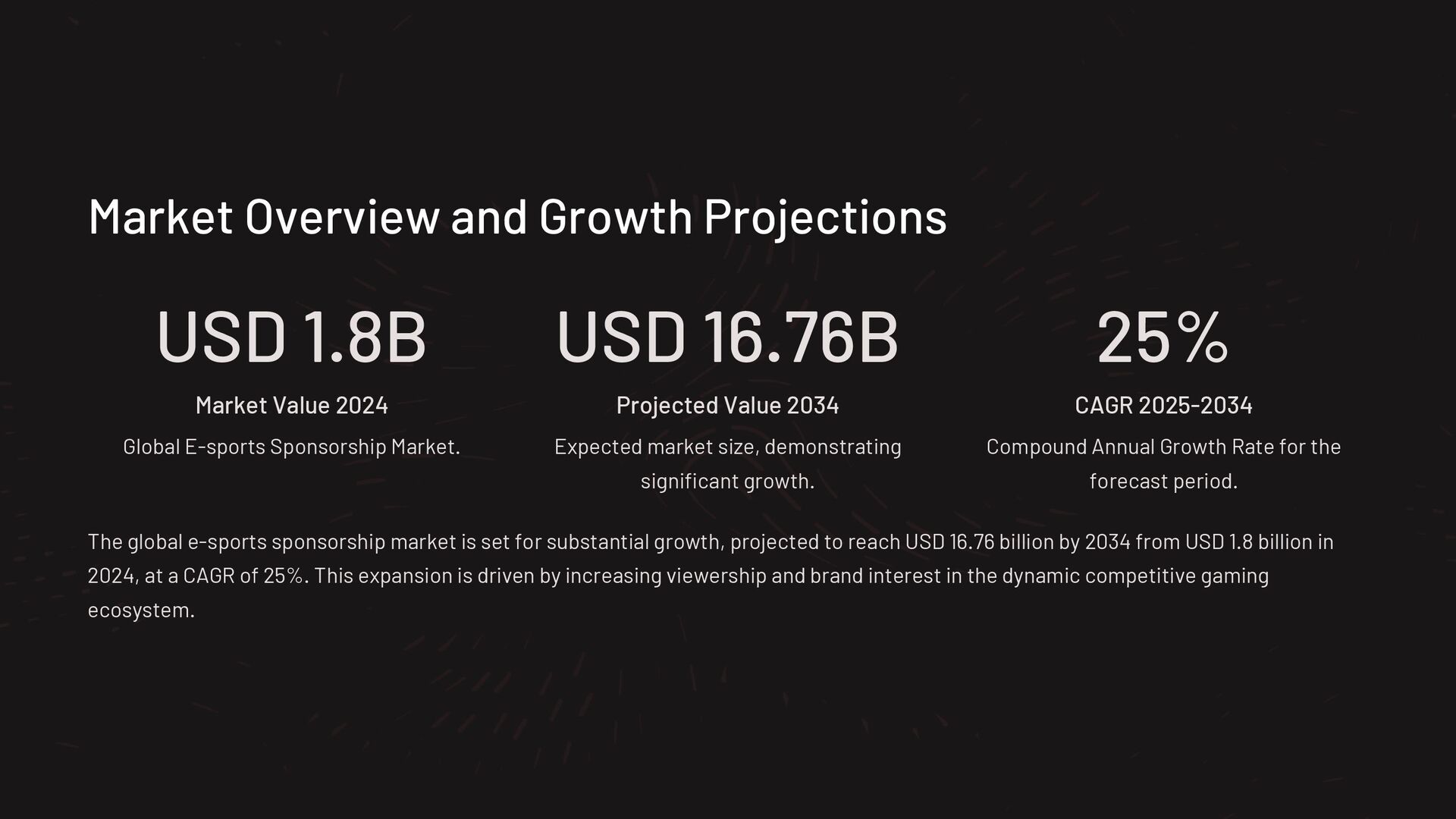

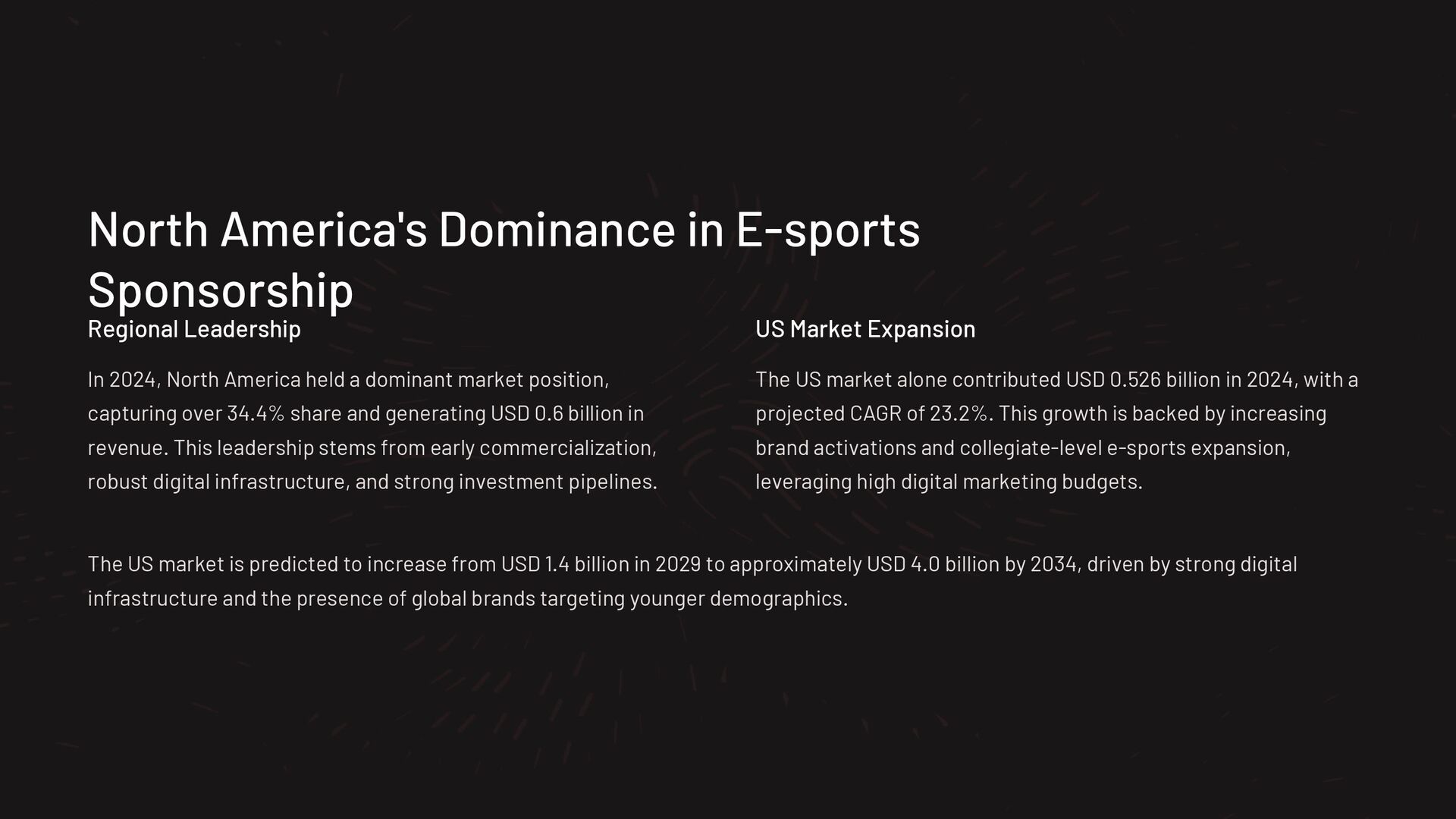

The Global E-sports Sponsorship Market size is expected to be worth around USD 16.76 Billion By 2034, from USD 1.8 billion in 2024, growing at a CAGR of 25% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 34.4% share, holding USD 0.6 Billion revenue.

In 2024, North America maintained a leading position in the global esports sponsorship market, securing over 34.4% of the total share and generating approximately USD 0.6 billion in revenue. This dominance was supported by elevated audience engagement levels and a well-structured league ecosystem that attracts consistent brand investments. Notably, the United States alone contributed around USD 0.526 billion, fueled by a strong CAGR of 23.2%, as collegiate-level esports and increased brand activations continued to expand nationwide.

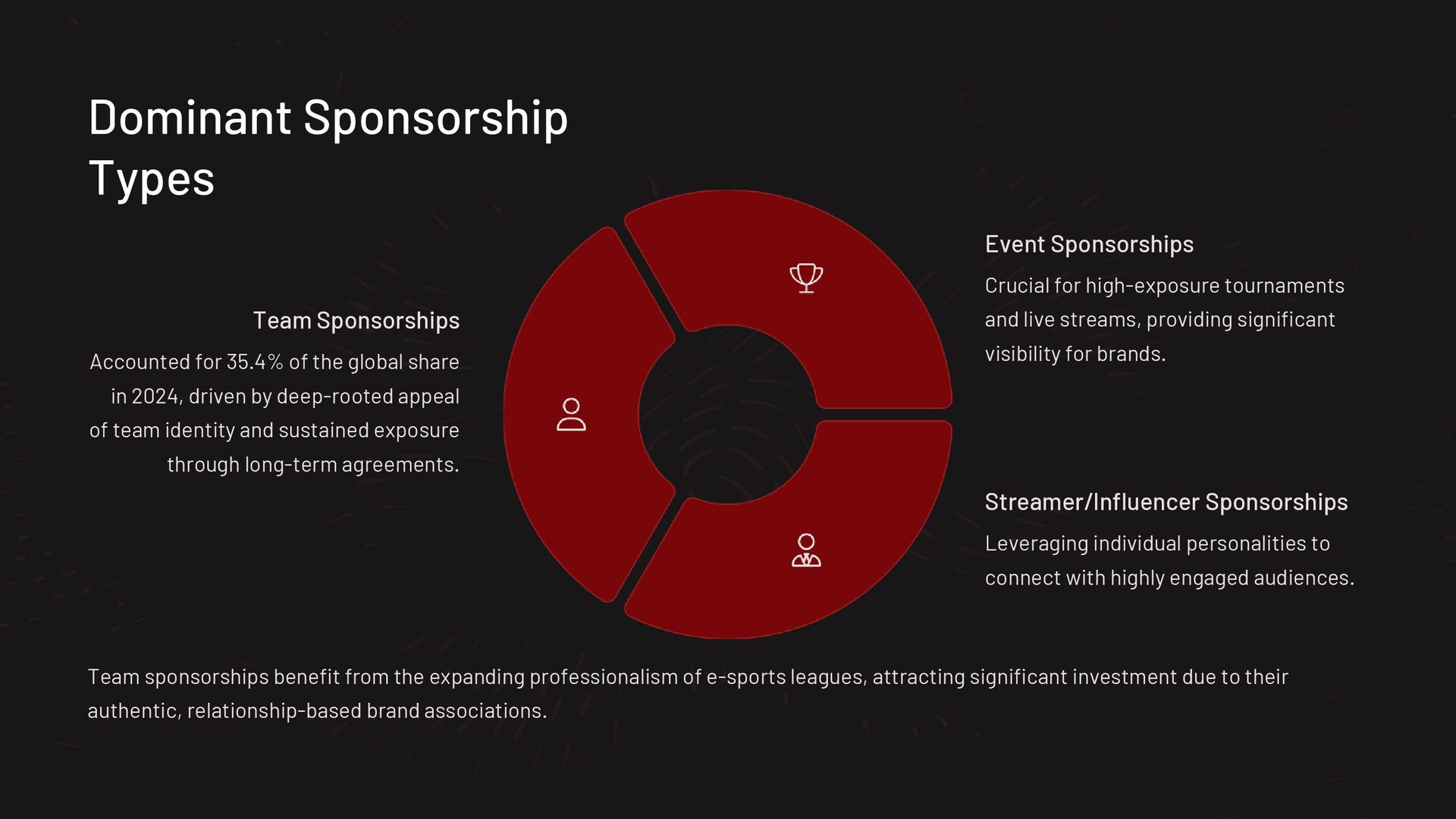

By sponsorship type, team sponsorships held a dominant share of 35.4%, as brands increasingly sought deeper, long-term visibility through jersey branding, team-owned content, and exclusive collaborations. These partnerships enabled sustained engagement with loyal fanbases and improved brand recall throughout tournament cycles.

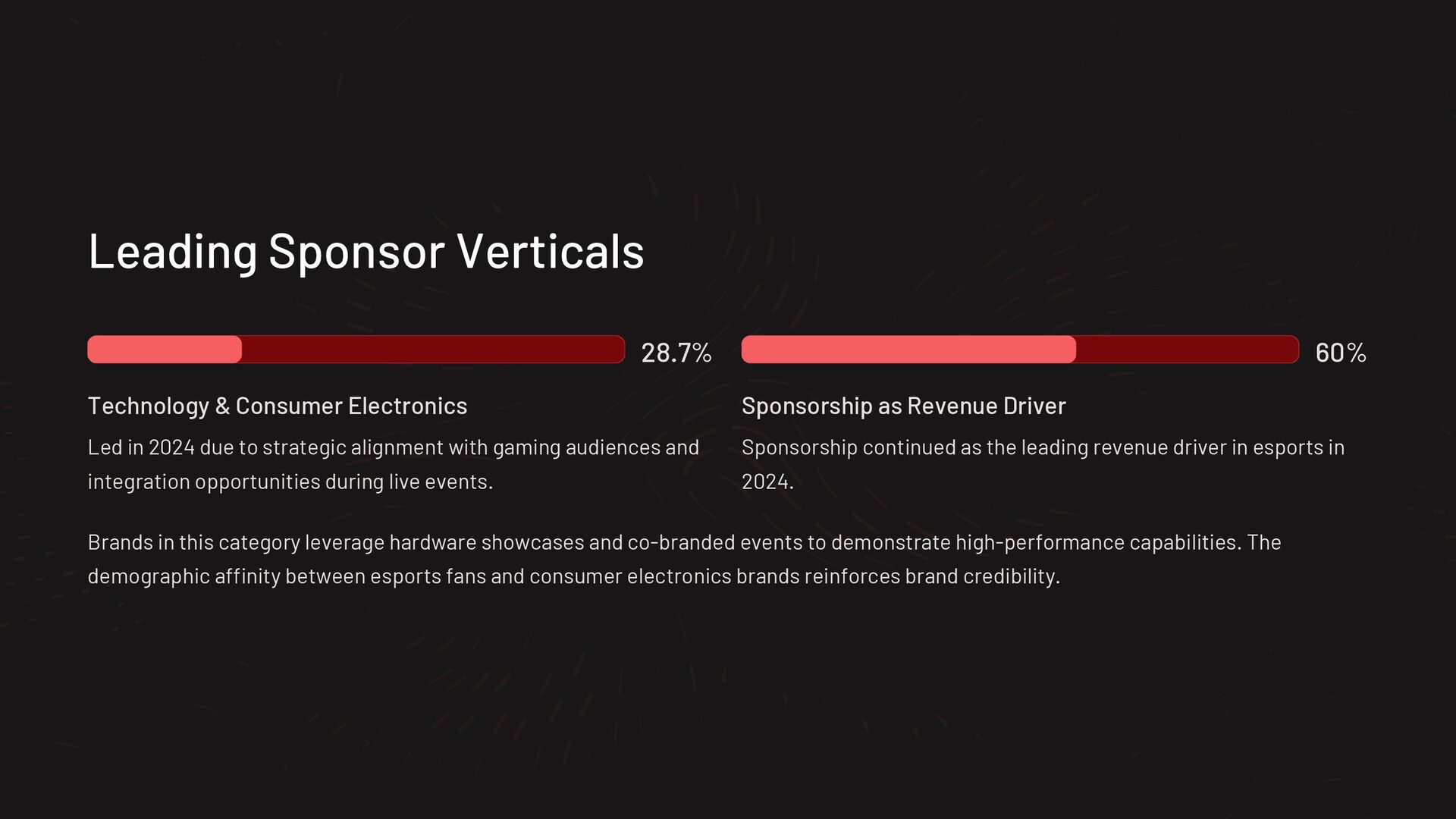

Among sponsor verticals, the technology and consumer electronics segment led with a 28.7% share. This was driven by the alignment of products with gaming audiences and the ease of embedding technology brands into live tournaments, stream overlays, and influencer-backed content.

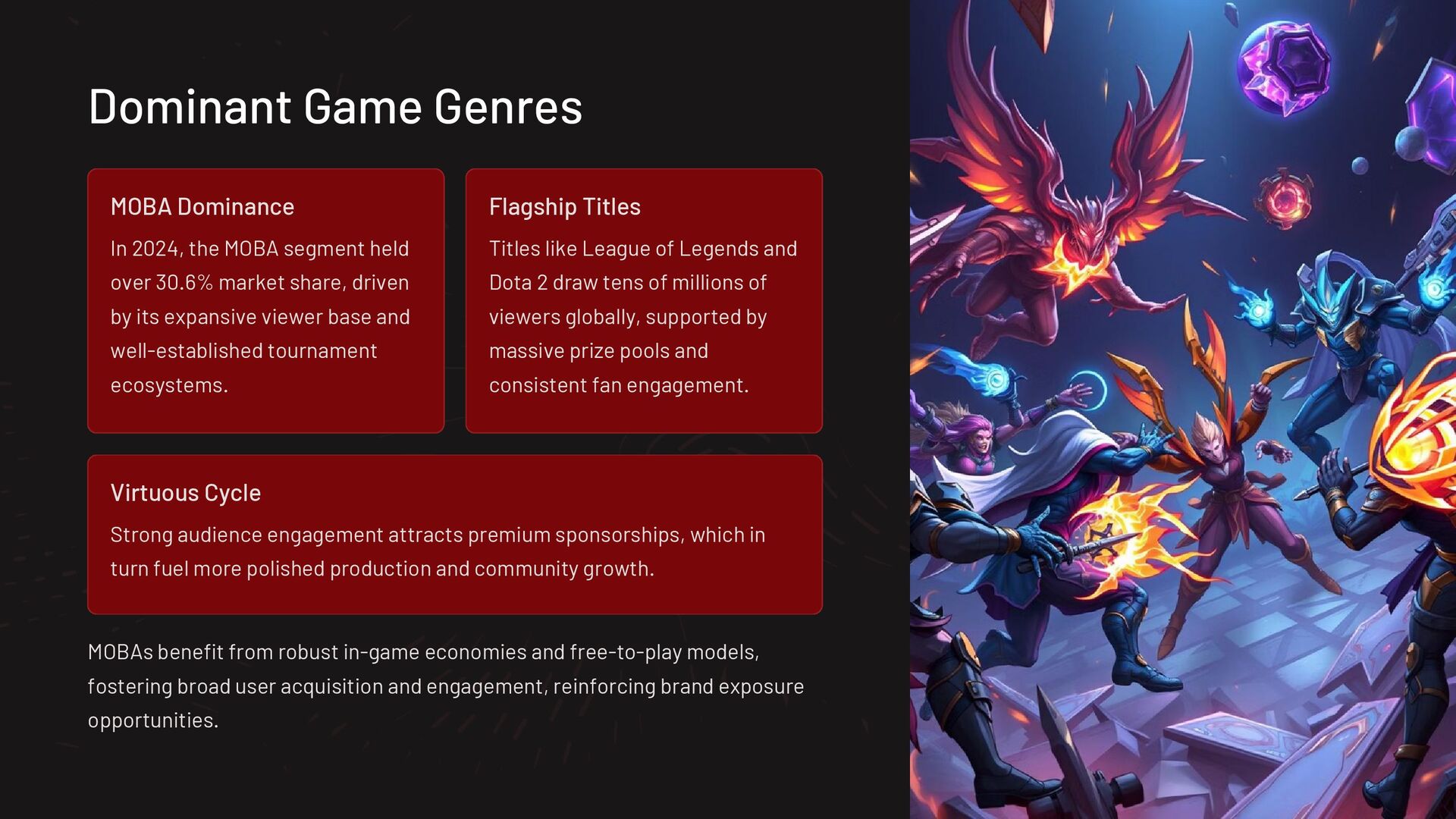

From a content perspective, MOBA (Multiplayer Online Battle Arena) games emerged as the top-performing genre, holding a 30.6% share. The success of this segment was attributed to high global viewership, structured competitive formats, and active fan participation across iconic titles such as League of Legends and Dota 2. The consistency in tournament scheduling and team narratives further deepened audience retention and sponsor loyalty.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}