a legally enforceable obligation to pay principal and (usually) interest thereon. • And in many cases it is clear whether a debt exists and, if so, what constitutes principal and what constitutes interest. • But some cases are not so clear. The course begins with an exploration of these cases. • The Treasury Regulations under section 385 add some clarity but only in limited circumstances. 2

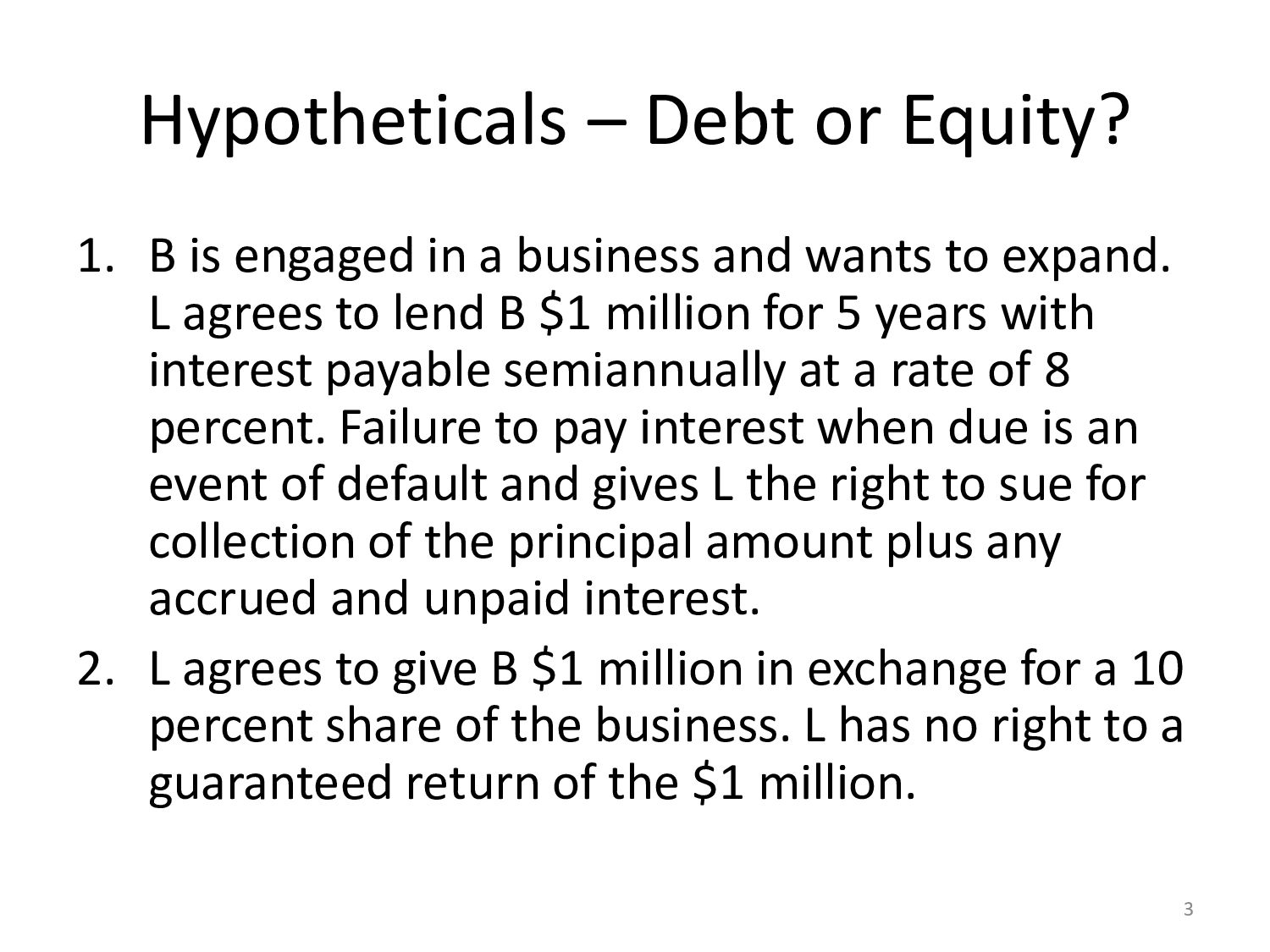

a business and wants to expand. L agrees to lend B $1 million for 5 years with interest payable semiannually at a rate of 8 percent. Failure to pay interest when due is an event of default and gives L the right to sue for collection of the principal amount plus any accrued and unpaid interest. 2. L agrees to give B $1 million in exchange for a 10 percent share of the business. L has no right to a guaranteed return of the $1 million. 3

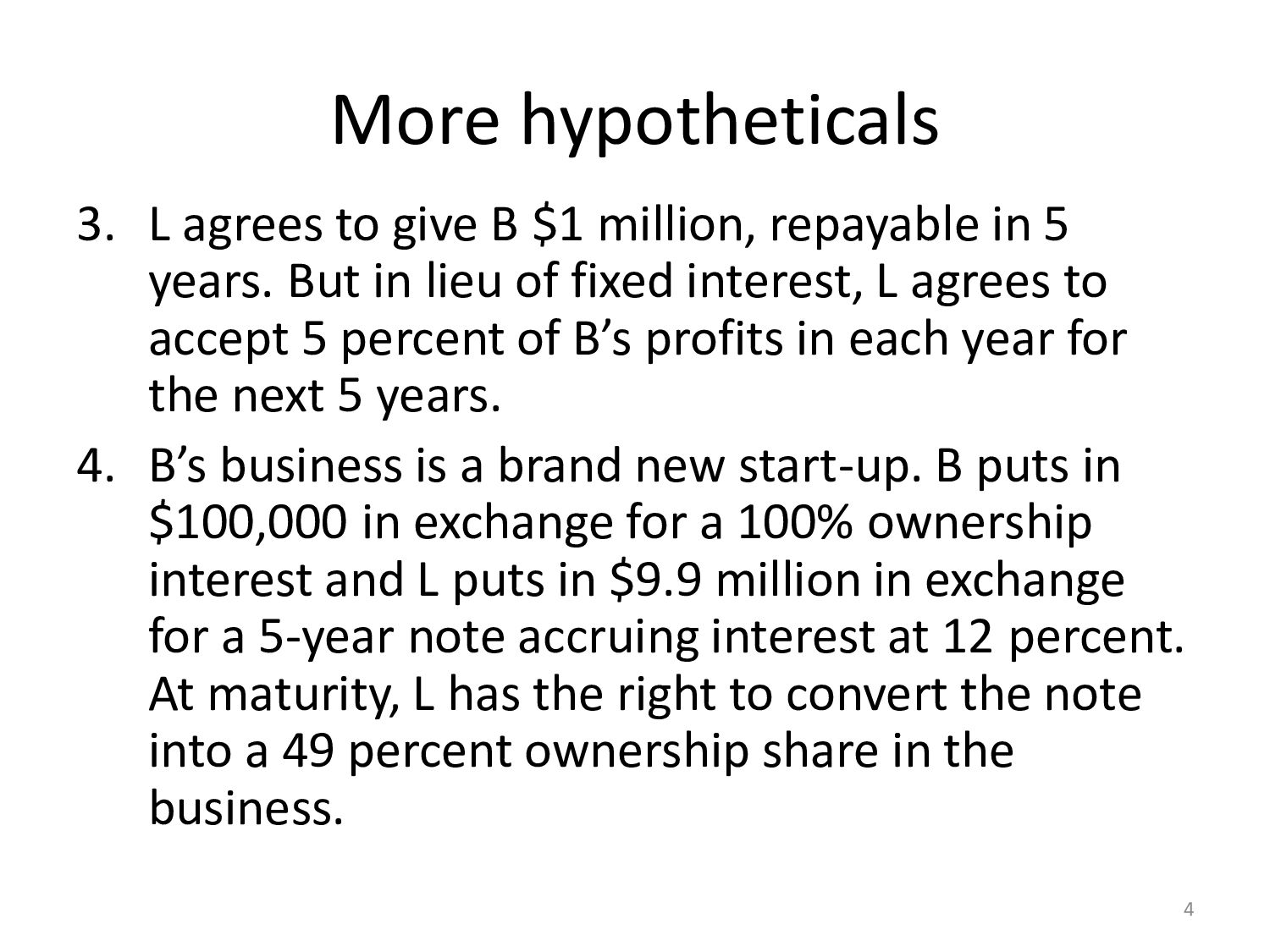

repayable in 5 years. But in lieu of fixed interest, L agrees to accept 5 percent of B’s profits in each year for the next 5 years. 4. B’s business is a brand new start-up. B puts in $100,000 in exchange for a 100% ownership interest and L puts in $9.9 million in exchange for a 5-year note accruing interest at 12 percent. At maturity, L has the right to convert the note into a 49 percent ownership share in the business. 4

the verge of an IPO. L gives B $9 million in exchange for a 3-year note for $9 million with interest at 10 percent, payable at maturity. But if B has a successful IPO, L’s note automatically converts into stock at a discount of 10 percent to the IPO price. For example, if the IPO price is $10 per share, L would receive 1 million shares. Debt or equity? 5

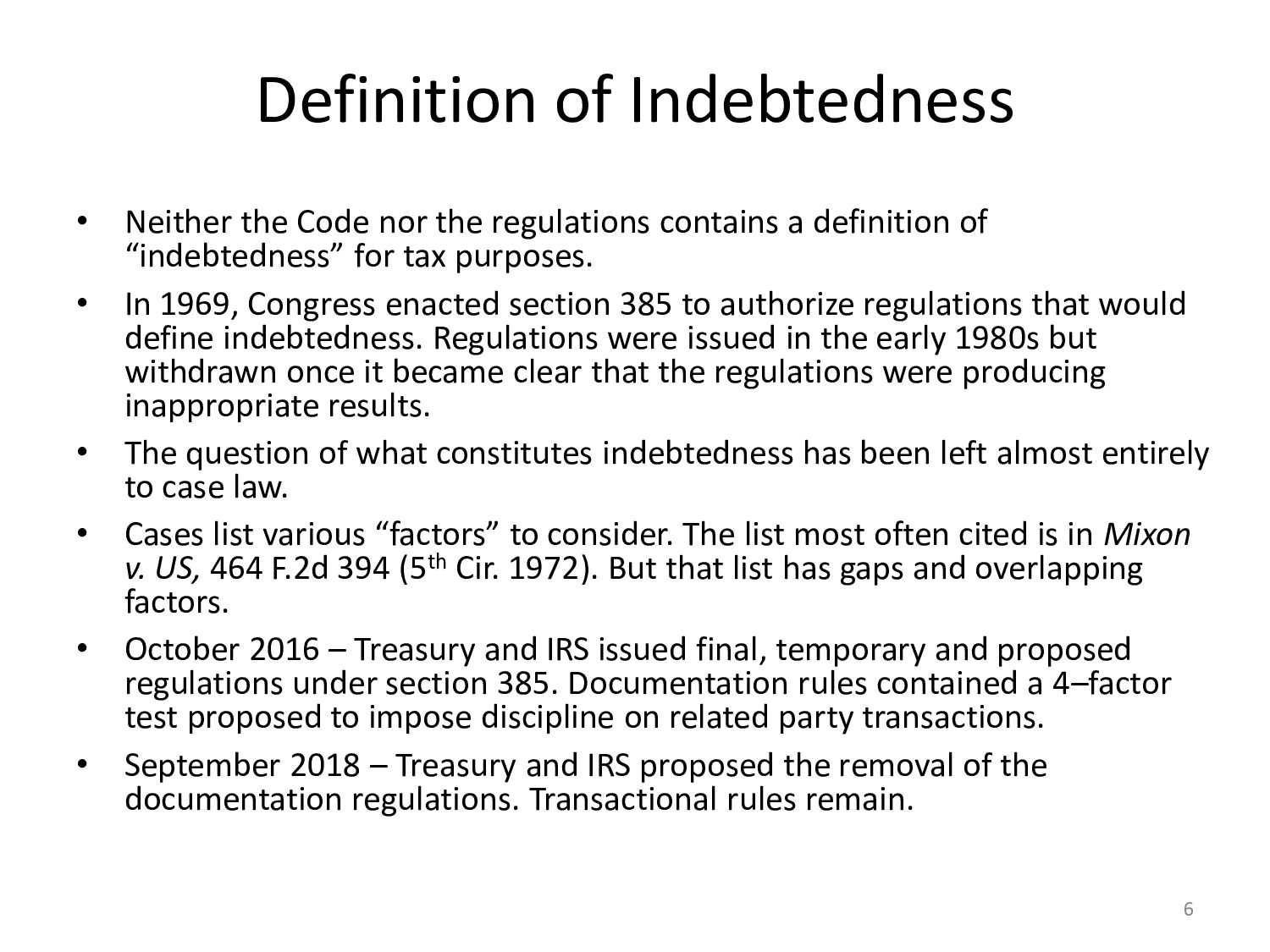

contains a definition of “indebtedness” for tax purposes. • In 1969, Congress enacted section 385 to authorize regulations that would define indebtedness. Regulations were issued in the early 1980s but withdrawn once it became clear that the regulations were producing inappropriate results. • The question of what constitutes indebtedness has been left almost entirely to case law. • Cases list various “factors” to consider. The list most often cited is in Mixon v. US, 464 F.2d 394 (5th Cir. 1972). But that list has gaps and overlapping factors. • October 2016 – Treasury and IRS issued final, temporary and proposed regulations under section 385. Documentation rules contained a 4–factor test proposed to impose discipline on related party transactions. • September 2018 – Treasury and IRS proposed the removal of the documentation regulations. Transactional rules remain. 6

debt and equity features, could it be part debt and part equity? • With rare exceptions, the cases hold an instrument to be either debt or equity. That is, they do not “bifurcate.” • The only two cases to bifurcate are Richmond, Fredericksburg & Potomac RR v. Comm’r, 528 F.2d 917 (4th Cir. 1975); and Farley Realty Corp. v. Comm’r, 279 F.2d 701 (2d Cir. 1960). Both involved debt with an “equity kicker” (profit participation). • More on this topic later when we talk about convertible debt and section 385. 7

$1 million in cash plus B’s note for $9 million, payable in installments over 5 years, with interest. • W performs services for E and accepts payment in the form of E’s note for $100,000 payable in one year with interest. • In both cases, a debt is created but there was no loan. A debt instrument does not have to be issued in exchange for money. 8

a sum certain (“principal”) • Payable on one or more fixed dates or on demand • Right to interest at a fixed or floating rate, regardless of profits • Creditor’s rights in the event of nonpayment 9

(direct or indirect) of the borrower, or are they under 100% common control? • Is the borrower thinly capitalized? • What is the intention of the parties? • The “acid test” – would an unrelated lender be willing to make a loan of the same amount to the borrower on generally the same terms (other than possibly the interest rate)? 11

corporation. S Corp lends $1 million to T in exchange for a 10-year note with traditional debt features other than a low rate of interest. S Corp has plenty of remaining cash and is unlikely to need the $1 million back to operate its business. • Is this a loan or something else? 12

of a corporation rather than into it, and the recipient is the 100% owner, the issue is whether there is a bona fide intention to repay. • Several court cases have found that such intention did not exist and hence a dividend. A leading case is Alterman Foods v. U.S., 505 F.2d 873 (5th Cir. 1974). • If the taxpayer wants the loan to be respected, he should be scrupulous in abiding by the terms. • Note that if the shareholder is a U.S. company and the payor is a foreign corporation, section 956 would treat the loan as a dividend even if the debt is valid. 13

R forms an LLC and contributes $5 million in exchange for all the equity. The LLC borrows $15 million from a bank and buys a parcel of real estate for $20 million. The bank has a security interest in the property acquired, but R is not personally liable on the debt. If the venture fails, the bank’s only recourse is to foreclose on the property and to recover any deficiency from the LLC. • Is this a valid debt? 14

declined in value to $10 million. Assume the outstanding debt amount is still $15 million. R sells the equity in the LLC to H for $1. Is the debt still valid with H as the new obligor? For the full $15 million? • Alternatively, suppose R transfers the equity in the LLC (or the property) to the bank. Does R have – a) An amount realized on the disposition of the property of $15 million, or b) An amount realized of $10 million and $5 million of income from the cancellation of indebtedness (i.e., COD income)? 15

fair market value of the property securing the debt is not respected for tax purposes. Estate of Franklin v. Comm’r, 544 F.2d 1045 (9th Cir. 1976). • In non-abusive cases where originally-valid debt is assumed but the property is underwater, courts have respected the debt up to the value of the property. • If property is transferred to the holder of a nonrecourse loan, there is no COD income and the amount realized is the full amount of the debt. Comm’r v. Tufts, 461 U.S. 300 (1983). 16

L for 20 years. The monthly rental amount is higher than the market rate. L is responsible for all expenses related to the airplane. At the end of the lease term, L has a right to buy the airplane for $1. • Same facts except that the rent is set at the market rate and L has the right to buy the airplane at the end of the lease term for its then fair market value. The expected useful life of the airplane is 25 years. 18

a debt given by the purported lessee to acquire the property is called a “finance lease.” • There is little difference in substance between a long-term net lease and a purchase-money obligation. • Many cases have considered this question, and the IRS has published safe-harbor guidelines. • Financial accounting has a similar concept, but the standards are not the same. 19

has litigated many cases on a contingent fee basis and expects to collect substantial fees over the next several years. To get some cash in the door now, LF enters into a contract with S under which S gives LF $5 million today in exchange for all of LF’s future contingent fees on a specified list of cases until S has received $5 million plus interest on its investment at a rate of 18 percent. • Sale or nonrecourse financing? 20

rate cap, it is clear that LF has sold its future income to S and the cash received is taxable income. No debt exists from F to S. • If it is highly likely the interest rate cap will be hit and S is taking little risk other than timing, the transaction can be viewed as a nonrecourse loan. Several cases have so held. See, e.g., Mapco v. U.S., 556 F.2d 1107 (Ct. Cl. 1977). • Intermediate cases are unclear. • Novoselsky v. Comm’r, T.C. Memo. 2020-68 (May 28, 2020) – repayment contingency in a litigation funding agreement negates loan treatment and funds are currently taxable – there was no “reasonable expectation of repayment regardless of the success of the venture” 21

pays life insurance company L $1 million for the right to monthly payments of $5,000 starting at age 65 for the longer of the rest of his life or 10 years. (If A dies before age 75, his estate is entitled to the remaining monthly payments.) • Same facts except that upon reaching age 65 A has the right to elect a lump sum settlement for an amount that exceeds $1 million. 22

insurance company and called an annuity will be taxed as an annuity. This means there will be no taxation during the deferral period and straight line principal recovery over the insured’s expected life, assuming he does not elect cash settlement. • If the obligation is from a non-insurance company, it must have a “real and substantial” life contingency to qualify as an annuity. 23

new customers with a low credit score to deposit $500 cash as a condition of obtaining service. The deposit earns interest at a market rate similar to a bank savings account. If the customer pays bills on time for 6 months, the deposit and interest earned thereon can either be refunded or applied to future bills until used up. 24

Power & Light Co., 493 U.S. 203 (1990), the Supreme Court held that the utility had received a deposit (i.e., had borrowed the money from its customers) and so was not taxable on the cash as prepaid income for future electric services. • The right of the customer to get the cash back is key. If the deposit can only be applied to future bills for service, then it is not a loan even if the deposit earns interest. 25

712 (5th Cir. 1972) held that the shareholder was the true borrower, even though the corporation was ultimately successful and was able to pay off the debt on its own. • The test is essentially the same as the related- party loan test – could the corporation have borrowed without the shareholder guarantee (albeit at a higher interest rate)? 28

of corporations that includes numerous operating subsidiaries. P and its subs enter into a line of credit agreement with lender L for up to $50 million. P and each subsidiary is jointly and severally liable for the entire amount drawn on the line, regardless of which company received the proceeds of any particular draw. P and its subs enter into a Contribution Agreement that requires each sub to repay the principal that it draws and to pay interest thereon, and that if any entity is called upon by L to pay more than its share of interest or principal, then it has a right to collect the excess payment from the entity that fell short in its payment. 29

on the debt, only one entity can get the interest deduction. • Because most groups file a consolidated federal income tax return, this is mostly a state tax issue. • Case law deals mostly with cash-basis co-obligors and holds that the person who pays the interest expense is entitled to the interest deduction. • In the corporate setting, where accrual accounting prevails, the entity that is responsible for the interest and principal under the Contribution Agreement should be entitled to the interest deduction. 30

means an obligation to pay a fixed principal amount on a specified date or on demand, where the failure to pay gives rise to creditor’s rights. • Liability – a broader term, including debt and some contingent obligations. Also an accounting concept. • Obligation – the broadest category. 32

any legal document evidencing debt. • Bond – a medium to long-term corporate or government debt instrument. • Note – a short to medium-term corporate or government debt instrument, or a debt instrument of any other issuer. • Debenture – an unsecured, corporate debt instrument. • Mortgage loan – a debt instrument secured by real estate. • T-bill – a U.S. Government debt with a term of 1 year or less. 33

money. • In practice, interest is paid periodically – typically monthly, quarterly, semiannually or annually. • If a lender allows a borrower to defer the payment of interest until maturity, it is in effect making an additional loan of the interest. • Compound interest is interest on unpaid interest. 34

Term of loan = 3 years • Annual interest rate = 10 percent • First year interest accrual = $100 ($1,000 10%). If not paid, loan balance is $1,100 • Second year interest accrual = $110 ($1,100 10%). If not paid, loan balance is $1,210 • Third year interest accrual = $121 ($1,210 10%). Total amount due after 3 years is $1,331 35

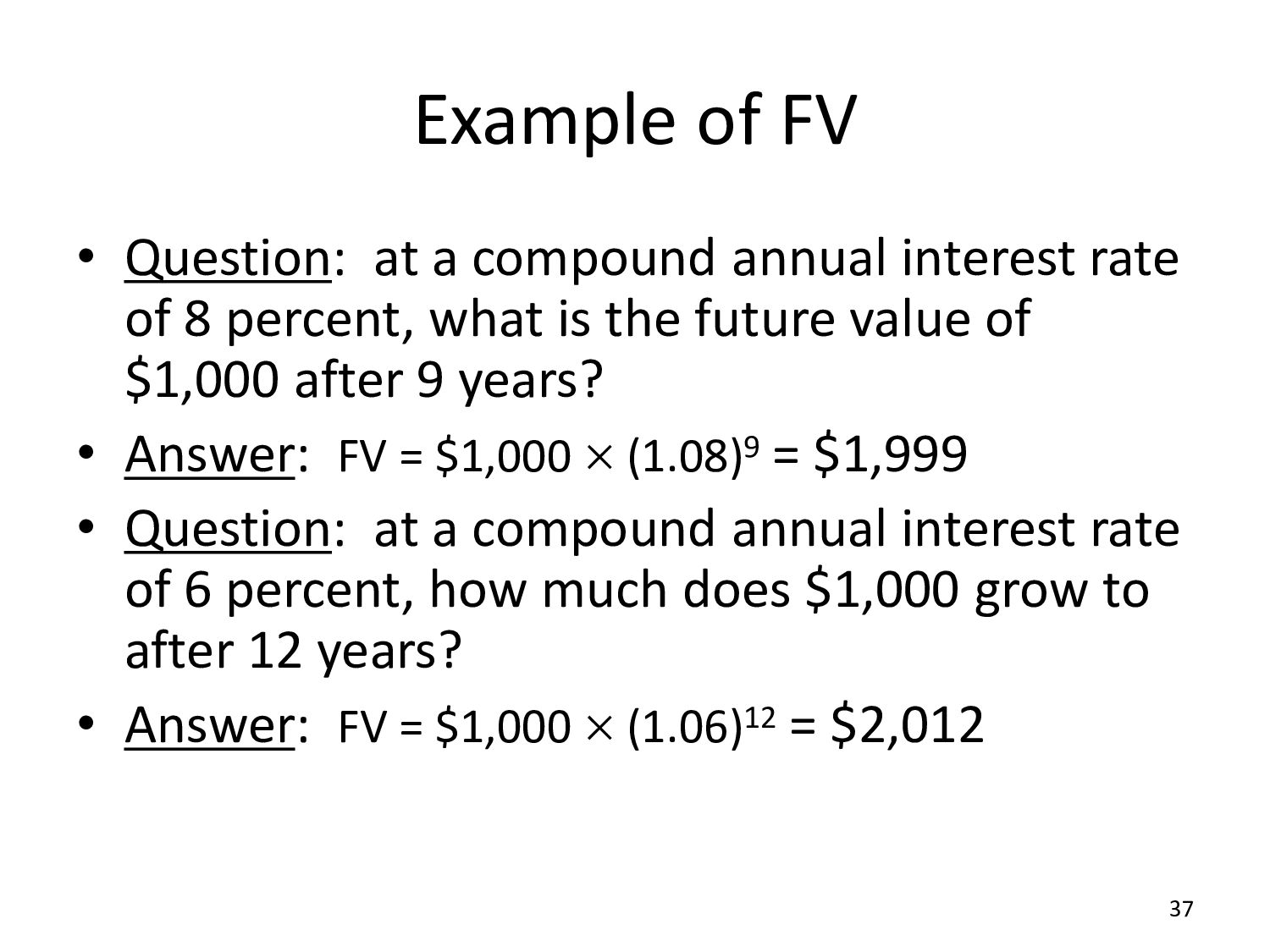

is the amount to which the present value (PV) will grow at a specified rate of compound interest. • The formula for determining future value is: FV = PV (1 + i)t • PV = present value • i = rate of interest, per period • t = term of the instrument (number of periods) 36

rate of 8 percent, what is the future value of $1,000 after 9 years? • Answer: FV = $1,000 (1.08)9 = $1,999 • Question: at a compound annual interest rate of 6 percent, how much does $1,000 grow to after 12 years? • Answer: FV = $1,000 (1.06)12 = $2,012 37

an amount of money will be double the PV if the product of the interest rate and the number of periods is 72. • Examples – money doubles in 6 years at 12%, in 8 years at 9%, etc. • Approximation is best when i and t are close in value (e.g., 8 and 9). 38

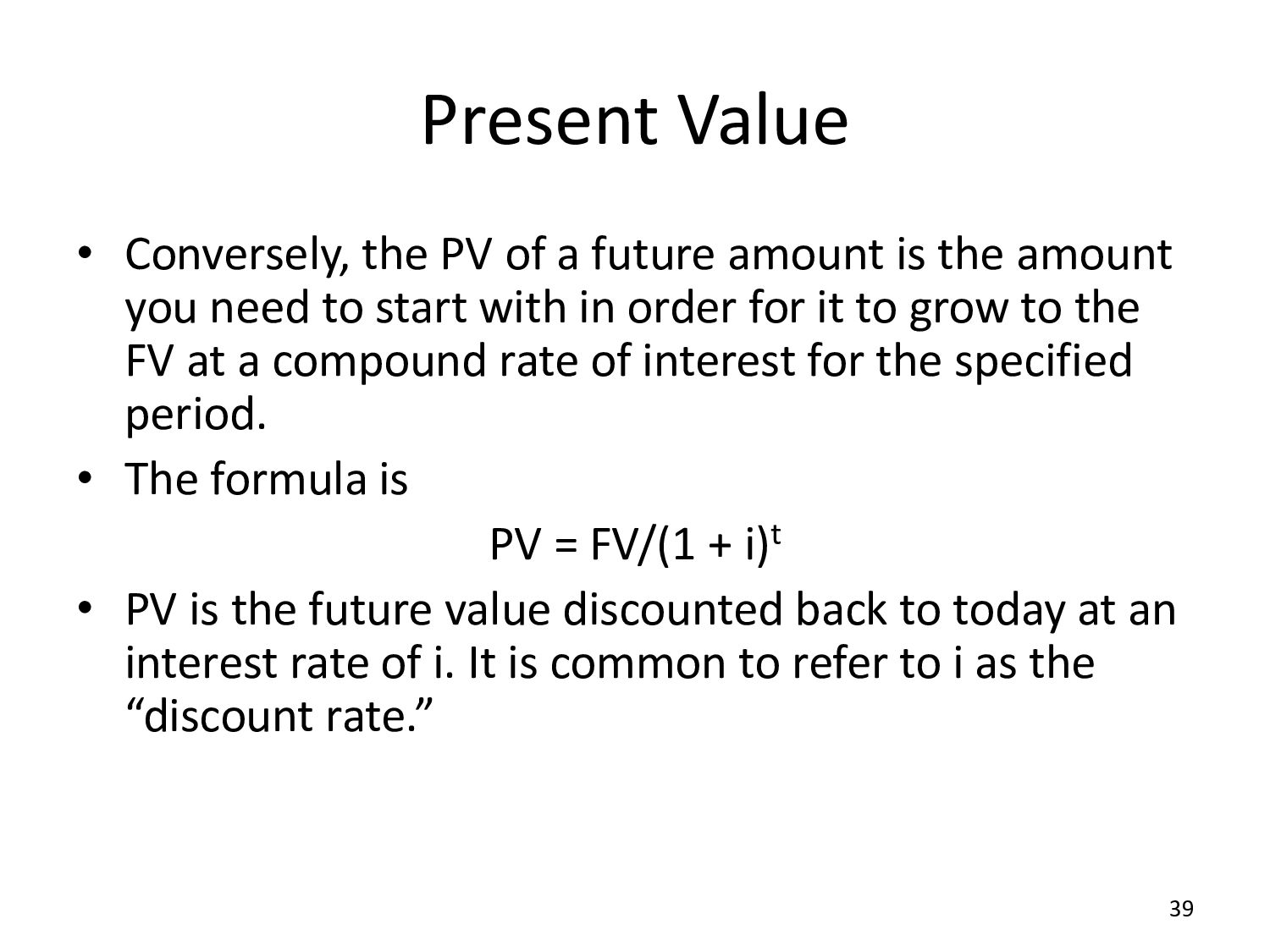

is the amount you need to start with in order for it to grow to the FV at a compound rate of interest for the specified period. • The formula is PV = FV/(1 + i)t • PV is the future value discounted back to today at an interest rate of i. It is common to refer to i as the “discount rate.” 39

single payment of $1 million after 4 years (a “zero coupon” bond). The annual interest rate is 5 percent. What does the bond sell for? • Answer: PV = $1 million/(1.05)4 = $822,702 40

X has a face amount of $1,000, a term of 8 years, and a stated interest rate of 9% compounded annually. At maturity the bond pays $2,000 (Rule of 72). • Bond Y has a face amount of $2,000 and no stated interest. It is sold at original issue at a discount price equal to 50% of its face amount, or $1,000. • The bonds are identical in substance – only the labels differ. This shows that original issue discount (OID) is a form of interest. 41

either – Interest at a single fixed rate, or – Interest at a rate that resets periodically based on current short-term rates at the time of each reset (a floating or variable rate). • On most loans, interest must be paid or compounded at least annually. • The tax law generally follows these conventions. 42

of interest rate. • If a loan has a known fixed rate of interest that is paid or compounded at least annually, the YTM is that rate. • If the interest rate is unknown or is not stated as a single rate that is paid or compounds at least annually, then the YTM must be computed. • For any loan, the YTM is the discount rate that, when used in computing the PV of all payments to be made on the loan, produces an amount equal to the amount loaned. 43

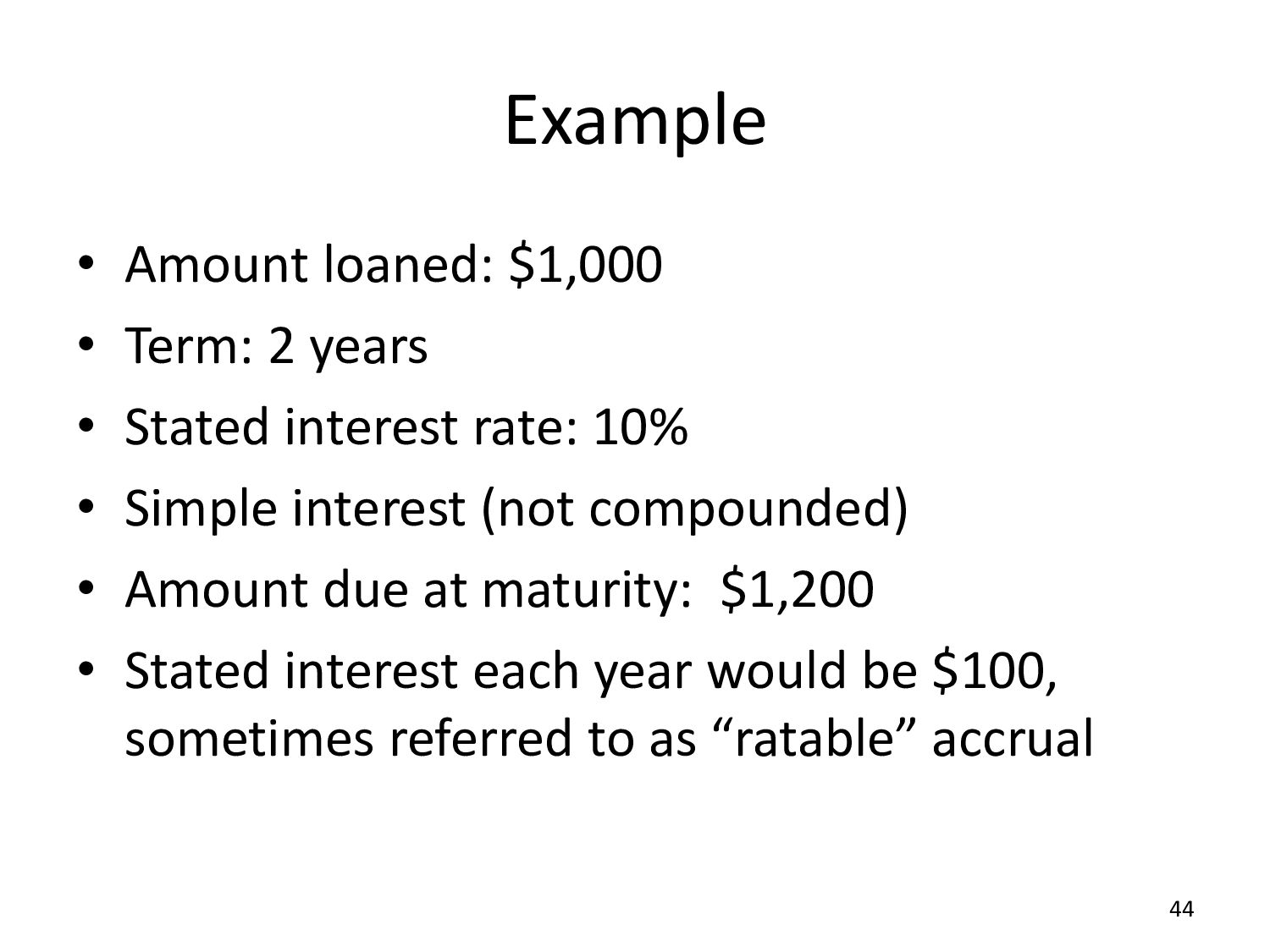

Stated interest rate: 10% • Simple interest (not compounded) • Amount due at maturity: $1,200 • Stated interest each year would be $100, sometimes referred to as “ratable” accrual 44

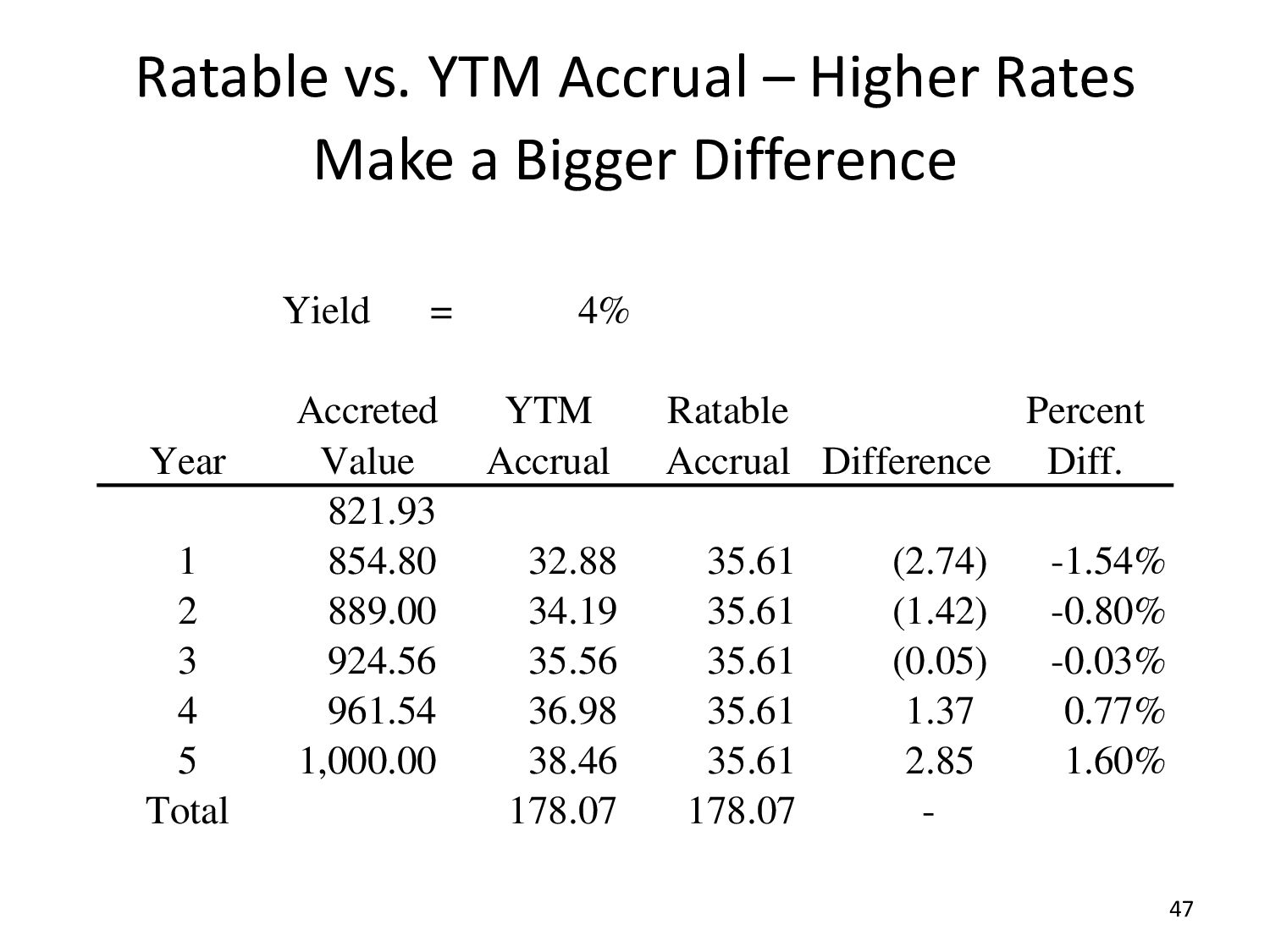

Year 1 accrual is $1,000 9.545% = $95.45 • Loan balance increases to $1,095.45 • Year 2 accrual is $1,095.45 9.545% = $104.55 • Loan balance after 2 years is $1,200 • The interest accrual is $4.55 less than ratable accrual in Year 1, and $4.55 more than ratable accrual in Year 2 46

semiannually, or twice a year. • All computations are made per period, not per year, so you have to multiply or divide by 2, as appropriate. • Example: a zero-coupon bond issued for $50 has a YTM of 8 percent, compounded semiannually. What is the accrual for the first six months? • Answer: the accrual is $2 ($50 × 8%/2) 49

before maturity. Such a loan is called an “amortizing” loan. • A loan that calls for level payments before maturity is called a “self-amortizing” loan (e.g., residential mortgages). • Each payment consists of a greater amount of principal and a lesser amount of interest. • A calculator or spreadsheet can be used to compute the amount of the periodic payment. 50

is the timing of income, gain, expense, or loss recognition in respect of economic returns from the instrument? • Character: What is the character of the income, gain, expense, or loss generated by the instrument? (This can also include tax-preferred income of various types, such as tax- exempt interest income from a municipal bond.) • Source: What is the source of the income generated by the instrument? (This question is relevant for determining whether U.S. withholding tax is imposed on payments from a U.S. person to a foreign person and for purposes of computing the foreign tax credit.)

of the instrument (e.g., section 1256 (futures), Reg. §1.446-3(NPCs)) • The identity of the taxpayer (e.g., dealers and traders in securities, which are subject to mark to market taxation under section 475) • The purpose for which the transaction is entered into by the particular taxpayer (e.g., straddle and hedging rules).

instrument whose value is derived from one or more underlying assets, market securities or indices. The derivative contract specifies conditions – in particular, dates and the resulting values of the underlying variables – under which payments (including the final payment), are to be made between the parties.

euro Company plans borrowing in near future and wants to hedge against interest rate increase Company enters into purchase agreement denominated in Euro and wants to hedge against possible decline in value of Dollar against the Euro Manufacturer uses natural gas in production and wants to hedge against increased fuel costs, but retain benefit if prices drop Futures contract to sell Treasury bonds Option to buy natural gas

means you own it, have a right or contract to buy it for a fixed price, or otherwise profit from the appreciation in the property and/or suffer from a decline in its value. • Having a “short” position means you have a contract or obligation to deliver or sell the property for a fixed price, or otherwise profit from a decline in the value of the property and/or suffer from an increase in its value.

position) agrees to deliver to the buyer (long position): – Specified property – At specified price or rate (contract price or rate) – On a specified future date (forward date) Seller Buyer Forward Price Property $0$ $ For Delivery in Future

Not exchange-traded – Non-standardized terms that can be tailored to client – Price and quantity generally fixed, but also can be variable determined by a formula – Holder generally makes no initial payment because contract price/rate is set so that contract’s initial value = $0. But a forward contract can also be “prepaid,” which means that one party pays cash up front and receives specified property on a specified future date. – Can be “cash settled” for the difference between the specified price and the value of the property.

and B enter into a contract under which S agrees to sell to B (and B commits to buy) 100,000 barrels of a specified grade of crude oil on July 15, 20xx at a price of $95 per barrel, to be paid on the same date the oil is delivered. • Prepaid forward contract: Same as above, except that B pays S $9.4 million on January 15, 20xx in exchange for S’s commitment to deliver 100,000 barrels of oil on July 15, 20xx. • Cash settlement: The spot price of oil on July 15, 20xx is $90 per barrel. On the first contract, above, the parties settle by B making a cash payment of $500,000 to S. No oil is actually delivered (at least not by S).

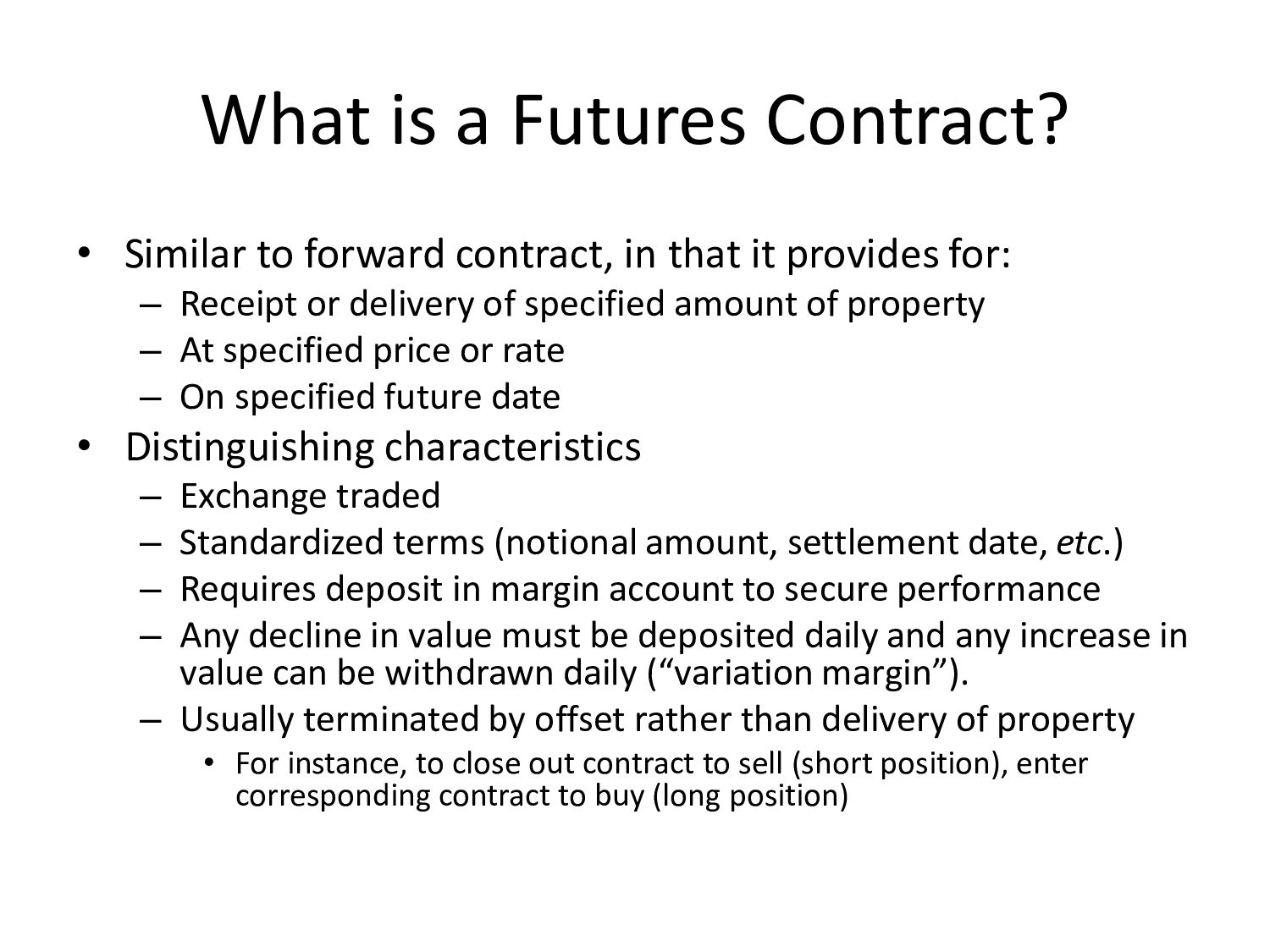

in that it provides for: – Receipt or delivery of specified amount of property – At specified price or rate – On specified future date • Distinguishing characteristics – Exchange traded – Standardized terms (notional amount, settlement date, etc.) – Requires deposit in margin account to secure performance – Any decline in value must be deposited daily and any increase in value can be withdrawn daily (“variation margin”). – Usually terminated by offset rather than delivery of property • For instance, to close out contract to sell (short position), enter corresponding contract to buy (long position)

no special recognition rule applies, normal gain/loss realization rules apply (wait-and-see). • Common law – If property is acquired pursuant to a forward contract, the property is just treated as having been acquired for the forward price. Gain or loss is not recognized at the time of contract. Similarly, the seller does not separately recognize gain or loss on the contract date, only when the property is sold.

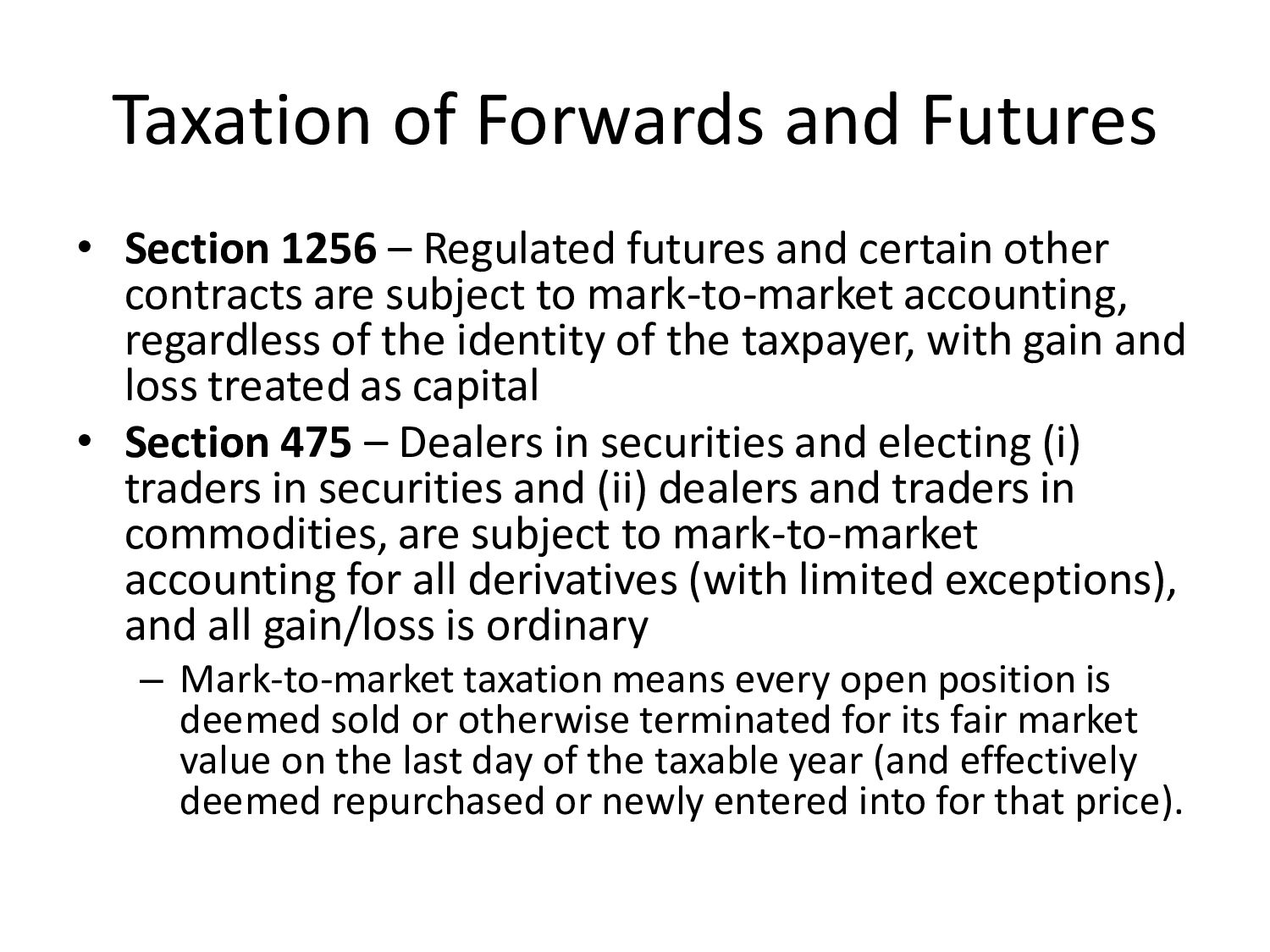

futures and certain other contracts are subject to mark-to-market accounting, regardless of the identity of the taxpayer, with gain and loss treated as capital • Section 475 – Dealers in securities and electing (i) traders in securities and (ii) dealers and traders in commodities, are subject to mark-to-market accounting for all derivatives (with limited exceptions), and all gain/loss is ordinary – Mark-to-market taxation means every open position is deemed sold or otherwise terminated for its fair market value on the last day of the taxable year (and effectively deemed repurchased or newly entered into for that price).

the Use of the Product • Business hedges – Includes certain transactions designed to manage business risks – Gain/loss is ordinary in nature, and timing is subject to matching rules (Treas. Reg. §1.446-4 and 1.1221-2) • Straddles – Definition – Taxpayer enters into offsetting positions, such as long and short positions on same stock – Section 1092 defers loss recognition if there is unrealized gain on an offsetting position • More on both of these topics in later classes

not obligation, to buy or sell property at a fixed price within a specified time period or on a specified date – Written on stocks, bonds, commodities, and currencies – Employee stock options are a special case (not discussed) • Call option – Right to purchase property • Put option – Right to sell property Option writer (seller) Option holder (buyer) Premium Property $ $0$ $

option • Holder – Purchaser of option • Premium – Price paid for option (usually a lump sum paid up front) • Expiration date – Last day option can be exercised • Strike price – Stipulated purchase price (call option) or sales price (put option) • Lapse – Holder fails to exercise option on or before expiration date • Listed option – Standardized option (notional amount, expiration date, etc.) traded on an exchange

buy a specified quantity of stock (or other property) from the option writer at a fixed price for a given period. • Example: a purchaser of a call option pays $10 to the writer of the option for the right to purchase one share of IBM stock at $100 from the writer on (or before) June 15, 20xx. • Thus, if the market value of IBM stock at expiration were below the strike price specified in the option contract, then the holder normally would not exercise the option and would allow it to lapse. On the other hand, if the market value of the underlying stock at expiration of the option is above the strike price, then the holder would exercise the option on its maturity date. • Generally no benefit from exercising an option early because price could change later. There could be an economic detriment.

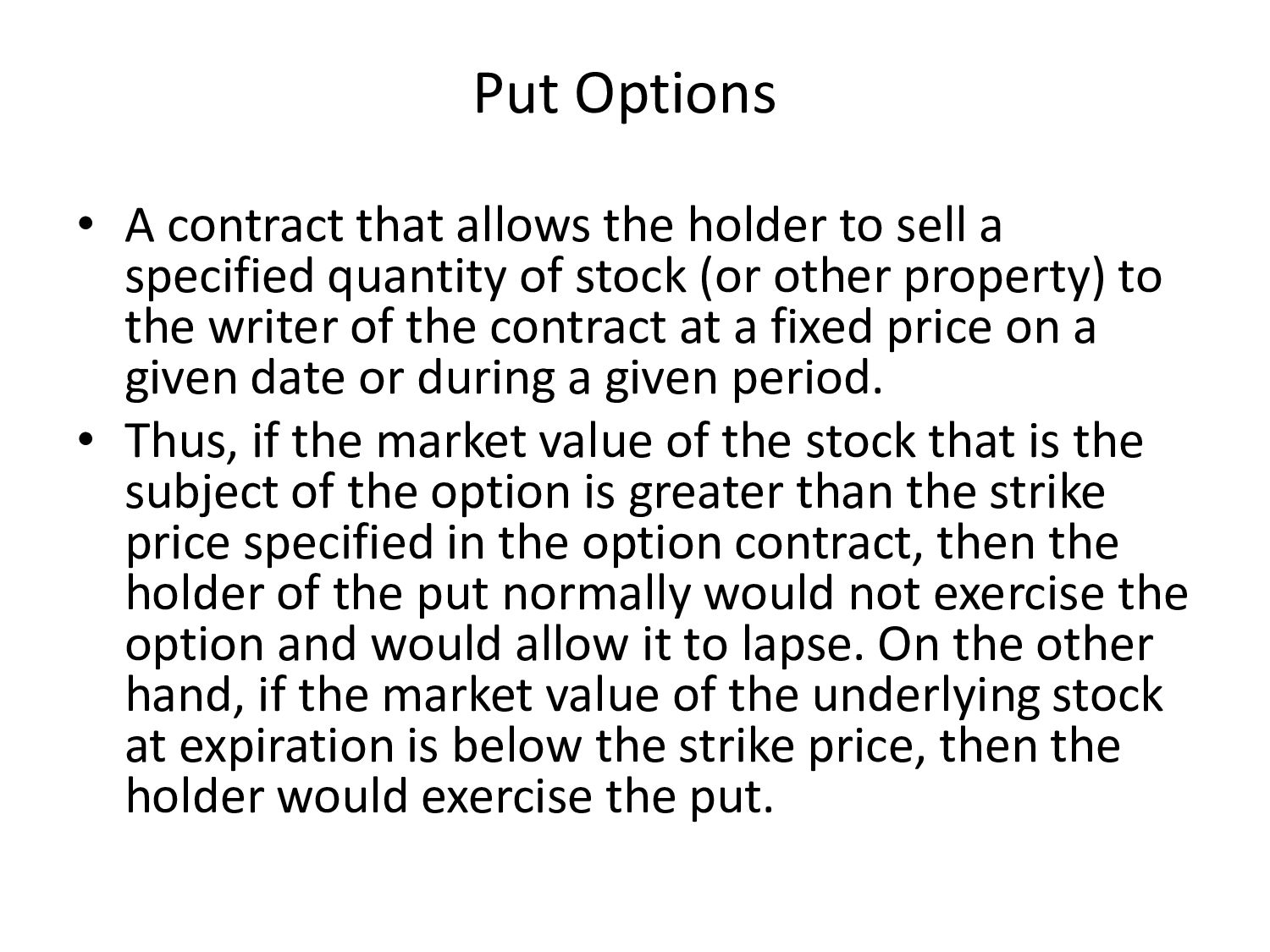

sell a specified quantity of stock (or other property) to the writer of the contract at a fixed price on a given date or during a given period. • Thus, if the market value of the stock that is the subject of the option is greater than the strike price specified in the option contract, then the holder of the put normally would not exercise the option and would allow it to lapse. On the other hand, if the market value of the underlying stock at expiration is below the strike price, then the holder would exercise the put.

money” if the property is worth more than the strike price. “At the money” means strike price equals value. A call is “out of the money” if the property value is less than the strike price. – These tests can be measured at any time. • Corresponding concepts apply for put options. • An option’s intrinsic value is its value if it were exercised immediately. An option has intrinsic value only to the extent it is in the money. • The remaining value of an option is called its time value. The time value of an option on its maturity date is zero.

options that are not marked to market (see below): – No taxable event upon entering into the option. – If option is cash-settled, gain or loss on the option is the difference between (or sum of) the amount of the option premium and the cash settlement amount. – If the option is physically settled, the price paid for property is the sum of (call option) or difference between (put option) the option premium and the exercise price. • §1234(b): in the case of the grantor, any gain or loss on the sale or lapse of an option is short-term, even if the option was outstanding for more than 1 year.

are marked to market. • An option is a section 1256 contract only if: – It is listed on a qualified board or exchange, and is either • A dealer equity option or • A nonequity option – For this purpose, an option on a broad-based stock index such as the S&P 500 is treated as a nonequity option. • Under §475, a “dealer in securities” or electing “trader” generally must mark to market all of its securities (including options and other derivatives). – There is an exception for identified positions that are hedges of other positions that are not marked to market.

the disposition of an option, forward, or futures contract generally is sourced according to the residence of the contract holder receiving the gain. • Thus, capital gain recognized by a foreign holder would be foreign- source gain that would not be subject to U.S. tax, unless the foreign holder is engaged in a U.S. trade or business with which the gain is effectively connected. • These rules also apply if the derivative is used for hedging purposes. • §865(j)(2) authorizes Treasury to promulgate regulations governing the source of gain from dispositions of forward contracts, futures, options, and other financial products. These regulations have not been promulgated to date.

provides for: – Payments between contracting parties – At specified intervals – Calculated by reference to a specified index – Upon a notional principal amount – In exchange for specified consideration or promise to pay similar amounts (Reg. §1.446-3(c)(1)) • Proposed regulations in 2011 would broaden the definition of specified index to include certain non-financial information, such as weather- related data (degree days, etc.).

interest rate caps, interest rate floors, commodity swaps, equity swaps, currency swaps, and similar agreements. • Section 1256 contracts, debt instruments, options, and forward contracts are not NPCs. • Function – most often used to hedge against risks of adverse price or interest rate fluctuations in the future. Counterparties are usually banks or dealers who offset (or absorb) the risk.

that, for a term (e.g., 5 years), – T will make semiannual payments to D based on a fixed rate (say 5%) times a notional principal amount (say $100 million) – D makes semiannual payments to T based on a floating interest rate (say 6-month LIBOR* plus 2 percent) times the same notional principal amount. • In practice, payments between T and D are netted. • *LIBOR stands for London Interbank Offered Rate. It will no longer be used as a reference rate for new transactions after December 31, 2021.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}