Having %$&# for Brains! Samuel Smith Old Brewery, the 250-year-old brewery that operates The Cock Tavern and more than 200 other pubs across Britain, in April instituted a “zero- tolerance policy” against swearing—the first time, pub historians say, a British pub chain has sought an official ban.

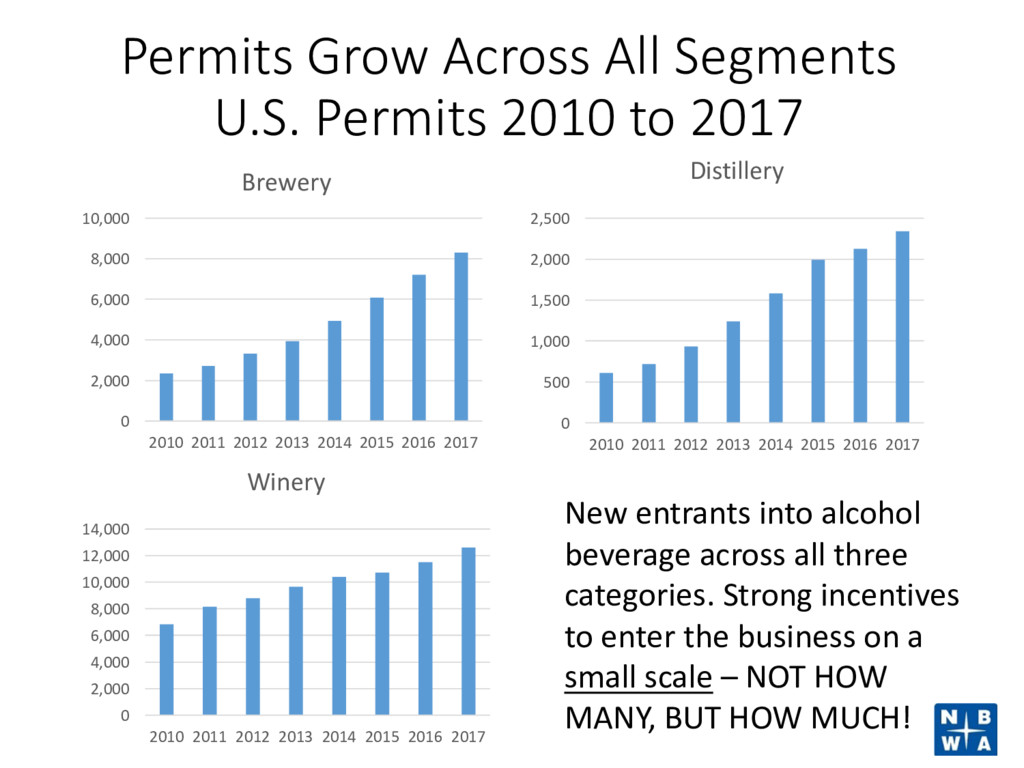

0 2,000 4,000 6,000 8,000 10,000 2010 2011 2012 2013 2014 2015 2016 2017 Brewery 0 500 1,000 1,500 2,000 2,500 2010 2011 2012 2013 2014 2015 2016 2017 Distillery 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 2010 2011 2012 2013 2014 2015 2016 2017 Winery New entrants into alcohol beverage across all three categories. Strong incentives to enter the business on a small scale – NOT HOW MANY, BUT HOW MUCH!

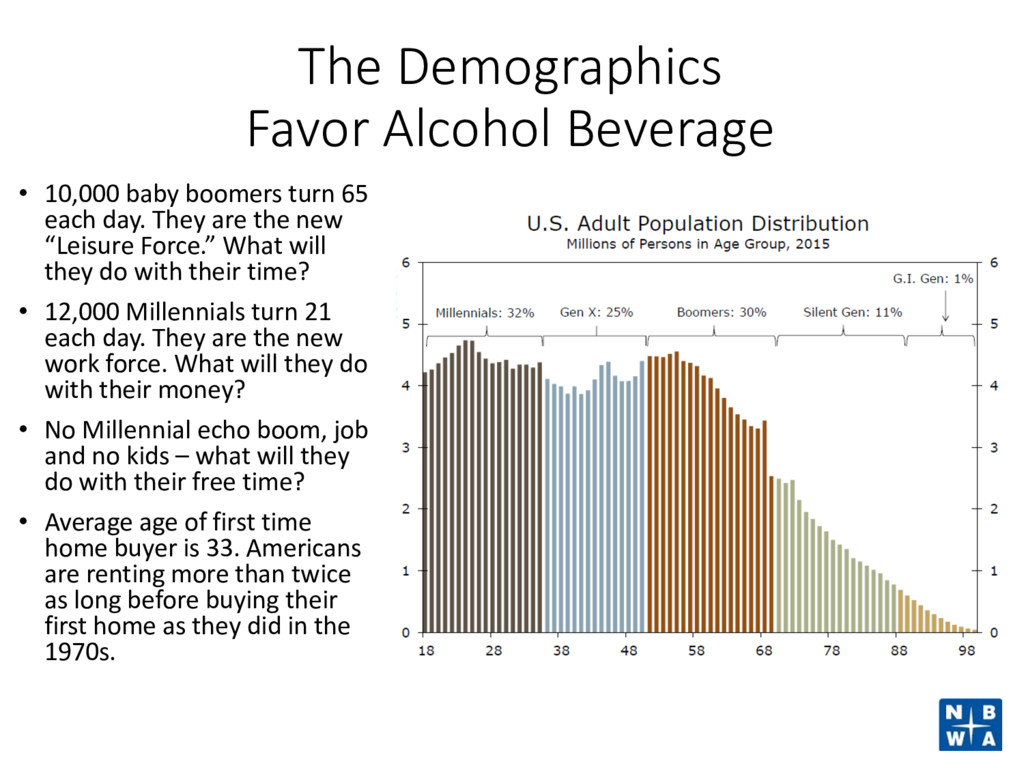

65 each day. They are the new “Leisure Force.” What will they do with their time? • 12,000 Millennials turn 21 each day. They are the new work force. What will they do with their money? • No Millennial echo boom, job and no kids – what will they do with their free time? • Average age of first time home buyer is 33. Americans are renting more than twice as long before buying their first home as they did in the 1970s.

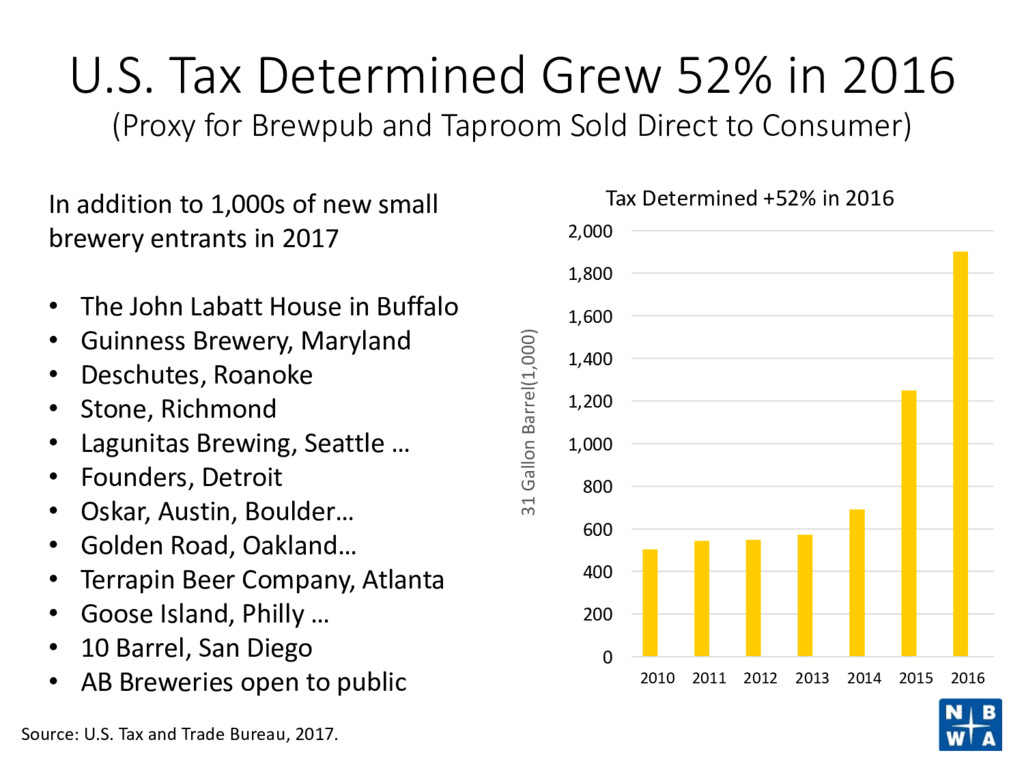

and Taproom Sold Direct to Consumer) 0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000 2010 2011 2012 2013 2014 2015 2016 31 Gallon Barrel(1,000) Thousands Tax Determined +52% in 2016 Source: U.S. Tax and Trade Bureau, 2017. In addition to 1,000s of new small brewery entrants in 2017 • The John Labatt House in Buffalo • Guinness Brewery, Maryland • Deschutes, Roanoke • Stone, Richmond • Lagunitas Brewing, Seattle … • Founders, Detroit • Oskar, Austin, Boulder… • Golden Road, Oakland… • Terrapin Beer Company, Atlanta • Goose Island, Philly … • 10 Barrel, San Diego • AB Breweries open to public

1. How many can there be? 2. How big can they be? 3. How many seats? 4. How much beer? 5. How do they get along with existing local retailer? 6. How many locations, six? I. 6 x 100 seats = 600 II. 6 x 1000 seats = 6000 III. 6 x 2000 seats = 12,000 7. What is a brewery…music venue, dog park, food truck court parking lot, yoga studio, or manufacturer? 1. How many can there be? 2. How big can they be? 3. How many seats? 4. How much beer? 5. How do they get along with existing local retailer? 6. How many locations, six? I. 6 x 100 seats = 600 II. 6 x 1,000 seats = 6,000 III. 6 x 2,000 seats = 12,000 7. What is a brewery…music venue, dog park, food truck court, yoga studio, or manufacturer?

find new accounts? As Milwaukee has grown, what are the new accounts and new places people are drinking? Question 2: Draft beer is important today as it was 75 years ago when everyone drank at the local tavern. Can you talk about how your company is using draft to grow? Question 3: New drinkers, new brands, new places to drink…what can you tell us about the consumer in your markets? How are the different or the same?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}