: who have a lot of experience in the construction site not facing a lot of problems because: the previous information and data about the works will help them: o in the money expenses within the construction period.

cost labour market plant or equipment are very important to: support the contractor and professional members to: decide the most reasonable price for every element of the construction.

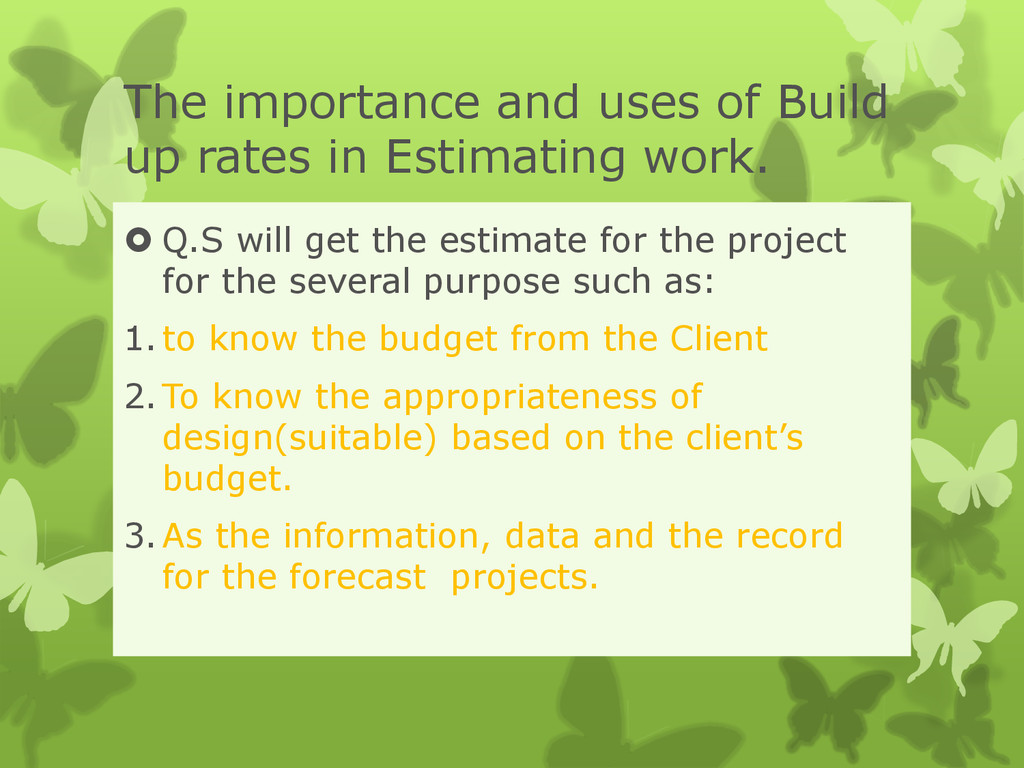

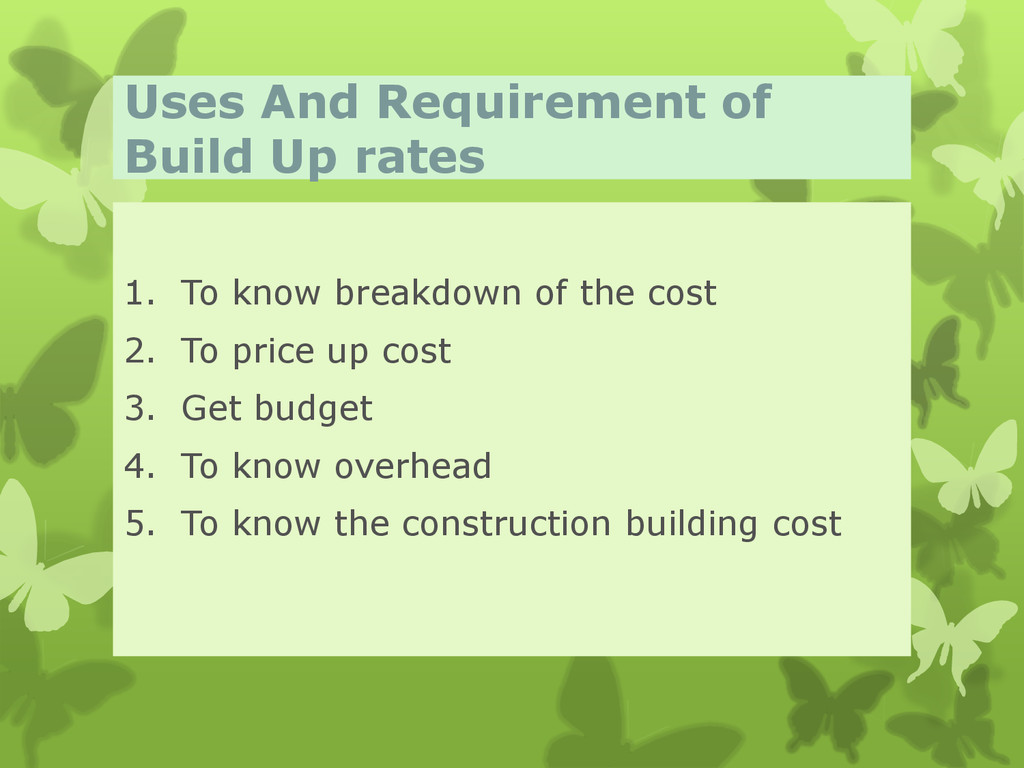

work. The professional members such as: Quantity Surveyor(Q.S) :will use the build up rate in the design stage. to get the estimate for the project.

work. Q.S will get the estimate for the project for the several purpose such as: 1.to know the budget from the Client 2.To know the appropriateness of design(suitable) based on the client’s budget. 3.As the information, data and the record for the forecast projects.

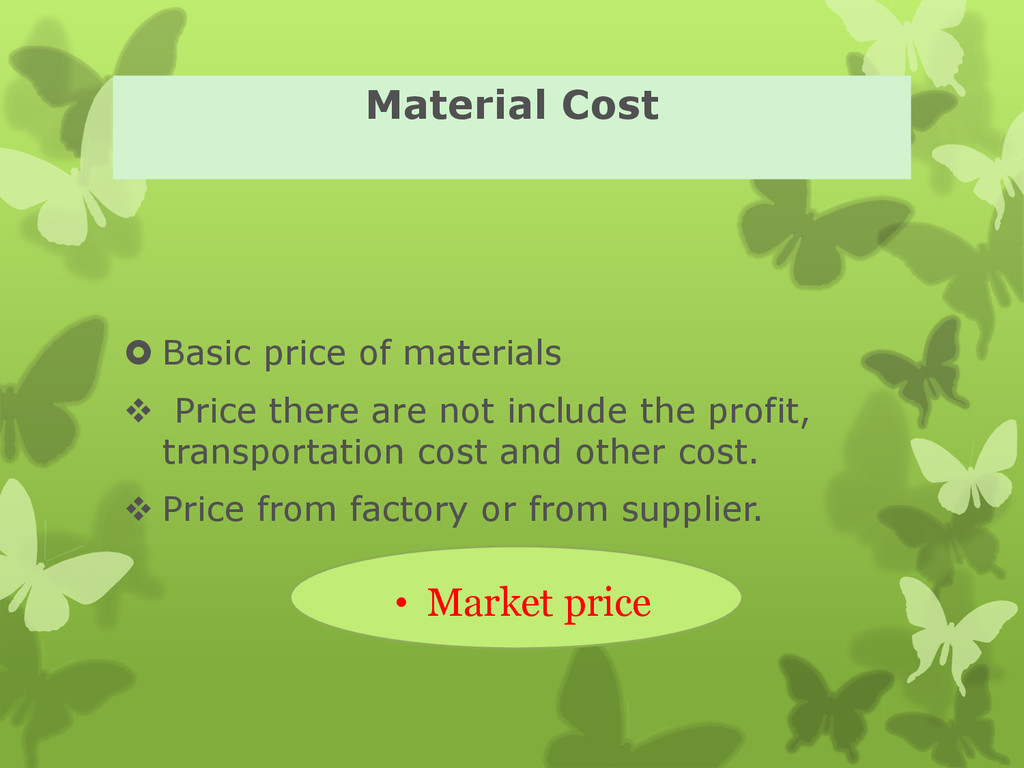

of material to the site. Extra cost to delivery material to the site. Supplier decide the price base on the distance of the place to deliver the material. Material Cost

substance noy fully utilized materials (not fully used): wastage. estimate for wastage: 10% -15% material on site gone to waste and damage. Material Cost

worker after he had completed his work. labour Payment is different based on their experience. Basically there are four(4) types of labour in the market.

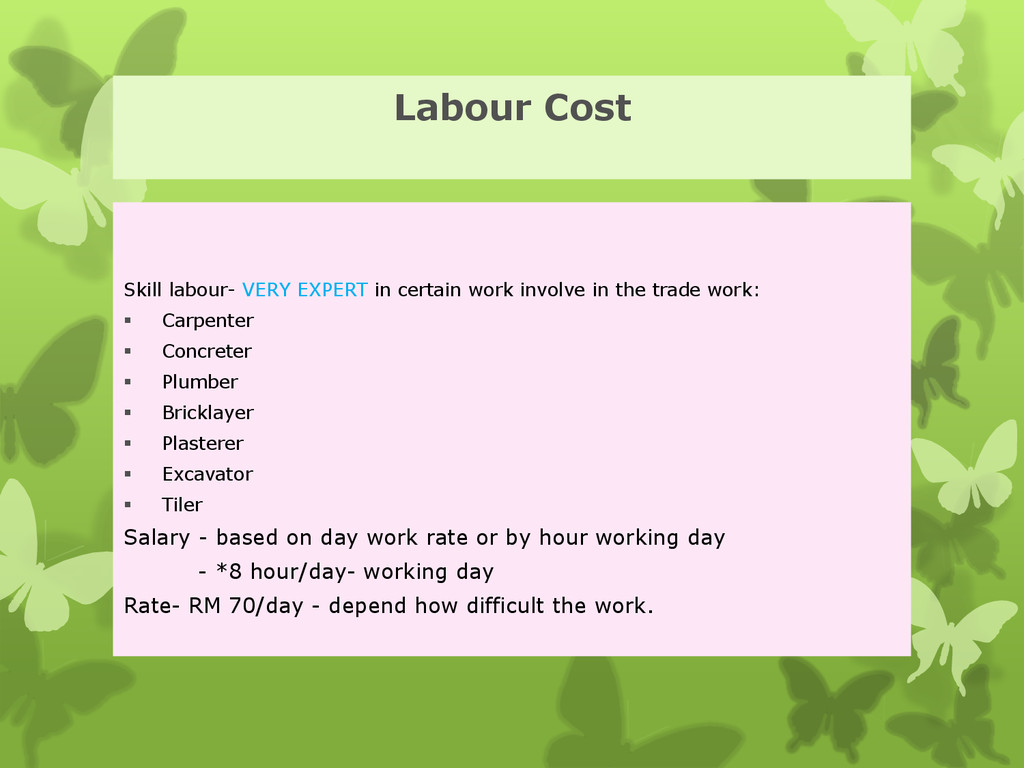

in the trade work: Carpenter Concreter Plumber Bricklayer Plasterer Excavator Tiler Salary - based on day work rate or by hour working day - *8 hour/day- working day Rate- RM 70/day - depend how difficult the work.

labour or medium labour. - do the work like: transport material by manual remove the material site clearing from the surplus Salary- around RM 20 – RM 30

group of workers: Skill workers, Medium workers, General workers - Responsible to operate and supervise on site the construction work on behalf of the contractor. - very expert in certain field: manage the material on site, tools/equipment,labour.

the worker to complete their work based on the certain unit. • Skill and labour capacity is not similar to each other. • Skill must be measured by labour constant. • Unit : hour/m, hour/m2 : hour/m3 ,hour/kg : etc.

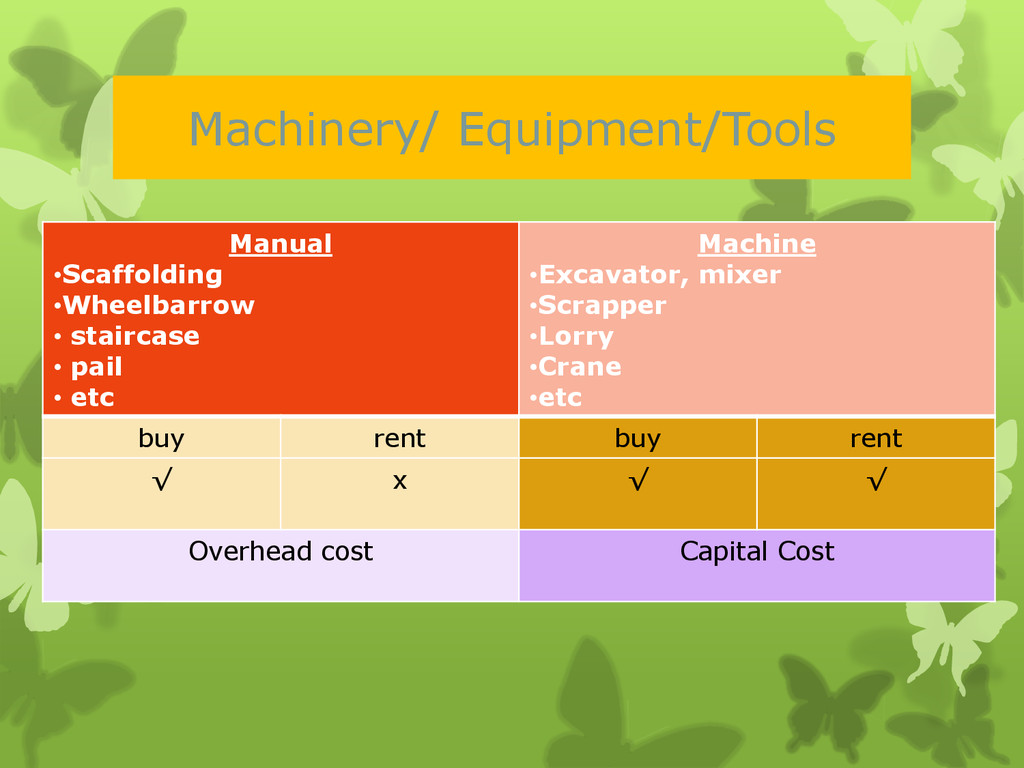

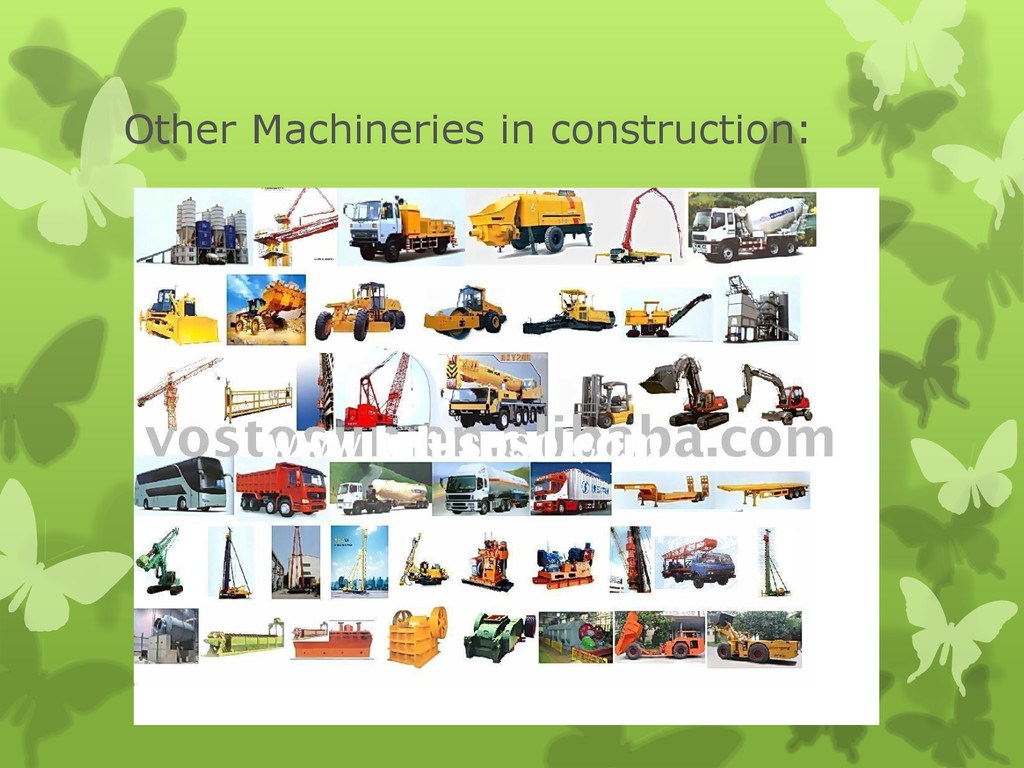

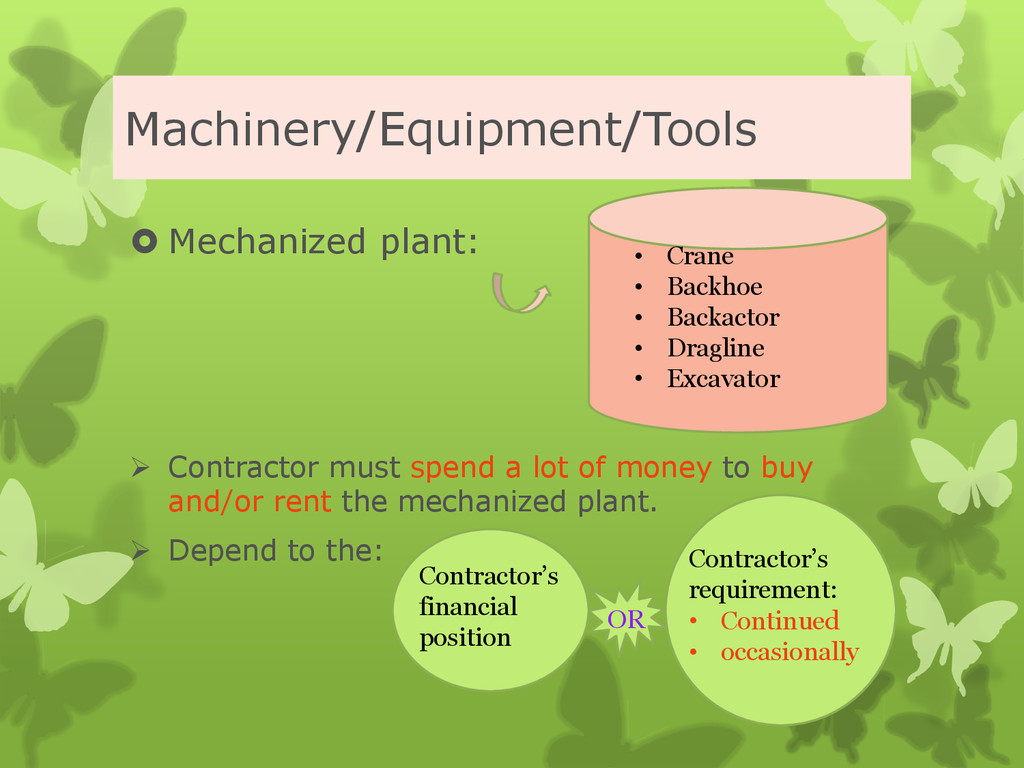

of money to buy and/or rent the mechanized plant. Depend to the: • Crane • Backhoe • Backactor • Dragline • Excavator Contractor’s financial position Contractor’s requirement: • Continued • occasionally OR

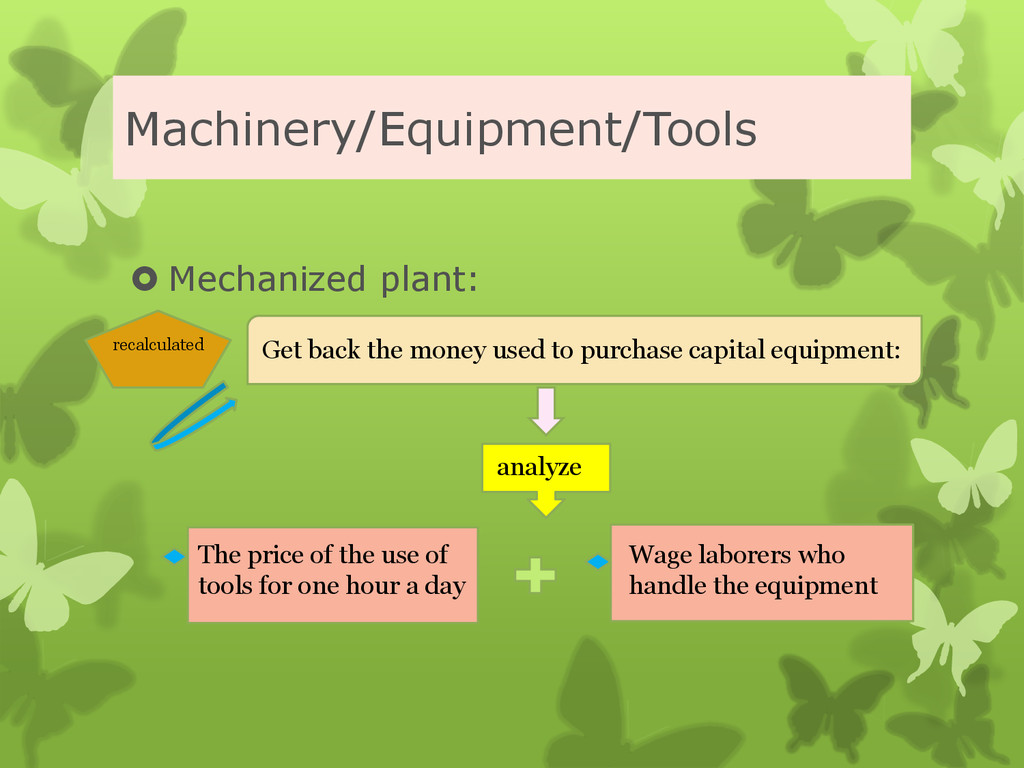

these devices should be recalculated to obtain the cost of capital has been issued. How to get back the money used to purchase capital equipment ? It must:

rented: • Include the machinery, driver and fuel. Personal machinery – buy, loan Cost incurred by the contractor are: • Cost depletion for each machinery until it sale by second hand cost.

is: To manage and administer the staff and the office equipment. • the rate of expenditure incurred by the company • Salaries • Allowance • & other payment to the staff: overtime, bonus, etc

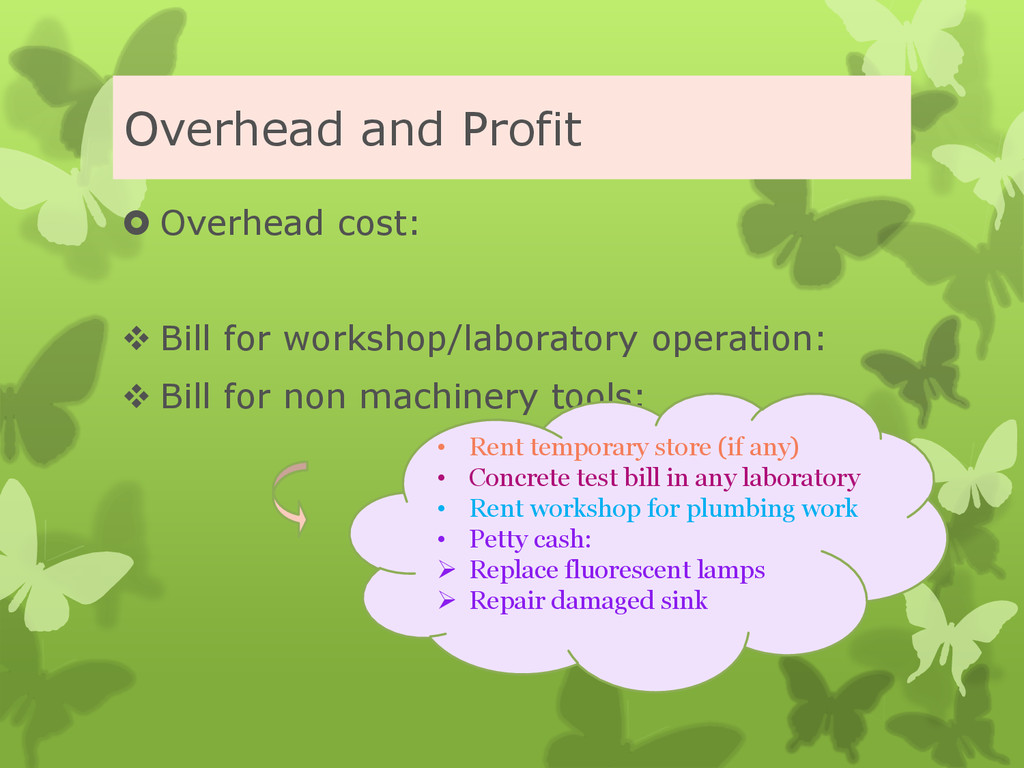

operation: Bill for non machinery tools: • Rent temporary store (if any) • Concrete test bill in any laboratory • Rent workshop for plumbing work • Petty cash: Replace fluorescent lamps Repair damaged sink

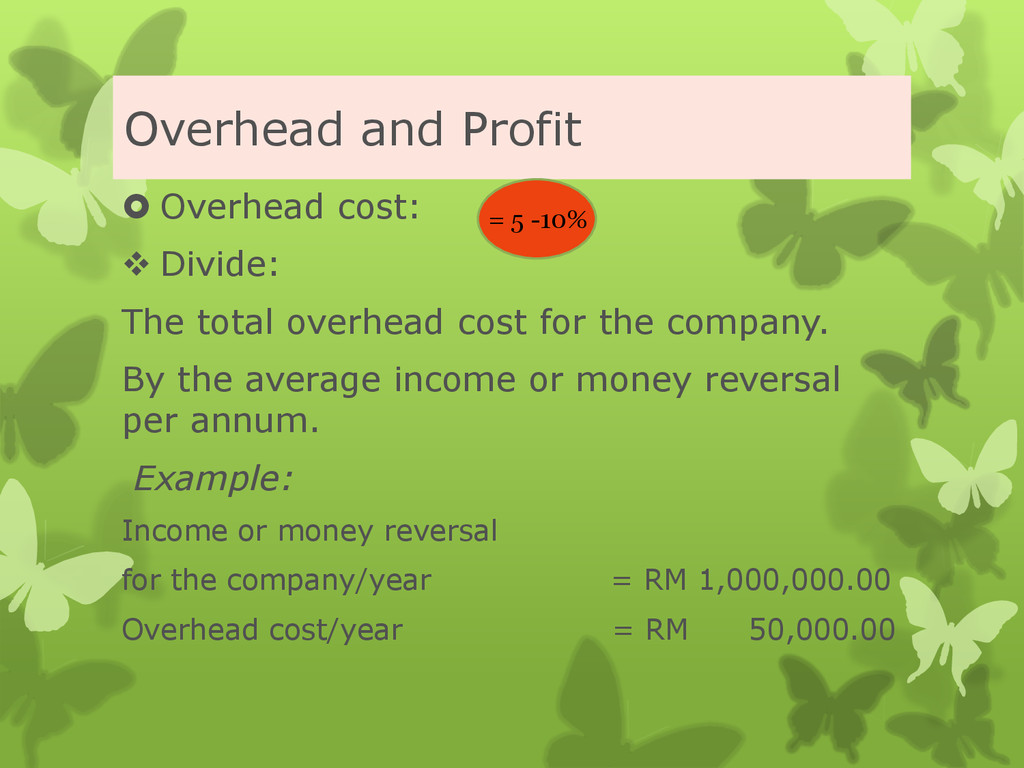

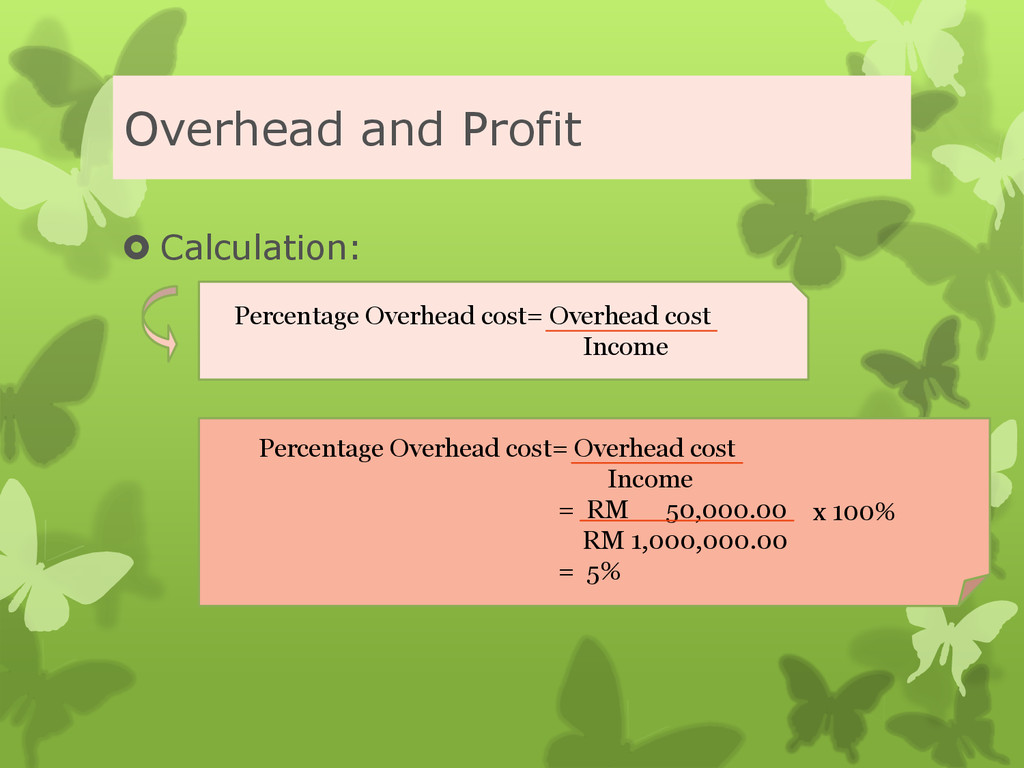

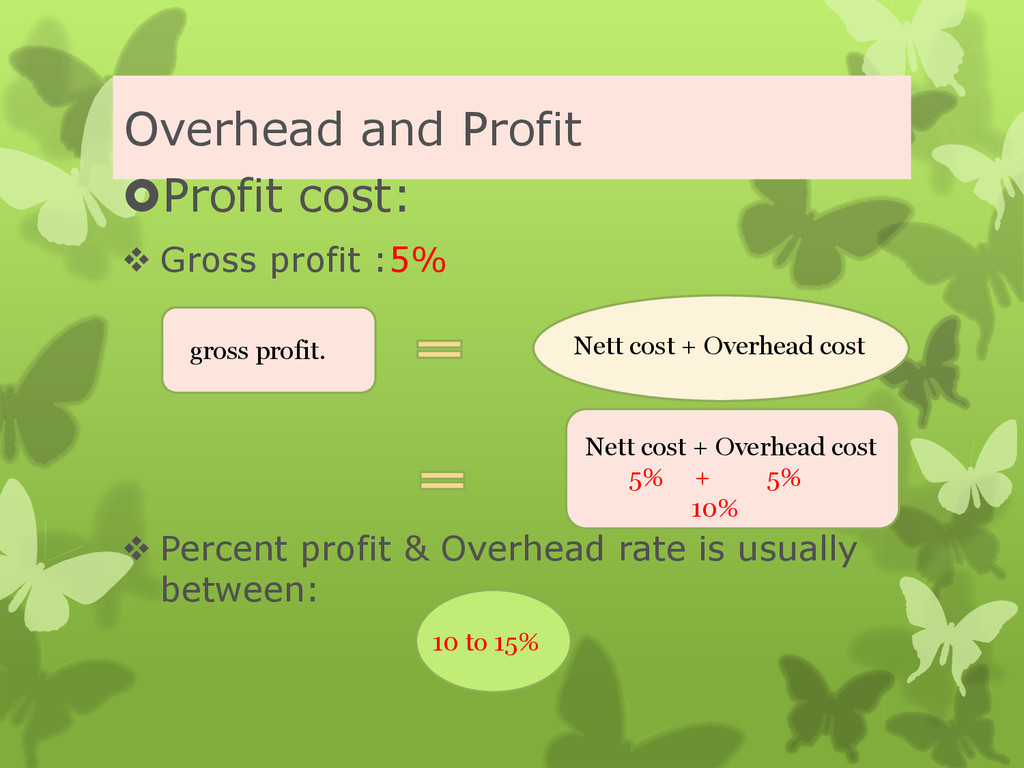

overhead cost for the company. By the average income or money reversal per annum. Example: Income or money reversal for the company/year = RM 1,000,000.00 Overhead cost/year = RM 50,000.00 = 5 -10%

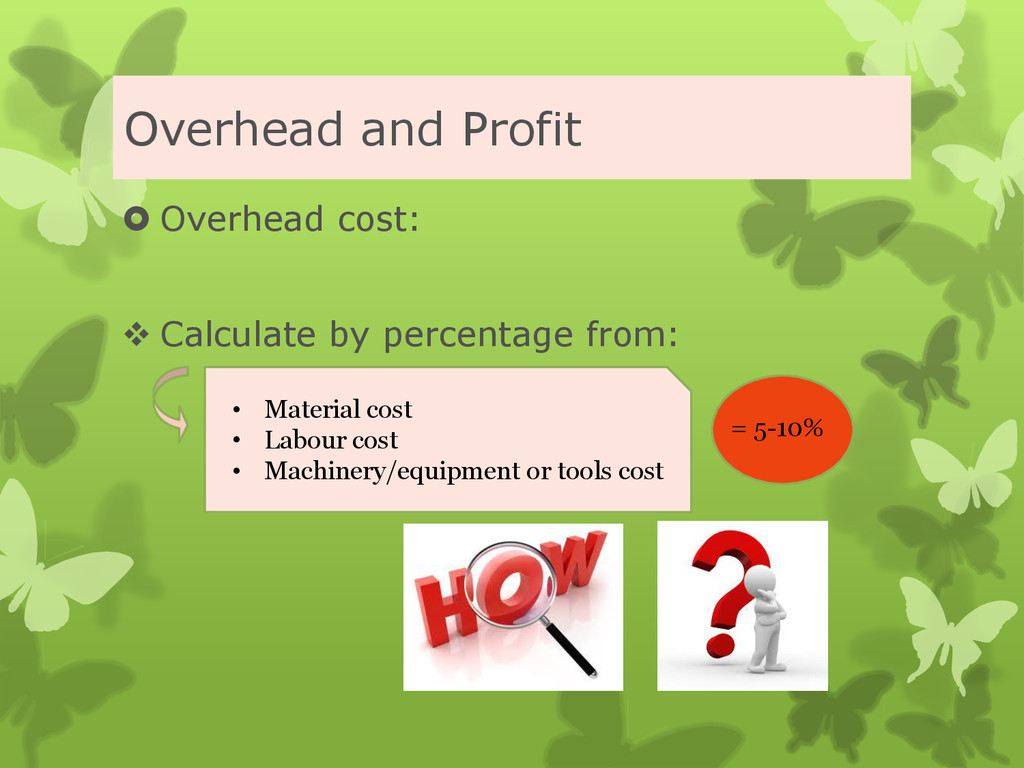

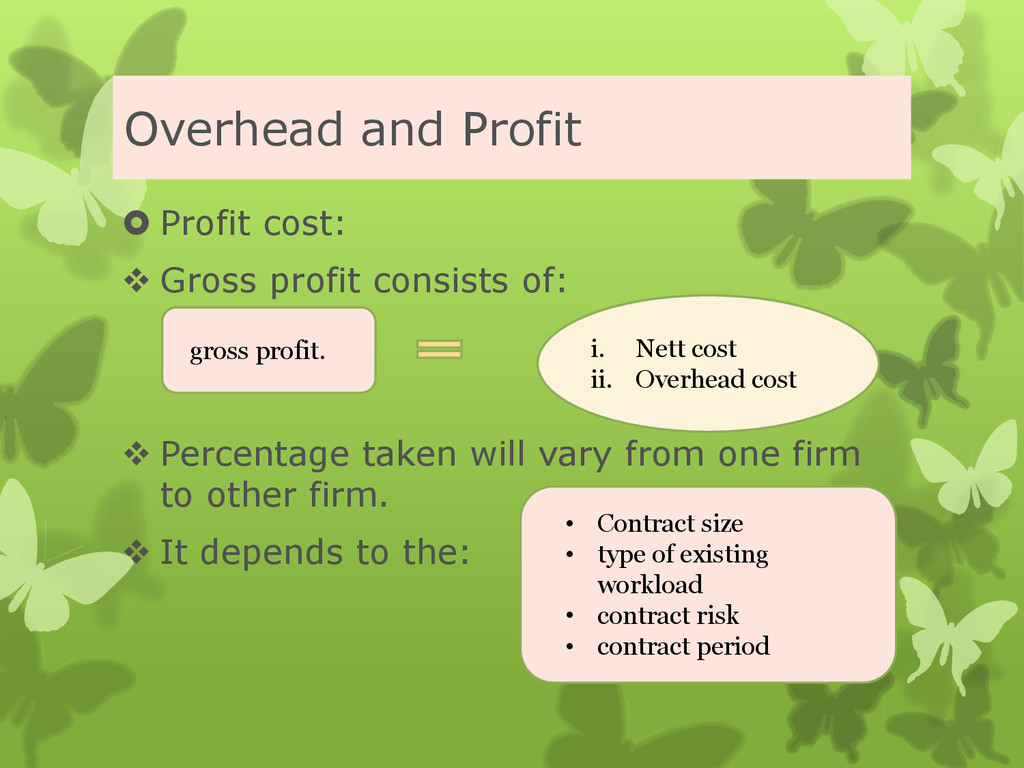

of: Percentage taken will vary from one firm to other firm. It depends to the: i. Nett cost ii. Overhead cost gross profit. • Contract size • type of existing workload • contract risk • contract period

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}